- How Much Are Your £500,000 Mortgage Repayments?

- How Much Do You Need to Earn to Get a £500,000 Mortgage?

- How Much Deposit Do I Need for a £500,000 House?

- What Factors Affect How Much a £500,000 Mortgage Costs?

- What Other Costs Should You Consider with a £500,000 Mortgage?

- How to Get a £500,000 Mortgage Approved

- Key Takeaways

- The Bottom Line

£500,000 Mortgage Repayments: How Much Will You Pay?

If you’re considering a £500,000 mortgage, you probably have a lot of questions—like what your monthly repayments might be or how much you need to earn to qualify.

In this guide, we’ll explain the costs, factors that influence repayments, and everything else you need to know to make an informed decision.

By the end, you’ll feel more confident about taking the next step towards buying your dream home.

How Much Are Your £500,000 Mortgage Repayments?

It’s important to note that your monthly repayments will vary depending on a few different factors: your mortgage term, interest rate, and the type of mortgage interest rate you go for.

For a typical repayment mortgage (where you’re repaying both the interest and the capital), let’s say you’ve got a 25-year term at an interest rate of 5%.

Based on this rate, you’re looking at around £2,923 per month.

But a longer term (say, 30 or even 35 years) will help bring that monthly payment down, even though you’ll end up paying more interest overall.

If you’re curious about an interest-only mortgage, things change a little.

Here, your monthly payments would be considerably less—at 5%, you’d pay roughly £2,083 per month.

But remember, with interest-only mortgages, you’re not actually reducing the size of the mortgage itself until the end of the term.

You’ll need to have a plan in place to pay back that hefty £500,000 eventually.

Use a mortgage calculator to get a clearer picture of what your monthly payments might look like, depending on the term and rate you choose.

For clarity, here’s an example of how your monthly payments are calculated for a £500,000 mortgage:

| Mortgage Term | 2% Rate | 3% Rate | 4% Rate | 5% Rate | 6% Rate | 7% Rate |

|---|---|---|---|---|---|---|

| 5 years | £8,764 | £8,984 | £9,208 | £9,436 | £9,666 | £9,901 |

| 10 years | £4,601 | £4,828 | £5,062 | £5,303 | £5,551 | £5,805 |

| 15 years | £3,218 | £3,453 | £3,698 | £3,954 | £4,219 | £4,494 |

| 20 years | £2,529 | £2,773 | £3,030 | £3,300 | £3,582 | £3,876 |

| 25 years | £2,119 | £2,371 | £2,639 | £2,923 | £3,222 | £3,534 |

| 30 years | £1,848 | £2,108 | £2,387 | £2,684 | £2,998 | £3,327 |

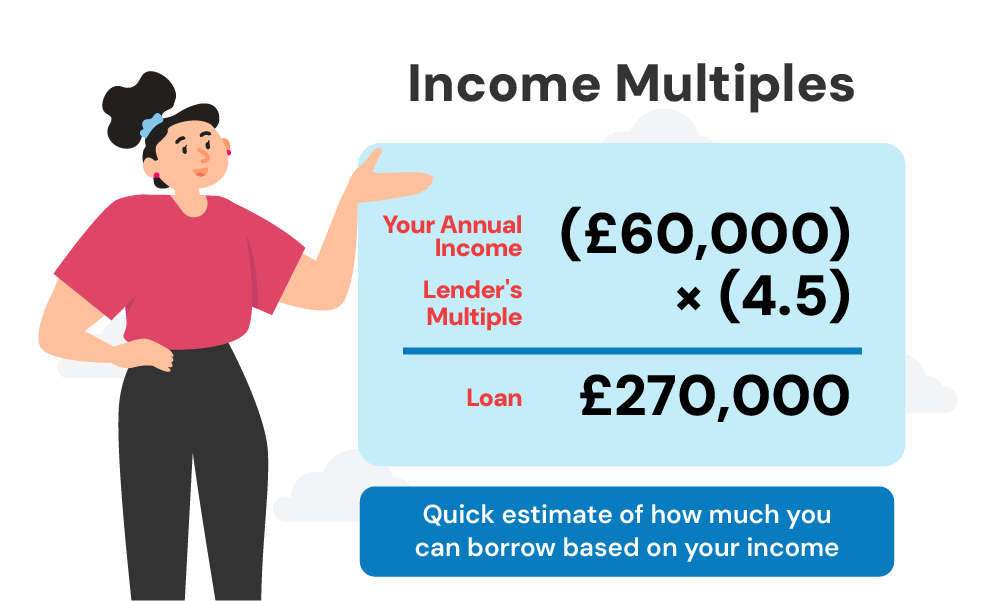

How Much Do You Need to Earn to Get a £500,000 Mortgage?

To get a mortgage on a 500k house, you’ll need to prove you can afford those monthly payments—and lenders generally use a salary multiple to work that out.

Most lenders will let you borrow around 4 to 4.5 times your income, which means you’re looking at needing an annual salary of between £111,000 and £125,500.

If you’re teaming up with your partner to buy, that combined income can help push you closer to your goal. And if you’re in a high-earning profession, like being a doctor or a lawyer, some lenders might even stretch to 5 or 6 times your income.

In some cases, lenders may offer different income multiples based on factors like job stability and future income potential, so it’s always worth speaking to a mortgage broker who can guide you through the options.

Want to know if you can afford a £500,000 mortgage? Use our Mortgage Affordability Calculator to get a clear picture of what you can afford based on your income

How Much Deposit Do I Need for a £500,000 House?

Typically, you’ll need a deposit of at least 5% to 10% of the property’s value. So, for a £500,000 house, you’re looking at needing between £25,000 and £50,000 upfront.

The bigger your deposit, the better your chances of securing a competitive interest rate.

If you’re able to put down a larger deposit—say 20% or even 25%—you’ll not only lower your loan-to-value (LTV) ratio but also potentially get a lower interest rate.

Lower rates mean lower monthly repayments and more money in your pocket for all those new home projects you’ve been dreaming about.

And if you’re wondering about getting a mortgage with no deposit at all? Well, it’s not entirely impossible, but it’s extremely rare and typically only available under special circumstances.

It’s also important to remember that a larger deposit can make your offer more appealing to sellers, especially in a competitive housing market.

If you want to know how much deposit you need, or how your LTV might affect your mortgage, use our loan-to-value ratio calculator. This way, you can make a smart, informed decision on what’s affordable for you, and feel a bit more in control of the whole process.

What Factors Affect How Much a £500,000 Mortgage Costs?

There are several factors that affect the cost of a £500,000 mortgage. Knowing these factors will help you make smarter decisions and potentially save money. Here’s a rundown:

Interest Rates

Let’s face it—interest rates are the big deal when it comes to your monthly payments.

A higher rate means higher payments, and a lower rate means you’ll pay less. Even a small difference can really add up.

For example, at a 4% interest rate, your monthly repayment would be £2,639 on a 25-year term, whereas at 5%, it’s £2,923.

So, finding the best rate could save you hundreds per month.

Mortgage Term

As we’ve discussed, the length of your mortgage also plays a big part.

If you opt for a shorter term—say 15 or 20 years—you’ll have higher monthly payments, but you’ll pay less in interest over the entire term.

A longer term, like 30 or even 40 years, will spread the cost out more, lowering your monthly payments, but you’ll be paying a lot more in interest overall.

Type of Mortgage

Are you going for a capital repayment mortgage or an interest-only one? With capital repayment, your payments cover both the interest and the loan amount.

This means your balance goes down over time. With interest-only, you’re just paying the interest, which means lower monthly payments now, but you’ve still got that big £500,000 to deal with at the end.

Deposit Size

As we mentioned earlier, the bigger your deposit, the better. A larger deposit lowers your LTV ratio and can mean better interest rates and more choice of lenders.

Your Credit History

The stronger your credit history, the more likely you are to secure a favourable interest rate.

If you’ve had credit blips in the past, you might find yourself with fewer choices and higher rates, meaning bigger monthly payments.

Employment Type

Lenders often consider the type of employment you have—whether you’re employed, self-employed, or on a fixed contract.

Stable, long-term employment can work in your favour when applying for a mortgage, while self-employed applicants may need to provide additional documentation to prove their income.

What Other Costs Should You Consider with a £500,000 Mortgage?

It’s not just about the monthly repayments when you take out a £500,000 mortgage—there are a few other costs to consider too:

- Arrangement Fee.This is a fee charged by the lender to set up your mortgage. It’s usually between £0 and £2,000. You can sometimes add this fee to your mortgage, but then you’ll pay interest on it.

- Valuation Fee. Your lender will want to value the property to ensure it’s worth what you’re paying. This can set you back between £250-£1,500.

- Stamp Duty. This is the tax you pay on property purchases over a certain amount. If you’re not a first-time buyer, expect to pay some stamp duty on that £500k house.

- Legal Fees. These cover the solicitor’s services for conveyancing and usually cost anywhere from a few hundred to a few thousand pounds.

- Early Repayment Charges (ERCs). If you want to pay off your mortgage early, there may be fees to pay—these can be between 1%-5% of the mortgage balance.

- Insurance. Building insurance is a must to protect your home, and you may also want to consider life insurance to cover the mortgage balance.

- Broker Fees. If you decide to use a mortgage broker, there may be a fee involved—typically between £500-£1,000 or a small percentage of the loan amount.

It’s important to budget for these additional costs so you’re not caught off guard during the buying process.

How to Get a £500,000 Mortgage Approved

Getting a mortgage for a £500,000 property isn’t something you can do on a whim—it takes preparation and the right support. Here’s how you can get ready:

- Save for a Deposit. Aim to save at least 10%, but if you can save more, even better. A larger deposit often means better rates.

- Check Your Credit Score. Before applying, check your credit score. You can use free tools to do this, and fixing any issues now could lead to better mortgage rates later on.

- Gather Your Paperwork. You’ll need proof of income, bank statements, ID, and more. Your mortgage broker will guide you on what’s needed.

- Speak to a Broker. This step is key. A good broker knows the market well and can help you find the best deal. They’ll also assist with the paperwork and answer any questions you have.

- Get a Mortgage in Principle. Having a mortgage in principle shows sellers you’re serious and ready to buy, which can be a real advantage in a competitive market.

Key Takeaways

- Monthly repayments on a £500,000 mortgage vary based on the term, interest rate, and mortgage type. A 25-year repayment mortgage at 5% costs around £2,923 per month, while an interest-only mortgage at the same rate is roughly £2,083.

- Lenders typically offer around 4 to 4.5 times your salary, though higher earners may qualify for more.

- Interest rates, mortgage terms, and deposit size all affect your mortgage costs. A longer term lowers monthly payments but increases overall interest, while a larger deposit can mean lower rates.

- Additional costs like arrangement fees, stamp duty, legal fees, and insurance should be factored into your budget to avoid surprises.

The Bottom Line

Taking on a £500,000 mortgage is a big financial step. There’s a lot to consider—interest rates, mortgage terms, paperwork, and a whole bunch of details that can make the process feel overwhelming.

This is where a mortgage broker can make all the difference. They’re like a personal guide, helping you find your way through the mortgage maze with ease and saving you heaps of time.

Here’s what a broker can do for you:

- Find the best interest rates for your finances.

- Guide you through each step, from mortgage affordability to paperwork.

- Access exclusive deals not available to the public.

- Tailor advice based on your job, credit history, and deposit.

If you’re ready to save time (and maybe avoid a few headaches) on your mortgage hunt, reach out to us. We’ll match you with a reliable broker who’ll help you find the perfect mortgage fit for your situation.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What are the repayments on a £500k buy-to-let mortgage?

Repayments for a buy-to-let mortgage are calculated similarly to residential mortgages, but the average interest rate is usually higher—around 6% or more. Many buy-to-let mortgages are interest-only, meaning you’ll pay around £2,500 per month at a 6% interest rate.

How much mortgage should I secure for a £500,000 house in the UK?

For a £500,000 house in the UK, the amount of mortgage you need to secure will depend on the size of your deposit.

Generally, lenders require at least a 5-10% deposit, though a larger deposit can lead to better rates and terms. Here’s a quick breakdown:

- 5% Deposit: You’d need £25,000 upfront and a mortgage of £475,000.

- 10% Deposit: You’d need £50,000 upfront and a mortgage of £450,000.

- 20% Deposit: You’d need £100,000 upfront and a mortgage of £400,000.

- 25% Deposit: You’d need £125,000 upfront and a mortgage of £375,000.

The more you put down, the less you’ll need to borrow.

Plus, a higher deposit can improve your chances of securing a better interest rate, which can lower your monthly repayments.

Can I get a £500,000 mortgage even with bad credit?

Yes, you can get a £500,000 mortgage with bad credit. You’ll likely need a larger deposit, around 20-25%, and expect higher interest rates. Specialist lenders are more flexible, so a mortgage broker can help you find suitable options.

Related Articles

£50,000 to £90,000 Mortgage Repayments Explained

Are you considering a mortgage of £50,000, £60,000, £70,000, or even £90,000? Whether you’re eyeing a modest property or looking to refinance, it’s essential to know what your monthly repayments could look like. Understanding how factors like interest rates, loan terms, and your deposit size affect your payments can help you plan your finances confidently. […]

What’s the Cost of a £450,000 Mortgage Per Month?

Getting a big mortgage can be confusing with lots of numbers, percentages, and options to think about. If you’re eyeing a £450,000 mortgage, you might be wondering: How much will it cost me every month? How long will I need to keep paying? And how can I make those numbers work in my favour? Well, […]

How Much Will £400,000 Mortgage Repayments Cost You?

Getting a mortgage is a huge financial decision, so it’s important to understand what you’re getting into. A £400,000 mortgage might seem overwhelming, but don’t worry—we’re here to make it simple. Knowing your monthly repayments, interest rates, and options will help you feel more in control and confident about your choices. In this guide, we’ll […]