- What Is a Short-Term Mortgage?

- Why Choose a Short-Term Mortgage?

- What Are the Types of Short-Term Mortgages?

- Short-Term Mortgage vs Long-Term Mortgage

- Am I Eligible for a Short-Term Mortgage?

- What Is the Minimum Mortgage Amount in the UK?

- How To Get a Short-Term Mortgage?

- Short-Term Commercial Mortgages

- Short-Term Self-Build Mortgages

- Short-Term Buy-to-Let Mortgages

- Can You Remortgage a Short-Term Mortgage?

- How Do I Get the Best Short-Term Mortgage Rates?

- The Pros and Cons of Short-Term Mortgages

- Alternatives to Short-Term Mortgages

- Key Takeaways

- The Bottom Line

A Full Guide About Short Term Mortgages in the UK

Paying off your mortgage doesn’t have to take decades.

If you’re close to retirement, planning to move, or just want to be debt-free, a short-term mortgage might be a good choice.

It can help you pay off your home faster, reduce the amount of interest you pay, and give you more financial freedom for whatever comes next.

Let’s look at how it works and why it could be a smart option for you.

What Is a Short-Term Mortgage?

A short-term mortgage is repaid over 15 years or less.

In the UK, standard mortgages run for 25 years, but with rising house prices, lenders now offer terms ranging from six months to 40 years.

If you want to clear your home loan quickly, a short-term mortgage could be a good option.

While your monthly payments will be higher, you’ll pay much less in interest overall.

For example, borrowing £150,000 over 15 years means higher payments each month compared to a 30-year term, but you’ll pay less interest and own your home faster.

Why Choose a Short-Term Mortgage?

Here’s why a short-term mortgage could work for you:

- Own your home faster. Pay off your loan quickly and own your home outright sooner.

- Save money on interest. Shorter mortgages mean less interest to pay over time.

- Build equity more quickly. The faster you pay off your mortgage, the more your home is worth.

- A good option if you’re older. Lenders might be more likely to offer you a short-term mortgage if you’re nearing or in retirement.

- Ideal for smaller loans. Short-term mortgages are often easier to get for smaller amounts of money.

- Perfect for a temporary home. If you’re selling one home and buying another, a short-term mortgage can help you bridge the gap.

- Flexible for unexpected money. If you’re expecting a windfall, like an inheritance, a short-term mortgage can be easily paid off.

- Great for property investors. If you’re buying a property to rent out, a short-term mortgage might be a good choice.

What Are the Types of Short-Term Mortgages?

There are several options when it comes to short-term mortgages. Depending on your situation, one of these would suit you:

Short-Term Fixed Rate Mortgages

Fixed-rate mortgages are popular because they offer stability. Your interest rate remains constant for a set period, usually two, five, or ten years.

Some lenders may offer fixed terms as short as one year, often through product transfers for existing customers.

Just be aware that if you pay off the loan early, you might face early repayment charges (ERCs).

Short-Term Tracker Mortgages

Tracker mortgages follow an external rate, usually the Bank of England base rate.

If this rate changes, so does your mortgage rate. These can be attractive when rates are low, but your payments can rise if rates increase.

Similar to fixed-rate mortgages, tracker deals often come with early repayment charges.

Short-Term Interest-Only Mortgages

You only pay the interest each month, so payments are lower, but you’ll need to repay the full loan at the end.

Lenders usually ask for proof of a repayment plan, such as savings, investments, or a pension.

Some lenders may also ask for a higher deposit—sometimes up to 50%—and proof of a higher income, often £75,000 to £100,000 or more.

Short-Term Offset Mortgages

Offset mortgages lets you link your savings to your mortgage balance, reducing the interest you pay.

For example, if you owe £100,000 and have £10,000 in savings, you’ll only pay interest on £90,000. This helps lower your interest costs and could help you pay off the loan quicker.

Offset mortgages are more specialised, so it’s best to speak with a qualified mortgage broker.

Discounted Rate Mortgages

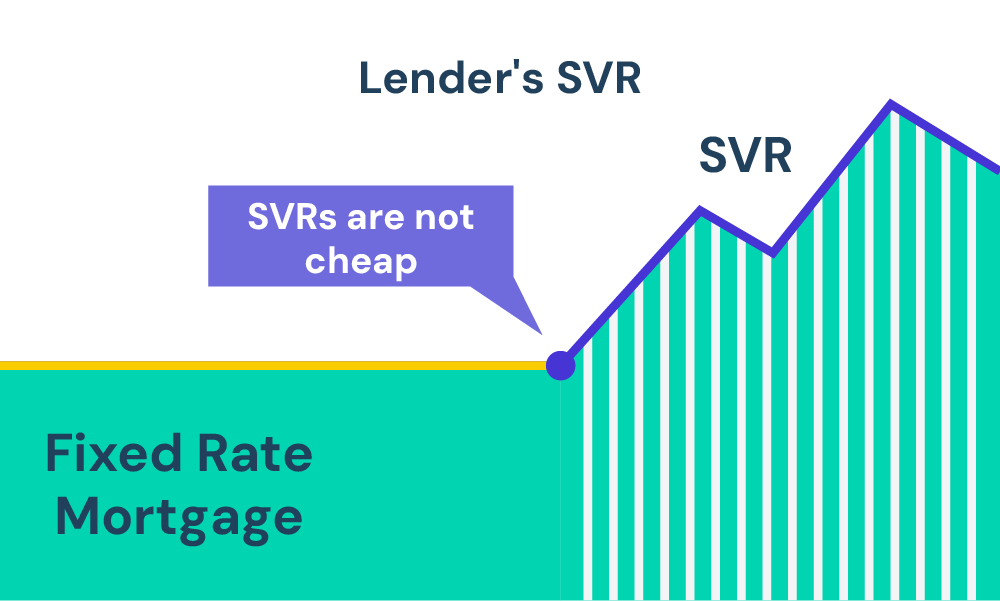

With a discounted rate mortgage, your interest rate follows the lender’s standard variable rate (SVR) but at a discounted rate.

This means the interest rate can fluctuate, which makes monthly payments unpredictable. Early repayment charges may apply during the discount period.

Standard Variable Rate (SVR) Mortgages

These are tied to the lender’s SVR, which can change at any time.

While they’re less predictable than fixed or tracker mortgages, SVR mortgages often allow you to repay early or switch without penalties.

Short-Term Mortgage vs Long-Term Mortgage

Short-term and long-term mortgages each have their benefits and drawbacks.. Here’s how they stack up:

Short-Term Mortgages

- You’ll have higher monthly payments because the loan is paid off in a shorter time.

- You’ll pay less interest overall, saving you money in the long run.

- You’re less exposed to long-term interest rate changes.

- You can pay off your mortgage faster, becoming debt-free sooner.

- You’ll have less flexibility if your financial situation changes.

- You’ll have a lower overall loan cost compared to a long-term mortgage.

Long-Term Mortgages

- You’ll have lower monthly payments, which can be easier to manage.

- You’ll pay more interest over the life of the loan.

- You’re more exposed to interest rate changes over time.

- You’ll take longer to pay off the mortgage.

- You’ll have more flexibility if your finances change.

- You’ll end up paying more in total due to the extended loan period.

Example: If you borrow £150,000 over 30 years at 4% interest, your monthly payment would be £716, and you’d pay £257,678 in total.

For 15 years, the payment would be £1,109, but the total cost drops to £199,662.

If the term was reduced to 2 years, your monthly payment would be much higher, and missing payments could impact your credit.

| Short-Term Mortgage | Long-Term Mortgage |

|---|---|

| Higher monthly payments. | Lower monthly payments. |

| Less interest paid overall. | More interest paid over time. |

| Less affected by rate changes. | More exposed to rate changes. |

| Loan repaid faster. | Loan repaid over a longer period. |

| Less flexibility with payments. | More flexibility with payments. |

| Lower total cost. | Higher total cost. |

Am I Eligible for a Short-Term Mortgage?

Your eligibility for a short-term mortgage depends on a few key factors that lenders will check:

- Affordability – Lenders need to be sure you can handle the higher monthly payments. They’ll look at your income, expenses, and any existing debts. Remember, higher payments mean less money left over each month, so careful budgeting is essential.

- Credit History – Your credit score is important. A good credit score can help you get better rates and increase your chances of approval.

- Age – Lenders may have age limits, especially if you’re close to retirement. They often prefer shorter terms for older borrowers to ensure the loan is repaid while you still have regular income.

- Deposit – A larger deposit can make it easier to get approved. For interest-only mortgages, some lenders might ask for a deposit of up to 50%.

If you can afford a short-term mortgage, you’ll pay off the loan faster and save on interest. Just make sure the higher payments won’t put too much pressure on your finances.

What Is the Minimum Mortgage Amount in the UK?

While there’s no hard and fast rule, lenders typically have minimum mortgage amounts ranging from £25,000 to £50,000.

This can vary depending on the lender and the type of mortgage you’re applying for.

How To Get a Short-Term Mortgage?

Getting a short-term mortgage is similar to applying for a standard one, but there are a few key things to keep in mind.

Here’s a simple guide to help you:

Check Your Finances

Lenders will look closely at your income, expenses, credit score, and any debts to make sure you can handle the higher monthly payments of a short-term mortgage.

You’ll need to show proof of income, like payslips and bank statements, and details of any loans or financial commitments.

It’s important to have a good credit score to get better rates. If your credit needs improvement, pay down debts and make sure all bills are paid on time before you apply.

A larger deposit also boosts your chances of approval and can get you a better deal.

Speak to a Mortgage Broker

A qualified mortgage broker can help you find the best short-term mortgage deals by comparing different lenders.

They can also assist with paperwork and submitting your application. Good brokers often have access to deals you won’t find directly with lenders.

Get an Agreement in Principle (AIP)

An AIP shows how much you can borrow and helps prove to lenders that you’re serious about buying.

Most AIPs are valid for up to 90 days and give you a clear idea of your budget. It’s not a final offer, but it’s a useful step before house hunting.

Start Your Property Search

With your budget in mind, you can begin looking for properties.

If you’re buying to let or planning to develop the property, make sure it fits your investment goals.

Submit Your Mortgage Application

Once you’ve chosen a property and mortgage, submit your full application.

You’ll need to provide proof of income, your deposit, and other financial information.

The lender will carry out a credit check and assess your finances before making a decision.

Valuation and Survey

The lender will arrange a valuation to check the property’s value matches the loan amount.

You might also want to arrange a survey to spot any potential problems with the property.

Get Your Mortgage Offer

If everything goes well, the lender will give you a formal mortgage offer. This will include details of the loan amount, repayment terms, and interest rate.

Review it carefully to make sure it’s right for you.

Completion

Once the offer is accepted, the final step is completion. This is when the lender transfers the money to the seller, and you become the property owner.

Your solicitor will handle the legal work, and once everything is finalised, you’ll get the keys to your new home.

Short-Term Commercial Mortgages

A short-term commercial mortgage is ideal if you want to buy a commercial property but avoid a long-term commitment. Businesses and investors often use these mortgages for temporary financing.

Commercial mortgages typically last between 3 and 25 years. However, short-term mortgages are usually for 1 to 3 years. This is perfect if you plan to sell or refinance the property soon.

Lenders consider short-term commercial mortgages riskier. Therefore, they often charge higher interest rates.

Remember to factor this into your budget. 💡

These mortgages are useful for buying office spaces, warehouses, or retail units. They’re also helpful for refurbishing or redeveloping properties.

When applying for a commercial mortgage, lenders will assess your business’s finances. This includes profit and loss statements, cash flow, and future income projections.

Be ready to provide this information.

Short-Term Self-Build Mortgages

Building your own home is exciting, and a short-term self-build mortgage can help finance it. These mortgages are for people building their property for a limited time.

Unlike traditional mortgages, self-build mortgages release funds as your project progresses. This helps cover land, construction, and material costs at different stages.

Short-term self-build mortgages typically last until your home is finished. Then, you can refinance the loan into a standard residential mortgage.

Lenders often require a larger deposit for self-build mortgages, sometimes up to 25%. The more you pay upfront, the better your chances of getting a good rate.

Self-build mortgages are riskier for lenders due to potential delays or unexpected costs. It’s important to have a solid financial plan before taking this type of loan.

Short-Term Buy-to-Let Mortgages

A short-term buy-to-let mortgage is suitable for investors buying a rental property. These mortgages have shorter repayment terms for properties rented out to tenants.

Investors often use short-term buy-to-let mortgages for buying, renovating, and quickly selling or refinancing properties. This offers financing without a long-term loan commitment.

Although less common than long-term buy-to-let mortgages, they are available for investors with specific strategies.

However, they often have higher interest rates and stricter lending criteria.

Lenders usually require a larger deposit, typically around 25% or more, for most buy-to-let mortgages.

They also assess potential rental income to ensure it covers mortgage payments. Provide a realistic estimate when applying.

Since these mortgages are short-term, you need a clear exit strategy. This could be selling the property, refinancing into a longer-term mortgage, or paying off the loan as rental income increases.

Working with a broker helps find the best options.

Can You Remortgage a Short-Term Mortgage?

Yes, you can remortgage a short-term mortgage, but it’s not always common or necessary.

Remortgaging can involve fees, which may make it more expensive than other loan options.

If you want to reduce your monthly payments or need another loan, it’s worth considering other choices before deciding to remortgage.

If you’re on a fixed-rate or tracker mortgage, check for early repayment charges that could apply if you switch before the term ends.

Make sure to review your current mortgage terms to understand any costs involved.

When your short-term mortgage is ending, remortgaging to a longer-term deal can lower your monthly payments and offer more flexibility.

But, it’s important to assess your financial situation, including your income and expenses, to decide if remortgaging is the right move for you.

How Do I Get the Best Short-Term Mortgage Rates?

To get the best mortgage rates, you need to carefully assess your financial situation and compare offers from different lenders.

A qualified mortgage broker can help with this, as they can search the whole market to find the best deals for you.

Lenders usually offer better rates if you have a strong credit history, a stable income, and a larger deposit. If you meet these criteria, you’re more likely to secure a better deal.

The Pros and Cons of Short-Term Mortgages

Before you decide, here’s a quick rundown of the pros and cons of short-term mortgages:

Pros

- You pay less interest overall, saving money in the long run.

- You own your home outright sooner, achieving faster homeownership.

- You build equity more quickly, which can be useful for refinancing or future investments.

- Ideal for those nearing retirement, as lenders often prefer shorter terms for older borrowers.

- Suitable if you’re borrowing a small amount, as lenders may approve smaller loans more easily with shorter terms.

- Less exposure to long-term interest rate changes, making payments more predictable over a shorter period.

- Flexible option for property investors who want to renovate or sell quickly.

Cons

- Monthly payments are significantly higher, which could put pressure on your budget.

- It may reduce your disposable income due to the larger monthly repayments.

- Limited borrowing power; lenders may offer smaller loan amounts due to the shorter term.

- Less flexibility if unexpected financial issues arise, as higher payments must still be met.

- You might face early repayment charges (ERCs) if you switch mortgages or pay off the loan early.

- Fewer lender options, as not all providers offer short-term mortgage products.

Alternatives to Short-Term Mortgages

If a short-term mortgage doesn’t suit your needs, there are other options worth considering:

- Overpaying on a Long-Term Mortgage. Many long-term mortgages allow you to make overpayments without penalties. This lets you pay off your mortgage faster while benefiting from lower monthly payments.

- Bridging Loans. Bridging loans are short-term loans designed to bridge a gap between buying and selling a property. They are useful if you need to purchase a new property quickly but haven’t yet sold your existing one.

- Personal Loans. For smaller loan amounts, a personal loan might be an alternative to a short-term mortgage. Personal loans tend to have higher interest rates but could be an option if you don’t need a large sum.

- Development Finance. If you’re building or refurbishing a property, development finance provides funds throughout the project. These loans are typically short-term and are paid back once the project is completed.

Key Takeaways

- Short-term mortgages are repaid within 15 years or less, offering faster homeownership and lower interest costs.

- Types of short-term mortgages include fixed-rate, tracker, interest-only, and offset options, each with its own benefits and limitations.

- Short-term mortgages save money on interest but come with less flexibility if financial circumstances change.

- Alternatives include overpaying on long-term mortgages, bridging loans, personal loans, or offset mortgages for those who want flexible options.

- Commercial, self-build, and buy-to-let investors can also benefit from short-term mortgage options, with specific lending criteria for each.

- Remortgaging a short-term mortgage is possible but may involve fees; explore all options before deciding.

The Bottom Line

A short-term mortgage could be a great option if you can handle the higher monthly payments. You’ll pay less interest and build equity faster.

If this sounds right for you, it’s a good idea to speak to a mortgage broker who can find the best deals that suit your needs.

Here’s how a broker can help you:

- Access to many lenders and exclusive deals.

- Get personalised advice tailored to your finances.

- Let someone else handle the paperwork, saving you time.

- Secure the best rates while making the process easier for you.

If you want to save yourself time and stress, reach out to us. We’ll connect you with a trusted broker who can help with your mortgage.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I get a short-term mortgage if I’m retired?

Yes, many lenders offer short-term mortgages to older borrowers, particularly if you can demonstrate the ability to repay the loan within a shorter period.

What’s the smallest mortgage amount I can get in the UK?

The smallest mortgage amount varies by lender, but most will not offer loans under £25,000. Some may have higher minimums, especially for remortgages.

It’s best to check with your lender or broker to confirm their specific minimum mortgage requirements.

Are short-term mortgages a good idea?

If you can afford the higher monthly payments, short-term mortgages can save you thousands in interest and help you own your home faster.

What if I can’t pay my mortgage?

If you’re struggling to pay your mortgage, the first step is to contact your lender as soon as possible. They may offer options like a payment holiday, switching to an interest-only mortgage, or extending the term to lower your payments.

It’s important to act quickly to avoid falling behind, as missed payments can affect your credit score and lead to further financial difficulties.

Will a short-term mortgage save me money?

Yes, a short-term mortgage can save you money on interest. Because the loan is repaid over a shorter period, less interest accrues over time.

But, keep in mind that the monthly payments will be higher.

If you can comfortably afford the larger payments, you’ll save money in the long run compared to a longer-term mortgage.

Can I get a holiday let mortgage for a short term?

Yes, you can get a short-term holiday let mortgage. These are designed for properties rented out to holidaymakers, usually for seasonal or short-term periods.

Lenders will assess the rental income potential and may offer mortgages with terms as short as two to five years.

Specialist lenders may also offer more flexible options.

What are the best options for short-term mortgages?

The best options for short-term mortgages include fixed-rate, interest-only, tracker, and offset mortgages. Each type offers different benefits, depending on your financial goals.

For example, fixed-rate mortgages provide payment stability, while tracker mortgages fluctuate with interest rates.

Choosing the right option depends on your personal circumstances and budget.

What exactly is a short-term bridge mortgage?

A short-term bridge mortgage is a temporary loan used to bridge the financial gap between buying a new property and selling an existing one. It’s typically repaid within 6 to 12 months and helps you secure a new home before your current property sells.

Bridging loans often have higher interest rates and fees, so they’re best suited for short-term use.

Do any brokers focus on short-term mortgage deals?

Yes, some mortgage brokers specialise in short-term mortgage deals. These brokers have access to a wide range of lenders and can help you find the best options for your specific needs, whether it’s for a fixed-term, interest-only, or buy-to-let mortgage.

A broker can also assist with niche products like short-term holiday let or bridging loans.

Related Articles

Tracker Mortgages Rates: Everything You Need to Know

Is your mortgage holding you back from saving money? Maybe you’re a first time buyer, planning to move soon, or a homeowner expecting interest rates to dip. A tracker mortgage might be perfect for you. This mortgage offers you more flexibility than a fixed-rate mortgage. But, like with any financial product, you want to make […]

What You Need to Know About Specialist Mortgage Lenders

When it comes to finding the right mortgage lender, not everyone fits into the standard high street lending rules. If you’re self-employed, have bad credit, or need a more customised mortgage, it can feel frustrating when your bank says “no.” But don’t worry – specialist mortgage lenders can help. These lenders focus on people who […]

Mortgage Valuation Types & Fees: What Should You Expect?

Wondering how much the property you want to buy is really worth? A mortgage valuation helps both you and your lender figure that out. But not all valuations are the same, and costs can vary. Knowing which type of valuation fits your situation can save you time and money during the mortgage process. In this […]