- What Are Commercial Mortgages?

- How Do Interest-Only Commercial Mortgages Work?

- Who Qualifies?

- Why Opt for an Interest-Only Commercial Mortgage?

- What Challenges Come with Interest-Only Commercial Mortgages?

- How Much Can You Borrow?

- How to Apply for an Interest Only Commercial Mortgage?

- Tips To Manage Your Interest-Only Commercial Mortgage

- Key Takeaways

- The Bottom Line

Interest Only Commercial Mortgages Explained

As a business owner, you definitely want to nail your mortgage repayment terms. (Of course, nobody wishes to get it wrong when it comes to mortgages.)

But how do you decide on the best repayment term for your business?

If you can afford larger monthly payments, a repayment mortgage might be the best choice. This way, you’re chipping away at both the principal and the interest every month.

On the flip side, if your cash flow is a bit tighter, an interest-only commercial mortgage might be up your alley. With this one, you’re only covering the interest each month and then you settle the full loan amount when the term ends.

Sounds cheap and simple, right?

But hold up, before you jump in, you must know the long-term impact of this mortgage type on your business.

Ready? Here’s a dive into the details:

What Are Commercial Mortgages?

A commercial mortgage is a loan specifically designed for buying commercial property, like office buildings, warehouses, or retail stores. It works just like a regular mortgage for a house but for business purposes.

There are two main ways to repay the commercial mortgage loan: interest-only and capital repayment.

How Do Interest-Only Commercial Mortgages Work?

An interest-only commercial mortgage lets you focus on growing your business in the early years.

Instead of paying down the loan amount with your monthly payments, you just pay the interest on the loan, often between 3-25 years in the UK.

This frees up cash for things like renovations or building your inventory. These mortgages are good for properties expected to increase in value or where rent covers the interest comfortably.

But remember, you’ll still owe the original loan amount later.

You’ll need a plan to repay it, either by selling the property, refinancing, or using another source of funds.

Who Qualifies?

While eligibility requirements are generally similar to capital repayment mortgages, individual lenders may have their preferences.

Here’s a breakdown of some key factors lenders typically look at:

- Deposit. Expect a minimum deposit requirement, typically between 25% and 40% of the property value. A larger deposit can lead to lower interest rates.

- Business viability (owner-occupiers). Lenders will assess your business’s financial health through plans, projections, and records. Strong profitability increases your chances of approval

- Rental income (investors). If you’re buying to rent, the amount you can borrow will depend on the rental income the property generates. This income needs to comfortably cover the interest payments.

- Exit strategy. You’ll need a clear plan (selling the property, refinancing) to repay the loan amount at the end of the interest-only term.

- Credit history. A positive credit record shows you’re a reliable borrower, increasing your approval odds for loans and credit cards.

- Property value. Lenders will verify the property’s value through an appraisal to ensure it aligns with the loan amount.

Remember, these are general guidelines.

It’s always best to consult a commercial mortgage broker who can help you understand specific lender requirements and find the best option.

Why Opt for an Interest-Only Commercial Mortgage?

Here are the benefits of choosing an interest only commercial mortgage:

- Lower monthly payments. Free up cash to invest in your business or upgrade your property.

- Maximise cash flow. Use the extra money for expansion, building inventory, or renovations.

- Improve short-term cash flow. Particularly beneficial for startups or businesses needing more breathing room in the early years.

- Potential for property appreciation. If the property value increases, you can potentially refinance with a lower principal amount later.

- Monthly income for investment properties. If you plan to rent the property, the rental income can cover the monthly interest payments, generating a steady income stream.

What Challenges Come with Interest-Only Commercial Mortgages?

Here are the downsides of choosing an interest only commercial mortgage:

- Loan repayment plan. You’ll still owe the original loan amount later. Have a solid plan to repay it (sell, refinance, etc.).

- Increased risk at maturity. If property values decline, remortgaging might be difficult.

- Interest rate fluctuations. Rising interest rates can significantly increase your monthly payments when you transition to principal repayment.

- Pressure to maintain high occupancy. Vacancies can make it harder to cover interest payments.

- Risk of repossession. If you can’t keep up with payments, the lender could repossess the property and sell it to recover the debt. This could disrupt your business or force tenants to relocate.

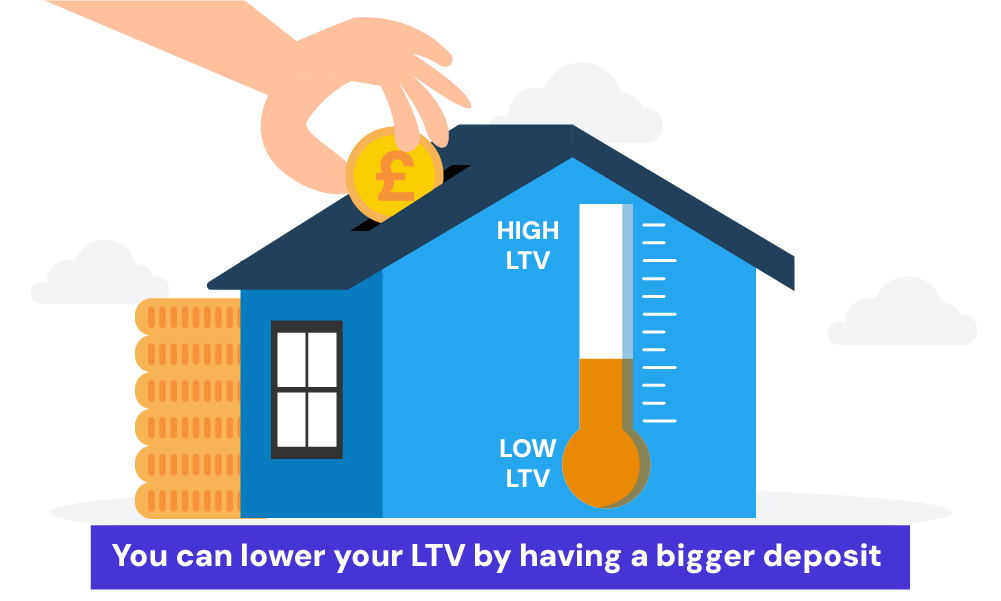

How Much Can You Borrow?

The amount you can borrow isn’t just a random figure. Lenders look at a few important things to decide.

One major factor is the Loan-to-Value Ratio (LTV). This is all about comparing the loan you want with the value of the property.

Generally, you might get up to 75% of the property’s value as a loan if you have a good credit history and your property is worth a lot.

Also, if you can make a big down payment, it reduces the risk for the lender and could mean you can borrow more.

For those planning to rent out the property, the expected rental income is key.

Lenders will check if this income will cover the interest payments well enough. This ensures you can handle the loan without stress.

If you’re getting the property for your own business, how well your business is doing matters too.

Lenders will want to see your business plans, financial statements, and how profitable you are. If your business looks financially healthy, you might get a higher loan amount.

Want a quick idea of how much you might be able to borrow? Try our commercial mortgage calculator!

It provides an initial estimate based on factors like property value, interest rate, and loan term.

Remember, this is just an estimate, and the actual amount you can borrow will depend on your specific circumstances.

[Embedded commercial mortgage calculator]

How to Apply for an Interest Only Commercial Mortgage?

Applying for an interest-only commercial mortgage requires careful planning. Here’s a breakdown of the process:

1. Gather Documentation

The documents you’ll need depend on whether you’re an owner-occupier or an investor.

- For Owner-occupiers:

- Past 2 years business accounts (profit and loss statements, balance sheets)

- Cash flow forecasts for the next few years

- Business plan outlining your strategy and future profitability

- For Investors:

- Past 2 years’ personal tax returns

- Property details including address, legal description, and square footage

- Rental income projections demonstrating your ability to cover the interest payments

- Standard documents across both categories include:

- 3 months bank statements

- Statement of assets and liabilities

- Details of any properties you own (your home, and any other residential and commercial property)

- Proof of deposit (purchase only)

2. Choose the Right Lender with a Broker’s Help.

Research and compare lenders with a commercial mortgage broker to find the best deal for your situation.

Brokers have access to a wider range of lenders and can help you consider factors like interest rates, loan terms, lender reputation, and customer service.

Additionally, some lenders might only work with applicants who go through brokers, potentially limiting your options if you go it alone.

The lender will arrange for a valuation to confirm the property’s value aligns with the loan amount.

A lower valuation might result in a reduced loan offer or even a loan rejection. A broker can help navigate this situation by finding alternative lenders.

4. Formal Offer and Legal Work

If your application is approved, you’ll receive a formal offer letter outlining the loan details (amount, interest rate, term, fees).

A conveyancing solicitor will then handle the legal aspects of transferring the property to your name.

Once everything is finalised, the mortgage funds will be disbursed.

Tips To Manage Your Interest-Only Commercial Mortgage

Here are some ways to keep your interest-only commercial mortgage on track:

- Make timely payments. Paying your monthly interest on time is crucial to avoid penalties and damage to your credit score. Late payments can snowball, adding interest and extending the loan term, ultimately costing you more.

- Track market trends. Stay informed about property values and interest rates. This allows you to identify potential refinancing opportunities to lock in a lower rate when transitioning to principal repayment. Ideally, remortgage before the end of the interest-only period to secure a better deal.

- Plan for an exit strategy. Don’t wait until the later stages. Develop a solid strategy now (selling, refinancing, etc.) to ensure you have the funds to repay the principal loan amount at the end of the interest-only term.

- Review your mortgage at renewal. As you approach the end of your initial interest-only period, explore refinancing options. Remortgaging can potentially save you money on interest or even release equity from the property for other investments.

Key Takeaways

- A commercial mortgage is a loan to buy business properties like shops or offices, with repayment options such as interest-only or capital repayment mortgages.

- Interest-only mortgages let you pay just the interest for a set period, freeing up cash for your business, but you’ll still need a plan to repay the full loan later.

- To qualify, lenders look at factors like your deposit (usually 25–40%), business finances, rental income (if renting out the property), and credit history.

The Bottom Line

Interest-only commercial mortgages offer lower monthly payments, freeing up cash flow for business needs.

They can be ideal for investment properties or businesses in the early stages. However, remember you’ll still owe the original loan amount later. Careful planning and a strong repayment strategy are important.

Not sure if an interest-only mortgage is right for you?

Talking to a professional can help you make an informed decision. We can connect you with a commercial mortgage broker who understands your goals and can guide you through the process.

Simply, fill out this form and we’ll set up a free, no-obligation consultation with a good broker to help you get started with your business.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I secure an interest-only commercial mortgage in the UK?

Yes, interest-only commercial mortgages are available in the UK. However, they are less common than traditional capital repayment mortgages.

Is it possible to get a mortgage with a lower or no deposit?

While possible, it’s less common. Lenders are more cautious with lower down payments, so expect stricter eligibility requirements and potentially higher interest rates.

To get a 100% commercial mortgage, you can use equity from another property you own (like your home) to help secure the loan. But remember, that property is also at risk if you can’t repay the mortgage.

Related Articles

Can You Change From Commercial Mortgage To Residential?

Since 2015, it’s been easier to switch your mortgage from commercial to residential, all thanks to the UK government’s major changes to the General Permitted Development Order (GPDO). These rules have simplified changing a building’s use from commercial to residential, offering developers more opportunities to turn unique business spaces into homes. You might be considering […]

Should You Get A Semi-Commercial Mortgage? A Guide

If you want to own a building with a shop on the ground floor and flats above, you’re the perfect candidate for a semi-commercial mortgage. This option is also great for investors looking to buy such mixed-use properties and for developers aiming to create spaces that blend living and commercial areas. Curious? This article explores […]

How To Buy A Pub With Commercial Mortgages? A UK Guide

Pubs are more than just places to drink. They’re the soul of British culture – a haven where locals gather to unwind, celebrate, or simply enjoy a quiet pint after a long day. For anyone dreaming of swapping their office view for the behind-the-bar camaraderie, the idea of running a pub might sound like the […]