- What Is a Multi-Applicant Mortgage?

- How Many People Can Be on a Mortgage?

- Who Is Eligible?

- Can 3 People Buy a House Together?

- How Does a 3-Person Mortgage Work?

- How Much Can You Borrow for a Multi-Person Mortgage?

- Which Lenders Offer 3-Applicant Mortgages?

- What Are the Pros and Cons of a Multi-Person Mortgage?

- Things To Consider Before Applying for a Multi-Applicant Mortgage

- How To Apply for a Multi-Applicant Mortgage?

- Alternatives To Multi-Person Mortgage

- Key Takeaways

- The Bottom Line

What You Must Know To Get a Mortgage with 3 or 4 People

Rising house prices, strict lending rules, and high living costs—any one of these might be the reason you’re struggling to buy your first home.

But there’s a solution that’s gaining popularity: mortgages with multiple applicants.

This lets you team up with your best mates to apply for a mortgage and buy a house together.

On paper, it sounds ideal—shared expenses and increased buying power. Unfortunately, lenders will scrutinise each of you with equal intensity.

Any hiccup in one applicant’s financial history, credit score, or income can jeopardise the entire application.

That’s why in this guide, we’ve explained how this mortgage works, who can apply, and the pros and cons to consider before you apply. With helpful tips on how to ace your mortgage application 😀.

Whether you’re a first-time buyer, or looking to move, this guide can help.

What Is a Multi-Applicant Mortgage?

A multi-applicant mortgage, also known as a together mortgage or multiple-person mortgage, is a home loan shared between more than two people.

This mortgage type lets you combine your financial resources with friends or family members to increase how much you can borrow and make homeownership more affordable.

How Many People Can Be on a Mortgage?

Typically, most UK lenders allow up to 4 people to be on a mortgage.

However, some lenders have stricter rules and might only accept applications from two or three people.

The number of applicants a lender considers will depend on their own criteria and the relationship between the applicants themselves.

For instance, some lenders may be more willing to accept multiple applicants if they’re all family members.

Who Is Eligible?

Similar to a standard mortgage criteria, to qualify, you need:

- A good credit score

- Proof of stable income

- Steady employment (extra documents needed if you’re self-employed)

- A deposit of at least 5%-20% of the property’s value

- A low debt-to-income ratio (use this calculator to check yours)

- Legal right to live in the UK (some lenders have restrictions for non-UK residents)

- To meet the lender’s age and property criteria

As discussed, most lenders prefer applicants with clear relationships, like partners, family members, or close friends, for a stable living arrangement.

They’ll check each applicant’s financial history, including past bankruptcies, defaults, or significant debts.

You and your partners must agree to be jointly responsible for the mortgage payments. If one person misses a payment, the others must cover the shortfall.

Can 3 People Buy a House Together?

Yes, three people can buy a house together in the UK.

This option, often called a “three-person mortgage,” is growing in popularity, especially among young professionals and friends who want to combine their resources.

Buying with three people means everyone is on the deed and shares the mortgage responsibility. This can make homeownership more achievable, as you can pool your income and savings for a bigger deposit and potentially a nicer property.

However, it’s important to think about the long term. You’ll need to have open discussions about what happens if someone wants to sell their share or move out.

To avoid future arguments, a legal agreement outlining everyone’s rights and responsibilities is a good idea.

How Does a 3-Person Mortgage Work?

A 3-person mortgage works similarly to a standard mortgage but with a few key differences.

When you apply for a 3-person mortgage, the lender will assess the financial situation of all three applicants. This includes looking at your income, credit histories, and existing debts.

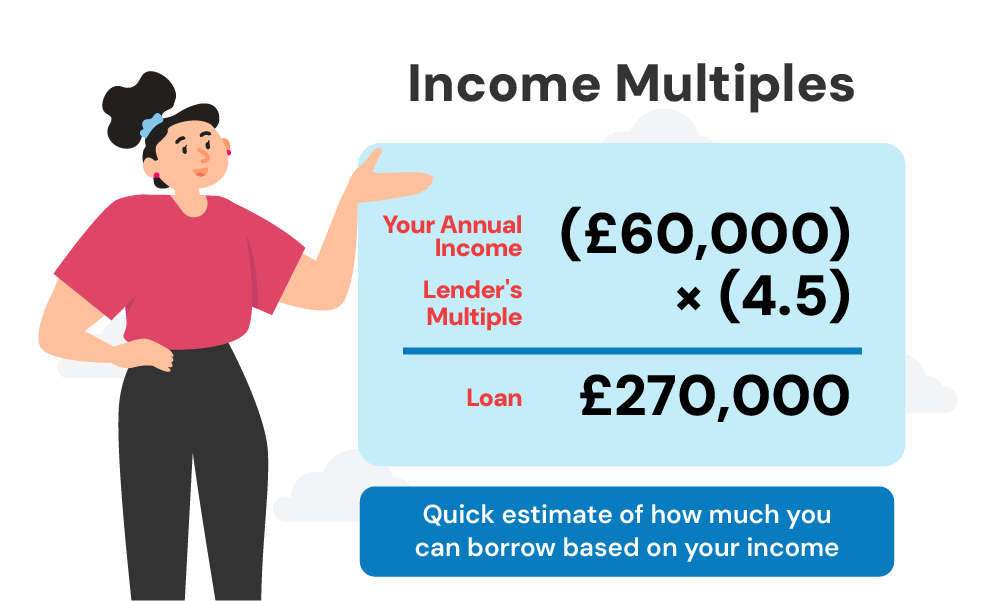

A big perk of this option is the chance to borrow more. Many lenders use income multiples to figure out how much you can borrow.

So, if a lender offers 4.5 times your annual salary, combining three incomes can significantly boost your borrowing power.

However, be aware that not all lenders consider all three incomes when calculating affordability.

Some might only take the two highest incomes into account. So, it pays to shop around or use a mortgage broker to find the best deal for your situation.

How Much Can You Borrow for a Multi-Person Mortgage?

Figuring out how much you can borrow with a multi-person mortgage can be trickier than a standard one.

There’s no one-size-fits-all calculator, but you can estimate what you might be able to borrow.

Most lenders use a system based on income multiples. This means they multiply your combined annual income (or the two highest incomes if that’s their rule) by a number, typically between 4 and 4.5.

Here’s a quick way to get a rough idea:

- Add up everyone’s annual income (or just the two highest if that applies).

- Multiply that total by the lender’s income multiple (e.g., 4 or 4.5).

For example, if three applicants earn £30,000, £35,000, and £40,000 respectively:

- Total income: £105,000

- Potential borrowing at 4.5x income: £472,500

Remember, this is just an estimate.

Lenders will also consider your credit histories, existing debts, and regular outgoings when determining how much they’re willing to lend.

Use our mortgage affordability calculator to see how much you can afford for a mortgage.

Which Lenders Offer 3-Applicant Mortgages?

Finding a lender that offers 3-applicant mortgages can be a bit trickier than securing a standard mortgage, but don’t worry – options do exist.

Some of the UK lenders known to consider 3-person mortgage applications include:

- Barclays

- Metro Bank

- Leeds Building Society

- Teachers Building Society

- Skipton Building Society

Each lender has its own requirements and treats multi-applicant mortgages differently.

For example, Barclays might allow four applicants but only consider the two highest incomes for affordability.

Metro Bank, on the other hand, might take everyone’s income into account.

It’s important to note that lender policies can change, and some may only offer these products through mortgage brokers.

Because of this, it’s often a good idea to work with a specialist broker who understands multi-applicant mortgages.

What Are the Pros and Cons of a Multi-Person Mortgage?

Like any financial decision, taking out a multi-person mortgage comes with its own set of advantages and disadvantages.

Let’s break them down:

Pros:

- More bang for your buck. Combining incomes means you can potentially afford a nicer property or get a better interest rate.

- Larger deposit. Pooling your savings can result in a larger deposit, which could lead to better mortgage terms.

- Shared responsibilities. Sharing mortgage repayments and property upkeep makes things more manageable financially.

- Get on the ladder faster. Especially for first-time buyers, a multi-person mortgage can open the door to homeownership sooner.

Cons:

- Joint liability. All applicants are equally responsible for the mortgage. If one person can’t pay their share, the others must cover it.

- Complexity. More people means more paperwork and potentially more complicated negotiations.

- Future complications. Job changes, and breakups – can make things complicated down the line.

- Credit score implications. Your credit score could be affected by your co-applicants’ financial behaviour.

- Selling difficulties. Decisions about selling need everyone’s agreement, which can be an issue if people disagree.

Things To Consider Before Applying for a Multi-Applicant Mortgage

Before you jump into a multi-applicant mortgage, there are some key things to think through:

- Trust and reliability. You’re in this for the long haul with these people. Make sure you trust them completely and that they’re responsible with money.

- Exit strategy. What happens if someone wants out? Will the others buy them out or will you sell the property? Discuss this beforehand.

- Legal structure. Decide how you’ll own the property: joint tenants or tenants in common. This impacts inheritance if someone dies.

- Contributions. Agree on how much each person will contribute to the deposit, monthly payments, and maintenance costs.

- Decision making. How will you decide on things like renovations or selling the property? Establish a plan upfront. Make sure to also agree on how changes in your lives (new jobs, relationships, children) might affect the arrangement.

- Professional advice. It’s wise to seek legal advice and potentially draw up a cohabitation agreement to protect everyone’s interests.

How To Apply for a Multi-Applicant Mortgage?

Applying for a multi-applicant mortgage follows a similar process to a standard mortgage application, but with a few additional steps:

1. Sort out your finances

Start by checking your credit reports and fixing any issues you find. All applicants need to ensure their credit is in good shape.

Next, agree on how much each person will contribute to the deposit and begin saving.

Make sure everyone is clear on their financial responsibilities to avoid any surprises.

2. Gather documents

Each applicant will need to provide proof of income, bank statements, and identification. Here’s a list of what lenders usually ask for:

- Proof of income (payslips, P60s, accounts if self-employed, tax returns, etc.)

- Proof of affordability (3+ months of bank statements)

- Details of bonuses or commissions

- Proof of deposit source (savings, gift letter if family helped, etc.)

- Proof of identity (passport, driving licence)

- Proof of address (utility bills, bank statements)

- Details of any debts, loans, or credit commitments

- College transcripts (if recently graduated)

- Property cost breakdown

- Hired conveyancer or solicitor details

- Divorce or separation paperwork (if applicable)

- Shared ownership agreements that show ownership percentages & responsibilities (If applicable)

3. Get an agreement in principle

An Agreement in Principle (AIP) gives you an idea of how much you could borrow.

Start by contacting a lender or mortgage broker. They’ll check your financial situation, including income, expenses, credit history, and employment status.

Provide basic information and documents like proof of income and identification. The lender will perform a credit check and evaluate your affordability.

If everything checks out, they will issue an AIP, stating the amount they are willing to lend you.

An AIP is valid for 30-90 days, so keep this timeframe in mind during your property search.

Note that the lender’s credit check might be a hard inquiry, which can temporarily affect your credit score.

While an AIP is not a mortgage guarantee, it helps you understand your borrowing potential and streamlines the home-buying process.

4. Find a property

Once you’ve got an agreement in principle, it’s time to start house hunting. Make sure the property meets everyone’s needs and preferences.

Have a chat about your budget and the type of property you’re after to keep things smooth.

5. Make a full application

When you’re ready, submit your full mortgage application with all the necessary documents.

This includes proof of income, bank statements, identification, and any details of debts.

Each of you will need to provide your financial information. The lender will then look at your combined finances to see if you qualify for the mortgage.

6. Get a solicitor

You’ll need a solicitor to handle the legal side of things, like property searches and contracts.

If you’re buying with others, it’s wise to get the solicitor to draw up a cohabitation agreement.

This will set out everyone’s rights and responsibilities, including what happens if someone wants to sell their share.

7. Complete the purchase

Once your mortgage is approved and all the checks are done, you can finalise the purchase of your new home. This means signing the contract, transferring the deposit, and setting a completion date.

Your solicitor will take care of transferring the funds and registering the property in all your names.

Then, you can move into your new home and start your new chapter together.

Alternatives To Multi-Person Mortgage

If a multi-person mortgage doesn’t fit the bill, here are a few other options you might consider:

- Guarantor Mortgage. One person takes out the mortgage, but a guarantor (usually a family member) agrees to cover the payments if the borrower can’t. This is handy if one of you has a weaker financial profile.

- Joint Borrower, Sole Proprietor Mortgage (JBSP). Multiple people can be on the mortgage, but only one person owns the property. This is ideal if a parent wants to help their child get on the property ladder without owning part of the home.

- Shared Ownership. Buy a share of a property (between 25% and 75%) and pay rent on the remaining share. This can make it easier to afford your first home.

- Co-ownership. Rather than a traditional mortgage, you and your co-buyers can pool your resources to buy a property outright. This requires significant upfront cash but saves on mortgage interest and repayments.

- Family Offset Mortgage. Family members can use their savings to offset the mortgage, reducing the amount of interest payable. This can make the mortgage more affordable for the main borrower.

- Renting Together. Instead of buying, you might consider renting a property together. This avoids the long-term commitment and financial responsibility of a mortgage while still allowing you to live together.

Key Takeaways

- You can get a mortgage with 3 or 4 people to boost your borrowing power and split the costs.

- A multi-applicant mortgage helps you afford a nicer property, but everyone is responsible for the payments.

- Make sure you have a legal agreement that clearly outlines each person’s rights and responsibilities

The Bottom Line

Multi-applicant mortgages are a great option to break into today’s tough property market. But there are things to consider and potential problems to avoid.

A whole-of-market mortgage broker specialising in multi-applicant mortgages can help you sort through these issues. They’ll provide personalised advice and open doors to a wide range of lenders.

Need a good broker? Contact us and we’ll connect you with a qualified mortgage broker to help you secure your mortgage.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can you add a third person to a mortgage?

Yes, adding a third person to your mortgage is possible. Most lenders accept up to four applicants on a single mortgage.

This can boost your combined income, potentially allowing you to borrow more. But there’s a catch: all applicants need to pass the lender’s checks, including credit scores, income proof, and affordability assessments.

Remember, everyone involved will be on the hook for repayments, and late payments can damage everyone’s credit score.

To avoid any confusion, having a legal agreement outlining each person’s responsibilities and ownership stake is a smart move.

Talking to a mortgage broker and a solicitor can help make the process smooth sailing.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]