- What is Mortgage Porting?

- What Should You Expect When Applying for Mortgage Porting?

- Should You Consider Porting a Mortgage?

- What Factors Impact Your Ability to Port a Mortgage?

- Is a Credit Check Necessary?

- What Happens if I Have a Bad Credit Score?

- How Does Retirement Affect Mortgage Porting?

- Can You Port Your Mortgage to a Less Expensive Property?

- What Happens When You Upgrade to a Pricier Home?

- When to Reconsider Mortgage Porting

- Don’t Go It Alone: Why You Need a Remortgage Broker

Can You Port Your Mortgage to a New Home?

Buying a new home while having an existing mortgage may seem daunting. You might be contemplating the possibility of transferring your current mortgage, whether it’s a variable rate, fixed rate, or tracker mortgage, to your new property. This practice is known as “mortgage porting“.

But how do you proceed if your financial circumstances have changed since you first got your mortgage? It could be that your income has decreased or your credit score has declined.

Is it still feasible to opt for mortgage porting under such conditions, and what are the steps involved?

In this article, we will unfold the concept of mortgage porting, outline the scenarios in which it might be a beneficial choice, and address the potential worries regarding changes in your financial situation.

What is Mortgage Porting?

Mortgage porting is the process of transferring your existing mortgage to a new property. This means that you can keep your current interest rate, term, and other terms and conditions when you move.

Porting a mortgage can be a good option if you have a good interest rate and you don’t want to have to pay any early repayment charges.

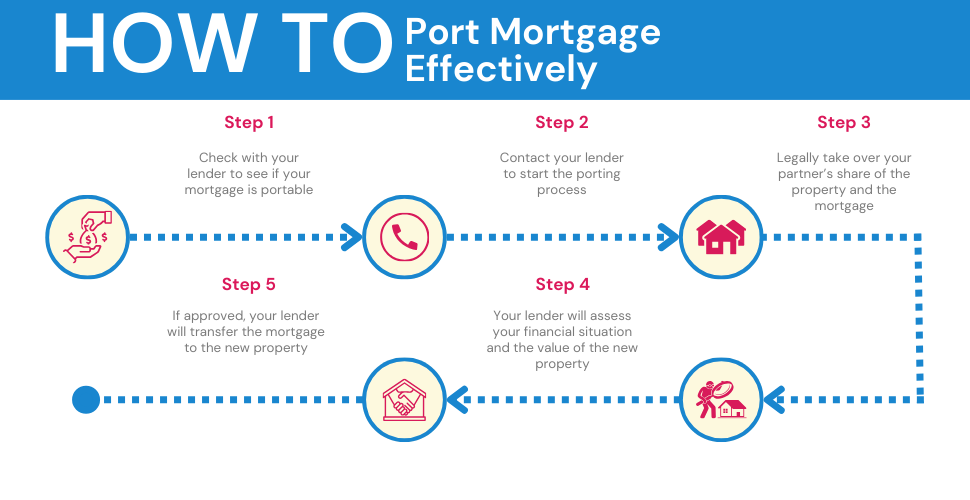

To port your mortgage, you will need to contact your lender and ask them to approve the port. Your lender will need to assess your financial situation to make sure that you are still eligible for the mortgage.

They will also need to appraise the new property to make sure that it is worth enough to secure the mortgage.

If your lender approves the port, they will transfer the mortgage to the new property. You will need to pay a small fee for the port, but this is usually much less than the cost of breaking your mortgage early.

There are a few things to keep in mind when porting a mortgage:

- Not all mortgages are portable. You will need to check with your lender to see if your mortgage is eligible for porting.

- You may need to pay a higher interest rate when you port your mortgage. This is because the lender is taking on more risk by transferring the mortgage to a new property.

- You may need to pay closing costs when you port your mortgage. These costs can vary depending on the lender and the property.

In other words, this move is not to be made impulsively. It demands thoughtful consideration and expert advice.

Consulting with a mortgage specialist can help you understand the finer details of the process and facilitate a seamless move.

They can also help you evaluate the pros and cons of porting and tailor the strategy to your individual needs.

What Should You Expect When Applying for Mortgage Porting?

When you apply to port your mortgage, your lender will take a detailed look at both your personal and financial circumstances, possibly more closely than when you first secured your mortgage.

This could be because of changes in your life like a significant increase in income or perhaps starting a family, which can alter your financial profile.

In addition to evaluating your income and expenses, you might want to borrow extra funds to cover the cost of the new property.

Your lender will also arrange for a survey and valuation of the new property before approving to port your mortgage.

Ideally, you’d complete the purchase of the new property and settle the mortgage on your old home on the same day to ensure a smooth transition.

But, some lenders offer a grace period, typically between 30 to 90 days, to complete the process if a same-day transition isn’t feasible.

Should You Consider Porting a Mortgage?

Considering mortgage porting is a significant step that comes with its set of advantages and disadvantages.

It’s a choice that warrants serious consideration. Here are the pros and cons when choosing to port a mortgage:

Pros of Opting for Mortgage Porting

- Avoid Unnecessary Expenses. By sticking with your current lender and terms, you can sidestep the costs that come with early repayment or exiting your mortgage.

- Retain Your Favourable Interest Rate. If the interest rate of your initial mortgage is lower than the current rates, you’re in luck! You get to enjoy this lower rate even when you move to your new home.

- Skip the Hassle. Moving your mortgage means you won’t have to go through the rigorous process of applying for a new one, since your lender already has most of your details, making things a lot easier.

Cons of Choosing to Port a Mortgage

- Missed Opportunities. Be cautious, as sticking with your existing lender might mean missing out on better deals elsewhere. It’s wise to explore and compare with other options before making a decision.

- Additional Costs. Brace yourself for some extra charges such as valuation, arrangement, and legal fees. You might also have to pay a small fee for transferring or exiting your mortgage.

- Potential Complexities. If your new home costs more, the extra amount you borrow might have a different interest rate. This means you might end up juggling two different mortgages with varied terms, so seeking expert advice could be a lifesaver.

What Factors Impact Your Ability to Port a Mortgage?

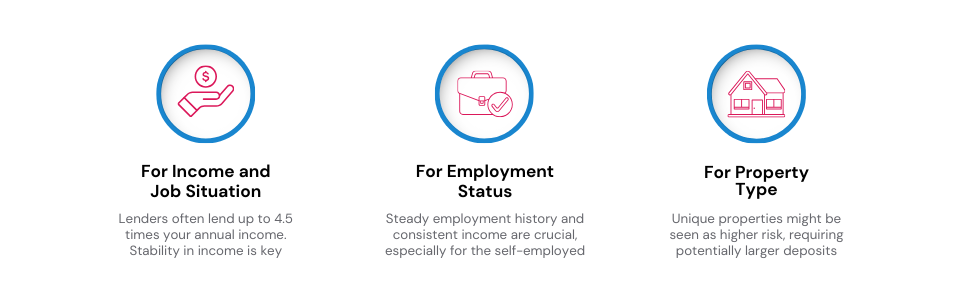

Income and Job Situation

Since you first signed up for your mortgage, the lending criteria might have evolved, and this could influence the amount you are eligible to borrow now.

It’s a known fact that lenders have their specific methods to determine how much they can lend, which often hinges on your annual income and other factors.

As a guideline, many lenders restrain themselves from offering more than 4.5 times the applicant’s annual income. However, in certain conditions, there could be lenders willing to extend a larger loan amount.

Employment Status

When it comes to your job status, lenders tend to delve deep. They’re interested in knowing details like your basic salary, the duration you’ve held your current position, and any bonuses you might receive.

If you’ve recently switched jobs, it might be a bit harder to secure a loan, as lenders usually favour individuals who have been in the same job for a considerable period, typically around a year.

For the self-employed, showcasing a steady income might require presenting full accounts for the last two or three years.

While it becomes quite tough if you’re newly self-employed or changing jobs soon, it’s not an absolute roadblock.

Seeking advice from a professional can pave a viable path for mortgage porting.

Property Type

If you’re eyeing a property that falls on the more unique side of the spectrum, you might find it a bit more challenging to sell later on.

Lenders often see these properties as a riskier proposition because of the potential difficulties in selling them in the event of a repossession.

However, not all hope is lost. Some lenders might be willing to work with you, possibly suggesting a larger deposit to balance out the perceived higher risk associated with such unconventional properties.

Is a Credit Check Necessary?

Absolutely. Given that this process mirrors a fresh mortgage application, it invariably includes the customary credit inspections.

Your lender will assess your affordability based on their latest lending criteria, so it’s prudent to safeguard a commendable credit score as you approach the time to relocate.

Moreover, you’ll be asked to furnish additional documents, which might encompass:

- Proof of identity

- Recent bank statements

- A few months’ evidence of income

>> More about What Happens on a Credit Check?

What Happens if I Have a Bad Credit Score?

Lenders are naturally cautious with applicants who have a less-than-stellar credit history, viewing them as higher risk.

This could mean you’re asked to put down a larger deposit or, in some instances, your application might be turned down due to an inadequate credit score.

Nevertheless, if you’re planning to move to a property with a similar or lower value and you don’t require additional borrowing, your lender might still consider allowing the porting of your mortgage, recognising that the loan is already established.

>> More about Remortgaging with a Bad Credit

How Does Retirement Affect Mortgage Porting?

If you’re retired or nearing that stage, you might be wondering about your prospects of porting a mortgage. The good news is that being retired doesn’t outright exclude you from the possibility.

Especially if you’re nearing the completion of your mortgage term or have managed to settle most of it against your current home, your chances are still bright.

Generally, lenders have a cap on the age limit, usually around 75, but they also factor in the age you’ll be at the termination of the mortgage tenure.

Having a nest egg can be a boon here, as being able to prepay a portion of your mortgage can elevate the likelihood of your lender giving a green light to your application.

Can You Port Your Mortgage to a Less Expensive Property?

If you’re considering moving to a less expensive home or neighbourhood, porting your mortgage can be a straightforward option, especially if you don’t need to borrow additional funds.

Although you will need to cover the valuation fee for the new property, you can sidestep other charges like arrangement fees and early repayment penalties.

However, the complexity arises when you wish to maintain the same loan amount despite moving to a property of lesser value. From the lender’s perspective, this increases the risk linked with the loan.

Here’s a simplified example to illustrate this:

Imagine your current home is valued at £250,000 with a £180,000 mortgage against it, which results in a loan-to-value (LTV) ratio of 72%. If you aim to retain a £180,000 loan but the new home is valued at £220,000, the LTV ratio escalates to over 81%.

This shift might be seen as a red flag by the lender, urging them to ask for a reduction in the loan to maintain the existing LTV ratio.

Moreover, they might request a portion of the mortgage to be paid off to preserve the LTV, which isn’t necessarily a downside as it could lead to reduced monthly mortgage repayments.

This could be a silver lining, particularly for those who have experienced a dip in their income.

Nevertheless, it’s crucial to remember that the approval of the ported mortgage isn’t guaranteed, as your financial and personal circumstances might have altered since you took out the original loan.

What Happens When You Upgrade to a Pricier Home?

When you’re eyeing a move to a home with a heftier price tag, porting your mortgage could be a viable route.

However, this process might involve taking out an additional loan, and it’s important to note that the interest rate of this new loan might not align with your current mortgage rate.

Your lender will present you with options from their current offerings, which might not be as favourable compared to what other lenders can offer.

This scenario can lead you to manage two separate loans, each having different completion dates. Therefore, it is prudent to scrutinise all available options before making a decision.

When to Reconsider Mortgage Porting

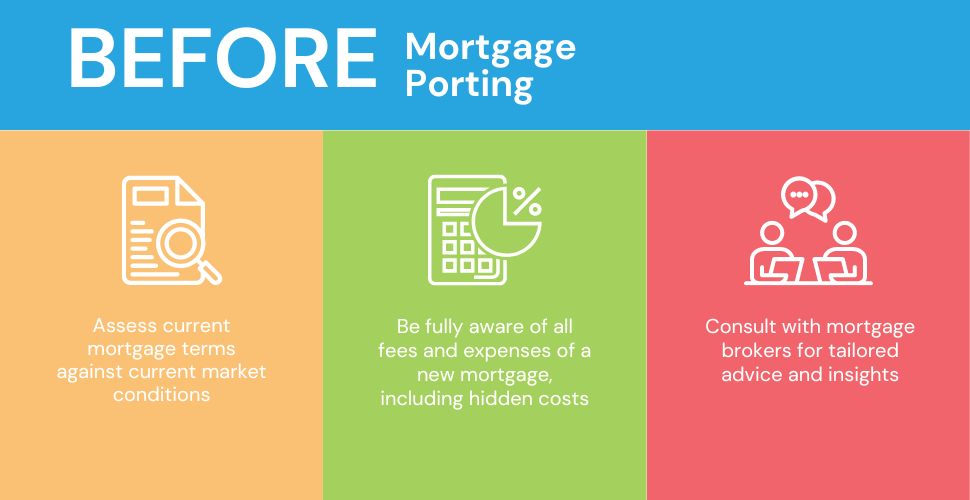

Before deciding to port your mortgage, take a close look at your current deal.

Consider if the interest rates and terms are still favourable in today’s market. Sometimes opting for a new mortgage might offer you better benefits.

It’s vital not to overlook the total costs that a new mortgage entails. Pay attention to fees and additional expenses that might arise.

Ensure that taking a new mortgage won’t strain your finances, considering both monthly repayments and possible hidden costs.

Even if you’re experienced in the property market, expert advice can be invaluable. Consulting with professionals can offer insights and guidance, helping you make a well-informed choice that suits your financial situation best.

By considering these factors, you’ll be better equipped to make a decision that aligns with your financial objectives and ensures a smoother transition, whether you choose to port or get a new mortgage.

Don’t Go It Alone: Why You Need a Remortgage Broker

Taking the leap to port your mortgage isn’t something to be done lightly. It’s essential to understand the benefits and potential pitfalls.

Will you save money? Is the process right for your current financial situation? These are just a few questions that might swirl in your head.

This is where a remortgage broker steps in.

By consulting with someone who specialises in mortgage porting, you’re equipping yourself with a guide who knows the terrain.

They can offer insights, answer your burning questions, and steer you towards choices that benefit you the most.

Ready to make the move? Just fill out a simple form, and we’ll link you up with professionals for tailored advice on your mortgage porting journey.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Is it a good idea to port a mortgage?

Whether porting a mortgage is a good idea depends on various individual factors including the terms of your existing mortgage, the costs associated with transferring, and your financial circumstances.

It can be a wise decision if you have a favourable interest rate on your current mortgage that you’d like to maintain. Consulting with a mortgage broker can provide insight and help you decide based on your unique situation.

Can a mortgage be transferred to another property in the UK?

Yes, transferring a mortgage to another property, also known as mortgage porting, is possible in the UK. However, it is important to note that not all lenders offer this service.

If your lender does permit mortgage porting, you can transfer your existing mortgage to a new property, potentially saving money on early repayment charges. You should consult with your lender to understand the specific terms and conditions of porting your mortgage.

How quickly can you port a mortgage?

The timeframe for porting a mortgage can vary widely depending on the lender and the complexity of your specific circumstances. Generally, it can take anywhere from a few weeks to a couple of months to complete the process.

It’s advised to initiate the process well in advance of your planned move to avoid any potential delays. Always consult with your lender for an accurate time estimate based on your specific details.

Will I have to undergo an affordability check again when porting?

Yes. Your lender will likely check if your financial situation has remained stable since your first application and confirm that you can manage the monthly repayments. If you’re relocating to a pricier property and borrowing more, the lender will certainly conduct an affordability test.

Is a deposit necessary when porting my mortgage?

For a property of the same or lower value, the equity in your current home often covers the deposit for the new property. However, if you’re moving to a pricier home and your existing equity doesn’t meet the lender’s loan-to-value criteria, you might need to provide an additional deposit.

What's next after porting my mortgage?

Once you decide porting is right for you, typically, your lender will require that you settle your old mortgage and complete the purchase of your new property on the same day.

Some lenders might let you retain your current deal for a short period, usually between 30 days to three months, before completing the process.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Do I Need To Pay Solicitor Fees When Remortgaging?

Remortgaging your home can be a smart way to reduce your monthly mortgage payments or tap into your property’s equity. But the process isn’t always straightforward. One potential cost that often confuses homeowners is solicitor fees. Do you actually need to pay for a solicitor when remortgaging? Let’s take a closer look. When Do You […]

Unencumbered Mortgage: How To Remortgage a Fully Owned Home?

Owning a property without any debts hanging over it – sounds liberating, doesn’t it? And with that freedom, you might be thinking about the different ways to make the most of your fully paid property. Maybe it’s time to fix up the house or invest in a new opportunity? In this article, we’ll break down […]

How to Remortgage to Buy a Car: A Complete Guide in 2025

Car financing options like auto loans and leasing agreements typically come with scary double-figure interest rates. This coupled with the escalating car costs can discourage you from even dreaming of buying a new vehicle. But whether you’re eyeing a sleek electric sports car or a vintage camper van, getting behind your dream wheels isn’t out […]