- What is a Tracker Mortgage Rate?

- How Do They Work?

- How Do You Find the Best Tracker Mortgage?

- What Are the Current Tracker Rates?

- What Should First-Time Buyers Know About Tracker Mortgages?

- Should You Switch to a Tracker Mortgage When Remortgaging?

- The Pros and Cons of Tracker Mortgages

- What Are the Alternatives to a Tracker Mortgage?

- Why You Should Speak to a Mortgage Broker

- Key Takeaways

- The Bottom Line

Tracker Mortgages Rates: Everything You Need to Know

Is your mortgage holding you back from saving money?

Maybe you’re a first time buyer, planning to move soon, or a homeowner expecting interest rates to dip.

A tracker mortgage might be perfect for you. This mortgage offers you more flexibility than a fixed-rate mortgage.

But, like with any financial product, you want to make sure you fully understand how it works before diving in.

After all, it’s probably the biggest financial commitment you’ll ever make.

So, whether you’re completely new to this or already a homeowner, this guide will explain tracker mortgages, help you find the best rates, and show you whether it suits your needs.

What is a Tracker Mortgage Rate?

A mortgage rate tracker follows the Bank of England (BoE) base rate, plus a little extra added on top by your lender.

When the base rate goes up, your mortgage payments follow suit. When it drops, so do your payments.

Now, here’s the thing—tracker mortgage rates tend to be cheaper than standard variable rates, but they come with the risk of change.

Unlike a fixed-rate mortgage, your payments won’t stay the same each month. They go up or down depending on the BoE rate. But, if you like a little flexibility, this could be the one for you.

How Do They Work?

As we’ve discussed, tracker mortgages follow the BoE base rate, but they’re usually set slightly above that rate. We call this the margin—the extra percentage your lender adds to the base rate.

So, if the BoE base rate is 5% and your lender adds a 0.75% margin, your total interest rate would be 5.75%.

If the base rate drops to 4.5%, your interest rate would also drop to 5.25%, meaning lower monthly payments for you.

But if the base rate goes up, your payments will increase too.

Many tracker mortgages offer an introductory period with a lower margin. This means you’ll pay less interest for the first few years, typically 1 to 5 years.

After this period, you’ll usually switch to your lender’s standard variable rate, which is generally higher.

Some tracker mortgages also include a collar. This is a minimum interest rate that your rate can’t fall below, even if the base rate drops.

So, if your collar is 5%, your interest rate will never go below 5%, even if the base rate falls lower.

How Do You Find the Best Tracker Mortgage?

With so many deals out there, picking the best tracker mortgage can feel like searching for a needle in a haystack.

Here’s the trick—don’t do it alone.

Speak to a Good Mortgage Broker

This is your most important step. A good mortgage broker will have access to deals that aren’t available to the public.

They know the ins and outs of the market and can quickly spot the best deals based on your deposit, income, and loan term.

Plus, they’ll save you the time and hassle of comparing tracker mortgage rates UK by yourself.

Working with a broker is hands down the easiest and most effective way to find the right deal.

Know What You Want

Before choosing a tracker mortgage, it helps to think about a few key things:

- Term Length – Do you want a short-term deal (2–3 years) for flexibility, or a longer-term deal (5–10 years) for stability? Shorter terms mean you’ll remortgage sooner, while longer terms offer more consistency.

- Deposit Size – The bigger your deposit, the better the rate. Lenders typically offer lower rates to those with a deposit of 20% or more, while smaller deposits (like 5–10%) may come with higher rates.

- Budget – Consider what you can afford if rates go up. With a tracker mortgage, payments can change, so make sure your budget can handle potential increases.

- Risk – Are you comfortable with your payments fluctuating? Tracker mortgages follow the Bank of England base rate, which means they can rise or fall over time.

If you’re unsure about any of these, your broker can guide you through the options and help you make the right choice.

Keep an Eye on Fees

It’s not just about the rate—fees matter too!

Lenders often charge various fees that can quickly add up, so it’s essential to factor them in when comparing deals.

Here’s a quick rundown of what you might come across:

- Product/Booking Fees. These are common and can range from £995 to £1,000, or sometimes be a percentage of your loan amount.

- Early Repayment Charges (ERCs). If you decide to overpay on your mortgage or pay it off early, many lenders have limits (usually up to 10% of the loan annually). Exceeding that could result in a hefty fee.

- Exit Fees. Planning to leave the deal early? You might face exit fees, which can range anywhere from £50 to £300.

- Valuation Fees: Some lenders require a property valuation, and this cost typically falls on you. Depending on the lender, it could be between £150 and £1,500, depending on the property value and type.

- Arrangement Fees. These fees can be charged upfront for securing the deal and can range from a few hundred pounds to as much as £2,000. Some lenders allow you to add this fee to your mortgage, but keep in mind, you’ll pay interest on it if you do.

- Legal Fees. Even though it’s less talked about, you’ll need to budget for solicitors or conveyancers to handle the legal side of your mortgage. Some lenders offer deals with free legal services, but not all do, so you may need to set aside £500 to £1,500.

- Mortgage Account Fees. Some lenders charge an account setup fee, often called a “completion fee” or “account handling fee,” which can be between £100 and £300. This is typically charged when your mortgage starts or ends.

All of these fees can quickly add up, so make sure you’re aware of them when comparing tracker mortgage deals.

If you’re looking to avoid as many fees as possible, some lenders do offer no-fee tracker mortgages—but you’ll likely need a broker’s help to find the best ones.

What Are the Current Tracker Rates?

Tracker rates can vary quite a bit, depending on the lender and your deposit size.

As a rough guide, most tracker mortgage rates in the UK are a few percentage points higher than the BoE base rate, often around 0.5% to 1% above.

So, if the base rate is 5%, you’re looking at a tracker rate of around 5.5% to 6%.

However, the lowest rates are reserved for those with larger deposits—say 20% or more.

Some lenders also offer long-term lifetime trackers, where the rate will follow the BoE base rate for the entire length of your mortgage.

These are great if you think rates will stay low, but if they shoot up, so will your payments. It’s a bit of a gamble, but it could be worth considering.

What Should First-Time Buyers Know About Tracker Mortgages?

If you’re a first-time buyer, you might be tempted by the flexibility of a tracker mortgage, especially if rates are low.

However, it’s important to consider whether you’re comfortable with the risk of fluctuating payments. You’ll need to make sure your budget can handle any potential increases if rates rise.

That said, some lenders offer tracker deals specifically for first-time buyers, so it’s worth speaking to a broker to find the best option for you.

Just be sure to fully understand how the deal works before signing on the dotted line.

Should You Switch to a Tracker Mortgage When Remortgaging?

If your current mortgage deal is ending, or you’ve been moved onto your lender’s standard variable rate (SVR), switching to a tracker mortgage might be a smart option.

Many people remortgage to a tracker deal to avoid the high payments that come with an SVR, which is often much more expensive than both tracker and fixed rates.

The potential to save money is one of the biggest draws.

If you’re comfortable with some uncertainty and believe rates will stay low or drop, a tracker can offer the flexibility you need.

But remember, if rates go up, so will your payments, so it’s important to consider your budget and risk tolerance.

If you’re not sure whether to stick with a tracker or explore other options like a fixed rate, speaking with a broker can help you decide what’s best for your situation.

The Pros and Cons of Tracker Mortgages

Tracker mortgages can offer a lot of flexibility and potentially save you money, but like anything, they have their pros and cons.

Let’s take a look at what they are so you can decide if they’re right for you.

Pros:

- Lower payments. If interest rates fall, your mortgage payments could go down too.

- No early repayment fees. Some tracker mortgages let you pay off your mortgage or switch to a different deal without paying a penalty.

- Flexible payments. You’re not stuck with the same payments every month, so you can take advantage of lower interest rates.

- No collar. Some tracker mortgages don’t have a minimum interest rate, so you could benefit even more from falling rates.

- Interest rate cap. Some lenders limit how high your interest rate can go, protecting you from sudden increases.

- Flexibility. You can switch to a different mortgage or pay off your mortgage early without being tied into a long-term contract.

Cons:

- Higher payments. If interest rates rise, your mortgage payments will go up too.

- No cap. Without a cap, your interest rate could rise sharply, leading to higher payments.

- Higher interest rate after the introductory period. Once the initial offer ends, you might be moved to a higher interest rate.

- Collar. If your tracker mortgage has a collar, you won’t benefit from interest rate drops below a certain level.

- Unpredictable payments. Fluctuating interest rates can make it difficult to budget, especially if rates rise more than expected.

- Early repayment charges. Some tracker mortgages still have penalties for paying off your mortgage early or switching to a different deal.

What Are the Alternatives to a Tracker Mortgage?

If you’re not sure a tracker mortgage is right for you, there are a few alternatives worth considering:

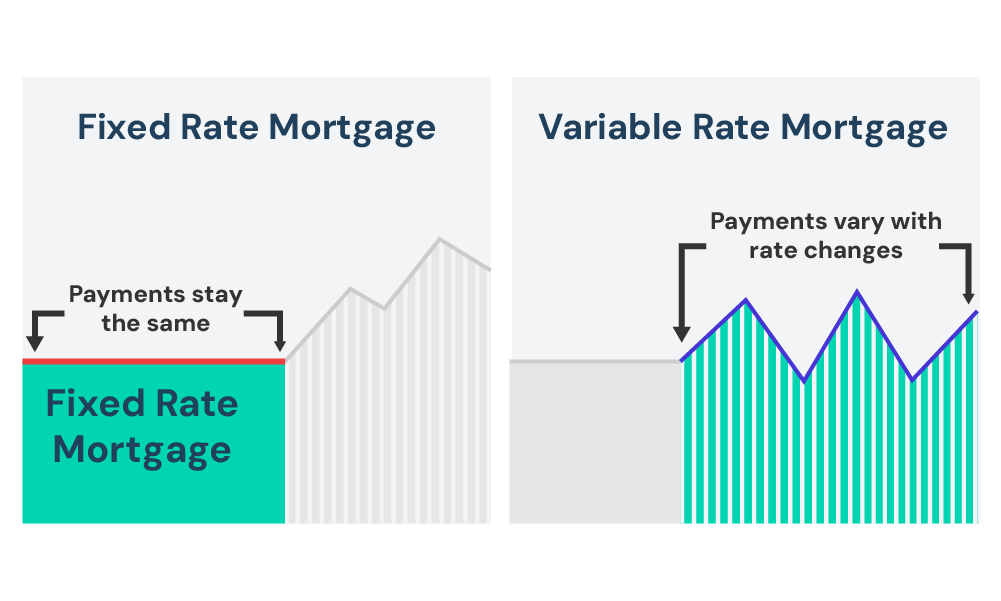

Fixed-Rate Mortgages

A fixed-rate mortgage locks in your interest rate for a set period, usually between 2 to 5 years, but sometimes even up to 10 or 15 years.

This means your monthly payments stay the same, regardless of what happens with the Bank of England base rate.

It’s great for budgeting and gives you peace of mind, especially if you expect rates to rise. However, if rates drop, you won’t benefit from lower payments.

Variable-Rate Mortgages (SVR)

With a standard variable-rate mortgage (SVR), your payments can go up or down, but they don’t directly follow the Bank of England base rate.

Instead, the lender can adjust the rate at their discretion, which gives them more control over how much interest you pay.

While it can sometimes be cheaper, it’s less predictable, and rates can change without much warning.

Discount Mortgages

Discount mortgages offer a rate that’s set below the lender’s SVR for a certain period. So, if their SVR is 5%, and you have a discount of 1%, you’ll be paying 4%.

The catch is that if the lender increases their SVR, your payments will also go up.

Like tracker mortgages, they offer flexibility, but the unpredictability of payments remains a concern.

Why You Should Speak to a Mortgage Broker

We’ve said it before, but it’s worth repeating: A good broker is your best mate when it comes to navigating the tracker mortgage world.

They’ll help you figure out what deal works best for you, whether you should go for a 2-year, 5-year, or even lifetime tracker, and what lender is most likely to offer you a great rate.

The best tracker mortgage rates aren’t always easy to find, but with a broker’s help, you can rest easy knowing you’re getting the best possible deal.

Key Takeaways

- A tracker mortgage’s interest rate rises and falls with the Bank of England base rate, plus a fixed amount. This means your payments can change as the base rate changes.

- The best tracker mortgage rates in the UK often require a large deposit for lower rates.

- Watch out for additional fees, including product fees, early repayment charges, and exit fees.

- First-time buyers can get tracker mortgages, but it’s important to understand the risks of changing payments.

- Remortgaging onto a tracker deal can help avoid higher standard variable rates.

The Bottom Line

Choosing a tracker mortgage is all about balance—do you want flexibility, or are you after security?

If you’re okay with a little risk (and potential reward), a tracker mortgage could be a great option. But if you like the idea of fixed monthly payments, a fixed-rate mortgage might be more your speed.

Whatever you decide, make sure you’re informed, speak to a broker, and factor in all the extra costs. That way, you can make a decision that’s right for you.

To get started, reach out to us. We’ll connect you with a qualified mortgage broker who can help secure the best mortgage deal for you.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Are tracker mortgages cheaper than fixed-rate mortgages?

Tracker mortgages can be cheaper than fixed-rate mortgages, especially when the Bank of England base rate is low.

However, their rates fluctuate with the base rate. This means you could save money when rates are low but pay more if they rise.

How often does the tracker rate change?

The tracker rate changes whenever the Bank of England changes its base rate. This can happen up to eight times a year, depending on decisions made by the Bank of England’s Monetary Policy Committee.

Can I get a no-fee tracker mortgage?

Yes, some lenders offer tracker mortgages with no upfront fees. However, these deals can be harder to find.

Working with a mortgage broker can help you identify the best no-fee tracker mortgage options available to suit your needs.

Can I get a tracker mortgage deal with a bad credit score?

Yes, you can get a tracker mortgage with a bad credit score. However, it might be more difficult. Lenders will evaluate your credit history, income, deposit, and affordability.

While some may offer higher rates or require a larger deposit, getting a mortgage is still possible if you meet their criteria.

A good broker specialising in bad credit mortgages can help you find lenders more likely to consider your situation.

Related Articles

What You Need to Know About Specialist Mortgage Lenders

When it comes to finding the right mortgage lender, not everyone fits into the standard high street lending rules. If you’re self-employed, have bad credit, or need a more customised mortgage, it can feel frustrating when your bank says “no.” But don’t worry – specialist mortgage lenders can help. These lenders focus on people who […]

Mortgage Valuation Types & Fees: What Should You Expect?

Wondering how much the property you want to buy is really worth? A mortgage valuation helps both you and your lender figure that out. But not all valuations are the same, and costs can vary. Knowing which type of valuation fits your situation can save you time and money during the mortgage process. In this […]

A Full Guide About Short Term Mortgages in the UK

Paying off your mortgage doesn’t have to take decades. If you’re close to retirement, planning to move, or just want to be debt-free, a short-term mortgage might be a good choice. It can help you pay off your home faster, reduce the amount of interest you pay, and give you more financial freedom for whatever […]