- Can I Still Get a Mortgage Even if I Lie on My Application?

- What Constitutes Lying on a Mortgage Application?

- What Are the Penalties for Lying on a Mortgage Application in the UK?

- Categories of Mortgage Fraud

- Why Do People Lie on Mortgage Applications?

- Can Lenders Detect False Information?

- What Should You Do If You’ve Already Lied on Your Application?

- Do You Have to Declare Dependents on a Mortgage Application?

- What Are Better Alternatives to Lying?

- What Should You Not Tell a Mortgage Lender?

- The Bottom Line

Is Lying on a Mortgage Application Illegal in the UK?

Applying for a mortgage is a big step, but you might be tempted to bend the truth to improve your chances.

Before you go down that path, understand the consequences. Lying on a mortgage application in the UK isn’t just unethical—it’s illegal.

Let’s look at why it’s a bad idea and what can happen if you’re caught.

Can I Still Get a Mortgage Even if I Lie on My Application?

Trying to lie on your mortgage application is a bad idea. It’s illegal and very unlikely to work.

Mortgage lenders in the UK thoroughly check everything from your salary to your personal details.

They’ll expect proof you qualify and will scrutinise your application throughout the process. Even if you slip past the first hurdle, they’ll likely catch your deception later on.

The consequences of lying on your application are severe. You’ll be denied the mortgage if they find any false information.

Mortgage fraud is a crime, and you could face fines or even jail time. Plus, getting caught lying will damage your credit score and make it difficult to get any loans in the future.

The best approach is to be honest and provide accurate information. If you’re worried about qualifying for a mortgage, talk to a mortgage broker. They can help you find suitable options based on your true financial situation.

What Constitutes Lying on a Mortgage Application?

Lying on a mortgage application means giving false information about your finances, job, and life situation.

Here’s how people try to cheat the system:

Income falsification

Exaggerating your income or providing false payslips. Some believe they don’t earn enough to get a mortgage, but lenders will flag this in background checks.

A good broker can help find a suitable mortgage for you, considering supplemental income and high-income multiples.

Employment misrepresentation

Lying about your job status or employer. This includes falsely claiming to be employed when you’re not, exaggerating your job title or responsibilities, or providing fake employment details.

Lenders verify your employment through various means, including contacting your employer directly.

Misrepresenting this information can lead to your mortgage application being denied and might also damage your credibility with other lenders.

Debt omission

Failing to disclose existing debts or credit issues. Hiding credit cards or other debts will eventually be uncovered by the lender.

Reliable brokers can help those with credit issues find a suitable mortgage.

First-time buyer status

Falsely claiming to be a first-time buyer when you’ve owned property before. Banks can check if you’ve been a homeowner, even overseas.

Misrepresentation here can result in your mortgage being withdrawn.

Dependent non-disclosure

Not declaring dependents who rely on your income. Some lenders use discretion regarding dependents.

Be transparent about any child support you’re receiving; this might work in your favour. Honesty is crucial to avoid disqualification and ensure you get a mortgage amount you can realistically afford.

Marital status deception

Hiding your marital status or your spouse’s financial situation. You don’t need to take out a joint mortgage just because you’re married.

Brokers can explain options, including joint borrower and sole proprietor agreements.

Property misrepresentation

Providing false information about the property you’re buying, such as its condition, value, or your intended use.

Lenders will conduct their own property assessments and appraisals, and discrepancies can lead to loan denial.

Forgery

Submitting forged documents, such as fake bank statements, tax returns, or identification, is a serious offence.

Lenders have rigorous verification processes, and forgeries will be detected, leading to legal consequences.

Any of these actions can be considered mortgage fraud, which is a serious offence under UK law.

Always be honest and transparent in your application to avoid severe consequences.

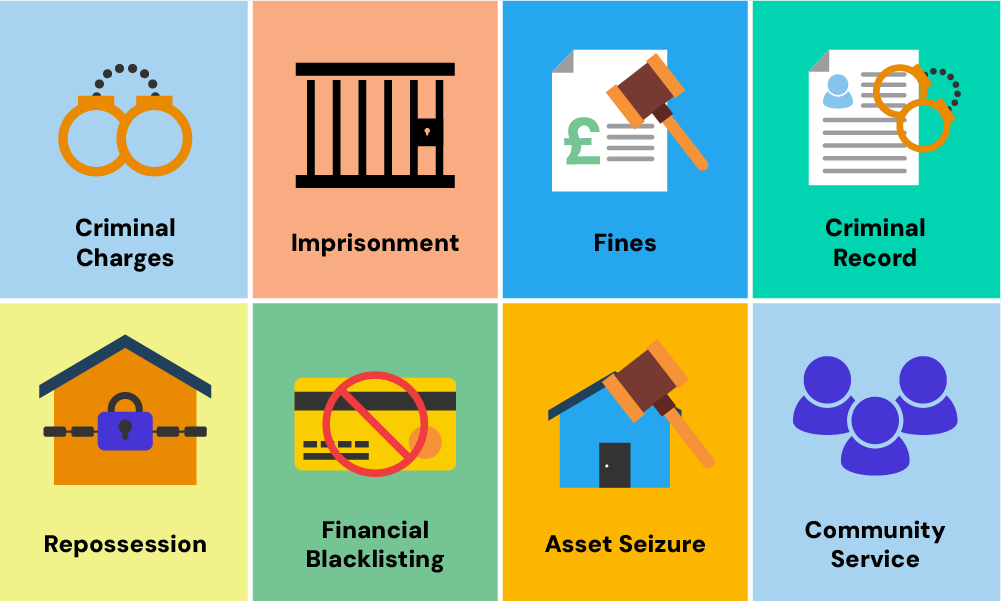

What Are the Penalties for Lying on a Mortgage Application in the UK?

If you’re caught lying on a mortgage application in the UK, the consequences can be severe.

The penalty for lying on a mortgage application UK can include:

- Criminal Charges. Mortgage fraud is a criminal offence. If you enter false or misleading information knowingly, you could face imprisonment for up to 10 years, pay unlimited fines, or both.

- Imprisonment. Serious cases of mortgage fraud can result in up to 10 years in prison.

- Fines. Courts can impose unlimited fines for mortgage fraud.

- Criminal Record. A conviction will stay on your record, affecting future employment and financial opportunities.

- Repossession. If the mortgage was obtained fraudulently, your home could be repossessed.

- Financial Blacklisting. You may find it extremely difficult to obtain credit or financial products in the future. Mortgage fraud often results in an automatic disqualification from future borrowing.

- Asset Seizure. In severe cases, authorities may seize your assets as part of the penalty.

- Community Service. You might be required to perform community service.

The severity of the punishment often depends on the scale and nature of the fraud.

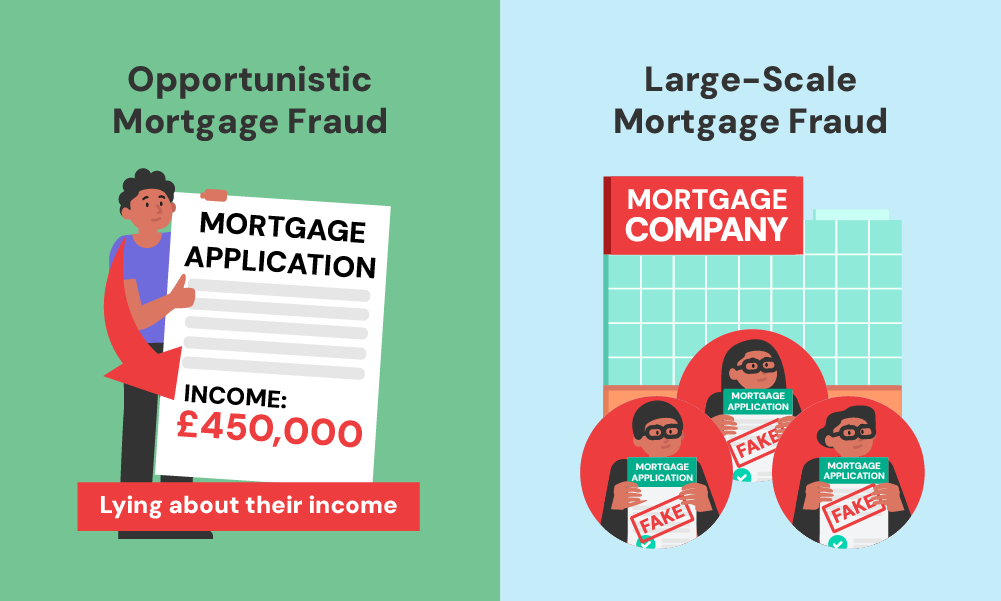

Categories of Mortgage Fraud

Mortgage fraud falls into two main categories: opportunistic and large-scale.

- Opportunistic Mortgage Fraud. This type is usually committed by individuals who lie about their income, employment, or other factors to borrow more money and acquire property. It’s treated seriously, but penalties may be lighter compared to large-scale fraud.

- Large-Scale Mortgage Fraud. This involves organised crime and money laundering through property transactions. It’s often carried out by those with industry knowledge. Penalties are stricter due to its broader impact and connections to organised crime.

Even small falsifications can lead to severe legal consequences and long-term damage to your financial credibility.

Why Do People Lie on Mortgage Applications?

Despite the risks, some people are tempted to lie on their mortgage applications.

Common reasons include:

- Fear of rejection. Believing they won’t qualify based on their actual circumstances.

- Desire for a larger loan. Hoping to borrow more than they’d qualify for honestly.

- Hiding past financial mistakes. Attempting to conceal credit issues or previous property ownership.

- Misunderstanding the process. Some may not realise the seriousness of providing false information.

- Seeking Favourable Terms. Omitting or lying about income and employment details to get better mortgage terms or interest rates.

- Industry Fraud. Sometimes, industry professionals might lie about a client’s financial information to maximise profits from the transaction.

While these motivations are understandable, they don’t justify the risks and potential consequences of lying.

Can Lenders Detect False Information?

You might wonder if you can get away with lying on a mortgage application. The short answer is: probably not.

Lenders have sophisticated methods to verify the information you provide:

- Credit checks. These reveal your financial history, including debts and credit issues.

- Employment verification. Lenders often contact employers directly to confirm job status and income.

- Bank statement analysis. Your spending habits and income sources are scrutinised.

- HMRC checks. Some lenders use the Mortgage Verification Scheme to cross-reference your details with HMRC records.

- Property ownership databases. These can reveal if you’ve owned property before, even abroad.

With these tools at their disposal, lenders are likely to uncover any discrepancies in your application.

What Should You Do If You’ve Already Lied on Your Application?

If you’ve submitted an application with false information, it’s crucial to act quickly:

- Contact the lender immediately to explain that you need to amend your application.

- Be honest about the mistake; admitting the error before it’s discovered can work in your favour.

- Provide correct information by submitting accurate details to replace the false ones.

- Seek professional advice by consulting a mortgage broker or financial advisor for guidance.

Taking these steps doesn’t guarantee you’ll avoid consequences, but it’s better than waiting for the lender to discover the falsehood.

Do You Have to Declare Dependents on a Mortgage Application?

A common question is whether you need to declare dependents when applying for a mortgage.

The answer is yes, you should.

Lenders need to know about dependents to accurately assess your outgoings, ensuring they act responsibly by offering a mortgage you can afford.

Withholding this information could be considered fraud. In some cases, declaring dependents might work in your favour, especially if you receive child support.

Remember, transparency is key in the mortgage application process.

What Are Better Alternatives to Lying?

Instead of resorting to falsehoods, consider these alternatives:

- Speak to a mortgage broker – They can help find lenders suited to your circumstances.

- Improve your financial situation – Work on boosting your credit score and saving for a larger deposit.

- Consider alternative mortgage products – Some lenders offer specialised mortgages for various situations.

- Be patient – If you’re not ready for a mortgage now, focus on improving your position for the future.

- Explore government schemes – Programs like the Mortgage Guarantee Scheme or shared ownership might be suitable.

These options might take more time, but they’re legal, and ethical, and won’t put you at risk of severe penalties.

What Should You Not Tell a Mortgage Lender?

Nothing. Always be completely honest with your mortgage lender.

Lying on a mortgage application is illegal. Be 100% transparent about your details, finances, and circumstances.

Hiding or falsifying information can lead to serious consequences, including charges of mortgage fraud.

Lenders verify everything you provide, and any discrepancies will be uncovered during their review.

Honesty ensures a smooth application process and helps you avoid legal and financial troubles.

Always provide accurate information to maintain your credibility and secure a mortgage successfully.

The Bottom Line

Lying on a mortgage application in the UK is a serious offence with potentially life-changing consequences. The risks far outweigh any perceived benefits.

Always be honest in your application, seek professional advice if you’re unsure, and remember that there are legal alternatives if you’re struggling to qualify for a mortgage.

Your integrity and financial future are worth more than any short-term gain from deception.

Instead of risking it all, consider using a whole-of-market mortgage broker to improve your chances of approval.

With a good broker, you gain:

- Access to a wider range of mortgage products

- Expert knowledge of the mortgage market

- Assistance with paperwork and documentation

- Tailored advice to suit your financial situation

- Faster and smoother application process

- Potential to secure better interest rates

- Support throughout the entire application process

Need a broker? Get in touch. We’ll pair you with a qualified mortgage broker to help with your mortgage application and get you the BEST deal.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What happens if I lie on my mortgage application?

Lying on your mortgage application is mortgage fraud in the UK, a serious criminal offence.

If caught, you face severe consequences: your application could be rejected, your loan could be recalled, and you could be fined or imprisoned. It also harms your credit score and future credit prospects.

Mortgage lenders have sophisticated methods to verify your information, so honesty is crucial to avoid these life-changing repercussions.

Do I have to disclose all bank accounts to a mortgage lender in the UK?

Yes, you must disclose all bank accounts to your mortgage lender in the UK.

Lenders need a full view of your finances to assess your loan repayment ability. This includes statements for all current, savings, and other accounts.

Hiding information can be seen as misleading and might lead to application rejection or legal consequences. Transparency builds trust and ensures a smoother application process.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]