- What is a Second Charge Mortgage?

- Getting a Second Charge Mortgage for Buy-to-Let Properties

- Who Should Consider a Second Charge Mortgage?

- Benefits of Second Charge Mortgage for Buy To Let Properties

- Assessing the Risks: A Cautious Approach

- How to Qualify for a Buy-to-Let Second Mortgage?

- What Are the Costs Involved in a Second Charge Mortgage for Buy-to-Let?

- What are the Interest Rates to Expect?

- How To Find the Right Mortgage Lender?

- How to Find The Best Buy-To-Let Second Charge Mortgages?

- The Bottom Line

Buy To Let Second Charge Mortgages: A Wise Move?

In the UK, buy-to-let mortgages have become a popular choice for those looking to invest in the property market. These mortgages are designed specifically for properties that will be rented out.

However, there is another option that investors should consider: second-charge mortgages for buy-to-let properties.

This article aims to explain everything you need to know about second-charge mortgages for buy to let properties in the UK.

What is a Second Charge Mortgage?

A second charge mortgage is a loan you can get against a house or flat that already has a mortgage. It uses the part of your property that you fully own as security.

This type of mortgage is different from your main mortgage.

If you sell your property, the money from the sale will first pay off your main mortgage, then the second charge mortgage.

Getting a Second Charge Mortgage for Buy-to-Let Properties

The UK market offers a variety of lenders for second-charge loans, providing flexibility for property investors.

One of the key benefits of a buy-to-let second charge is the absence of conveyancing or early repayment fees.

This can result in a more cost-effective and straightforward process compared to traditional remortgaging.

When you remortgage, you replace your existing mortgage, which can be a more complex and time-consuming process.

A second-charge mortgage, on the other hand, can be a simpler and more direct route to securing additional funds, without disrupting your current mortgage agreement.

Who Should Consider a Second Charge Mortgage?

You must think about a second charge mortgage for your rental property if:

- You have significant equity in your property and need extra money.

- You want to keep the favourable terms in your current mortgage and avoid renegotiations.

- You’re faced with high early repayment fees when you opt to remortgage.

- You need quick access to fund your home improvements or portfolio expansion.

- As an investor, you want to buy another property or need money for a deposit.

- You need to fix up your rental property but don’t have the cash right now.

Benefits of Second Charge Mortgage for Buy To Let Properties

The benefits of second charge mortgages for buy-to-let investments can be particularly appealing under certain conditions.

- You can get more money without changing your current good mortgage deal.

- Typically lower arrangement fees compared to a full remortgage.

- You can avoid early repayment fees, which can be high.

- It’s often faster and more flexible than remortgaging.

- You can borrow up to 75% of your property’s value.

Remember, while these advantages are significant, they should be weighed against your specific financial circumstances and investment goals.

Assessing the Risks: A Cautious Approach

Second-charge mortgages can be a risky investment, so it’s important to understand the risks involved before taking one out. These risks include:

- The primary lender may not agree to a second charge mortgage, as it increases their risk.

- You will need to ensure that your rental income is sufficient to cover your mortgage repayments.

- Second-charge mortgages typically have higher interest rates than primary mortgages.

- If you cannot repay your second charge mortgage, you could lose your property.

When considering a second-charge mortgage, it’s wise to consult with a financial advisor to fully understand these risks and how they apply to your specific situation.

How to Qualify for a Buy-to-Let Second Mortgage?

To qualify for a buy-to-let second charge mortgage, you will need to:

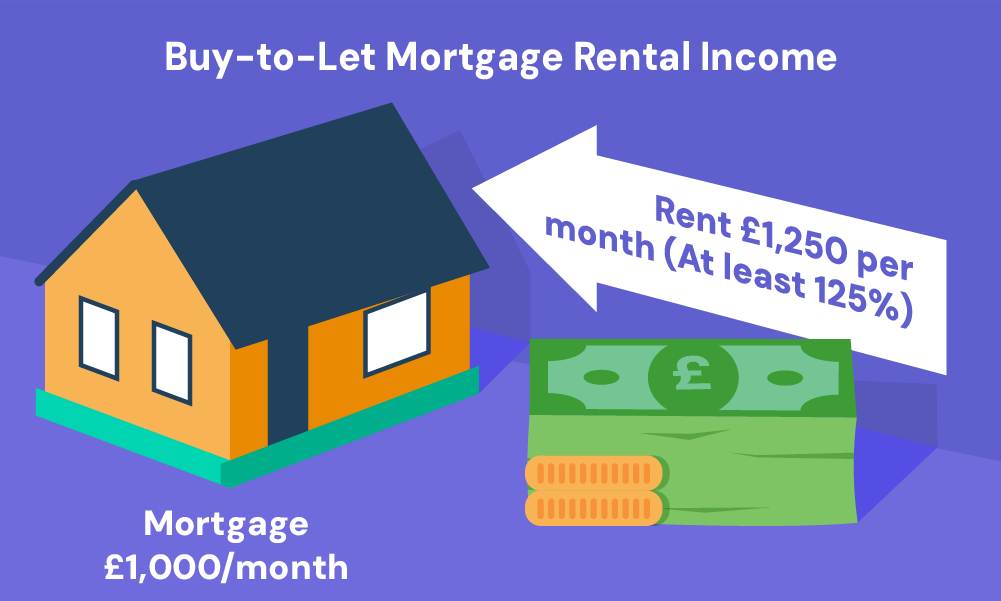

- Rental income – Your rental income should cover at least 125% of your total mortgage payments.

- Deposit and equity – You need a deposit of 20-25% of the property value and substantial equity in the property.

- Property type and LTV – Some types of properties, such as flats above shops, may be restricted. Lenders will also look at the loan-to-value (LTV) ratio, which is the amount you borrow as a percentage of the property value. A higher LTV may mean higher interest rates.

- Borrower’s income and credit history – Your income is also considered, and you will need a good credit history.

- Portfolio size, age, and circumstances – Lenders may limit the number of properties you can own. They will also consider your age and personal circumstances.

- Additional fees and economic factors – There are additional costs, such as arrangement fees and valuation fees. Interest rates and market conditions can also affect lenders’ decisions.

To increase your chances of getting a mortgage, talk to a financial adviser. They can help you meet the criteria and find the best deal for you.

What Are the Costs Involved in a Second Charge Mortgage for Buy-to-Let?

Before taking out a second charge mortgage, it’s important to understand the various costs involved:

- Arrangement fees. Lenders often charge an arrangement fee for setting up the mortgage. This fee can range from 1% to 2% of the loan amount.

- Valuation fees. Lenders often require a valuation of the property to determine its worth. The cost can range from £150 to £1,500.

- Legal fees. There are legal costs involved in setting up a second-charge mortgage, which can range from £500 to £1,000.

- Broker fees. If you use a broker to find your mortgage, they may charge a fee for their services. This fee is typically around 1% to 1.5% of the loan amount.

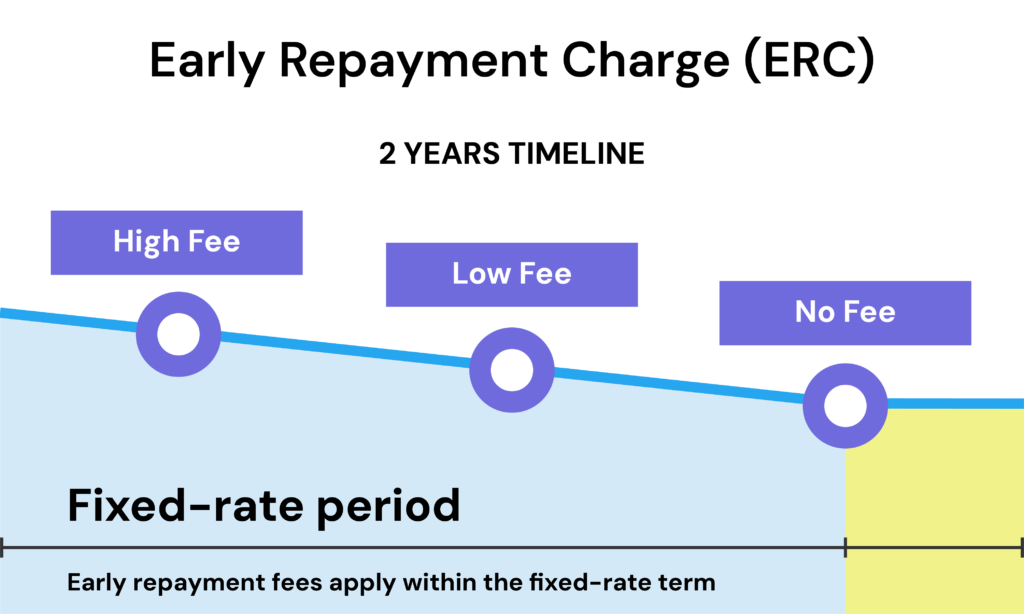

- Early repayment charges. If you decide to pay off your mortgage early, there may be a charge for this. The amount varies but can be a percentage of the outstanding loan or a number of months’ interest.

It’s important to factor in all these costs when considering a second-charge mortgage. They can add up and significantly impact the overall cost of the loan.

Always ask your lender for a detailed breakdown of all charges before proceeding.

What are the Interest Rates to Expect?

Second-charge mortgage interest rates are usually higher than primary mortgage rates. They typically range from 2% to 3% above the Bank of England’s base rate.

The interest rate you are offered will depend on how well you meet the lender’s risk criteria.

This means that one lender may offer you a higher rate or deny your application, while another may offer you a more competitive rate.

You may find either interest-only or capital-repayment mortgages. Your choice should depend on your current financial situation and future goals.

Interest-only mortgages can be attractive if you plan to sell your property soon, refinance your mortgage, or use other assets to pay off the loan.

How To Find the Right Mortgage Lender?

Many lenders are offering Buy-To-Let (BTL) second-charge mortgages.

While well-known banks like Barclays and Santander offer these loans, you may find a better rate with a specialist lender.

Specialist lenders often have lower interest rates but may not have a high-street presence. Many specialist lenders work primarily through referrals and do not accept applications directly.

It is important to explore different options and possibly seek professional advice to find the lender that best suits your individual needs.

How to Find The Best Buy-To-Let Second Charge Mortgages?

Finding the best second-charge mortgage deals for buy-to-let properties is a bit like shopping around for the best deal on anything else.

You want to compare interest rates from different lenders but don’t forget to also look at the fees. These can vary between lenders and add a lot to the overall cost of your mortgage.

It’s also important to think about the flexibility that different lenders offer. Some might let you make overpayments without penalties or give you the option to only pay interest for a certain period.

This flexibility can be important depending on what you’re trying to achieve with your investment property.

One of the best ways to find the right deal is to talk to a buy-to-let mortgage broker.

These brokers are experts in the market and have access to a wide range of mortgage products, some of which you might not be able to find on your own.

They can give you personalised advice based on your finances and investment goals.

A broker can also save you time and effort in finding the right deal and can often negotiate better terms on your behalf.

They can do this because they have relationships with lenders and know the ins and outs of the mortgage industry.

Remember, the best deal isn’t just about getting the lowest interest rate. It’s also about getting a mortgage that fits your overall financial and investment plans.

The Bottom Line

If you’re looking to invest in a buy-to-let property and are considering a second charge mortgage, it’s highly recommended to consult with a qualified mortgage advisor.

They can provide you with tailored advice, help you understand the various options available, and assist you in finding a mortgage deal that aligns with your investment strategy.

Unsure where to find the right mortgage advisor? Simply, reach out to us. We’ll take the hassle out of your endless research and connect you with an FCA-qualified broker who specialises in buy-to-let mortgages.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What is the difference between a second-charge mortgage and a second-home mortgage?

A second-charge mortgage is different from a second home mortgage because of what they’re used for and how they’re set up.

A second charge mortgage is a loan you take against the value of your property, sitting behind your first mortgage. You usually use this kind of mortgage to borrow more money against your current house.

On the other hand, a second home mortgage is for buying another property besides the one you already live in. This could be a holiday home or another house you want to rent out.

The main difference is that a second charge mortgage is borrowing more on your existing house, while a second home mortgage is for buying a completely different property.

Can I have more than one second charge mortgage on a buy-to-let property?

Yes, you can have more than one second charge mortgage on your buy-to-let property.

If you get another mortgage after the second one, these are called third-charge mortgages, and so on. It’s not very common, but some lenders do offer them.

Because these situations can be quite tricky and there’s more risk, it’s really important to talk to a specialist broker.

They know the right people and have the know-how to help you find the right mortgage for your situation.

Just remember, getting more mortgages means more financial risk, so it’s wise to think it through carefully and get good advice from experts.

Related Articles

A Quick Guide to Find the Best Second Mortgage Rates

Second charge mortgages let you borrow money using the value of your home, on top of your first mortgage. The interest rates are usually higher because lenders take more risk—they get paid back after your first mortgage if you can’t keep up with payments. These loans are regulated to protect borrowers and are often used […]

How To Find the Right Second Charge Mortgage Lenders?

Life throws curveballs, and often, they come with a price tag. Home improvements, debt consolidation, or big life events – they all need funds. As a homeowner, you’ve got a powerful option at your disposal: second charge mortgages. These loans let you tap into your home’s equity without touching your first mortgage. The landscape for […]

Second Charge Mortgage Calculator – Get a Quick Quote

You’re looking to borrow more money using your home, and a second charge mortgage might just be what you need. In the UK, these mortgages let you borrow from a few thousand pounds up to larger amounts, depending on your home’s value and how much you still owe on your first mortgage. How much exactly? […]