- What is Development Finance?

- How Development Finance Can Work for You

- What are the Different Types of Development Finance?

- How Do You Qualify?

- What You’ll Need for a Smooth Application

- How Much Money Can You Borrow?

- What are the Interest and Fees?

- Full Financing for Your Project

- Understanding Commercial and Residential Development Finance

- What is Development Exit Finance?

- How Do You Repay a Development Loan?

- Key Tips Before You Get Started

- Key Takeaways

- The Bottom Line

Development Finance: What It Is and How to Get It

Building a new house or making home improvements can be pretty expensive. A standard mortgage might not be enough to cover everything you need.

So, how can you pay for your project without running out of money?

That’s where development finance comes in. It’s a special type of loan that helps you pay for things like buying land or starting construction.

This loan lets you take on bigger projects, and if you play your cards right, you could make more money later by selling or renting out the property.

In this guide, we’ll explain what development finance is, how it works, and how you can get it.

What is Development Finance?

Development finance is a special type of loan made for building projects.

It’s different from regular loans you’d use to buy a house because it’s designed for creating or transforming properties, like building something new or fixing up an old place.

Unlike standard mortgages, these loans are short-term and usually last between 6 to 24 months.

They’re perfect if you’re starting a big project, like building from scratch, converting a building into something new, or doing major renovations.

How Development Finance Can Work for You

Development finance is made to support every step of your building project, whether it’s for a house or a business property.

It’s flexible enough to work for different plans, like starting from scratch or making big changes to an existing property.

What makes development finance different from regular mortgages? Instead of focusing on the property’s current value, it looks ahead to what it could be worth once your project is finished.

When lenders review your loan application, they check two key things:

- Loan-to-Cost (LTC): How much of your project’s total cost the loan will cover.

- Loan-to-Gross Development Value (LTGDV): How the loan compares to your property’s estimated value after it’s completed.

They’ll also consider your past success and whether you’ll be able to repay the loan.

A big perk of development finance is how it handles interest. You don’t have to make monthly payments while building.

Instead, the interest is added to the total loan amount and paid off later—either when you sell the property or refinance it.

This gives you breathing room to focus on getting the project done without worrying about extra costs during construction.

Development Finance: A Practical Example

Suppose you’ve located a plot of land with a price tag of £550,000. You plan to build eight four-bedroom houses. The projected construction cost for all eight houses is £1,800,000.

The estimated Gross Development Value (GDV) after completing the construction can be calculated as:

- GDV= Price per house × Number of houses = £400,000 per house ×8=£3,200,000

Key Figures

- Land cost: £550,000

- Build cost: £1,800,000

- Total deal cost: £2,350,000

- GDV: £3,200,000

| Description | Percentage | Calculation | Loan Amount |

|---|---|---|---|

| Land Cost Loan | 65% | 65% of £550,000 | £357,500 |

| Build Cost Loan | 85% | 85% of £1,800,000 | £1,530,000 |

| Total Loan Facility (The Pool) | – | £357,500 + £1,530,000 | £1,887,500 |

How the Loan Works

- Initial Land Purchase. The lender will provide £357,500 (65% of the land cost), and you’ll need to contribute £192,500 from your own funds to complete the land purchase.

- Construction Phase. The remaining £1,530,000 (85% of the build cost) will be released in phases as construction moves forward. You’ll use your funds first, and then the lender follows with further drawdowns as needed.

- Loan Repayment. Upon selling the houses, you’ll repay the borrowed amount of £1,887,500 plus any accrued interest. Since this isn’t a joint venture, you’ll retain all the profits.

- Interest. Interest is typically only charged on the funds that have been drawn from the loan pool. This way, you’re not paying interest on the full £1,887,500 from the get-go, but only on the funds you’ve used.

What are the Different Types of Development Finance?

There’s no universal financial solution for every development project, as each has its unique requirements. Various types of development finance are available to cater to these different needs.

Here’s a guide to help you understand your choices:

- Residential Development Finance – Ideal for projects ranging from a single home to larger residential schemes. This type of finance generally covers everything from land acquisition to construction costs.

- Commercial and Semi-Commercial Development Finance – Suited for projects that involve business premises or mixed-use buildings. This option usually accommodates more complex valuation criteria.

- Land Development Finance – Used for purchasing undeveloped land and preparing it for construction, including obtaining the necessary permits and conducting site improvements.

- Renovation and Refurbishment Finance – Geared toward the enhancement of existing properties, whether it’s a straightforward refurbishment or a more complex conversion.

- New Construction Finance – Ideal for large-scale, ground-up construction projects, covering both material and labour costs.

- Exit Financing – Provides a short-term financial cushion after the completion of your project, giving you time to sell the property or secure refinancing.

- Regulated Development Loans – Required when more than 40% of the development will be a residential space occupied by the borrower. These loans are regulated by the Financial Conduct Authority (FCA).

- Mezzanine Finance – Bridges the gap between the primary loan and the total project cost, offering additional funds to ensure the project’s completion.

- Development Bridging Finance – Useful for quick property acquisitions or auction purchases, acting as a temporary measure before more long-term financing is secured.

Some projects may demand a mix of these finance types. If you’re still uncertain about which financing route to go down, consult a professional. They can guide you through the process, ensuring you choose the best option for your project.

How Do You Qualify?

To qualify for development finance, you’ll need to meet an array of criteria.

Generally, lenders seek applicants with a proven track record in property development. For those new to the field, a robust team or experienced partners can significantly improve your application’s credibility.

Your expertise and the presence of certified professionals in your team might also factor into the lender’s decision.

Credit history is another crucial aspect. A clean financial record, devoid of bankruptcies or defaults, enhances your appeal to lenders.

In addition to a clean credit record, lenders may also look at your existing cash reserves or accessible lines of credit as assurance against unforeseen expenses.

Financial documentation is non-negotiable. Expect to provide an extensive range of details including project plans, cost estimates, projected profits, and timelines.

You may also be required to submit a comprehensive business plan, market research, and proof of legal compliance. Lenders often request a professional valuation of the property or land you aim to develop.

Many lenders also require some form of security, usually the property you’re developing, another asset, or even corporate or personal guarantees.

A deposit will also be needed; the amount generally falls between 20% to 40% of the total project cost but could vary depending on additional factors like the project’s location and the level of risk assessed by the lender.

Given that each lender has unique requirements, it’s advisable to consult a mortgage broker specialising in development finance.

This ensures that you are not only meeting the baseline criteria but are also aligning your application with the most suitable lender for your project’s specific needs.

What You’ll Need for a Smooth Application

Beyond the criteria for qualification, the application process itself involves several steps, all requiring their own set of documents. Here’s what you should have at hand:

- Planning permission and architectural drawings.

- Any planning restrictions that could affect profitability.

- A complete cost breakdown of the project.

- Examples of your past developments, if any.

- A detailed operational calendar.

- Contacts for your architects and contractors.

- A list of your current assets and liabilities.

- Your exit strategy.

- The project’s projected final value.

Even if you’re a first-time developer, don’t worry. There are lending options suited for you as well.

How Much Money Can You Borrow?

In development finance, you have the option to borrow from £200,000 up to £50 million. The ceiling amount will depend on the lender you pick.

So, whether you’re a small developer planning a quick fix-up or a larger outfit with ambitious plans, there’s probably a loan that fits your financial scope.

To get a handle on what your repayments might look like, give our calculator below a go. You can adjust factors like the Loan-to-Value (LTV) and loan term to see how they change your repayment amounts.

[Embedded Development Finance Calculator]

While the calculator is a good place to start, it shouldn’t be your only reference. It’s wise to talk to a specialist broker who can double-check your numbers and steer you towards the best loan for your needs.

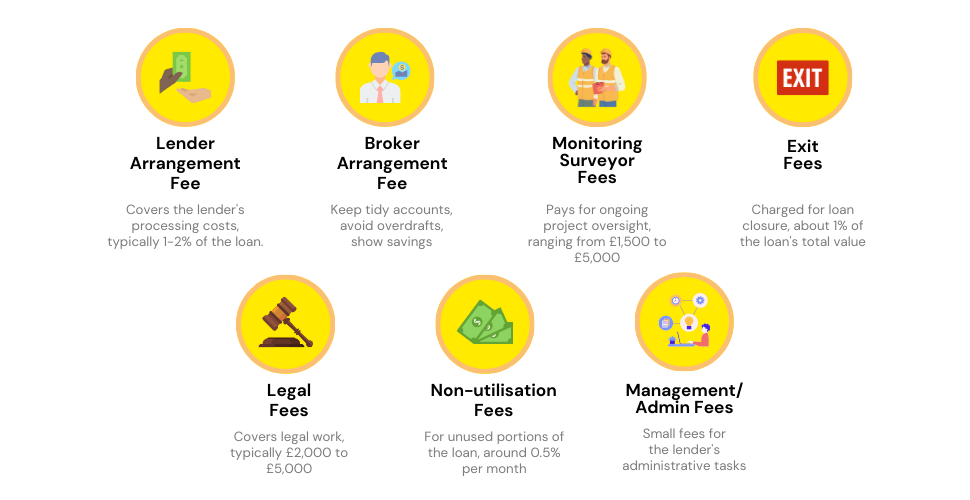

What are the Interest and Fees?

Interest rates for development finance can range from 7% to 16% APR. While you might find these rates significant, keep in mind that these loans are generally short-term.

That makes the interest rate often less crucial compared to the total cost of the loan, including various fees and terms set by the lender. In short, the cheapest rate doesn’t always mean it’s the best deal for you.

Beyond the principal and interest, there are additional costs you should be aware of, and these can vary depending on your project and loan details. Here’s what to expect:

- Lender Arrangement Fee. This fee is often 1-2% of the loan amount. So, for a £1 million loan, you could be looking at £10,000 to £20,000.

- Broker Arrangement Fee. If you use a broker, they might charge a similar fee of around 1% of the loan amount.

- Monitoring Surveyor Fees. Also known as Quantity Surveyor Fees, these could range from £1,500 to £5,000 depending on the project’s complexity.

- Exit Fees. These vary widely but could be around 1% of the loan’s total value or the gross development value.

- Legal Fees. Expect to pay around £2,000 to £5,000 for legal costs, including solicitor fees.

- Non-utilisation Fees. These are less common but can be about 0.5% of the undrawn loan amount per month.

- Management/Admin Fees. These are usually nominal, perhaps a few hundred pounds, covering the lender’s administrative costs.

It’s crucial to look at the full picture when evaluating loan options, considering both the interest rate and any additional fees. Consulting a mortgage broker specialising in development finance can offer further insights tailored to your situation.

Full Financing for Your Project

In the UK, most development loans typically cover between 60% and 80% of your total project cost. However, if you’re looking to cover all your project expenses, there are ways to achieve 100% financing. Here’s how:

- Joint Ventures: Pairing up with a financier could enable you to cover the full project cost. In this setup, the financier would provide the funding in exchange for interest payments and a portion of the project’s profits.

- Extra Collateral: If you’ve got additional assets, like more property or even valuable equipment, you can offer these as extra security to get a loan that covers 100% of your project costs.

Important Note: Both options come with their own set of terms and conditions. It’s crucial to weigh these against your project needs to see which route is more advantageous for you.

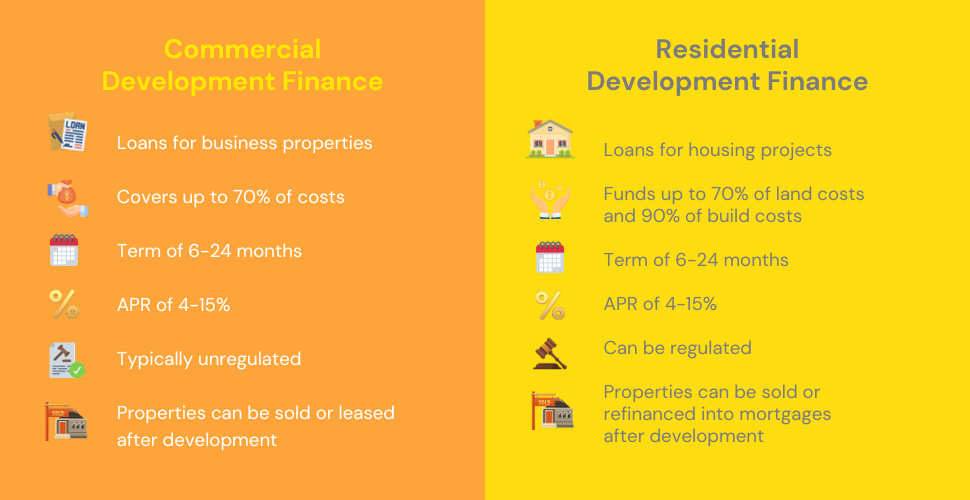

Understanding Commercial and Residential Development Finance

When you’re diving into a property development project, you’ve got two main types of development loans to consider: commercial and residential.

But what sets them apart? Here’s a breakdown:

Commercial Loans

- Purpose: These loans are aimed at developing properties for business use or mixed-use, combining business units with residential spaces.

- Maximum Loan Value: You can usually borrow up to 70% of both land and build costs.

- Loan Term: These are short-term loans, lasting from 6 to 24 months typically.

- Interest Rate: Expect rates to fall between 4% and 15% APR.

- Regulation: Generally unregulated.

- Exit Strategy: Once your development is complete, you can either sell the property to repay the loan or retain and lease it out, transitioning into a long-term mortgage.

Residential Loans

- Purpose: Perfect for developing properties primarily for residential use, like single homes or a handful of units.

- Maximum Loan Value: You can often secure up to 70% for land and 90% for build costs.

- Loan Term: Like commercial loans, these are usually short-term, ranging from 6 to 24 months.

- Interest Rate: Rates typically range from 4% to 15% APR.

- Regulation: May be regulated if more than 40% of the completed project is for personal residential use.

- Exit Strategy: Similar to commercial loans, you can sell the property to repay the loan or keep it and lease it out, eventually shifting to a long-term mortgage.

To further differentiate the two, commercial developments typically necessitate a comprehensive sales and marketing strategy. This is because the end goal for most commercial developers is to sell the completed property.

On the other hand, residential developments generally require less aggressive marketing, which often makes securing a loan for such projects more straightforward.

What is Development Exit Finance?

Development exit finance serves as a bridging loan that you can take out after your project is complete but before it’s sold or refinanced with a long-term mortgage.

This loan is designed to pay off your initial, costlier development loan, providing a financial cushion until you can sell the property or switch to a more permanent mortgage solution.

One of the benefits is that the interest rates for development exit finance are often lower than those of standard development loans. It’s a practical way to bridge the financial gap between project completion and your next steps.

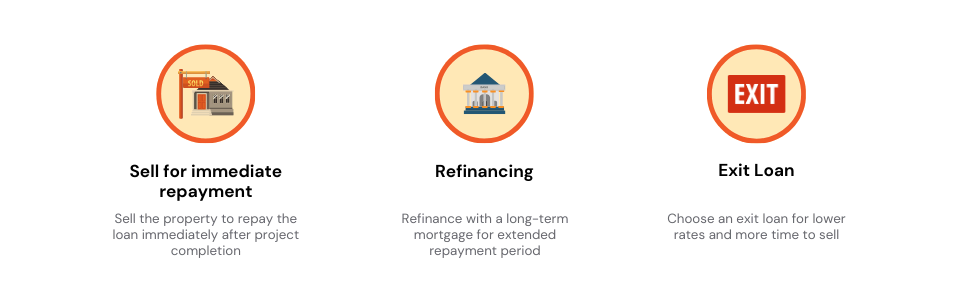

How Do You Repay a Development Loan?

You have several straightforward options when it’s time to square up your development loan:

- Sell and Settle. You can repay your loan in full with the money you make from selling your completed property.

- Switch Gears with Refinancing. If you’re not in a hurry to sell and want to keep the property for yourself or rent out, consider refinancing with a long-term mortgage. This changes your short-term obligation to a more manageable, longer-term one.

- Exit with an Exit Loan. Opting for a development exit bridging loan is another savvy move. Not only does it usually come with a lower interest rate, but it also allows you to retain more of your profits as you wait for your property to sell.

Key Tips Before You Get Started

Before you apply for a development finance loan, take a moment to ask yourself some important questions. These will help you figure out if you’re ready to take on the project:

- Why hasn’t this property been sold yet?

- Can I afford the property and the building costs?

- Are there any surprise expenses that could pop up?

- Are my architects and contractors reliable?

- Do I have a backup plan if things go wrong?

- How does this property’s value compare to others like it?

- Will people want this property when it’s done?

- Who am I trying to sell to or rent to?

- Is there a lot of competition in the market?

- How much profit will I make, and when will the project be finished?

- Is my credit score good enough for a loan?

- Do I have all the documents I need?

- Can I afford the deposit, or do I have something to use as collateral?

If you can confidently answer these questions, then you’re well-prepared for the next steps.

Key Takeaways

- Development finance is a short-term loan made for building or fixing properties, focusing on what they’ll be worth when finished, not their current value.

- These loans can cover land purchases, construction, or big renovations, and you won’t need to make monthly payments during the project—interest is added to the loan and paid off later.

- Lenders look at how much your project will cost and its future value, as well as your credit, team, and detailed plans like budgets and timelines.

- There are different types of development loans, so it’s worth getting help from a specialist broker—they can save you time, find the best lender, and maybe even score you a better deal.

- You can repay the loan by selling the property, refinancing to a long-term mortgage, or using a bridging loan to cover the gap while you wait to sell.

The Bottom Line

Choosing the right loan is just as important as picking the right team for your building project. You’ve got lots of options—banks, investment companies, and property lenders—each with its own rules.

Some lenders might ask for loads of paperwork and detailed plans, while others care more about your credit score or how much the property will be worth.

A development finance broker can make things a lot easier. They’ll help you find the best lender for your project, negotiate better deals, and handle all the boring stuff like gathering documents.

If you’re ready to make a smart choice, get in touch with us. We’ll connect you with a development finance expert who can guide you every step of the way.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Do I need planning permission before getting a loan?

Yes, lenders usually require full planning permission before approving a loan. However, some lenders may be willing to move things forward if you have at least outline planning permission. Keep in mind that they will not release the funds until you have full approval.

Can a newbie like me get funding?

Yes, you can. It’s trickier if you’ve never done this before, but it’s not impossible. You’ve got two options: either find a niche lender who’s willing to take a chance on you, or team up with a pro who knows the ropes. With their experience on your side, regular lenders might be more willing to back you up.

What if my credit is a bit dodgy?

Don’t sweat it. Some lenders specialise in cases like yours, where the credit isn’t exactly spotless. So even if you’ve been knocked back before, we might still be able to get you that loan. Give us a ring, and let’s chat about how we can make your project happen.

What is joint venture property development finance and how does it work?

Joint Venture (JV) property development finance is a partnership where you team up with a financier who can cover your entire project cost. You’ll both establish a temporary company, known as a Special Purpose Vehicle (SPV), to manage funds and legalities. When the property sells, you repay the loan and share the profits, often in a 60-40 split.

What are the alternatives to development finance in the UK to fund my project?

In the UK, besides development finance, there are various other ways to fund your property development project. You could consider:

- Bridging Loans – These are short-term financing options designed to bridge a gap in your financing, usually for quick projects or buying at auctions.

- Private Investors or Angel Investors – Some individuals are willing to invest in property projects in exchange for equity or a share of the profits.

- Mezzanine Financing – This is a hybrid of debt and equity financing that gives the lender the right to convert to an equity interest in case of default, generally, after venture capital companies and other senior lenders are paid.

- Crowdfunding – Online platforms allow you to raise small amounts from a large number of people, although this might come with its own set of challenges, such as management complexity.

Each of these options comes with its own benefits and drawbacks, so it’s essential to consult with financial advisors or mortgage brokers specialising in development finance to find the best solution for your project.

Related Articles

Residential Development Finance: A Complete Guide

If you’re eyeing a property development opportunity, chances are you’re also wondering how to finance it. It’s rare for anyone to have enough upfront cash to cover all the costs, and that’s precisely why residential development finance is invaluable. This specialised loan could be the linchpin that holds your project together, setting the scope and […]

How To Get Better Development Finance Rates In The UK?

Did you know that even a small change in interest rates can cost you a lot of money? For example, if you borrow £1 million for a property project and the interest rate goes up by just 1%, you’ll pay an extra £10,000 each year. Over a three-year project, that adds up to £30,000 more! […]

Development Finance Calculator: Get A Quick Quote

In development finance, the borrowing range is expansive, stretching from £200,000 to as much as £50 million, depending on your chosen lender. However, unlike more straightforward loan types, what you can borrow is influenced by unique factors such as the projected profitability of your development, the loan-to-cost (LTC) ratio, and even planning permissions. That’s where […]