- What is a Joint Loan?

- Why Consider a Joint Loan?

- How Does a Joint Loan Work?

- Can You Take Out a Joint Personal Loan?

- Key Terminology for Joint Loans

- Who Can Get a Joint Loan?

- What to Think About Before Getting a Joint Loan

- Pros and Cons of Getting a Joint Personal Loan

- Can I Get Joint Loans with Bad Credit?

- How To Use Joint Loans?

- How To Pick the Best Joint Personal Loan?

- The Bottom Line

How To Get Joint Loans with Bad Credit: An In-Depth Look

Imagine you and your friend are craving a pizza, but neither of you has enough money to buy it on your own.

What do you do? You chip in together, and voila! Pizza is served.

A joint loan works pretty much the same way, but instead of pizza, you’re aiming for something bigger like a new car or a home renovation.

In a joint loan, two or more people come together to borrow money. The primary benefit? You often get better terms—like higher loan amounts and lower interest rates—because there’s less risk for the lender.

Your combined income makes you a stronger candidate for a loan, but there’s also a catch: both of you are responsible for paying it back.

If you’ve ever wondered what a joint loan is, how it works, and whether it could be a fit for you, then this guide is for you.

What is a Joint Loan?

As discussed, a joint loan is a loan that you and someone else — a partner, friend, or family member — apply for together.

Whether you’re dreaming of a new car or planning to refurbish your kitchen, a joint loan could help you get more funding than you could alone.

But that’s not the only advantage. With shared responsibility, the loan becomes less risky in the eyes of the lender, opening doors to higher amounts and better interest rates.

In simple terms, two heads can be better than one.

Why Consider a Joint Loan?

Bigger Loans, Better Rates

The major perk of a joint loan is the potential for a more favourable loan package. When you apply together, lenders look at both of your incomes.

Simply put, more income means you can borrow more money. Plus, lenders often see joint loans as less risky, which could translate to a lower interest rate for you.

Shared Responsibility

You’re not in this alone. With a joint loan, both parties are equally accountable for repaying the amount borrowed.

That means if life throws a curveball and one of you can’t make a payment, the other is there as a safety net.

How Does a Joint Loan Work?

Just like any other loan, you borrow a sum of money and repay it in monthly chunks, plus interest. But here’s where it gets interesting.

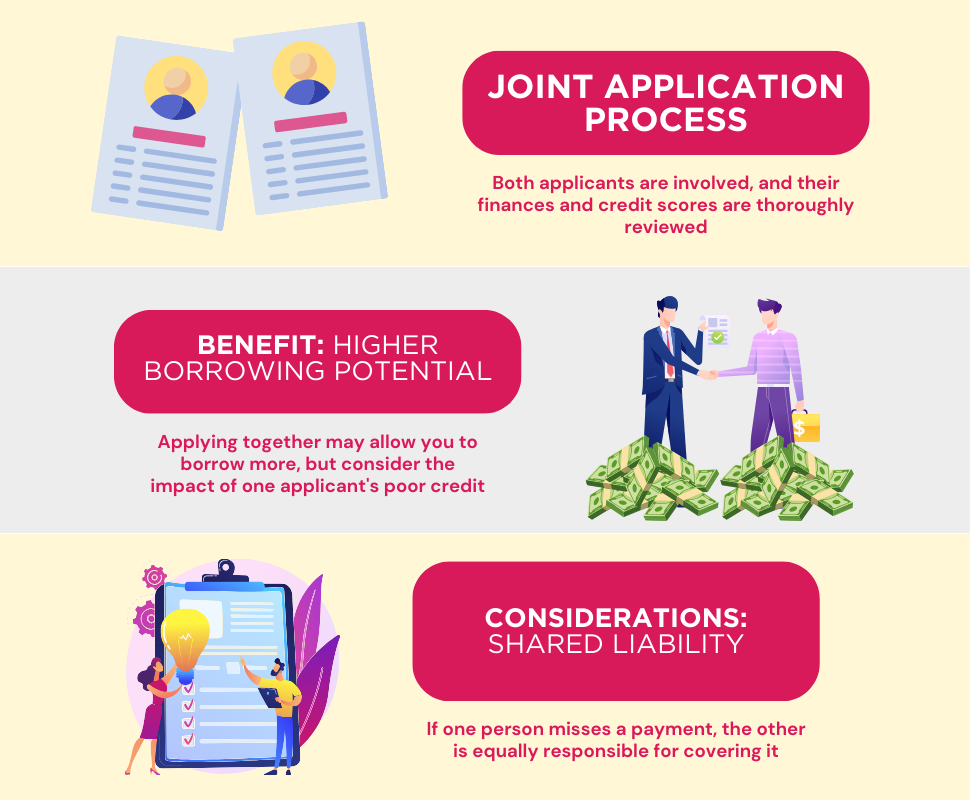

When you apply for a joint loan, both applicants have to roll up their sleeves and get involved in the application process. Your financial backgrounds, credit scores, and incomes are all up for review.

The best part? Teaming up often means you can borrow more money. But be careful if one of you has a poor credit score; it might be a deal-breaker for the lender.

And remember, this is a full-on partnership. If your loan buddy misses a payment, the lender will expect you to cover it.

This is called “joint and several liability,” which simply means you’re both on the hook for the full loan amount, not just half.

Can You Take Out a Joint Personal Loan?

Yes, you can.

Lenders often offer personal loans designed for two people. You and your co-applicant share the task of paying it back, which also boosts your chances of getting the green light from the lender.

Unsecured Joint Loans

Think of unsecured loans as the everyday personal loans offered by most banks. You can typically borrow between £1,000 and £25,000.

The repayment time? Usually from 1 to 5 years. And the best part is, you don’t need to put up any collateral like a house or car.

Secured Joint Loans

In the secured loan arena, you’ll need to pony up an asset—like your home or family car—as a safety net for the lender. If you can’t pay the loan back, the lender could take ownership of that asset.

The upside? These loans often come with lower interest rates and allow you to borrow more compared to an unsecured loan.

Mortgages

A mortgage is a big-league secured loan, usually aimed at helping you buy a property. For many, teaming up to apply is the only way to get the funds they need for this significant purchase.

Joint Loans for Debt Consolidation

Got different loans cluttering up your financial life? A debt consolidation joint loan might be just what you need.

By pulling all those loans into one, you might snag a better interest rate and make your monthly payments more manageable.

Bad Credit Joint Loans

If both you and your partner have a history of credit hiccups, a joint loan could be your ticket to approval. The lender might see you as more reliable together than you would be separately.

Bank Account Overdrafts

A joint bank account overdraft is like a loan in disguise. Both account holders are on the hook for paying back whatever you borrow.

Key Terminology for Joint Loans

- APR (Annual Percentage Rate) – APR stands for Annual Percentage Rate and it’s a big deal when it comes to any loan. It gives you a complete picture of how much your loan will cost annually, including both interest and fees. Here’s the kicker: lenders only have to give the advertised APR to about half of the borrowers. So, even if you see a low APR advertised, there’s no guarantee you’ll get it.

- Interest Rate – This is how much you’ll be paying in interest on your loan. Interest rates can be either fixed or variable. A fixed rate is stable, it doesn’t change. On the other hand, a variable rate can increase or decrease over time, depending on market conditions.

- Liability – When it comes to joint loans, the term “liability” is crucial. Both you and your co-applicant are fully responsible for paying back the whole loan amount, not just your shares.

- Unsecured Loan – These are loans that don’t require collateral like a house or car. You get approved based on your creditworthiness alone, which makes them a bit riskier for lenders, but potentially quicker to obtain.

Who Can Get a Joint Loan?

Just like any loan, there are boxes you’ll need to tick. You’ll have to:

- Be at least 18 years of age

- Live in the UK

- Own a UK bank account

Different lenders might also have their unique requirements, like a minimum income level. Sometimes, you’ll need to show proof of your relationship with the co-applicant, so be ready for that.

What to Think About Before Getting a Joint Loan

Before you sign on the dotted line for a joint loan, know what you’re getting into. Your credit score will be tied to the other person’s. If they have bad credit, it could hurt your future loan chances.

Also, you’ll both need to pay the loan back, no excuses. If something happens to the other person, like if they pass away, you’ll have to cover the whole bill yourself.

Ask yourself, do you trust this person? How well do you know their money habits? If they can’t or won’t make the payments, you’ll have to take care of it.

Pros and Cons of Getting a Joint Personal Loan

Joint loans can be a great way to borrow money and get better rates, but they also come with some risks. If you are considering a joint loan, it is important to weigh the pros and cons carefully.

Pros:

- Bigger Loan Amounts. With two people applying, you’re more likely to get approved for a larger loan.

- Easier Qualification. If you can’t qualify for a loan on your own, adding a co-borrower could be your ticket to approval.

- More Manageable Payments. Two incomes can make repaying the loan easier on your wallet.

- Better Interest Rates. Two applicants usually mean less risk for lenders, which could result in lower interest rates for you.

Cons:

- Limited Lender Options. Fewer lenders offer joint loans, which could make shopping around for the best terms more challenging.

- Joint Liability. Both of you are responsible for the loan, so if one can’t pay, the other has to pick up the slack.

- Linked Credit Scores. If your co-borrower has a shaky credit history, it could negatively affect your credit score.

- Dual Credit Impact. Missing a payment hurts both your credit scores, not just one.

Can I Get Joint Loans with Bad Credit?

Yes, you can get a joint loan with bad credit. It might even help your chances if both of you have less-than-great credit scores.

But watch out—if one of you has bad credit, it will affect the other person because your credit files are linked.

How To Use Joint Loans?

Joint loans can be used for a variety of purposes, including:

- Paying for education. If you or your child is going to college, a joint loan can be a good way to pay for tuition fees. This can help you avoid dipping into your savings or burdening your child with student loans.

- Financing home renovations. If you own a home with your partner and need to make some renovations, a joint loan can be a smart move. Renovations can be expensive, and a joint loan can help you borrow enough money to cover the costs.

- Consolidating debt. If you have credit card debt or other loans that are making your finances complicated, a joint loan can help you consolidate them into one loan. This can make your payments easier to manage and can potentially save you money on interest.

How To Pick the Best Joint Personal Loan?

When you’re looking to get a joint personal loan, it’s crucial to shop around. Don’t just go with the first deal you see; compare different options. Here’s how you can do it effectively:

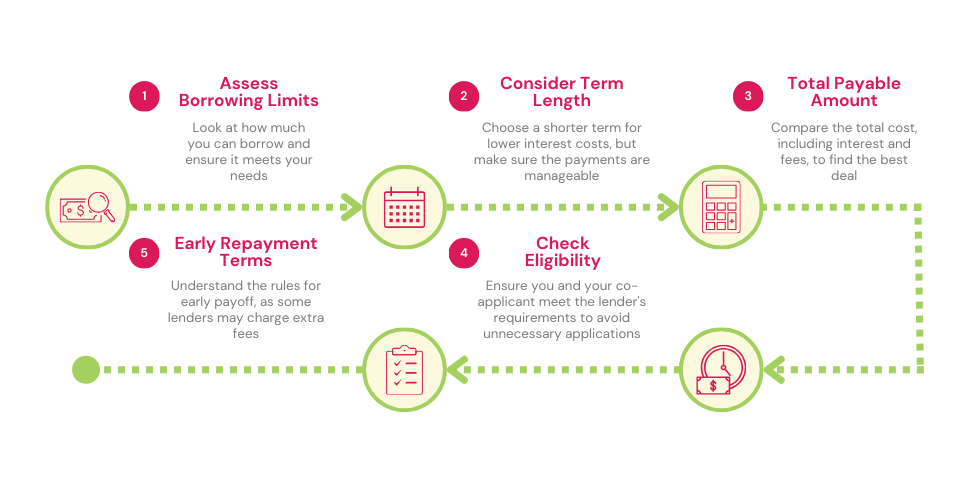

1. Look at How Much You Can Borrow

Pay attention to the most money each lender will let you borrow. Consider this along with the length of time you have to pay it back and the interest rate.

2. Mind the Term Length

Aim for the shortest loan term where you know you can make the monthly payments. The quicker you pay it back, the less you’ll spend on interest in the long run.

3. Check the “Total Payable” Amount

This is the full amount you will pay back to the lender, including the loan amount, interest, and any extra fees. Use this number to compare which loan is the best deal for you.

4. Check Eligibility Requirements

Most lenders will list the basic requirements you need to get a personal loan. Don’t bother applying if you and your co-applicant can’t meet these.

Too many loan applications in a short time can make you look risky to lenders, making it harder to get approved later.

5. Factor in Early Repayment

If you plan to pay off the loan early, see what the lender’s rules are about that. Some might charge extra fees for early repayment.

Even if you decide to pay off a part of the loan ahead of time, remember both of you are still responsible for the rest.

The Bottom Line

Getting a joint loan has its perks. You might borrow more money and get a lower interest rate. But, you’ve got to think this through.

Both of you are responsible for the full loan, so talk over the risks with your partner first.

Using a broker can give you an edge in the loan process. Brokers know the lending market inside and out, and they can often find you better deals and terms than you could find on your own.

This is especially helpful if you have bad credit since brokers know which lenders are more lenient.

When you’re ready to start, contact us. We’ll match you with a broker who can guide you through the loan process step-by-step, explain any confusing terms, and help you get approved.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can you get a joint credit card?

Nope, in the UK, you can’t have a joint credit card. You can have multiple cardholders, but one person has to handle paying off the debt.

What happens to your joint loan if the relationship ends?

Even if you break up, you both still owe the loan money. You usually can’t just remove yourself from the loan. After you’ve paid it off, check your credit report to make sure you’re financially unlinked from your ex. If you’re still linked, call the big three credit agencies (TransUnion, Experian, Equifax) to get that fixed.

Related Articles

Secured Loan Calculator – No Personal Details Required

If you’re sitting on a valuable asset like a home, why not put it to work for you? Secured loans can open doors to more funds, better repayment terms, and even loan approval when all other avenues fail. But remember, there’s a flip side: you could lose your prized asset if you don’t keep up […]

Loans for Pensioners: How to Get the Cash You Need?

Suppose you’ve reached retirement and find that, despite having assets in property or a robust pension plan, your daily cash flow isn’t quite as fluid. In that case, you may contemplate taking out a loan for things like home renovations, a new car, or even a well-deserved holiday. And why not? If you have a […]

How To Get a Secured Loan If You’re Self Employed

Starting a business takes courage, hard work, and, let’s be honest, money. Whether you want to launch a new product, buy better tools, or make your workspace bigger, a secured loan could help you make it happen. Finding a loan when you don’t have a regular job can feel tricky. But here’s the good news: […]