- What is Equity Release?

- How Equity Release Works: An Example

- Pros and Cons of Equity Release

- Equity Release Eligibility Criteria

- How To Get an Equity Release?

- How Much Does Equity Release Cost?

- Is Equity Release Safe?

- Lenders Offering Equity Release

- What if I have Multiple Properties?

- What are the Tax Implications of Equity Release?

- Is Short-Term Equity Release Possible?

- How to Choose the Right Equity Release Product?

- Key Takeaways

- The Bottom Line

Equity Release Explained: A Complete Guide in 2025

Equity Release Mortgages are an enticing choice, especially if you’re a homeowner who wants to free up some cash.

Imagine this – getting a financial boost without the need to leave your home. This method is transforming how people handle their financial planning, especially later in life.

Here’s what it does. By releasing equity from your home, you can get a lump sum, a regular income, or even both. It’s customised to what you need and want.

Interestingly, over 93,421 UK homeowners decided to release equity from their homes this year alone. This statistic highlights how much traction this option is gaining.

But, let’s be clear. This is no small financial decision. You need to understand how it works, the implications, and even the alternatives.

That’s where this article comes in. We’ve crafted a comprehensive guide on equity-release mortgages.

By the time you finish reading, you’ll have a better understanding of the ins and outs of equity release.

What is Equity Release?

Equity release is a financial solution that allows homeowners, usually over the age of 55, to access the wealth (or ‘equity’) tied up in their property.

This allows you to keep your home and get a lump sum, regular payments, or both, based on the value of your property.

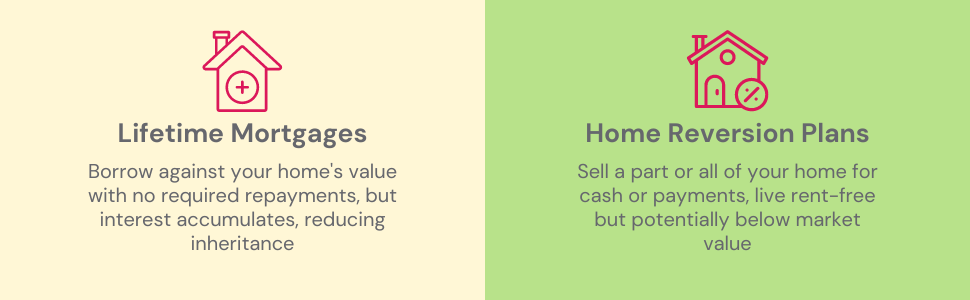

There are two main types of equity release: Lifetime Mortgages and Home Reversion plans.

Lifetime Mortgages

A Lifetime Mortgage is the most popular form of equity release. With this, you get a mortgage on your property while retaining complete ownership of your home. The loan, alongside any accumulated interest, is paid back once you pass away or move into long-term care.

Things to consider for Lifetime Mortgages:

- Interest can compound over time, increasing the total amount to repay.

- You keep full ownership, so you can benefit if property prices rise.

- Early repayment may incur charges.

- The amount you owe will reduce the value of your inheritance.

Home Reversion Plans

Home Reversion Plans are less frequently chosen, but they might be suitable in certain circumstances. Here, you sell a part or all of your home to a home reversion provider.

In return, you receive a lump sum or regular payments. You can still live in the property rent-free until your death, but it’s your responsibility to maintain the house.

Things to Consider for Home Reversion Plans:

- You no longer own all your homes and can’t benefit fully from price increases.

- You can continue to live in your home rent-free.

- Once agreed, the plan can’t be reversed as you have sold part of your home.

How Equity Release Works: An Example

Let’s say you’re a 70-year-old homeowner with a property valued at £400,000. You opt for a lifetime mortgage equity release scheme.

The provider might allow you to access up to 40% of your property’s value. That’s a tax-free lump sum of £160,000 that you can use however you like – supplementing your pension, making home improvements, or supporting your family.

Plus, you can live in your home for the rest of your life, or until you move into long-term care.

It’s important to note that equity release isn’t a one-size-fits-all solution and should be considered carefully. You should always seek financial advice before deciding which plan suits you best.

Pros and Cons of Equity Release

Like any financial decision, equity release comes with its share of benefits and drawbacks. Here are a few key points to consider:

Pros

- You can get a tax-free lump sum or a regular income without having to move out of your home.

- You don’t have to make monthly repayments. The loan and accrued interest are repaid when the property is sold.

- You will never owe more than your home’s value, even if property prices fall.

- You can use the released equity for various purposes, such as supplementing retirement income, home improvements, or helping family members financially.

Cons

- Interest can accumulate quickly, so the amount you owe can increase rapidly over time.

- Releasing equity can impact your entitlement to means-tested benefits.

- The equity in your home is reduced, which can leave less for your beneficiaries when you pass away.

- Equity release schemes can come with high upfront costs, such as application, legal, and valuation fees.

One big concern among homeowners is the reduction in the amount they can leave as an inheritance.

This can cause anxiety, especially for those hoping to leave a substantial legacy for their loved ones.

Equity release can be an effective solution for homeowners who have significant equity in their homes but are cash-poor.

It’s particularly attractive for older individuals who want to supplement their pensions or fund their lifestyle in retirement without having to move or downsize.

But, it’s important to carefully consider all the implications.

Equity Release Eligibility Criteria

To be eligible for an equity release scheme, you’ll need to meet a few key conditions:

- Age – The youngest homeowner should be at least 55, though some plans might stipulate an older age.

- Home Value – Your property should be worth a minimum of £70,000. The greater its value, the more equity you can potentially release.

- Residency & Condition – The property, located in the UK, should be your principal residence and well-maintained. A neglected home could reduce the amount of equity you’re able to access.

By satisfying these conditions, you’re likely to be eligible for an equity release scheme. But, remember that the exact terms may vary depending on the equity release provider.

As for the minimum equity release amount, this also varies between providers, but it’s often around £10,000.

It’s worth noting that the equity you can release also depends on other factors, including your health condition.

How To Get an Equity Release?

Securing an equity release is a straightforward process that involves a few key steps. Here are the common steps to get an Equity Release:

- Research – Start by learning about different types of equity release plans and familiarising yourself with their benefits and potential drawbacks.

- Consultation – Next, seek advice from an independent financial advisor who specialises in equity release. They can help you understand whether this option is right for you, and if so, which type of plan best suits your needs.

- Valuation – The equity release provider will arrange a property valuation to determine how much money you could potentially release.

- Application – If you decide to proceed, you’ll complete an application with the equity release provider. They’ll review your details, and if everything is in order, they’ll give you an offer.

- Legal process – You’ll need a solicitor to handle the legal aspect. They’ll ensure you understand the terms and conditions before you proceed.

- Completion – Once all the legal work is done, the money is released to you, either as a lump sum or regular payments, depending on the agreement.

Consulting with an experienced mortgage advisor is a critical step in this process. They can provide valuable insights and guide you through the process, ensuring that you make informed decisions.

To get started, you can drop us a line. And we’ll match you with a skilled mortgage broker in the field of equity release.

How Much Does Equity Release Cost?

Interest rates for lifetime mortgages currently begin at approximately 5%, with higher-end deals closer to 8.5 % MER.

This is considerably high compared to top rates on standard residential mortgages. But a lower interest rate doesn’t automatically mean it’s the best deal.

In considering which equity release product is most suitable, it’s important to realise that the substantial repayment amount comes into play if you’ve opted not to make monthly repayments.

In such cases, the interest compounds over time.

Here’s an example: Say you’re 65 and you decide to borrow £40,000 at a 5% interest rate on your £200,000 home.

Your debt will approximately double every 14 years. So, by the time you’re 79, you could owe around £80,000. If you reach 93, you might owe £160,000.

In addition, you’ll need to cover a few fees. These usually range from £1,500 to £3,000 and include costs like arrangement fees, property valuation, and legal and surveyor charges.

Keep in mind, these figures are rough estimates. The actual costs can change depending on your situation and the equity release provider you go with.

Is Equity Release Safe?

Equity release schemes in the UK are regulated by the Financial Conduct Authority (FCA). This ensures that providers adhere to strict standards designed to protect consumers.

Many equity release providers are also members of the Equity Release Council, a trade body that sets high standards for its members above and beyond regulatory requirements.

This includes a guarantee that you will never owe more than the value of your home, providing added peace of mind.

But, while there are protections in place, equity release is a significant financial decision. It’s essential to seek advice from a good mortgage advisor before proceeding.

Lenders Offering Equity Release

There are numerous UK-based lenders, each regulated by the Equity Release Council (ERC), offering unique equity release products. Some notable ones include:

- Aviva

- Legal & General

- More2Life

- Canada Life

- Pure Retirement

- Livemore Mortgages

- Standard Life Home Finance

- Scottish Widows

Remember, each lender has its unique offerings, so it’s crucial to find the one that fits your requirements and personal circumstances the best.

What if I have Multiple Properties?

If you’re lucky enough to own more than one property, you might wonder if you can take out equity release on all of them. The straightforward answer is yes, it’s possible.

Many lenders are willing to offer equity release on a second property or even a holiday home.

Keep in mind that each property will be assessed separately, and there will be separate plans for each. This means each property will have its own set of terms and conditions, interest rates, and fees.

But, unlocking equity from multiple properties isn’t a decision to be taken lightly.

It’s important to weigh up the pros and cons, consider how it might affect your tax position or benefit entitlements, and take into account any plans you might have for these properties.

What are the Tax Implications of Equity Release?

While the funds you gain from equity release are tax-free (HM Revenue & Customs doesn’t classify it as income), other tax implications can arise:

- If you invest your equity release funds and earn interest or dividends, you’ll need to pay income tax on those earnings.

- Using equity release can affect your entitlement to means-tested benefits.

- On the inheritance side, taking out equity release can reduce the inheritance tax bill. That’s because the value of your estate decreases by the amount borrowed. So, when it’s time for inheritance tax assessment, there’s a smaller estate value to tax.

Remember, though this might lead to a lower inheritance tax bill, your heirs will inherit less as the equity release needs repaying.

Always consult a financial adviser or tax specialist before making decisions related to equity release.

Is Short-Term Equity Release Possible?

Short-term equity release isn’t typically feasible as repayment is generally upon death or long-term care. But, those with a terminal illness could potentially see it as a short-term measure through an enhanced lifetime mortgage.

Other methods like remortgaging for equity release might seem more short-term but are not equivalent to equity release plans and aren’t usually considered short-term borrowing.

How to Choose the Right Equity Release Product?

Choosing the right equity release product is crucial. Here are a few tips:

- Understand Your Needs – Do you need a lump sum, regular income, or perhaps both? Your needs will dictate the best type of equity release for you.

- Compare Interest Rates – Different providers offer different interest rates. Make sure to compare these and understand how they’ll affect your loan over time.

- Consider the Flexibility – Some products offer more flexibility than others, like the option to make repayments or the ability to draw down money over time.

- Look at the Features – Some equity release plans come with useful features, such as the ability to protect a percentage of your property’s value for inheritance.

- Check for Early Repayment Charges – If there’s a chance you might want to repay the equity release plan early, look for a product with low or no early repayment charges.

- Take Advice – As mentioned earlier, an experienced equity release advisor can help you sift through the options and find a product that suits your circumstances.

Remember, what works best for one person may not be the best for another. So consider your situation and goals when choosing an equity release product.

Key Takeaways

- Equity release lets you take money from your home without selling it. You can get it as a lump sum, regular payments, or both.

- There are two main types: Lifetime Mortgages let you keep your home, while Home Reversion Plans involve selling part or all of it for cash.

- With a Lifetime Mortgage, interest adds up over time, so there might be less money left to pass on to your family.

- To qualify, you need to be at least 55, and your home must be worth at least £70,000 and in good condition.

- If you choose equity release, you’ll need to think about the costs. These include interest rates and other fees, which can make the total amount you owe grow a lot over time.

The Bottom Line

Equity release can be a game-changer for homeowners who want to make the most of their property’s value without the hassle of moving.

It offers flexibility and freedom, whether you’re looking to boost your retirement income, make home improvements, or lend a helping hand to family. That said, it’s not for everyone.

Taking the time to research, crunch the numbers, and speak to a trusted equity release adviser is key to making an informed decision that suits your needs and future plans.

For your next steps, don’t hesitate to reach out. Simply fill out this quick form, and we’ll link you with an experienced mortgage advisor who can give personalised advice.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I lose ny home through equity release?

Yes, it’s possible but unlikely. The main risk comes if you fail to meet the terms of the agreement, such as not maintaining the property.

But, all equity release products offered by members of the Equity Release Council come with a ‘no negative equity’ guarantee. This ensures that you’ll never owe more than the value of your home.

Can I move house if I’ve taken equity release?

Generally, you can move house after taking equity release. But, your new home must meet the lender’s criteria and the value of the new property will affect the amount you can transfer.

Do I need a lasting power of attorney?

It’s recommended to have a lasting power of attorney in place when taking out an equity release. This ensures that someone can make decisions on your behalf should you become unable to do so.

Can you get out of an equity release plan?

Yes, you can exit an equity release plan, but it can be challenging and costly due to substantial early exit fees. If you’re considering this, always seek professional advice to understand the potential financial implications.

Will my benefits be affected if I take out an equity release?

Yes, taking out an equity release can potentially impact means-tested benefits like Pension Credits and Council Tax Reductions.

The released equity may be considered as part of your assets or income, affecting your eligibility for these benefits.

Can I use equity release to buy a property abroad?

Some lenders may allow this, but it’s not standard. It’s essential to discuss this with your advisor and potential lenders.

Am I allowed to rent out my house If I've released equity from It?

Typically, no. Most equity release plans require you to live in the property as your primary residence. Renting out the property could violate the terms of the agreement. However, there may be exceptions depending on your lender’s policy, so it’s best to discuss this with them directly.

What properties qualify for equity release?

Typically, standard freehold houses and leasehold properties with a long lease remaining are approved for equity release.

But, the specifics can vary by lender, so it’s essential to check with individual providers. Some may accept flats, bungalows, or even properties with certain unique features, while others might not.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Can I Sell My House If I Have An Equity Release?

Selling your home with an existing equity release plan requires careful planning. Many homeowners considering a move – be it closer to family, downsizing, or a lifestyle change – often wonder if equity release complicates the sale. The good news is you can absolutely sell! 🎉 However, for a smooth process aligned with your financial […]

Equity Release Companies to Avoid in 2025: 8 Warning Signs

Equity release is a way for older people to get money from their home without having to sell it. It’s a big choice, so it’s normal to feel a bit unsure about which company to trust. Some companies are great, but others might not have the best intentions. So how do you figure out who’s […]

Equity Release Calculator – No Personal Details Required

Lifetime Mortgages are rapidly gaining traction across the UK, becoming a popular option for homeowners in their retirement years. If you’re curious about unlocking the equity in your home, you’ve come to the right place. How Much Equity Can You Release? Our equity release calculator will provide you with an immediate understanding of the equity […]