- What is Remortgaging?

- What is Home Equity?

- What is Loan-To-Value (LTV)?

- Why Consider Remortgaging for Equity Release?

- How Does Remortgaging for Equity Release Work?

- How Much Equity Can I Access?

- When is the Right Time to Remortgage to Release Equity?

- Pros and Cons of Remortgaging for Equity Release

- Alternatives to Remortgaging

- The Bottom Line: Seeking Advice on Remortgaging

Remortgaging to Release Equity From Your Home Explained

Owning a home is not only a significant milestone in life; it also opens doors to new financial opportunities.

Imagine having the ability to tap into your home’s worth to invest in your child’s education, make some much-needed home improvements, or even take that dream holiday you’ve always wished for.

This is exactly where remortgaging to release equity comes into the picture. It can be a viable route to reshaping your financial landscape.

But how can you be certain it’s the right path for you?

In this guide, we’re here to walk you through the ins and outs of remortgaging, helping you weigh its potential benefits in line with your personal and financial goals.

What is Remortgaging?

Remortgaging is essentially replacing your current mortgage with a new one, using the same property as collateral.

This can be done with your existing lender or a new one, with the primary aim of securing a more favourable interest rate or releasing equity from your home.

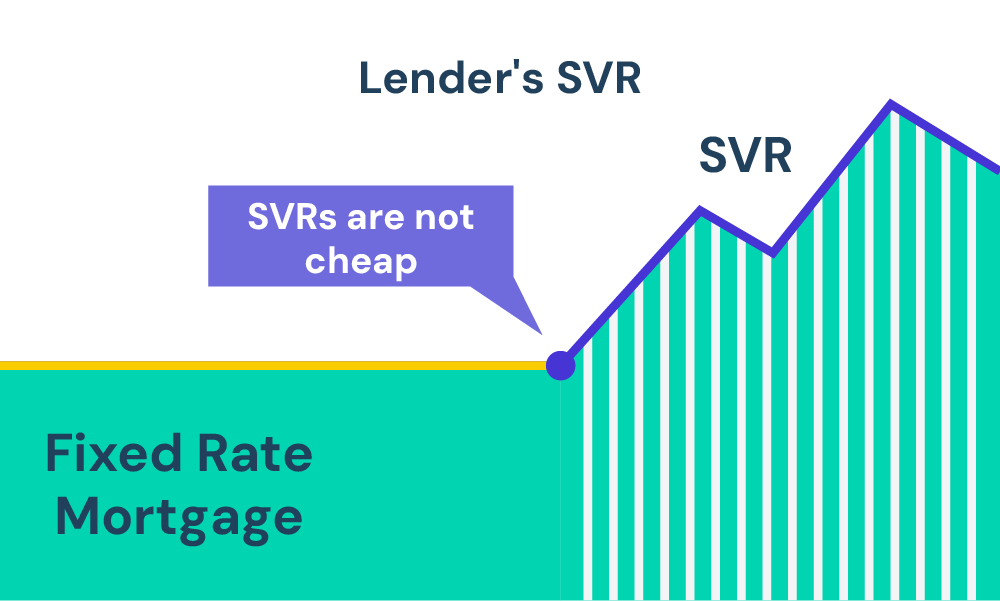

When you reach the end of your fixed-rate mortgage period, which usually lasts from two to five years, the lender often switches you to a standard variable-rate mortgage.

This could mean a significant bump in your interest rates, leading to higher monthly payments. However, by remortgaging, you can negotiate a better deal, potentially saving you a substantial sum in the long run.

What is Home Equity?

To fully grasp the concept of remortgaging for equity release, it is essential to understand what “equity” means in the context of homeownership.

Equity is essentially the portion of your home that you own outright, free of any mortgage obligations.

Imagine you have a house valued at £300,000 and you’ve got £100,000 left to pay on your mortgage. Your equity in this scenario would be £200,000.

This figure increases as you continue paying down your mortgage, or if the value of your property appreciates over time.

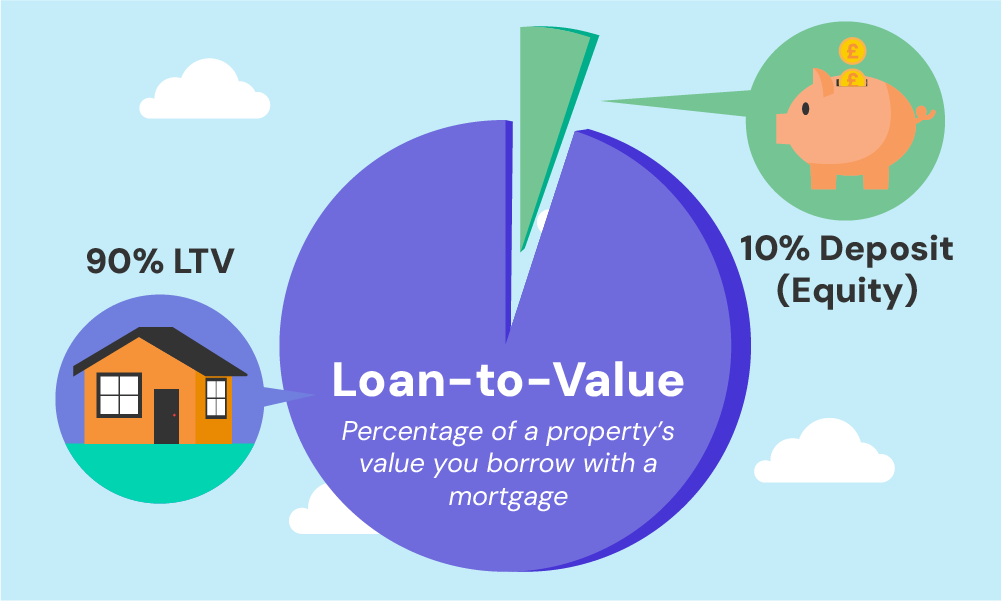

What is Loan-To-Value (LTV)?

Now that you have a grasp on equity, let’s talk about another critical term: the loan-to-value ratio, or LTV.

This percentage represents the difference between the size of your mortgage and the amount of equity you have in your home.

Suppose you are buying a home worth £200,000, and you put down a deposit of £50,000. You’d need a mortgage for the remaining £150,000, setting your LTV at 75% [£150,000/£200,000].

As you chip away at your mortgage or your property’s value increases, your LTV decreases, and your equity grows.

This metric is a crucial factor for lenders when determining the interest rates they offer during the remortgaging process.

Why Consider Remortgaging for Equity Release?

Let’s explore why you might consider remortgaging to release equity.

This financial move can be a game-changer for many homeowners. It allows you to free up a lump sum of money, which you can then utilise for various purposes such as:

- Home renovations

- Funding educational expenses

- Assisting your child in purchasing their first home

- Launching a business

- Settling short-term debts

- Facilitating care services and needs

Remember, this process differs from equity release schemes targeted at homeowners above the age of 55. It is essential to distinguish between the two to make informed decisions.

How Does Remortgaging for Equity Release Work?

Remortgaging to release equity is a bit different than getting a mortgage to buy a new home. It involves utilizing the financial value you’ve already built up in your home over the years.

Imagine you bought your home for £250,000 with a £50,000 deposit, which meant your initial mortgage was £200,000 and your Loan to Value (LTV) ratio was 80%.

As time passes, not only has the value of your home gone up to £300,000, but you have also managed to pay off £20,000 of your mortgage. This means your equity – the part of the home you truly own – is now a whopping £120,000!

When you decide to remortgage for, let’s say £200,000, you can now unlock £20,000 to use for other important things in your life, and enjoy a lowered LTV of 66%.

However, it’s important to remember, that with remortgaging, you are borrowing against your home’s value, and it might lead to higher monthly payments.

How Much Equity Can I Access?

To figure out how much equity you have in your home, you can start by getting a ballpark figure of your home’s current market value.

You might look up recent sales of similar properties in your area on the Land Registry or consult with a local estate agent for an estimated valuation.

Next, subtract the outstanding amount you have on your mortgage from this estimated value. The number you get is a rough estimate of the equity you hold.

It’s not an exact number but it gives you an idea of the amount you could potentially release through remortgaging.

Use our remortgage calculator to find out how much equity you could release from your home and what your monthly payments might be after remortgaging.

When is the Right Time to Remortgage to Release Equity?

The timeframe for remortgaging can vary greatly among different lenders. Generally speaking, a minimum of six months of ownership is required before you can initiate the process.

However, some lenders may offer a more flexible timeframe, with no mandatory waiting period.

>> More about Remortgage Within Six Months

Pros and Cons of Remortgaging for Equity Release

Like any financial decision, remortgaging for equity release comes with its own set of advantages and disadvantages. It is essential to weigh these carefully to make an informed decision.

Pros

- Get to Your Savings. You can access the money that is currently tied up in your home. It’s like opening up a savings jar you’ve had sitting on a shelf.

- Spend it Your Way. You can use the money you get for anything you like, whether it’s helping pay for your kid’s education, giving a nice gift, or making your home even better.

- Keep a Good Balance. If you’ve already paid a lot towards your home, remortgaging might not change your loan-to-value (LTV) ratio too much, which can be a good thing.

- Possible Better Rates. You might find yourself with a better interest rate on your new mortgage deal, which means you could pay less over time.

Cons

- Bigger Monthly Bills. If you decide to remortgage, you might notice that your monthly bills go up because you borrowed more money.

- Longer Payment Time. You might end up having to pay back the money over a longer time, which can feel like a never-ending cycle.

- Could be More Expensive. Sometimes, getting more money through remortgaging can be more costly than taking out a personal loan.

- Risk of Losing Your Home. If you can’t keep up with the higher payments, you risk losing your home, which is a very serious consequence.

- Owing More than Your Home is Worth. If house prices go down, you might end up owing more than what your home is now worth, which can be a stressful situation.

- Extra Charges. If you’re still in the early stages of your current mortgage, you could face big charges to remortgage, sometimes as much as 5% of the loan.

- Harming Your Credit Score. You should be careful and get advice before remortgaging because doing it wrong can hurt your chances of getting loans in the future and harm your credit score.

- Better Options Might be Available. Before you decide to remortgage, it’s a good idea to look at other ways you might raise the money you need because you might find a better option.

Alternatives to Remortgaging

Thinking of ways to get some extra money? Remortgaging is one option, but there are others you might consider before making a decision. Here are some alternatives:

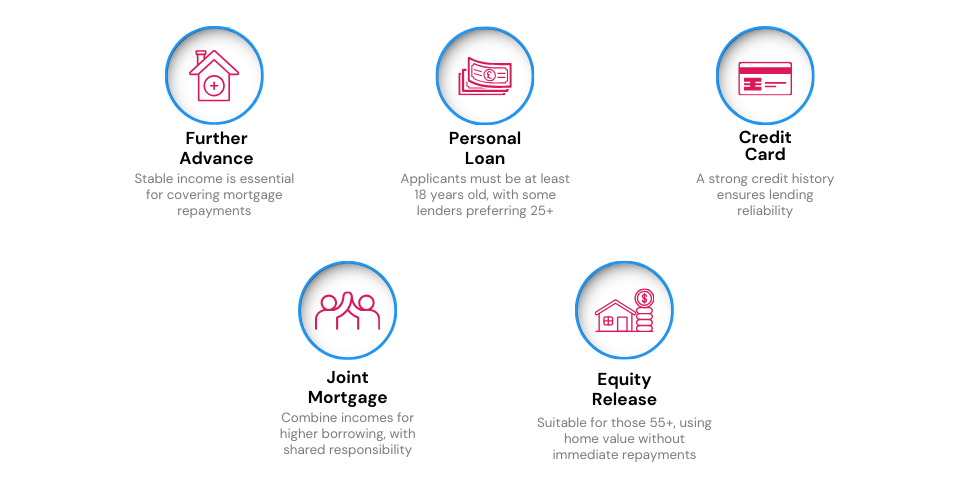

Further Advance from Your Current Lender

You can chat with your current mortgage provider to possibly borrow more money at your current or a competitive rate. This method can be quicker and more cost-effective as it avoids certain fees and legal processes.

But, remember, they might need to check if you can afford to repay the additional amount before lending it to you.

Personal Loan

This option might have a higher interest rate, but you could repay it much faster compared to remortgaging.

Depending on your situation, you might be able to borrow up to £25,000 and get the money in just a day or two.

Money Transfer Credit Card

If you’re looking for a smaller amount, this could be your option. You can transfer money directly into your bank account.

Just ensure to pay off the total amount before the 0% interest period ends to avoid high charges.

If your goal is to assist a family member in buying a property, consider a joint mortgage that combines both your incomes, allowing a higher borrowing limit.

Or, become a guarantor to cover the mortgage repayments if necessary, keeping in mind the risks involved.

Equity Release Mortgages (for those 55+)

This can be a suitable method to get income from your home’s value without monthly payments.

The repayment is deferred until your home is sold, generally when the last homeowner passes away or moves into long-term care.

The Bottom Line: Seeking Advice on Remortgaging

Making the decision to remortgage can be a big step, and getting advice from the right places is important.

A remortgage broker can be your invaluable ally in this process. They offer expert guidance, helping you find the best interest rates, understand the fine print of different mortgage agreements, and avoid hidden fees.

To get started, simply fill out this quick form and we’ll connect you to a remortgage advisor who specialises in this field.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

How much equity could I release from my home?

The equity you can release largely depends on your circumstances and the lender’s criteria. It’s essential to note that the lender will reassess your financial situation and credit rating to determine the amount and the deal they can offer.

Remember, if your credit score isn’t in the best shape currently, you might want to delay remortgaging or seeking other credits until it improves.

How long will it take to release equity through remortgaging?

It might take up to a couple of months to complete the remortgaging application process. So, make sure to allocate ample time before you need the money.

Can I still move house if I remortgage?

Yes, moving house is still an option after remortgaging. You can either transfer your mortgage to your new home or secure a new mortgage. Consulting a mortgage adviser to understand your options and the associated costs would be a wise step.

How much will remortgaging cost?

The costs can vary, but if you’re in the initial period of your current mortgage, you might face an early repayment charge. Other fees could include a mortgage arrangement fee, valuation fee, and legal costs. Ensure to inquire about any extra costs that might be involved with your provider or mortgage broker.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Do I Need To Pay Solicitor Fees When Remortgaging?

Remortgaging your home can be a smart way to reduce your monthly mortgage payments or tap into your property’s equity. But the process isn’t always straightforward. One potential cost that often confuses homeowners is solicitor fees. Do you actually need to pay for a solicitor when remortgaging? Let’s take a closer look. When Do You […]

Unencumbered Mortgage: How To Remortgage a Fully Owned Home?

Owning a property without any debts hanging over it – sounds liberating, doesn’t it? And with that freedom, you might be thinking about the different ways to make the most of your fully paid property. Maybe it’s time to fix up the house or invest in a new opportunity? In this article, we’ll break down […]

How to Remortgage to Buy a Car: A Complete Guide in 2025

Car financing options like auto loans and leasing agreements typically come with scary double-figure interest rates. This coupled with the escalating car costs can discourage you from even dreaming of buying a new vehicle. But whether you’re eyeing a sleek electric sports car or a vintage camper van, getting behind your dream wheels isn’t out […]