- Can You Pay Off Equity Release Early?

- What Happens if I Repay My Equity Release Plan Early?

- Early Repayment Charges Explained

- How To Pay Off Equity Release Early?

- What Is Downsizing Protection?

- Are Early Repayments Permitted by All Lenders?

- What are the Pros and Cons of Early Repayment?

- Should You Pay Off Equity Release Early?

- When Early Repayment Charges (ERCs) Donât Apply

- The Bottom Line

Is It Worth Paying Off Equity Release Early?

Curiosity often strikes when looking at financial commitments, and equity release is no exception.

Perhaps the idea of paying it off early has you wondering: “Will this save money or reduce the stress of long-term repayments?”

The thought of being financially ahead of the game is tempting and worth exploring.

This guide explains how early repayments can work for you, helping you understand the benefits, the challenges, and how to decide if it’s worth it.

Can You Pay Off Equity Release Early?

Yes, you can pay off equity release early.

If you’ve taken out a lifetime mortgage (the most common type of equity release), there are ways to make repayments before the loan is due.

Usually, lifetime mortgages are designed so you don’t have to make payments until something big happens, like moving into long-term care or passing away.

But if you want to pay earlier, you’ve got a few options:

- Pay just the interest to stop the loan from growing.

- Make occasional payments to reduce the total loan amount.

- Pay off the entire loan if that works for you.

Keep in mind that some lenders set rules on how much you can repay each year, like limiting payments to 10% of what you borrowed.

To get the full details of what’s possible with your plan, it’s best to speak with your equity release adviser or provider.

What Happens if I Repay My Equity Release Plan Early?

The outcome depends on the type of plan you have and the rules set by your provider. Here’s what to expect:

If You Have a Lifetime Mortgage

Paying off a lifetime mortgage early might come with an extra fee called an Early Repayment Charge. This is something you would’ve been told about when you first set up the plan.

Some plans don’t have early repayment fees, while others may charge them for a set number of years or for the entire length of the plan.

Talking to your adviser before repaying is key to understanding how this might affect you and choosing the right option for your situation.

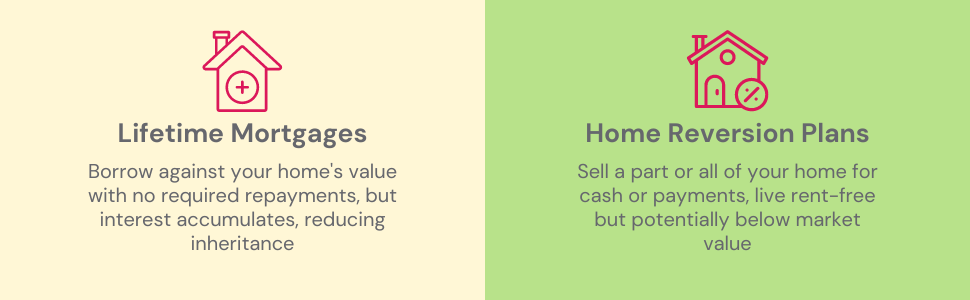

If You Have a Home Reversion Plan

With a home reversion plan, repaying early often means selling the share of your home that you gave to the provider. This might leave you without enough money to buy another property.

Thankfully, the Equity Release Council allows you to move to another suitable property if it’s affordable. This gives you a bit of flexibility if your situation changes.

General Notes on Early Repayment

Equity release plans are usually set up to last until the last borrower dies or moves into long-term care.

When the plan ends, the lender gets back the money they gave you plus any interest that has built up.

However, you do have the option to make partial payments or pay off the entire plan at any time.

Just keep in mind that you might need to pay an extra fee, called an Early Repayment Charge, if you choose to do this.

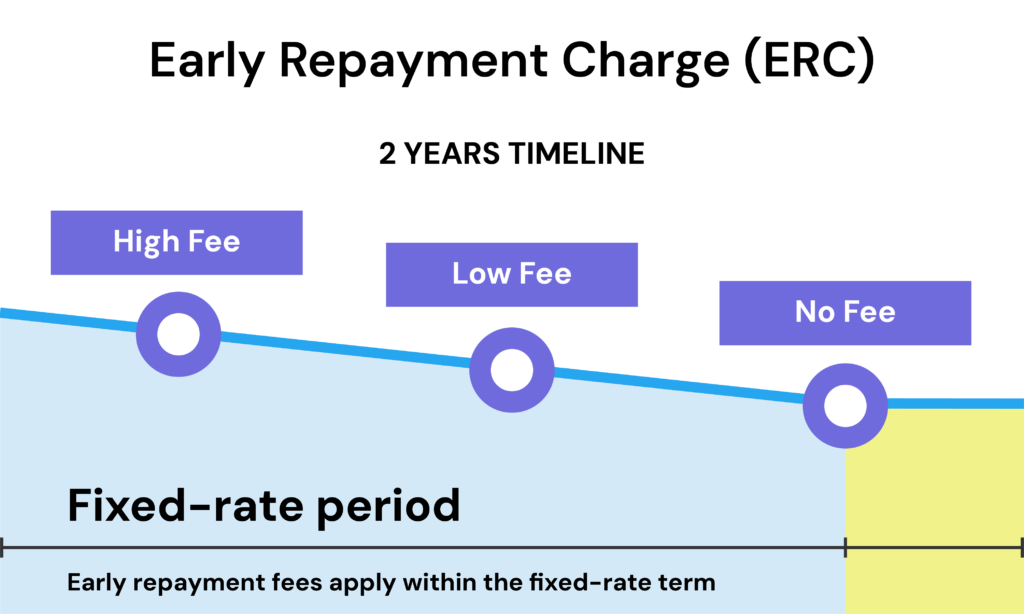

Early Repayment Charges Explained

When it comes to early repayment of equity release, understanding the charges involved is key. Let’s break down the two main types of early repayment charges you might encounter.

Fixed-rate ERCs provide the benefit of clarity right from the start.

You’ll know exactly what rate will be charged if you decide to repay early, eliminating any unexpected costs later on.

For instance, Canada Life is a provider that offers fixed-rate ERCs. Here’s an example of their charges:

| Years | Percentage ERC on the Amount Repaid |

|---|---|

| 1-5 | 5% |

| 6-8 | 3% |

| 9+ | 0% |

Canada Life allows payments at any time, but after any ERC-free exemptions, a charge will be levied on the amount that’s repaid.

Variable Rate Charges Based on Gilts

Variable-rate early repayment charges (ERCs) work differently from fixed ones—they can go up or down.

But, under the rules of the Equity Release Council, there’s always a cap on how high these charges can go.

Before explaining further, let’s break down what gilts are.

Gilts are bonds issued by the British government and are considered a safe investment. Their interest rates, also called yields, can change based on the economy.

For example, Aviva, a provider of equity release plans, uses gilt yields to calculate variable-rate ERCs. Here’s how their charges work:

- Maximum ERC: 25% of the amount borrowed.

- Minimum ERC: 0% (no charge).

The charge depends on how gilt yields change between the time you take out the loan and the day you’re quoted for early repayment.

If gilt yields are lower at the time of your quote, you’ll likely face a fee. This quote is valid for three working days.

In some cases, you might not have to pay any extra charges. But if you repay within the first few years, the fees could be significant.

This highlights how understanding economic factors, like gilts, can be helpful when managing your equity release plan.

If you’re thinking about repaying early, it’s always a good idea to speak to an experienced mortgage adviser. They can guide you through your options.

To make things easier, simply fill out this form, and we’ll connect you with a trusted adviser at no cost or obligation.

Key Takeaways

- Fixed-Rate ERCs – Predictable and set in advance, but may have higher charges in the early years.

- Variable-Rate ERCs – Flexible, potentially no charge, but can be unpredictable and substantial if yields fall.

How To Pay Off Equity Release Early?

Here’s a simple step-by-step guide to help you repay your equity release early:

- Check Your Plan’s Rules. Each lender has its own rules, so it’s important to know what your plan allows. This helps you avoid any surprise costs and figure out if early repayment is the right choice.

- Get Expert Advice. Talking to a specialist equity release adviser is a smart idea. They can explain your options and help you make the best decision for your situation.

- Make the Payment. Once you’re ready, choose how to pay. You can use a one-off direct debit, a regular standing order, a cheque, a bank transfer, or even pay over the phone. Your lender can guide you on what payment methods they accept.

Following these steps makes early repayment much easier. Knowing the costs, understanding the rules, and getting expert advice will help you feel confident about this big financial decision.

What Is Downsizing Protection?

Downsizing protection is a feature some equity release lenders offer. It lets you pay off your loan in full without any extra charges, as long as certain conditions are met.

Despite the name, downsizing protection doesn’t mean you have to move to a smaller home. It applies if you decide to move to a house that doesn’t meet your lender’s rules for equity release.

Each lender has different rules for this feature. A common one is that your loan needs to have been active for a certain time, usually five years, before you can use downsizing protection.

The idea behind this feature is to give you more freedom. If you need to move, you won’t have to worry about paying extra fees just because of your equity release plan.

If you’re planning to move, understanding downsizing protection is important. Talk to your adviser or lender to learn the exact rules so you can make the best choice for your situation.

Are Early Repayments Permitted by All Lenders?

Yes, every lender will let you make early repayments on a lifetime mortgage

Since 28 March 2022, a new rule makes it mandatory for lenders who are members of the Equity Release Council (ERC) to allow partial repayments without a penalty charge.

If your loan is ERC-approved, you can repay some of it early with no extra fee. But remember, this rule only counts for applications made after 28 March 2022. If your loan was taken out after then, you’re free to make early repayments without penalty.

What are the Pros and Cons of Early Repayment?

The following are some of the pros and cons of early repayment:

Pros

- Reducing the overall debt.

- Increasing the potential inheritance for your loved ones.

- Greater financial freedom and flexibility.

- Possibility of securing lower interest rates in the future.

Cons

- Potential high early repayment charges.

- Not all lenders may allow full repayment.

- Loss of certain benefits or features tied to the original agreement.

Before making any decisions, it will be wise to consult with a specialist equity release broker to understand your specific options and potential costs.

Should You Pay Off Equity Release Early?

Paying off equity release early isn’t for everyone, but there are certain situations where it might make perfect sense for you. Let’s explore some of those scenarios and the factors you should consider.

Scenarios Where Early Repayment Makes Sense:

- If you’re selling a property and want to be free from debt, early repayment could be the way forward.

- If you receive an inheritance, you may have the funds needed to reduce or clear your loan.

- If you have extra funds in your pension, paying off equity release could be a smart move.

- If you are moving to a new primary residence and want to buy it without debt on your current property.

Factors to Consider Before Repayment:

- Early Repayment Charges – Depending on your lender, you might face fees.

- Loan Amount – Consider how much you owe and how much you can afford to pay back.

- Financial Goals – Think about your long-term financial plans and how early repayment fits into them.

When Early Repayment Charges (ERCs) Don’t Apply

There are some situations where you don’t have to pay these charges:

- If the last person on the mortgage passes away

- If the last borrower moves into long-term care

- If your plan has special rules – Some plans have exemptions where ERCs don’t apply. These rules depend on the specific plan you have.

If you’re thinking about repaying part or all of your equity release plan early, it’s a good idea to talk to your adviser. They know the details of different plans and can help you choose one that fits your needs.

By planning ahead, you can avoid extra charges if your situation changes later.

The Bottom Line

Equity release is a big financial choice, so having the right information is really important. This guide gives you a good start, but nothing beats advice that’s personalised to your situation.

If you’re thinking about paying off equity release early, talking to an expert can make a huge difference. They’ll help you understand all your options and any costs, making it easier to decide what’s best for you.

No matter your situation, expert help is just a click away. Fill out a quick form, and we’ll connect you with a trusted equity release adviser.

We only work with advisers who are carefully checked to make sure you get top-notch advice you can trust.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

How can I avoid early repayment charges?

Early repayment charges can often be avoided in certain circumstances. For instance, if payments are made after the borrower’s death or if the borrower moves into long-term care, charges generally don’t apply.

Some lenders also have a downsizing protection feature, and others may allow penalty-free repayments up to a specific limit. If you’re planning to move house, you might not have to repay your loan, thus avoiding a hefty charge.

The plan can usually be transferred, as long as the new property fits your lender’s borrowing requirements.

What are the 4 little-known facts about equity release?

- You may have the option to pay interest monthly, keeping it under control.

- Despite common belief, many equity release plans allow you to move home.

- Some plans include a “No Negative Equity Guarantee,” ensuring that you’ll never owe more than your property’s value.

- Not all properties are eligible for equity release; factors like age, location, and condition play a role in eligibility.

Related Articles

Can I Sell My House If I Have An Equity Release?

Selling your home with an existing equity release plan requires careful planning. Many homeowners considering a move – be it closer to family, downsizing, or a lifestyle change – often wonder if equity release complicates the sale. The good news is you can absolutely sell! 🎉 However, for a smooth process aligned with your financial […]

Equity Release Companies to Avoid in 2025: 8 Warning Signs

Equity release is a way for older people to get money from their home without having to sell it. It’s a big choice, so it’s normal to feel a bit unsure about which company to trust. Some companies are great, but others might not have the best intentions. So how do you figure out who’s […]

Equity Release Calculator – No Personal Details Required

Lifetime Mortgages are rapidly gaining traction across the UK, becoming a popular option for homeowners in their retirement years. If you’re curious about unlocking the equity in your home, you’ve come to the right place. How Much Equity Can You Release? Our equity release calculator will provide you with an immediate understanding of the equity […]