- What is a Mortgage Rate?

- How Do They Work?

- What Interest Rate Should You Expect on a Bad Credit Mortgage?

- How to Get the Best Rate on a Bad Credit Mortgage

- What are the Different Types of Mortgage Rates?

- Other Factors That Determine Your Mortgage Rate

- What is the Easiest Type of Mortgage to Get If You Have Bad Credit?

- Key Takeaways

- The Bottom Line

How Does Bad Credit Affect Your Mortgage Rates?

Having bad credit might make you worry about getting a mortgage with reasonable rates.

But it’s not all doom and gloom. With the right knowledge and steps, you can find mortgage rates that won’t break the bank.

In this article, we’ll show you how bad credit affects your mortgage rates, and share some top tips to help you secure a better deal.

What is a Mortgage Rate?

A mortgage rate is the interest you’re charged for borrowing money to buy a house. It’s a percentage of the loan you take out from a bank or a lender.

The rate you get can greatly affect how much you end up paying back overall.

How Do They Work?

The Impact of Mortgage Rate

If you’ve got a high mortgage rate, you’ll be paying back more money over the life of the loan. On the flip side, a lower rate means you’re shelling out less in the long run.

Your monthly repayments are also affected. Higher rates mean bigger monthly bills and lower rates mean more manageable payments.

Fixed vs. Variable Rates

Mortgage rates can come in two main types: fixed and variable.

With a fixed rate, your interest rate won’t change for a set period. On the other hand, variable rates can go up or down depending on what’s happening in the financial market.

Influence of the Economy

The state of the economy plays a big role in determining mortgage rates. If the economy is doing well, rates often go up, since more people can afford to take out loans. But if things are looking grim, rates might drop to encourage more borrowing.

Your Credit Score Matters

Lastly, your credit score has a big impact on the mortgage rate you’ll be offered. A good credit score can help you secure a lower rate, while a poor credit score might mean you’re stuck with a higher one.

Remember, understanding mortgage rates is key to getting the best deal possible. Knowledge is power, after all.

So now you know what a mortgage rate is and how it works, let’s dive into how your credit score can affect the rates you’re offered.

What Interest Rate Should You Expect on a Bad Credit Mortgage?

Having a bad credit score can be a bit of a headache, especially when you’re looking for a mortgage.

The hard truth is that having bad credit might mean you’re offered a higher interest rate. But don’t panic – it’s not always like that.

So, how do lenders figure out your interest rate when you’ve got a bad credit score?

Here are a few factors they consider:

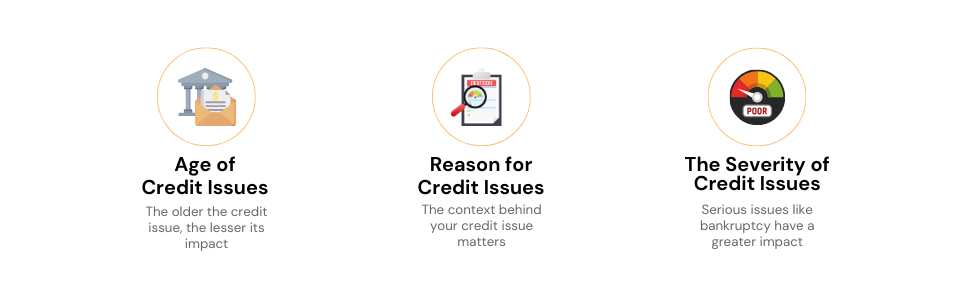

Age of Credit Issues

This is about how long ago you had credit problems. The older the issues, the less impact they might have on your mortgage rate. Lenders often view older credit issues as less of a concern – you’ve had time to sort things out, after all.

Reason for Credit Issues

The reasons behind your credit score taking a hit can also play a part. For example, if you fell into debt because of unexpected life events, like redundancy or illness, lenders might be more understanding.

The Severity of Credit Issues

More serious credit problems, like bankruptcies or repossessions, can lead to higher mortgage rates. Smaller issues like missing a single credit card payment might not impact your rate as much.

Each lender is different. They all have their ways of judging risk and setting interest rates. So getting the best rate will always depend on your circumstances.

>> More about Bad Credit Mortgages

How to Get the Best Rate on a Bad Credit Mortgage

Scoring a good mortgage rate with bad credit may seem tough. But, there are ways to up your game.

Here’s a handy list of tips to help you secure a better rate:

1. Check your credit report. Before you do anything else, have a look at your credit report. Get familiar with what’s on it and make sure everything is accurate. If you spot mistakes, get them fixed before your lender does.

2. Pay down debts. Owing less money can give your credit score a boost. So, if you can, try to reduce any outstanding debts you have.

3. Save a bigger deposit. The larger your deposit, the less risk for the lender. This could help you secure a better interest rate.

4. Speak to a broker. A broker can provide tailored advice and help find lenders who are willing to offer mortgages to those with bad credit.

Improving a credit score doesn’t happen overnight. It may take a bit of time, but every step you take towards paying off debts and staying on top of your finances can gradually improve your credit score. This, in turn, can open the door to more favourable mortgage rates.

What are the Different Types of Mortgage Rates?

Here are six main types of mortgage rates you might come across. Let’s break them down:

1. Fixed Rate

With a fixed-rate mortgage, your interest rate stays the same for a certain period. This could be two, three, five, or even ten years. This is great because you know exactly what your mortgage repayments will be during that period. No surprises.

- Pros: Makes budgeting easier as your monthly payments stay the same.

- Cons: You’re stuck with your rate even if rates drop. Some come with hefty early repayment charges.

2. Standard Variable Rate (SVR)

This is a lender’s default rate. Once your initial mortgage deal ends, you’ll likely move to this rate. The interest rate can go up or down, depending on various factors.

- Pros: Flexibility. You can overpay or leave anytime without penalty.

- Cons: Rates can rise or fall anytime. It’s usually higher than other rates after introductory deals.

3. Tracker Rate

These rates move in line with a nominated interest rate, usually the Bank of England base rate. This means your monthly repayments could rise or fall.

- Pros: When the base rate falls, your payments do too.

- Cons: If the base rate rises, your payments can increase, which can make it harder to budget.

4. Discount Rate

With this type of rate, you get a discount off the lender’s SVR for a set period. If the SVR changes, so does your rate, but the discount remains the same.

- Pros: You get a lower rate for a set period, which can make your initial repayments more affordable.

- Cons: Your rate will increase if the lender’s SVR increases, even during the discount period.

5. Capped Rate

This is a variable rate, but it won’t go above a certain limit, or ‘cap.’ This offers the flexibility of a variable rate with the security of knowing your rate won’t go beyond a certain level.

- Pros: Your rate won’t go beyond a certain level, giving you some security against large increases.

- Cons: The cap is usually set quite high. It can be more expensive than other types.

6. Offset Rate

Here, your savings account is linked to your mortgage. Instead of earning interest on your savings, you pay less interest on your mortgage. This can help you pay off your mortgage faster.

- Pros: You can save a good amount on interest and help pay off your mortgage quicker.

- Cons: You won’t earn interest on your savings. The rates can be higher than on other mortgages.

The best type for you depends on your circumstances and how much risk you’re willing to take. If you’re unsure, a chat with a mortgage broker can help clarify things for you.

Other Factors That Determine Your Mortgage Rate

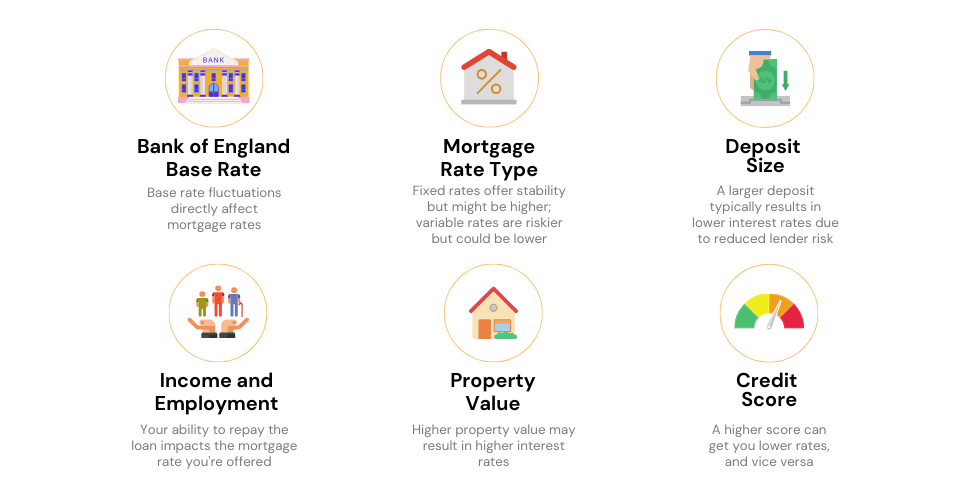

When it comes to working out your mortgage rate, credit history isn’t the only piece of the puzzle. There are other things that lenders have their eyes on:

- Bank of England base rate. The base rate set by the Bank of England impacts all mortgage rates. If the base rate rises, lenders usually increase their rates. If it falls, mortgage rates often fall too.

- Mortgage rate type. Whether you choose a fixed, variable, or other type of rate will affect the rate you get. For example, fixed rates can be higher, but give you the certainty of consistent payments.

- Deposit size. The size of your deposit can make a big difference. Bigger deposits can lead to lower interest rates because they pose less risk to the lender.

- Income and employment. Lenders want to know if you can pay back the loan. So, your income and job security can impact your mortgage rate.

- Property value. The price of the property you’re buying also matters. Higher-priced properties can sometimes attract higher interest rates.

What is the Easiest Type of Mortgage to Get If You Have Bad Credit?

If you have bad credit, you might be wondering what type of mortgage is easiest to secure. There isn’t a one-size-fits-all answer.

The best option depends on your unique situation. But, standard repayment mortgages are often a good bet.

They’re straightforward, popular, and widely available. Even with bad credit, sticking to a well-structured repayment plan can help.

But remember, you still need to play by the rules. Following advice from a mortgage broker and showing patience can pay off in the long run.

Key Takeaways

- Your credit history impacts your mortgage rate, but it’s not the sole determinant.

- Even with bad credit, you can secure a decent mortgage rate. This might mean making a larger deposit, improving your credit score, or simply biding your time.

- Mortgage types vary and your credit history plays a role in what options may be best for you.

- Standard repayment mortgages are often a straightforward choice for those with bad credit.

- Brokers can provide invaluable guidance, particularly if your credit history isn’t perfect.

The Bottom Line

As we close, it’s important to remember you’re not alone in this process. We’re here to help connect you with brokers who are experts in mortgages for those with bad credit.

They can guide you through your options and work to find the best mortgage deal for your circumstances. Don’t hesitate to reach out to us for assistance.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What interest rate should I expect with a CCJ?

A County Court Judgement (CCJ) can increase the mortgage rate you’re offered as it’s seen as a serious credit issue. However, rates can still vary widely depending on the lender and other factors. Consulting with a broker can help you find the most favourable rate for your situation.

What is the highest interest rate for bad credit?

Interest rates can vary widely, but they’re generally higher for those with bad credit. It’s important to note that it can go well above the standard variable rate (SVR), possibly double or more.

How much deposit do I need for a mortgage with bad credit?

While the amount can vary, generally, a larger deposit can help. You might need to aim for a deposit of at least 15-30% of the property’s value, depending on the severity of your credit issues.

Can I still get a good mortgage deal with bad credit?

Absolutely. Although challenging, with steps like increasing your deposit, improving your credit score, or consulting a mortgage broker, you can still secure a mortgage that suits your needs.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How To Remortgage With a Bad Credit: A Complete Guide

Thinking of renovating the kitchen, building an extension, or finally booking that dream family holiday? If bad credit’s been holding you back from remortgaging to free up cash, you’re not alone. Many people worry that their past financial mistakes might prevent them from using their home’s value. But good news: it’s possible to remortgage even […]

How To Improve Mortgage Credit Score? 10 Best Tips in 2025

When you’re applying for a mortgage, your credit score is like a summary of your financial behaviour. It shows how well you’ve managed credit in the past, and lenders use it to decide if they’ll approve your application. Your credit score doesn’t just affect approval—it also impacts the interest rate you’ll be offered. A higher […]

How To Get Subprime Mortgages in the UK: A Complete Guide

History has a funny way of shaping where we end up, and mortgages are no exception. If you remember the subprime mortgage crisis of 2007-2008, it was a huge shake-up that left lenders no choice but to tighten their rules and be far more careful. These days, things are a lot different. While borrowing money […]