- What Are Self-Build Mortgages?

- How Do Self-Build Mortgages in Northern Ireland Compare to Other UK Regions?

- What Financial Support Is Available for Self-Builds in Northern Ireland?

- How Can You Obtain a Self-Build Mortgage in Northern Ireland?

- Who Offers Self-Build Mortgages in Northern Ireland?

- What Are the Interest Rates for Self-Build Mortgages in Northern Ireland?

- The Bottom Line

How To Get Self Build Mortgages in Northern Ireland?

Building your own home in Northern Ireland is an exciting journey, but it’s not without its challenges.

You have to choose architects, get planning permissions, work with builders, and most importantly, sort out your finances.

These steps are crucial, but they can be overwhelming, making your dream project seem like a huge task.

You may feel swamped by the number of decisions and processes involved.

Every stage of home building, from the design to meeting legal requirements, has its unique challenges.

A critical part of this process is securing the right financial support for your project.

This guide is crafted to make things easier for you. We’re going to explain how self-build mortgages work in Northern Ireland.

You’ll learn about the different stages of applying, what lenders look for, and how to manage the financial side of building your home.

Let’s get started.

What Are Self-Build Mortgages?

Self-build mortgages are special loans designed for people who want to build their own homes.

Unlike standard mortgages, where you get the entire loan amount upfront to buy a house, self-build mortgages release money in stages.

As you build your home, you receive funds at key points, like after laying the foundations or completing the roof. This way, the lender ensures the money is spent as planned, and it reduces their risk.

These mortgages are crucial in Northern Ireland’s housing market. They offer a unique opportunity for you to design and create your dream home from scratch.

It’s an attractive option if you can’t find your perfect home on the market or if you wish to have a house tailored to your specific needs and tastes.

How Do Self-Build Mortgages in Northern Ireland Compare to Other UK Regions?

Self-build mortgages in Northern Ireland share many similarities with those in the rest of the UK.

The process of applying, the stage-by-stage funding, and the basic criteria for approval are quite consistent. However, there are some key differences too.

In Northern Ireland, finding a lender might be a bit trickier, as not all UK lenders offer self-build mortgages here. This is partly due to different land laws and property regulations in Northern Ireland compared to other regions.

Additionally, the choice of lenders may be more limited if you’re planning to build in a rural or less-populated area.

Despite these challenges, Northern Ireland offers unique opportunities for self-builders. For instance, you might find more available land or lower prices in certain areas compared to other parts of the UK.

The local councils might have different planning permissions, which could work in your favour, depending on your project.

So, while the basics of self-build mortgages are similar across the UK, in Northern Ireland, you need to be a bit more aware of the local market and regulations.

What Financial Support Is Available for Self-Builds in Northern Ireland?

In Northern Ireland, several financial support options are available to assist you with your self-build project. Let’s break them down.

Microgeneration Technologies Grant

This is a handy scheme if you’re planning to use renewable energy sources, like solar panels, in your self-build. It’s available in certain areas and can significantly offset the costs of installation. Imagine reducing your energy bills while also helping the environment!

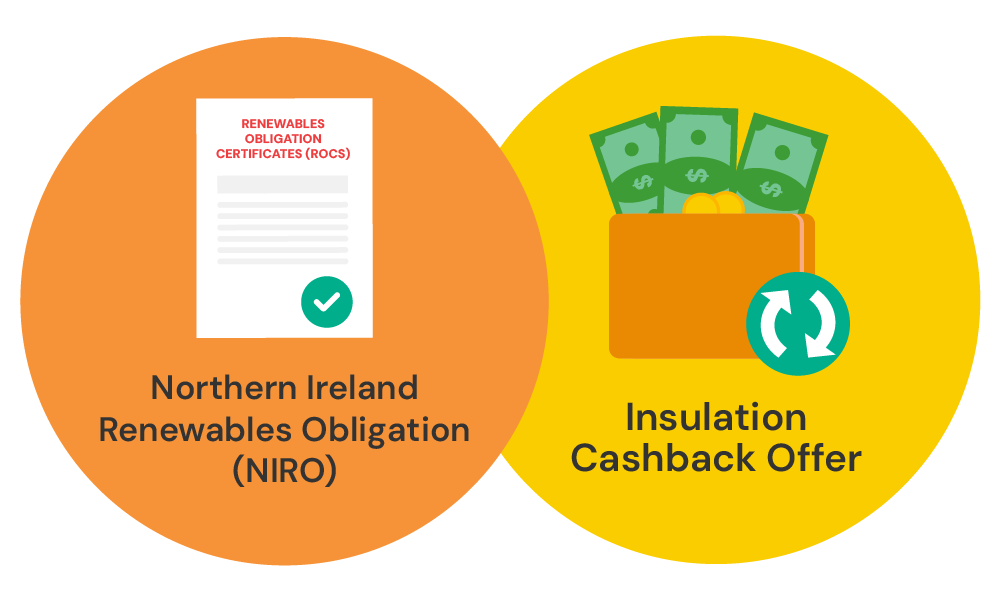

Northern Ireland Renewables Obligation (NIRO)

Under this scheme, you can claim Renewables Obligation Certificates (ROCs) for every unit of electricity your self-built home generates. These certificates can be quite valuable, as you can sell them to electricity suppliers. If you generate more electricity than you use, you can sell the surplus back to the grid, creating an additional income stream to offset your costs.

Insulation Cashback Offer

If your building plans include installing cavity walls or loft insulation, you could be in for some cashback. Spending £300 or more on insulation could make you eligible for a cashback of £250, helping reduce the overall cost of your self-build project.

To access these grants and schemes, you need to meet certain eligibility criteria and complete an application process, which often involves providing detailed information about your project and how it meets energy efficiency standards.

While it might seem like a lot of paperwork, these financial supports can significantly reduce the total cost of your self-build project and make your dream home a reality.

How Can You Obtain a Self-Build Mortgage in Northern Ireland?

Getting a self-build mortgage in Northern Ireland involves several steps.

First, you need to have a clear plan. This includes knowing what your house will look like and how much it’s going to cost.

You’ll need to buy the land first, as self-build mortgages usually don’t cover land purchases.

The key documents you’ll need include planning permission from the local council, detailed building plans, and proof of insurance for your project.

You’ll also need a report valuing your planned home and details about your builders and architects.

Here are a few tips to smooth out the process:

- Be clear about your budget and include extra for unexpected costs.

- Keep all your documents organised and up to date.

- If possible, show that you have experience in managing big projects or construction knowledge. This can reassure lenders that you’re a safe bet.

Remember, each lender has different criteria, so shop around to find the best deal for your situation.

It’s a good idea to talk to a self build mortgage advisor who knows about self-builds in Northern Ireland. They can guide you through the process and help you avoid common pitfalls.

To get started, reach out to us. We’ll pair you up with a good self build mortgage advisor who can make your homebuilding journey easier and less stressful.

Who Offers Self-Build Mortgages in Northern Ireland?

A range of lenders offer self-build mortgages in Northern Ireland, each with its unique terms and criteria. The Progressive Building Society is a key player, focusing exclusively on self-build mortgages in this market.

While mainstream banks like Natwest and Santander are active in Northern Ireland’s mortgage sector, they don’t provide self-build options.

In contrast, banks such as AIB and Danske Bank do consider applications for self-build mortgages.

Finding the right lender involves more than checking if they offer self-build mortgages. You need to understand their specific requirements and terms.

These lenders look at your financial stability, credit history, and how realistic your self-build project is.

They assess your income, savings, and your stake in the project. Their main concern is whether you can pay back the loan and if your construction plan is feasible.

When choosing a lender, think about more than just getting approval. Look closely at their interest rates, repayment terms, and how they release funds during the build. Some might offer lower rates but stricter terms.

Others could be more flexible but charge more. Your aim should be to find a lender whose terms suit your financial situation and the details of your self-build project.

Working with a mortgage broker who knows about self-builds can be really helpful. They can guide you through these choices and help you find the best way to finance your project.

What Are the Interest Rates for Self-Build Mortgages in Northern Ireland?

In Northern Ireland, the interest rates for self-build mortgages usually range between 3% and 7%.

These rates are a bit higher than those for standard mortgages. This difference is because self-build projects are seen as riskier by lenders.

Despite the higher risk, lenders understand that a well-done self-build project can lead to a home worth more than it costs to build. This increase in value can make lenders more willing to give you a better rate.

With self-build mortgages, you have two main options: interest-only or capital repayment. The best choice for you depends on your financial plan and how long your project will take.

After you finish your build, it’s common to refinance your loan. Many people find they can get better terms after the build because their home is now worth more.

The Bottom Line

Consulting a self build mortgage advisor in Northern Ireland can be a real game-changer when you’re looking at self-build mortgages.

These experts understand the ins and outs of the mortgage world. They know about the different lenders, their criteria, and what makes a strong application.

A specialist can guide you through the process, making it less overwhelming. They can help you find the best mortgage deal for your situation, and often, they know how to present your application to increase your chances of approval.

To find a reliable mortgage advisor, get in touch with us. We will connect you with a top mortgage advisor specialising in self build mortgages.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Is it hard to get a self-build mortgage in Northern Ireland?

Getting a self-build mortgage in Northern Ireland can be challenging, but it’s certainly achievable with the right preparation. The key is to have a detailed and realistic project plan, a clear understanding of your budget, and a strong financial background.

Are self-build mortgages more expensive than regular mortgages?

Generally, yes. The interest rates are usually higher because self-builds are seen as riskier. But, the final value of your home can offset this.

What happens if my self-build project goes over budget?

Going over budget can be a common issue in self-build projects. It’s crucial to have a contingency fund, typically around 10-20% of your total budget, to cover unexpected expenses.

If you find yourself over budget, communicate with your lender immediately. They might offer solutions like extending your loan or restructuring your payment plan.

However, be mindful that additional borrowing could lead to higher interest rates or longer repayment terms. Regularly reviewing your budget throughout the project can help you stay on track and manage costs effectively.

Can I do some of the building work myself?

Yes, you can undertake part of the building work yourself in a self-build project. However, this decision can impact your mortgage application.

Lenders often prefer – and sometimes require – that professional builders and contractors carry out the work to ensure quality and adherence to building regulations. If you have relevant skills and qualifications, some lenders might be more flexible.

Make sure to discuss your plans in detail with your lender, as this can affect the release of funds, the overall cost, and the timeline of your project.

Related Articles

First-Time Buyer’s Guide to Self Build Mortgages

More and more people are choosing to build their own homes these days. It’s a great way to save money and bring your dream home to life. Imagine that perfect bedroom with a walk-in closet or your ideal kitchen – it’s all within reach. But before you get lost in the excitement of planning your […]

Can You Get a Mortgage to Build a House in Your Own Land?

Building a home on your own land in the UK is an opportunity to turn your dream into a reality. It’s about more than just construction; it’s a personal journey. You get to design every detail to suit your taste and lifestyle, from the floor plan to the choice of materials. This approach not only […]

Should You Use Self-Build Mortgage Advisors?

Understanding self-build mortgages is essential if you’re considering building your own home in the UK. A self-build mortgage is different from standard mortgages, and having a specialised mortgage advisor can significantly benefit your project. These advisors have the expertise to guide you through the unique financial landscape of self-building, ensuring your project remains feasible and […]