- What Is a Commercial Buy-to-Let Mortgage?

- Can You Get a Buy-to-Let Mortgage on Commercial Property?

- Steps To Secure Commercial Buy-to-Let Mortgage

- What Determines Commercial Buy-to-Let Mortgage Rates?

- What Fees Do You Pay for Commercial Buy-to-Let Mortgages?

- Do You Need Commercial Leases for Buy-to-Let Properties?

- Do You Need a Solicitor for These Deals?

- What Should You Know About Mixed-Use Properties?

- The Bottom Line

How To Get Commercial Buy-to-Let Mortgages: A Guide

Fact: Many of us want to get into real estate.

The idea of extra money every month, the chance for your property to grow in value, and high demand from businesses looking to rent make it a tempting option in the UK.

Yet, getting the funds for these properties isn’t simple.

You need to do your homework and plan carefully before taking the plunge. It’s crucial to find a mortgage deal that fits you. Choosing the wrong one could mean losing thousands of pounds over time.

This guide teaches you more about commercial buy-to-let mortgages and how to secure one.

Ready?

What Is a Commercial Buy-to-Let Mortgage?

A commercial buy-to-let mortgage (also called commercial landlord mortgage, business buy-to-let mortgage, or commercial investment mortgage) is a loan for buying properties to rent to businesses.

It’s different from a regular buy-to-let mortgage, which is for renting out residential properties.

This loan can be used for offices, retail spaces, warehouses, or healthcare facilities. Lenders assess these loans more thoroughly, looking at potential rental income and your financial health.

Because these properties are for business use, the borrowing terms are usually stricter. This is due to the higher risks associated with commercial properties.

Can You Get a Buy-to-Let Mortgage on Commercial Property?

Yes, you can. It’s important to choose the correct mortgage and lender, though. If you plan to rent the property to businesses, you’ll need a commercial buy-to-let mortgage.

But, if you’re looking to rent out a house or flat, a regular buy-to-let mortgage is what you need.

For properties that have both living spaces and business areas, like a shop with a flat above, you’ll require a semi-commercial or mixed-use mortgage.

Steps To Secure Commercial Buy-to-Let Mortgage

Once you’ve decided to apply for a commercial buy-to-let mortgage, here are the steps you can take to apply:

1 – Speak with a Commercial Mortgage Broker

Talking to a commercial mortgage broker is a smart first move.

They can give you personalised and practical advice on how you can secure a buy-to-let mortgage for commercial properties.

They can:

- Guide you through the application process.

- Offer advice on which lenders are best for your situation.

- Help you understand the terms and rates available.

- Advise on the documents you need.

- Provide insight into the market and investment opportunities.

2 – Gather the Right Documentation

To smooth out the process, you need to collect the correct paperwork:

- Projected rental income

- Your financial information as an investor

- Proof of income

- Your business plans

- Details about the property you’re investing in

Before applying, also check your credit file with credit agencies. Your broker can help you ensure everything is for your application.

You should also get the details of your credit file from credit agencies before you apply to a lender. Your broker can guide you through this process to ensure you’re doing the right thing.

3 – Apply to the Right Commercial Mortgage Lender

Nobody wants to get stuck in the wrong mortgage deal.

That’s why picking the right lender is key in this process.

It’s important to find a lender comfortable with your property type and one who understands your financial situation.

Consider if the property will generate enough rent to cover the mortgage, often needing to meet or exceed 125% to 145% of your payments. Having a reliable commercial tenant can significantly boost your application.

Lenders will assess the lease if there’s already a tenant. Plus, personal checks like credit history and financial stability are standard.

Some lenders may require a surveyor’s visit to ensure the property’s suitability as security for the loan.

Whether applying as an individual or a company affects which lenders you can approach. A broker with experience in commercial buy-to-let is invaluable here.

Remember, the right lender offers terms that suit your finances. Always read the terms and conditions thoroughly.

Failing to keep up with your mortgage could mean losing your property.

What Determines Commercial Buy-to-Let Mortgage Rates?

Commercial mortgage rates are usually higher than residential ones. This is because lending for commercial properties is seen as riskier.

To guide you on what influences your rate, here are several factors lenders check to decide about your rate:

- Your deposit size

- Your credit history

- The lender’s criteria

- The business renting your property

- Your property experience

- Your income and expenses

- The type of property you’re buying.

Deposit Size

The more money you can put down, the lower your interest rates might be. This shows lenders you’re serious about your investment.

A deposit of 25-35% is common, but 40% or more could get you the best deals.

Credit History

Good credit means you’re seen as less of a risk, so you’ll likely get better rates. Bad credit can lead to higher rates, as lenders see you as more of a gamble.

Lender’s Criteria

Different lenders have different rules. They’ll look at your whole financial picture to decide on your rates. This is why choosing the right lender for your needs is important.

The Business Renting Your Property

If you have reliable businesses renting your property, lenders might offer you lower rates. This is because a steady rental income means less risk for them.

Property Experience

If you’ve successfully managed properties before, lenders might see you as a safer bet and offer better rates.

Income and Expenses

Lenders will look at your finances to make sure you can cover the mortgage payments, especially during tough times.

Having a solid income and manageable expenses is key.

Type of Property

The kind of property you’re buying affects your rates too. Riskier properties might have higher rates.

Each property, from offices to shops, has different considerations for lenders.

Remember, commercial mortgage rates are usually higher than residential ones. This is because lending for commercial properties is seen as riskier.

What Fees Do You Pay for Commercial Buy-to-Let Mortgages?

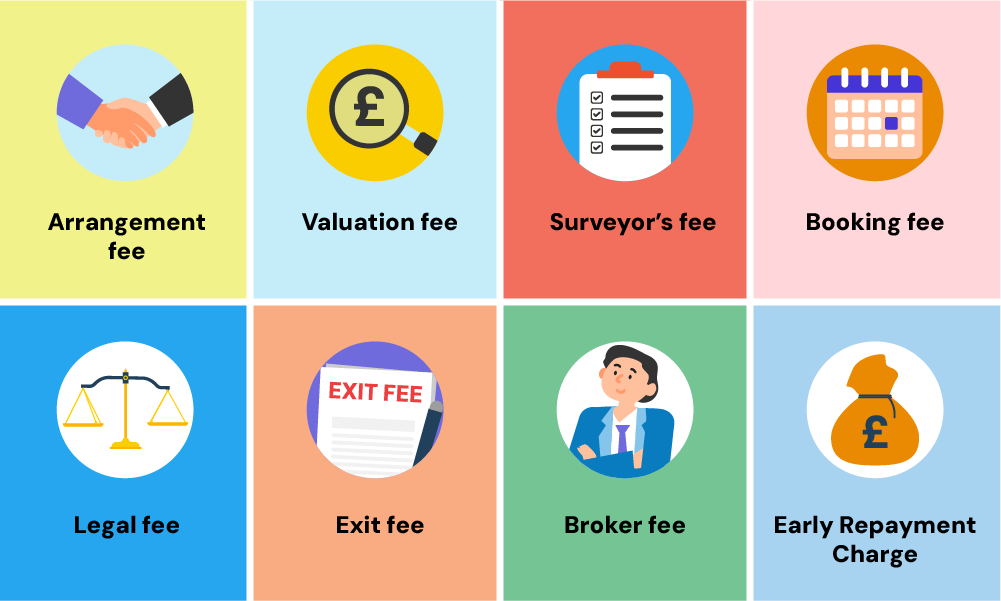

When you invest in commercial buy-to-let properties, you’ll come across several fees. Knowing these costs is key to planning your budget and getting a good mortgage deal.

- Arrangement Fees – This is what lenders charge to set up your mortgage. It usually ranges from 1% to 2% of your loan amount, but it can vary.

- Valuation Fees – Lenders need to know how much the property is worth and its rental potential before they say yes to your mortgage. The cost for this depends on how big and complex the property is.

- Legal Fees – You and the lender will need lawyers to make sure everything is above board. This includes paying for the legal work needed to transfer the property into your name.

- Surveyor Fees – Commercial properties often need a detailed check-up to find any issues. This check-up can cost more than it would for a house.

- Broker Fees – If you use a broker to help find the best mortgage, you’ll have to pay them. This could be a set fee or a percentage of your loan.

The kind of property you’re buying can also change how much these fees are. Riskier properties might need more checks and insurance, which can add to your costs.

To keep your costs down and get a better deal, try to:

- Talk to different lenders to compare deals.

- Have a solid business plan and property valuation ready to show lenders.

- Think about when you’re investing. The timing can affect your mortgage’s interest rates and fees.

Do You Need Commercial Leases for Buy-to-Let Properties?

Yes, commercial leases are crucial for buy-to-let properties. They make sure you get regular income by setting out rent, who fixes what, and how long the tenant stays.

These leases are usually for 5 to 10 years, longer than home rentals. They put more responsibility on the business renting your space to take care of it.

Having a solid lease makes lenders more likely to lend you money because it shows your income is stable.

Do You Need a Solicitor for These Deals?

Yes, a solicitor is essential when you’re dealing with commercial properties. They take care of the legal stuff, from checking the property to making the lease.

A good solicitor will draft a lease that’s in your favour. For instance, they can make sure the tenant pays for repairs and insurance. This is different from renting out homes, where you usually have to handle those costs.

They also help with the financial side, like business rates for when the place is empty. You might not have to pay these rates for some properties, but it’s best to ask your council. Without tenants, commercial properties can cost you a lot.

Solicitors also show you how the lease affects your mortgage and how to own your property in a way that saves you tax.

Their advice keeps you safe from legal troubles and makes your investment work better.

What Should You Know About Mixed-Use Properties?

Mixed-use properties blend living spaces with business areas, like a building with a shop on the ground floor and flats above.

For financing these properties, you need a unique type of mortgage. Lenders will assess the property based on its residential and commercial portions and the potential income from each.

Most often, you’ll need what’s called a semi-commercial mortgage for properties like these because they’re not purely commercial or residential.

If your mixed-use property also qualifies as an HMO (House in Multiple Occupation), you’ll require an HMO mortgage, distinct from standard commercial buy-to-let options.

This specificity ensures the mortgage aligns with the property’s dual-use nature.

When thinking about mixed-use properties, you should:

- Check how much rent you could get from the business and residential parts.

- Learn about local rules for buildings used for both living and working.

- Think about what it means to manage a building with both shops and homes. It can be more complicated than just renting out flats or offices.

The Bottom Line

In conclusion, finding the right mortgage for commercial or mixed-use properties is key to your investment success.

You’ll need to carefully pick the mortgage type, gather documents, and choose a lender that fits your needs.

Good planning, understanding the deal, and possibly consulting a solicitor will streamline the process.

Also, think about the rental income, and your legal duties, and seek expert advice to navigate the investment industry more easily.

A commercial mortgage broker could be incredibly helpful here. They know the market inside out, can advise on the latest trends, and help you find the right lender. They’re also skilled at negotiating, often getting you better terms or lower interest rates.

To find a great broker, ask for recommendations, check their credentials, and discuss their experience with similar projects.

Feeling overwhelmed by the search? Get in touch with us. We’ll connect you with your ideal commercial mortgage broker to help you find a suitable mortgage deal.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What is the difference between a mortgage and a commercial mortgage?

A mortgage is a loan you get to buy a house or flat, where you pay it back over time. A commercial mortgage is for buying properties for businesses, like shops or offices, and works a bit differently because it’s seen as riskier

Can you remortgage a commercial buy-to-let mortgage?

Yes, you can remortgage a commercial buy-to-let mortgage. It might even be easier the second time around because you’ve got experience and proof that you’re making money from your property. This could help you get a better deal.

How much can I borrow for a commercial buy-to-let mortgage?

The amount you can borrow for a commercial buy-to-let mortgage depends on several factors, including the rental income the property can generate, your financial situation, and the lender’s criteria.

Usually, lenders look at the potential rental income to decide how much they’ll lend you, aiming for the rent to cover 125% to 145% of the mortgage payments.

Your credit history and how much deposit you can put down also play a big part. For a more precise figure, it’s a good idea to use a mortgage calculator.

Related Articles

Can You Change From Commercial Mortgage To Residential?

Since 2015, it’s been easier to switch your mortgage from commercial to residential, all thanks to the UK government’s major changes to the General Permitted Development Order (GPDO). These rules have simplified changing a building’s use from commercial to residential, offering developers more opportunities to turn unique business spaces into homes. You might be considering […]

Should You Get A Semi-Commercial Mortgage? A Guide

If you want to own a building with a shop on the ground floor and flats above, you’re the perfect candidate for a semi-commercial mortgage. This option is also great for investors looking to buy such mixed-use properties and for developers aiming to create spaces that blend living and commercial areas. Curious? This article explores […]

How To Buy A Pub With Commercial Mortgages? A UK Guide

Pubs are more than just places to drink. They’re the soul of British culture – a haven where locals gather to unwind, celebrate, or simply enjoy a quiet pint after a long day. For anyone dreaming of swapping their office view for the behind-the-bar camaraderie, the idea of running a pub might sound like the […]