- What is a Self-Build Mortgage?

- Types of Self-Build Mortgages

- Why Choose a Self-Build Mortgage?

- What Are the Challenges of a Self-Build Mortgage?

- Can You Get a Self-Build Mortgage for Land You Already Own?

- How Much Do You Need For a Self-Build Project?

- How Lenders Release Finances for Self-Build Projects

- Key Considerations Before Getting a Self-Build Mortgage

- How Do You Get a Self-Build Mortgage?

- Who Offers Self-Build Mortgages?

- What Interest Rates Can You Expect for a Self-Build Mortgage?

- What are BuildLoan and BuildStore Services?

- How To Qualify for a Self Build Mortgage?

- Exploring Alternative Financing Options

- Key Takeaways

- The Bottom Line

Can You Get a Mortgage to Build a House in Your Own Land?

Building a home on your own land in the UK is an opportunity to turn your dream into a reality.

It’s about more than just construction; it’s a personal journey.

You get to design every detail to suit your taste and lifestyle, from the floor plan to the choice of materials. This approach not only brings your vision to life but can also be cost-effective.

Managing the build allows you to control expenses, often leading to significant savings.

For many, this is a chance to achieve a lifelong ambition, crafting a unique space that truly feels like home.

This guide is here to help you navigate this exciting journey, making your dream home a reality on your land.

What is a Self-Build Mortgage?

A self-build mortgage is designed for building your home. Unlike standard mortgages, which provide a single lump sum to buy an existing house, self-build mortgages release money in stages.

This way, you get funds when you need them during construction. It’s a smart way to manage your budget and keep your building project on track.

With a self-build mortgage, you get the flexibility to design and construct your house while the lender ensures their investment is protected by releasing funds for each completed stage of your build.

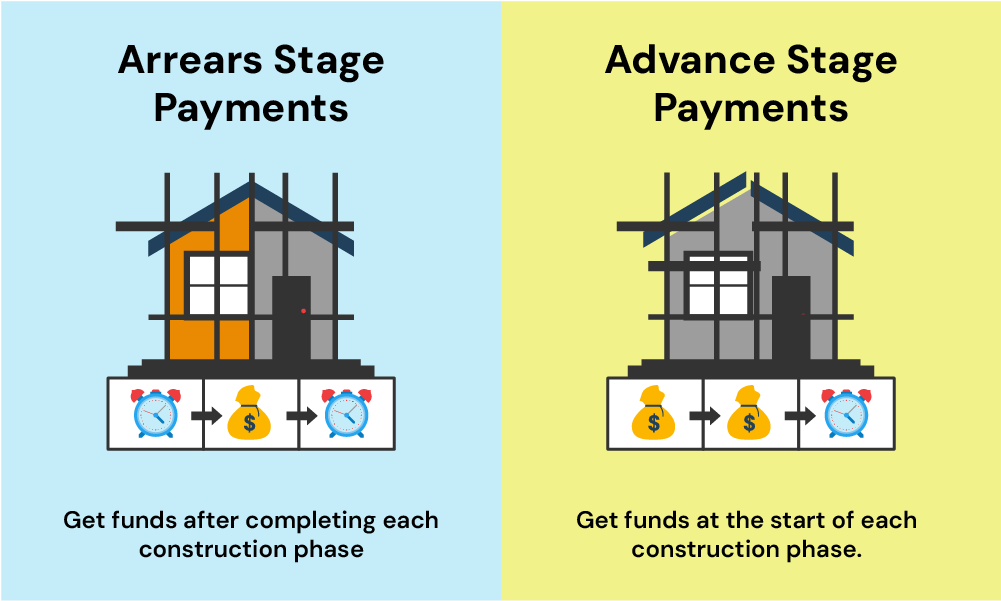

Types of Self-Build Mortgages

In the UK, self-build mortgages come in two main types, each suited to different stages of your building project.

1. Arrears Stage Payments

This is the most common type of self-build mortgage. Here, you receive payments at various stages of the build, but only after each stage is completed.

It’s great if you have enough savings to cover upfront costs because you pay for each phase before getting reimbursed.

Typical stages include laying the foundations, making the property watertight, and completing the interior.

2. Advance Stage Payments

This type is less common but can be very helpful. With this mortgage, you get funds at the start of each stage, not at the end.

This means you have cash available when you need it to begin each phase of construction. It’s a good option if you don’t have a large amount of savings to use as upfront costs.

It’s important to choose the one that aligns best with your cash flow needs and how you intend to manage the project.

Remember, no matter which type you choose, you’ll need detailed plans and a clear budget to get started.

Why Choose a Self-Build Mortgage?

If you want to have more control over your home design and construction, a self-build mortgage can help you secure the funds.

Here are some benefits you could enjoy:

Cut Down on Stamp Duty Costs

With a self-build mortgage, you can save on stamp duty.

You only pay this tax on the land if its cost is above £125,000, not on the building work or the finished property. This usually means less stamp duty compared to buying a ready-made home.

Control Your Spending

Building your own home gives you control over the budget. You can make cost-effective choices, such as sourcing materials or hiring contractors.

By managing these aspects, you might spend less compared to buying a ready-made house. It’s all about planning smartly and keeping a keen eye on your expenses.

Boost Your Home’s Value

Often, the final value of a self-built home is more than the total spend on land, materials, and building costs.

This means, that once completed, your home could be worth more than it costs to create, giving you a potentially higher property value.

What Are the Challenges of a Self-Build Mortgage?

While self-build mortgages offer great opportunities, they also come with their own set of challenges. It’s important to understand these potential drawbacks to know if this is the right one for you:

Be Aware of the Risks

Building your own home comes with risks.

Costs can overrun, and construction might take longer than expected. It’s important to plan well and be prepared for any unexpected challenges.

Consider the Higher Costs

Self-build mortgages often require a larger deposit and come with higher interest rates.

This means you’ll need to have a good amount of money saved up to start, and the total cost over the mortgage period could be higher.

Prepare for the Time Commitment

Building a house is a time-intensive project. From securing the land to completing the construction, it requires patience and good project management.

Be ready to invest time and effort to bring your dream home to life.

Can You Get a Self-Build Mortgage for Land You Already Own?

Yes, you can get a self-build mortgage if you already own the land. In fact, owning your land can be a plus point.

It often means you need to borrow less, as part of the project cost – the land – is already covered. When you apply for a mortgage, lenders will consider the value of the land as part of your contribution to the project.

However, keep in mind that lenders will look at several factors. They’ll check if the land has planning permission, which is crucial. They’ll also assess if the land is suitable for building.

So, if you’ve got land and are thinking about building your home on it, having these details sorted can make it easier to secure a self-build mortgage.

How Much Do You Need For a Self-Build Project?

The amount you’ll need to borrow for your self-build project varies. It depends on several factors – the cost of the land (if you haven’t already got it), construction costs, and your project’s overall scale and complexity.

Typically, lenders offer up to 75% to 80% of the project cost, which includes both land purchase and building expenses.

You’ll need to work out the total expected cost of your project first. This includes everything from materials to labour costs.

Once you have a figure, you can then estimate how much you need to borrow. Remember, the more accurate your cost projections are, the smoother the borrowing process will be.

It’s also important to have a contingency fund, as construction projects can often go over budget.

How Lenders Release Finances for Self-Build Projects

When you take out a self-build mortgage, lenders don’t give you all the money upfront.

Instead, the funds are released in stages as your building project progresses. This way, lenders make sure that the money is being used effectively for each stage of construction.

Typically, these stages are:

- Buying the land (if you haven’t already).

- Laying the foundations.

- Building to the watertight stage (roof on, windows in).

- Getting the interior done, like plastering and wiring.

- Completion Stages: Some lenders further subdivide this phase into:

- First Fix – Floors, ceilings, basic wiring, and plasterwork are installed.

- Second Fix – Doors, fitted kitchens and bathrooms, and electrical fixtures like lights and switches are added.

- Final Certification – Upon successful inspection of all completed work, the remaining funds are released, marking the project’s official completion.

You’ll usually get the money after each stage is finished and inspected. Some lenders offer the funds in advance for each stage, which can be helpful if you need cash to start the next phase.

Remember, each payment is subject to an inspection to ensure the work is done right.

Key Considerations Before Getting a Self-Build Mortgage

Check Land Suitability for Construction

It’s essential to confirm your land is fit for building. Have a chartered surveyor assess things like soil condition, access to services, and flood risk.

This step is crucial before you start planning or applying for a mortgage, as lenders will want proof that your land is suitable for construction.

Secure Planning Permission

Before you begin your build, you must have planning permission. This is your legal green light to start construction.

Lenders will need to see this permission before they consider your mortgage application. Remember, without it, your building project can’t legally proceed.

Work with the Right Professionals

Partnering with a skilled architect and builder is key. They will help you bring your vision to life, ensuring your plans are practical and within budget.

Your choice of professionals can greatly influence the success of your project, and lenders may require their credentials to ensure the viability of your plan.

Choose Your Construction Type

Decide on the type of construction for your home. Whether it’s a traditional brick house, a timber frame, or a more unconventional design, your choice will impact both the cost and the construction timeline.

Keep in mind that some lenders may be hesitant to finance non-standard types of construction, so consider consulting a broker to find a suitable lender.

Plan for Instalment-Based Financing

Understand that self-build mortgages are released in stages, not as a single lump sum.

You’ll need to plan your finances to cover each phase of the build until the next portion of the mortgage is released.

This requires careful budgeting and financial management throughout the construction process.

How Do You Get a Self-Build Mortgage?

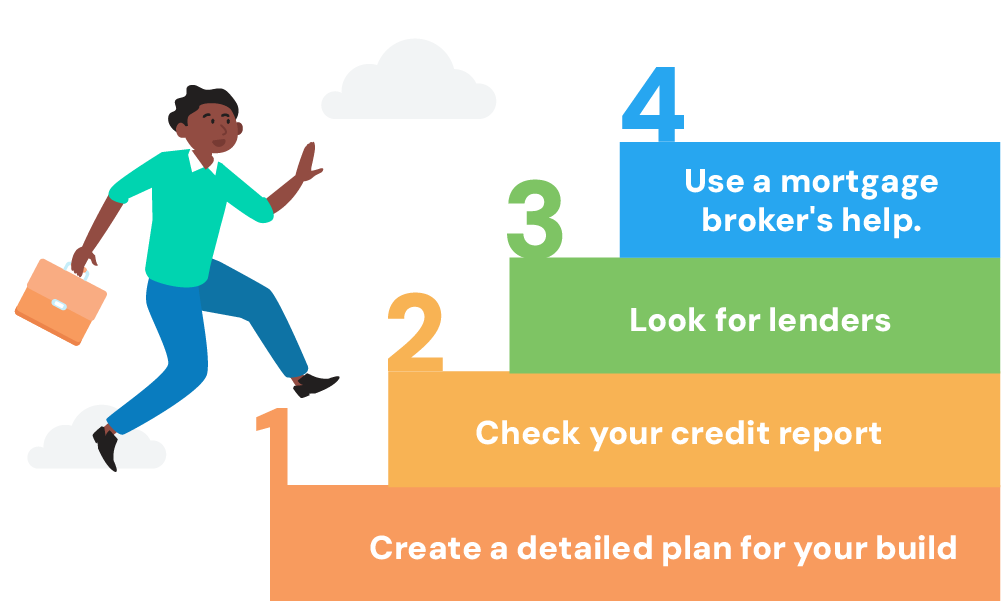

Getting a self-build mortgage involves several key steps.

First, create a detailed plan for your build, including costs, timelines, and designs. This demonstrates to lenders that you have a well-thought-out project.

Next, check your credit report to ensure it accurately reflects your financial situation. A good credit score is crucial for improving your chances of approval.

Then, it’s time to look for lenders. Compare their terms and interest rates, focusing on those who specialise in self-build projects as they’ll better understand your specific needs.

When preparing your application, include your building plans, cost estimates, and proof of planning permission.

Being well-prepared and ready to answer questions about your project and finances will make the process smoother.

One of the best moves to make everything easier and less stressful is to use a self-build mortgage broker.

They can guide you through the process and help find the right lender for your project. To get connected with an expert who specialises in your situation, simply send us an enquiry.

Who Offers Self-Build Mortgages?

When it comes to self-build mortgages, not all banks and building societies have these products.

Major banks like Barclays, HSBC, Nationwide, and NatWest typically don’t offer self-build mortgages, nor do some of the largest mortgage specialists such as Accord or Aldermore.

However, lenders like Halifax and Together, along with several smaller building societies, do provide these mortgages.

Their offerings differ significantly, especially in terms of funding release and loan amount decisions. It’s advisable to speak to an expert before applying to ensure the product meets your needs.

Specific lenders include:

- Ecology Building Society is known for supporting sustainable and eco-friendly self-build projects.

- Furness Building Society, which accepts applications via BuildLoan with specific loan-to-value ratios.

- Halifax offers considerations for loans that don’t exceed the total cost of land purchase and building.

- Scottish Building Society, catering to customers in Scotland and the North of England with specific loan ranges.

- Newcastle Building Society, provides mortgages through BuildStore with a maximum limit based on the loan-to-value at the end of the build.

- Lloyds offers tailored loans to suit different project timelines.

- AIB(NI) in Northern Ireland, offers mortgage options for self-build homes up to a certain loan-to-value ratio.

What Interest Rates Can You Expect for a Self-Build Mortgage?

When you’re looking into self-build mortgages, expect the interest rates to be a bit higher than standard mortgages.

Because these projects are often seen as riskier by lenders. The rates can vary, but generally, they’re around 1% to 2% higher than the average mortgage rate.

The table below gives a glimpse of what some lenders might offer.

Remember, these are just examples, so the actual deal you get could be different.

Your interest rate, monthly payments, and total costs will depend on things like your credit score, the amount you borrow, and the lender’s criteria.

These examples are based on a 2-year repayment period, with fees included in the overall cost.

| Lender | Product | Rate | Max LTV | Fees | Initial Payment | Total Repayment | Mortgage Term |

|---|---|---|---|---|---|---|---|

| Hanley Economic | Discounted Variable | 5.75% | 60% | £1,498 | £1,120 | £28,778 | 2 years |

| Penrith Building Society | Discounted Variable | 5.99% | 75% | £750 | £1,146 | £28,608 | 2 years |

| Saffron Building Society | Discounted Variable | 5.99% | 75% | £890 | £1,146 | £29,098 | 2 years |

| Suffolk Building Society | Discounted Variable | 6.09% | 80% | £1,198 | £1,157 | £29,208 | 2 years |

It’s important to compare rates from different lenders. Interest rates can depend on factors like how much you’re borrowing, your repayment plan, and the lender’s policies.

Remember, even a small difference in the rate can have a big impact over time. So, take your time to shop around and find the best rate for your situation.

What are BuildLoan and BuildStore Services?

BuildLoan and BuildStore are services that cater to your needs if you’re planning a self-build project.

BuildStore offers support throughout your self-build journey. It helps you with finding land, arranging finance, and even guides you in the process of obtaining planning permission and selecting an architect.

This service is about providing you with the necessary tools and advice to navigate the self-build process more effectively.

BuildLoan is connected to BuildStore and specialises in the financial side of self-build projects. It acts as an intermediary, giving you access to a variety of mortgage options specifically designed for self-builds.

These options are typically not available directly from mainstream lenders.

BuildLoan’s role is to bridge the gap between you and these specialised mortgage products, making it easier for you to find a financial solution that fits your project’s needs.

Both BuildLoan and BuildStore are focused on the specific requirements of self-build projects. They offer expertise in areas that might be new or challenging for you, making your self-build venture more manageable and less daunting.

How To Qualify for a Self Build Mortgage?

When applying for a self-build mortgage, lenders will assess several factors.

They typically require a larger deposit than standard mortgages. You might need at least a 25% to 40% deposit. In some cases, your land can even count as part of your deposit.

The type of property you plan to build also influences eligibility. Some lenders might not finance certain types of construction, like timber frame buildings.

They’ll also look at the projected length of your construction. Most prefer projects that can be completed within two years, as longer builds increase risk.

Your age and income source are also considered. Most lenders prefer applicants aged between 21 and 70, but there are exceptions.

If you’re self-employed or a contractor, your mortgage options might be limited but not impossible.

Lastly, a good credit history helps, though a less-than-perfect score doesn’t automatically disqualify you.

Exploring Alternative Financing Options

If a self-build mortgage isn’t the right fit for you, there are other financing routes to consider:

- Remortgaging Land or Property – If you already own land or another property, remortgaging can release capital to fund your build. This is often a practical option to gather the necessary funds.

- Help to Build Scheme – This government scheme can boost your deposit, making it easier to secure the needed funds, especially if you already own the land.

- Personal Loans – For smaller projects or to cover specific stages of your build, a personal loan might be suitable. It’s a viable option if you intend to live on the property.

- Commercial Finance – If your self-build is for business purposes, you might explore options like commercial development finance or joint venture property development finance.

- Bridging Loans – These are short-term loans that cover your costs until you secure long-term financing. They’re particularly useful if you expect to sell the property quickly after completion or transition to a regular mortgage.

Each of these alternatives has its benefits and considerations. It’s important to weigh them against your financial situation and project needs.

Key Takeaways

- A self-build mortgage funds the construction of your home, releasing money in stages as each part of the build is completed.

- You can choose arrears payments (money after each phase) or advance payments (money before each phase).

- If you already own the land, you can get a self-build mortgage to cover construction, with the land value considered as part of your project contribution.

- Lenders typically release funds in stages: buying land, laying foundations, making the structure watertight, and finishing the interior.

The Bottom Line

Securing the right mortgage for your self-build project can seem complicated. This is where a mortgage broker becomes essential.

They help navigate through various lenders, interest rates, and eligibility criteria to find what best suits your project.

A skilled broker not only understands your specific needs but also works to ensure you get the most suitable mortgage option

If you want to save time and reduce stress in your search for the right broker, reach out to us. We can connect you with an FCA-qualified broker who’s experienced in self-build mortgages and ready to help with your specific situation.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can land be used as a deposit?

Yes, in many cases, the land you own can be used as part of your deposit for a self-build mortgage. If you already own the land outright, its value is often factored into the loan-to-value calculation.

Is it possible to get a mortgage for a building site?

Yes, it’s possible. These are typically called land mortgages and are designed specifically for buying a building site. The availability and terms will depend on the lender.

How to transition to a standard mortgage after completion?

Once your build is complete and the property is habitable, you can switch to a standard mortgage. This process is known as remortgaging and allows you to potentially get lower interest rates.

What are the steps to carry out a self-build?

The steps include planning your project, securing planning permission, finding suitable land, arranging finance (like a self-build mortgage), and then overseeing the construction process.

What are your tips for ensuring approval for a self-build mortgage?

To improve your chances of approval, have a clear and detailed build plan, a realistic budget, and any necessary permissions. Also, keep a good credit score and save for a sizable deposit. Seeking the help of a mortgage broker can also be beneficial.

Related Articles

First-Time Buyer’s Guide to Self Build Mortgages

More and more people are choosing to build their own homes these days. It’s a great way to save money and bring your dream home to life. Imagine that perfect bedroom with a walk-in closet or your ideal kitchen – it’s all within reach. But before you get lost in the excitement of planning your […]

Should You Use Self-Build Mortgage Advisors?

Understanding self-build mortgages is essential if you’re considering building your own home in the UK. A self-build mortgage is different from standard mortgages, and having a specialised mortgage advisor can significantly benefit your project. These advisors have the expertise to guide you through the unique financial landscape of self-building, ensuring your project remains feasible and […]

How To Get Self Build Mortgages in Scotland?

Planning to build your dream home in Scotland is an exciting adventure. Imagine creating a home that’s completely yours, from the very first brick to the final splash of paint. But before you can make that dream a reality, there’s one important thing you’ll need to sort out: a self-build mortgage. Getting this type of […]