- Can You Get a Mortgage with a Limited UK Address History?

- Why Do Lenders Care About Your Address History?

- How Much Address History Do You Need for a Mortgage?

- What If You’re New to the UK?

- Are There Specialist Mortgages for Non-UK Citizens?

- How To Improve Your Chances of Getting a Mortgage with Limited Address History?

- What Documents Will You Need for Your Mortgage Application?

- What To Do When I Need To Change My Address?

- The Pros and Cons of Applying for a Mortgage With Less than 3 Years in UK

- How To Deal with Address Discrepancies?

- What Are Your Next Steps?

- Key Takeaways

- The Bottom Line

Mortgages With Less Than 3 Years UK Address: What to Know

Your address history isn’t just a tally of your past homes; it’s a vital piece of your mortgage puzzle. It can influence your credit score and whether a lender gives you a thumbs up.👍

If you’re new to the UK and haven’t racked up three years of address history, don’t fret.

There are lenders who understand and are ready to help you step onto the property ladder.

Yes, it might require a bit more effort, but with the right knowledge and a bit of expert guidance, you could be jingling those new house keys before you know it.

In this article, we’ll dive into why your address history matters, the hurdles you might face, and some tips to boost your application.

Can You Get a Mortgage with a Limited UK Address History?

Most lenders require at least 3 years of UK address history, and some ask for more.

If you’ve been here for less, your options are limited — but a specialist broker may still help you find a lender willing to consider your full situation.

Let’s dive into what you need to know about mortgages and address history.

Why Do Lenders Care About Your Address History?

Your address history is more important than you might think when it comes to mortgage applications.

Lenders use this information for several reasons:

- Identity verification. Your address history helps lenders confirm who you are and where you’ve been living. This is crucial for preventing fraud and ensuring they’re lending to the right person.

- Credit history tracking. Your addresses are linked to your credit report. Lenders use this to trace your financial behaviour over time and assess your creditworthiness.

- Stability assessment. A stable address history can indicate to lenders that you’re settled and reliable, which may work in your favour.

- Risk evaluation. Multiple addresses in a short period might raise red flags for some lenders, as it could suggest instability.

Understanding these factors can help you see why lenders place such importance on your address history when considering your mortgage application.

How Much Address History Do You Need for a Mortgage?

As we mentioned, most UK lenders require a minimum of 3 years’ UK address history when assessing mortgage applications. This helps them verify your identity and track your credit record across multiple addresses.

While a few lenders may consider applicants with less than 3 years, these cases are rare and often depend on other strong factors like your income, credit profile, or deposit size.

There’s no universal rule, but less than 3 years of address history will significantly limit your mortgage options.

Some lenders may automatically decline your application, while others may only proceed through a mortgage broker who can present your case directly.

If you’re a returning UK expat or someone with a strong international financial background, you might still be considered — but it’s not guaranteed.

This is where a specialist broker becomes essential.

What If You’re New to the UK?

If you’re new to the UK, getting a mortgage can be more challenging, but it’s not impossible. Here’s what you need to know:

For EU citizens:

- You typically need to have been resident in the EU for more than three years

- You should have a UK bank account

- A permanent job in the UK is usually required

- Permanent residence rights or a UK Work Permit may be necessary

For non-EU citizens:

- You generally need to have been resident in the UK for more than two years

- A permanent job in the UK is typically necessary

- You should have permanent residence rights or a UK Work Permit

- A UK bank account is usually required

If you’re on a work permit, some lenders might prefer you to have at least two years remaining on it. However, others may be more flexible.

Remember, these are general guidelines. Each lender has their own criteria, which is why seeking professional advice can be so valuable when you’re in this situation.

Are There Specialist Mortgages for Non-UK Citizens?

Yes, there are specialist mortgages available for non-UK citizens. These are designed to cater to the unique circumstances of foreign nationals living in the UK.

These specialist mortgages often:

- Offer expert advice on mortgage finance over £100,000

- Assist with complex income scenarios

- Provide access to banks that offer non-UK citizen mortgage solutions

- Are available for both short and long-term lending options

If you’re a non-UK citizen looking for a mortgage, these specialist options could be worth exploring.

They’re often more flexible when it comes to addressing history requirements and understanding the unique challenges you might face.

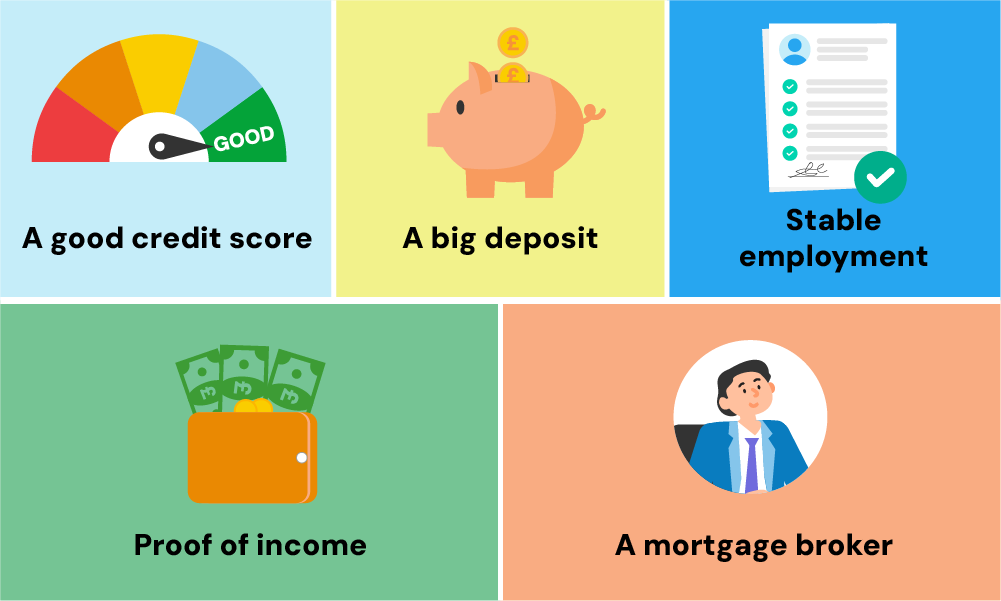

How To Improve Your Chances of Getting a Mortgage with Limited Address History?

While having a limited UK address history can make getting a mortgage more challenging, there are steps you can take to improve your chances:

- Build your credit score. A strong credit score can sometimes compensate for a limited address history. Make sure you’re on the electoral roll, pay bills on time, and consider getting a UK credit card to build your credit history.

- Save for a larger deposit. Some lenders may be more willing to overlook a limited address history if you have a substantial deposit. Aim for at least 25% if possible.

- Maintain stable employment. Having a permanent job in the UK, especially if you’ve been with the same employer for at least 6 months, can work in your favour.

- Use a specialist mortgage broker. They can guide you to lenders more likely to consider your application and help you navigate the process.

- Be prepared with documentation. Gather all necessary documents, including proof of income, bank statements, and any documentation related to your right to live and work in the UK.

- Consider a guarantor. If possible, having a UK resident as a guarantor might make some lenders more comfortable with your application.

Remember, every little bit helps when you’re trying to secure a mortgage with limited UK address history.

What Documents Will You Need for Your Mortgage Application?

When applying for a mortgage, especially with limited UK address history, you’ll need to provide various documents. These typically include:

- Proof of identity (passport or driving licence)

- Proof of address (utility bills, bank statements)

- P60 form and recent payslips

- Bank statements for the past 3-6 months

- Details about the property you’re looking to buy

- Information about your estate agent and solicitor

If you’re self-employed, you might need to provide 2-3 years of accounts. For non-UK citizens, you’ll likely need to show your visa or right to remain in the UK.

It’s crucial to ensure all information matches across your documents. Lenders are likely to scrutinise your application more closely if you have a limited address history, so accuracy is key.

What To Do When I Need To Change My Address?

If you need to change your address during a mortgage application, tell your lender immediately.

Any differences between your current address and the one on your application can cause delays or even a denial.

Keeping your lender updated makes sure your application stays accurate and moves smoothly.

To avoid problems:

- Inform your lender right away.

- Provide proof of your new address.

- Update your credit report.

The Pros and Cons of Applying for a Mortgage With Less than 3 Years in UK

Applying for a mortgage with less than 3 years of UK address history has both upsides and downsides. Here’s a simple breakdown:

Pros:

- Access to specialist lenders who focus on helping people with limited address history.

- Building credit and address history over time by securing a property.

- Potential eligibility for government schemes to help first-time buyers or those with limited credit history.

- Getting onto the property ladder faster.

Cons:

- Fewer lenders may consider your application.

- Higher interest rates due to perceived risk.

- Stricter documentation and verification requirements.

- Larger deposits may be required by some lenders.

- Slower approval process due to extra checks and verifications.

- Higher likelihood of additional fees because of the higher risk.

How To Deal with Address Discrepancies?

If there are mistakes or gaps in your address history, fix these issues before applying for a mortgage. Here’s how to handle it:

- Gather proof – Collect utility bills, bank statements, or rental agreements showing your previous addresses.

- Update records – Send these documents to credit agencies to correct your address history.

- Explain gaps – Be ready to explain any missing address periods to your lender.

If your application is declined due to address discrepancies, consult a mortgage broker. They can help you find lenders with easier requirements and help you correct mistakes before you reapply.

What Are Your Next Steps?

If you’re looking to get a mortgage with less than 3 years in the UK or limited address history, your first step should be to speak with a specialist mortgage broker. They can:

- Assess your circumstances

- Guide you to lenders more likely to consider your application

- Help you understand what documentation you’ll need

- Advise you on how to strengthen your application

Remember, while getting a mortgage with limited UK address history can be challenging, it’s not impossible.

With the right guidance and preparation, you can increase your chances of securing the mortgage you need to buy your home in the UK.

Key Takeaways

- Most lenders require at least 3 years of UK address history — some may require more.

- Having less than 3 years doesn’t automatically disqualify you, but it makes approval harder and limits your lender options.

- Address history is used to verify your identity, track your credit history, and assess financial stability.

- A mortgage broker can help you find specialist lenders who are more open to limited address histories — especially if you have a strong deposit or income.

- The more documentation, stability, and proof of creditworthiness you can provide, the stronger your application will be.

The Bottom Line

Don’t let a limited address history discourage you from pursuing your dream of homeownership in the UK.

While it may present some challenges, there are options available.

One smartest moves you can make is to work with a good mortgage broker. They:

- Have access to many lenders, including those specialising in non-UK citizen mortgages.

- Offer tailored advice based on your financial situation.

- Assist with complex income scenarios and credit history requirements.

- Connect you with lenders who understand the challenges newcomers face.

- Help with paperwork and strengthen your application.

- Negotiate to get you the best rates and terms.

With their help, you can focus on what matters to you.

If you need a good broker, simply contact us. We’ll instantly connect you with the right mortgage broker who can help with your mortgage application.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

How much can I borrow if I have less than 3 years of address history in the UK?

The amount you can borrow with less than 3 years of address history in the UK depends on several factors, including your income, credit score, and the lender’s criteria.

Generally, lenders may offer loans up to 4-5 times your annual salary.

However, with a limited address history, some lenders might consider you a higher risk and offer lower loan amounts or higher interest rates.

Working with a mortgage broker can help you find lenders who are more flexible with their requirements.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]