- Can I Sell My House If I Have a Fixed Rate Mortgage?

- What Happens If I Sell My House Before the Mortgage Term is Up?

- When Is The Best Time To Sell My House With A Mortgage?

- What Are The Ways To Sell My House With A Mortgage?

- How To Sell A House With A Fixed-Rate Mortgage?

- Dealing with Negative Equity

- What Should I Do If I Donât Need Another Mortgage After Selling?

- The Bottom Line

A Guide To Selling Your House During a Fixed Mortgage Term

Many homeowners wonder if selling before the mortgage term ends is possible, and if so, what it entails.

The answer is yes, you can sell your house with a fixed-rate mortgage. But there are some financial considerations to keep in mind.

This article will explore what happens when you sell a house with a fixed-rate mortgage, including potential costs and how to navigate the process smoothly.

Also, some people think you can’t sell your house during this period. That’s not true—you always can, but the timing might affect your wallet.

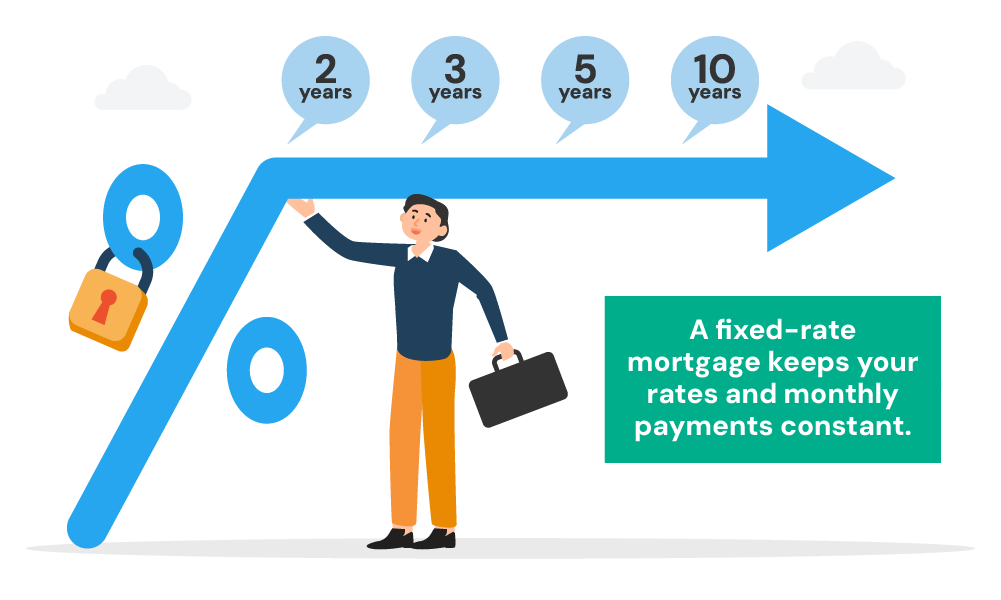

Can I Sell My House If I Have a Fixed Rate Mortgage?

Yes, you can, but let’s look at what that means.

A fixed rate mortgage locks your interest rate for a set period. This could be anywhere from two to ten years. This setup means your monthly payments stay the same, making budgeting easier.

However, selling your house during this period can have implications. The key point here is that while you can sell at any time, there might be extra costs. These are linked to how the fixed rate affects your mortgage terms.

What Happens If I Sell My House Before the Mortgage Term is Up?

When you sell your house before your fixed rate mortgage term ends, there are a few financial matters to handle.

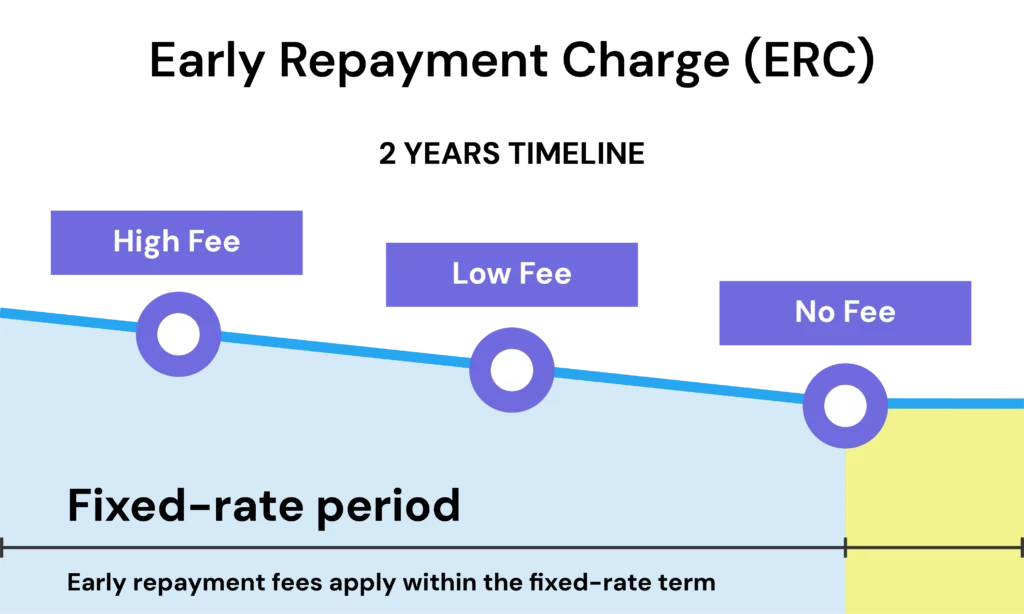

Firstly, you might have to pay an early repayment charge (ERC).

This fee is for the interest your lender will miss out on. ERCs usually range from 1% to 5% of what you still owe.

How much you pay depends on how long is left on your fixed term. For example, if you’re in the first year of a five-year term, the ERC could be higher than if you’re in the fourth year.

Here’s what else happens: when you sell, the money from the sale pays off your mortgage.

If your home sells for more than the mortgage balance, any extra money after paying the ERC and other selling costs is yours.

However, if the sale doesn’t cover your mortgage and the ERC, you’ll need to pay the difference, known as a mortgage shortfall.

You might use your savings for this or perhaps work out a payment plan with your lender.

Let’s say your mortgage balance is £200,000 and the ERC is 3%, you would pay £6,000 for the ERC.

If your house sells for £210,000, you pay off the £200,000 mortgage and the £6,000 ERC, and you keep the remaining £4,000. If the sale price doesn’t cover everything, you need to make up the shortfall.

These fees can affect when you decide to sell your house. Knowing these details helps you plan better and pick the best time to sell, avoiding hefty fees.

When Is The Best Time To Sell My House With A Mortgage?

Every situation is unique, so there’s no one-size-fits-all answer to this question.

But here are some ideal scenarios where it might be best to sell your house, even if you have a fixed-rate mortgage and might face an Early Repayment Charge (ERC):

- When your fixed-rate period is about to end. You might avoid large ERCs if you wait just a bit longer.

- If house prices are high and you can make a good profit, even after paying any ERCs.

- When you need to move for a new job or personal reasons, and it can’t wait until the mortgage term ends.

- If you’re downsizing and the money saved on cheaper living costs outweighs the ERC.

- When interest rates are low, and you can secure a new mortgage at a better rate even after paying the ERC.

- If you’ve found your dream home and it might not be available later, it could be worth the extra cost now.

- When changes in your personal life mean you need to change your living situation quickly.

Choosing the right time depends on balancing costs with your personal needs and market conditions.

What Are The Ways To Sell My House With A Mortgage?

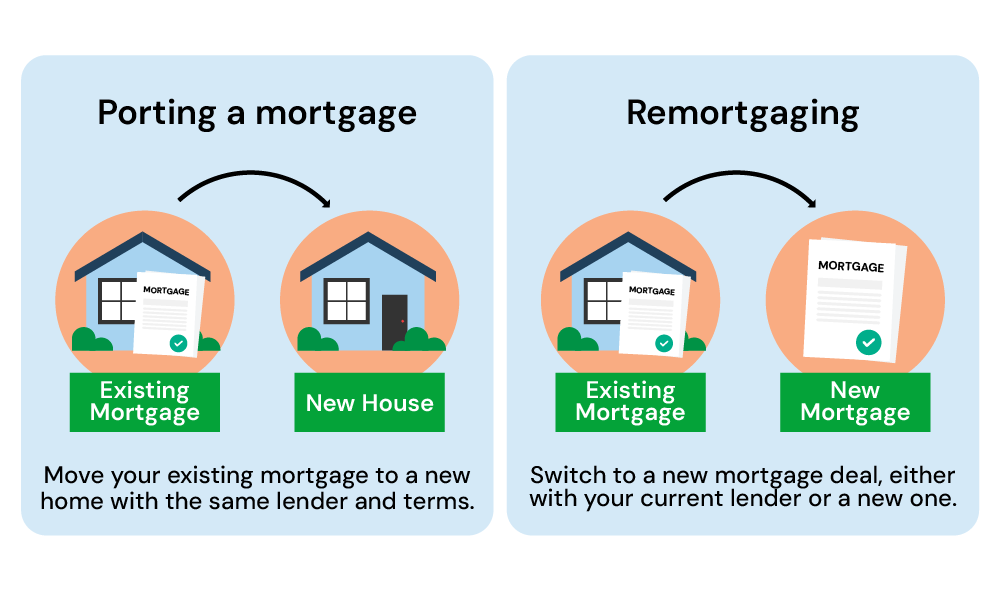

You’ve got TWO options: porting your mortgage or remortgaging. Here’s what you need to know about each option.

Porting Your Mortgage

Porting your mortgage means you take your current mortgage deal and move it to your new house. It’s useful if you’re happy with your mortgage’s interest rate and terms.

This way, you can avoid paying early repayment charges, which can be costly. But, porting isn’t always possible.

Your lender will need to approve the new property, which must meet their lending criteria. They might also ask you to pass an affordability test again to make sure you can still manage the payments.

If the new house is more expensive, you might need to borrow more, and this part could be at a different rate.

Remortgaging

If porting is not possible, one common choice is applying for a new mortgage, or remortgaging.

This means you start fresh with a new mortgage deal. And this might be a good choice if you find a better interest rate or more suitable terms.

With remortgaging, you can adjust the loan amount to better fit your new property’s price, especially if it’s higher.

When you remortgage, you’ll have to go through the approval process again, which includes proving your income and other financial details.

Keep in mind, as we’ve discussed earlier, you might face early repayment charges from your old mortgage when you switch. So, it’s important to check if the savings with a new mortgage will outweigh these costs.

Pro Tip:

When making a decision, think about what’s most important for your financial situation.

It’s wise to talk to a mortgage advisor who can help you compare the costs and benefits of each option. They’ll help you make a decision that fits your needs and financial plans.

How To Sell A House With A Fixed-Rate Mortgage?

Selling a house with a fixed-rate mortgage is a common process. Here’s a breakdown of the key steps:

- Know Your Numbers. Find out the payoff amount for your mortgage, which includes the remaining balance, interest, and any fees. This will help you calculate how much profit you’ll make after the sale.

- Price it Right. Set a selling price that covers your payoff amount, closing costs, estate agent fees, potential early repayment charges on your mortgage, legal fees, and other selling expenses.

- Get Help from a Pro. Hiring a qualified estate agent is recommended. They can guide you through the process, market your house effectively, and negotiate with potential buyers.

- Spruce Up Your Property. Before listing your house, clean, declutter, and make any necessary repairs to improve its presentation and attract buyers.

- Market and Negotiate. Your estate agent will list your property and handle marketing. Be prepared to negotiate offers and make adjustments if needed.

- Accepting an Offer and Finalising the Sale. Once you accept an offer, the legal procedures to transfer ownership will begin. The sale proceeds will be used to pay off your mortgage. Any remaining amount will be yours.

Dealing with Negative Equity

Selling a home with negative equity can be tricky since the sale price might be less than what you owe on your mortgage. Here are a few ways to handle this situation:

If you’re not in a hurry to sell, you could WAIT for property values to go up.

During this time, it’s a good idea to talk to your lender about any options they might have to help you manage your negative equity.

Another approach is a SHORT SALE, where you sell your home for less than the outstanding mortgage with your lender’s approval.

This could mean your lender might forgive the remaining debt, or they might ask you to pay it back over time.

Keep in mind, though, that a short sale can harm YOUR credit score.

Image that compares to options when dealing with negative equity – Wait and Short Sale. Then the consequences.

What Should I Do If I Don’t Need Another Mortgage After Selling?

If you’re selling your home and don’t plan to buy another one immediately, you have several options.

Maybe you’re thinking about renting, moving in with a partner, or even downsizing. Each choice comes with different financial considerations.

Firstly, if you’re paying off your mortgage in full from the sale, you might still face ERCs, depending on your mortgage terms. Make sure you know how much these fees are so you can plan your finances properly.

If you’re downsizing or changing your living situation significantly, think about how this impacts your budget and lifestyle.

Selling a home and moving to a different living arrangement can FREE up cash and REDUCE expenses, which might be exactly what you need at this stage in your life.

Whatever your situation, planning ahead and considering all your options will help you make a smooth transition from selling your home to your next step.

The Bottom Line

Selling your house with a fixed-rate mortgage can be straightforward. The key is planning ahead and understanding your options. Here’s where a mortgage broker comes in handy.

Mortgage brokers are experts who can explain the different deals available and recommend the BEST one for you. They’ll compare costs and SAVE you time, ensuring you avoid expensive mistakes.

They can also handle the complex paperwork involved, whether you’re keeping your current mortgage or starting fresh. This makes the whole process much easier for you.

Need a broker? Reach out to us. We can connect you with a qualified professional who will guide you through selling your house with a fixed-rate mortgage. They’ll ensure you make the BEST decision for your situation.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

How long does it take to sell a house with a mortgage?

The timeframe can vary depending on the market, property condition, and buyer demand. It typically takes 2-3 months on average in the UK, but can be shorter or longer.

Can I sell if I'm in negative equity or underwater on my mortgage?

Yes, but you’ll need to cover the difference between the sale price and what you owe on your mortgage. You can explore options like a short sale or waiting for the property value to increase.

Can I sell if I have an interest-only mortgage?

Yes, but you’ll need to pay off the entire loan balance when you sell the house.

Can I sell if I'm behind on mortgage payments (arrears)?

Yes, but any outstanding balance, including arrears, needs to be paid off at closing.

Do I need to tell my lender I'm selling?

Yes, your lender can provide a payoff statement and may have requirements for selling your property.

Can I sell if I have a second mortgage?

Yes, you can sell your house with a second mortgage. But here’s the thing: the sale money pays off your first mortgage first. Then, whatever’s left goes towards your second mortgage.

The key is, the selling price needs to cover both loans entirely. If it doesn’t, you’ll be responsible for the remaining amount unless you sort things out with your lenders.

To avoid any hitches, talk to both mortgage lenders and consider getting a financial advisor’s help for the smoothest sale possible.

Can I sell if I have a buy-to-let fixed-rate mortgage?

Yes, you can sell your property with a buy-to-let fixed-rate mortgage. Keep in mind, if you pay off this mortgage early because you’re selling, you might have to pay early repayment charges (ERCs).

Before you sell, check your mortgage terms to see the potential costs of early repayment.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How Long Should I Fix My Mortgage For? 2,3, or 5 Years?

For homebuyers and owners in the UK, deciding whether to fix your mortgage interest rate can be a tough decision. With rates RISING rapidly over the past year, securing a fixed rate deal protects you from further hikes – but it also locks YOU into a deal if rates start to fall again. This guide […]

What Happens When Your Fixed-Rate Mortgage Ends?

As your fixed rate mortgage draws to a close, it’s natural to ponder what lies ahead. 🤔 Whether your deal was locked in for 2 years or stretched out over 5, the end of this period marks a significant turning point in your mortgage journey. Let’s explore what’s in store when your fixed term is […]

What is a Long-Term Fixed Rate Mortgage?

A long-term fixed rate mortgage allows you to lock in an interest rate for an extended period, often 5 years or longer. With a traditional fixed rate deal, your interest rate is only set for 2-5 years before you need to remortgage. But with a long-term fixed, you can secure your rate for 10, 15, […]