- What is a Fixed Rate Mortgage?

- How Do Fixed Rate Mortgage Periods Work?

- What are the Current Best Fixed Mortgage Rates?

- Should I Fix My Mortgage Rate Now?

- How to Choose Between a 2, 3 or 5 Year Fixed Mortgage

- Is a 10 Year Fixed Mortgage a Good Idea?

- Is It Better To Fix My Mortgage Longer?

- How to Find the Best Fixed Rate Mortgage Deal

- Fees to Watch For on Fixed Rate Mortgages

- Is It Ever Worth Paying an ERC to Get a Better Rate?

- When Do Fixed Mortgages Not Make Sense?

- Key Takeaways

- The Bottom Line

How Long Should I Fix My Mortgage For? 2,3, or 5 Years?

For homebuyers and owners in the UK, deciding whether to fix your mortgage interest rate can be a tough decision.

With rates RISING rapidly over the past year, securing a fixed rate deal protects you from further hikes – but it also locks YOU into a deal if rates start to fall again.

This guide weighs up ALL the key considerations around 2, 3 and 5 year fixed rate mortgage deals.

We cover what fixed rates actually are, current rates on offer, the pros and cons of fixing, and how to choose the right fixed period for your circumstances.

What is a Fixed Rate Mortgage?

A fixed rate mortgage gives you the same interest rate for a set period.

This is different from a variable or tracker mortgage where the rate can change based on the Bank of England’s base rates, your lenders’ discretion, or other economic factors.

The main benefits of a fixed rate mortgage are:

- Protection from interest rate rises during the fixed period

- Ability to budget easily without repayment changes

- Avoids risk of rates spiking uncontrollably

With a fixed rate deal, you have true repayment SECURITY for the fixed term length, regardless of wider interest rate volatility. 🔐

How Do Fixed Rate Mortgage Periods Work?

Fixed rate mortgages come in different lengths—commonly 2, 3, 5, or even 10 years.

Once the fixed rate period ends, your mortgage will typically revert to your lender’s standard variable rate (SVR).

At this stage, you can either remain on the SVR, take out another fixed period, or remortgage to a new lender entirely for a new deal.

One key thing to note is that fixed rate mortgage deals have early repayment charges (ERCs) for exiting the fixed period early. These charges can be quite steep, so it’s good to be sure about your term length when you first apply.

What are the Current Best Fixed Mortgage Rates?

With Bank of England base rates at 5.25%, fixed-rate mortgage rates forecast from Pound Forecast UK are as follows:

- 5.76% for a 2-year fixed rate

- 4.96% for a 5-year fixed rate

In general, the LONGER the fixed rate period, the HIGHER the rate will be. Yet, with current trends and expectations for UK rates to vary, locking in a longer rate like a 10-year fixed can be wise.

It’s important to understand that fixed mortgage rates don’t just track the Bank of England’s base rate directly.

They are influenced by a range of factors that lenders ‘bake in’ to their pricing models, including:

- Inflationary pressures and expectations

- Demand for fixed vs variable rate products

- Each lender’s competitive position

- Overall cost of funds for the lender

So while the base rate is a core component, fixed mortgage rates can move disproportionately to the base rate based on market conditions.

Should I Fix My Mortgage Rate Now?

There are pros and cons to fixing your mortgage rate now amid the current economic climate:

Pros of Fixing Now

- Protection if interest rates rise further

- Budgeting stability for the fixed period

- Avoids the risks of volatile tracked rates

Cons of Fixing Now

- You may miss out on lower rates if they fall

- Rates may continue rising before peaking

- Early repayment charges for exiting early

Signs That May Suggest Fixing Soon

- The Bank of England indicates more base rate rises are likely

- Inflation remains persistently high, putting pressure on rates

- You prioritise payment security over potential future savings

Signs It Could Be Better to Wait

- Economists forecast interest rate cuts in the next 12-18 months

- Inflation falls sharply in line with the BoE’s 2% target

- You have a higher risk tolerance for volatile mortgage costs

Ultimately, fixing your mortgage rate provides reassurance but means you could potentially miss out on lower rates in future.

It’s about weighing up your need for budgeting stability now versus potential savings down the line.

How to Choose Between a 2, 3 or 5 Year Fixed Mortgage

Once you’ve decided that fixing your mortgage rate is right for your circumstances, you then need to consider the fixed period length.

The most common options are 2 years, 3 years or 5 years.

2 or 3 Year Fixes

- Lower rates than longer fixes currently

- Suits those planning to move again soon

- Ability to review options again quickly

- Risk of rates rising before you can fix again

5 Year Fixes

- Longer-term security from rate volatility

- Avoids multiple product transfers & fees

- Slightly lower rates than 2/3 year deals currently

- Less flexibility if you want to move home

So a 2 or 3 year deal gives you short-term security at a relatively low rate but less long-term certainty.

A 5 year fix costs more initially but provides lasting security and avoids having to switch products multiple times.

It depends on your homeownership plans, willingness to chase lower rates again soon, and your overall appetite for interest rate risk.

Is a 10 Year Fixed Mortgage a Good Idea?

While less common, some lenders do offer extended 10 year fixed rate mortgage periods. This gives homeowners a full decade of payment security.

The main advantages of a 10 year fixed deal are:

- Ultra long-term interest rate protection (helpful if you expect high rates for years)

- Avoids multiple remortgage product transfer fees & hassle

- Potentially a lower rate than fixing for 5 years multiple times

However, the BIG downside is that if rates do start to drop significantly during that 10 year lock-in.

You could end up paying over the odds compared to variable rates or shorter fixed periods. You’d likely also face hefty ERCs for trying to exit early.

10 year mortgage deals do provide exceptional long-term security. But most mortgage experts only really recommend them for those with an extremely low risk tolerance who want to fix their housing costs for the next decade regardless.

Is It Better To Fix My Mortgage Longer?

Deciding how long to fix your mortgage rate depends on what makes you feel safe and how much you want to pay each month.

Here’s a look at some current rates for different fixed periods:

| LTV | 2 years fixed-rate | 3 years fixed-rate | 5 years fixed-rate | 10 years fixed-rate |

|---|---|---|---|---|

| 60% LTV | 4.33% | 4.54% | 4.63% | 4.64% |

| 75% LTV | 4.65% | 4.79% | 4.70% | 4.79% |

| 80% LTV | 4.88% | 4.87% | 4.73% | 4.94% |

If you expect interest rates to rise, locking in a longer term could protect you against higher costs.

If rates might fall, a shorter term could offer savings later. Consider what feels RIGHT for managing your future payments.

>> More about Long-term fixed rate mortgages

How to Find the Best Fixed Rate Mortgage Deal

With so many lenders offering their own range of fixed rate deals across 2, 3, 5 and 10 year periods–and varying their qualifying criteria–using an independent mortgage broker is wise.

A good whole-of-market broker will take the time to understand your financial circumstances, home ownership plans and priorities around interest rate risk.

They can then scan deals from across the entire market to identify the most suitable options for YOUR needs.

As well as comparing pure interest rates, they’ll evaluate the overall cost factoring in arrangement fees, valuation charges, incentives and any expected early repayment charges.

Good brokers can also assess your eligibility for deals upfront to smooth the approval process.

An experienced broker’s expertise around ever–changing affordability criteria from lenders can prove invaluable when securing the right fixed rate deal.

Fees to Watch For on Fixed Rate Mortgages

While securing a fixed rate mortgage provides peace of mind and budgeting certainty, there are some extra costs to be wary of that can mount up compared to variable rate deals:

- Arrangement/Booking Fees (often ranges from £500-£1,000+ fee for setting up the mortgage)

- Valuation & Legal Fees

- Early Repayment Charges (usually 1-5% of your outstanding mortgage balance)

- Broker fees

- Exit fee (costing around £75-£300)

Some fee-free fixed rate options are available, but these tend to have even higher interest rates to compensate the lender for the lack of upfront revenue.

It may seem tempting to avoid fees by sticking with your existing lender’s deal. But their rate may be less competitive, in which case the hassle of remortgaging saves you far more over the deal period.

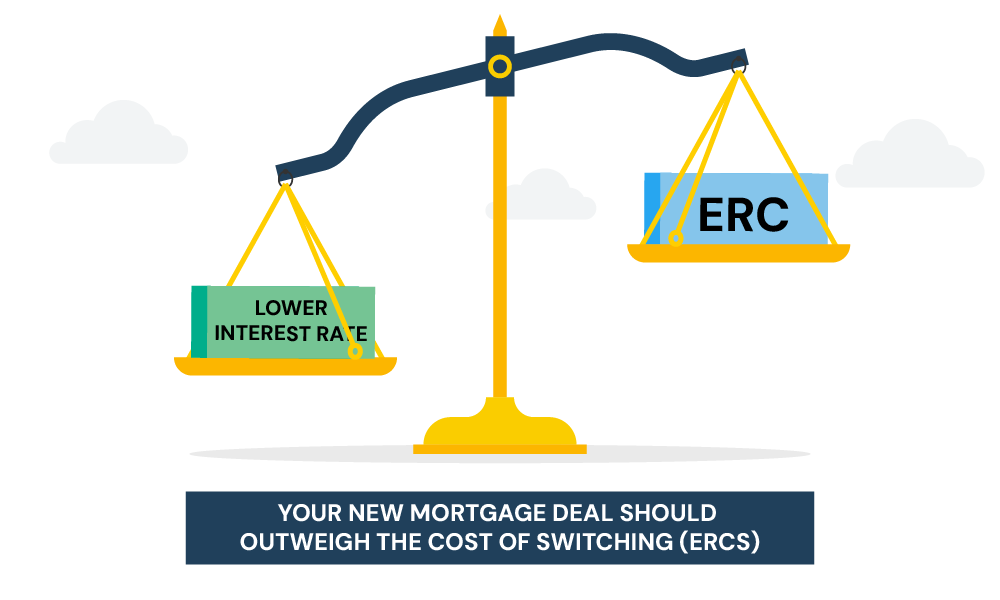

Is It Ever Worth Paying an ERC to Get a Better Rate?

It depends.

Sometimes, paying an ERC early makes financial sense to exit your current fixed-deal and get a LOWER new mortgage rate. But, you have to do the sums first. 🧮

Here are few ideal scenarios to guide you:

- Interest rates have dropped DRAMATICALLY since you originally fixed your deal. The bigger the difference, the more you could save by switching to a new deal, even after paying the ERC.

- You still have a LONG fixed period remaining until your current deal ends. The longer you can benefit from the new lower rate, the more it could offset the upfront exit penalty.

As a rough rule of thumb: if the ERC cost can be recouped through interest savings within around 12 months, remortgaging might be worth it.

To figure it out, compare the ERC cost to how much you’d save in interest by switching to the new deal.

Speaking to a mortgage broker can help YOU crunch these numbers properly. ✨

You could also explore options with your current lender, like a rate switch or product transfer. These let you move to a new deal without an ERC, but the rates might not be quite as good as remortgaging completely.

When Do Fixed Mortgages Not Make Sense?

While fixed rate deals provide welcome security, they don’t always make the most sense for every borrower’s situation.

There are certain scenarios where opting for a variable or tracker rate mortgage could be MORE suitable.

If you only plan to be in your home for a relatively short period, say 2-3 years, then variable trackers might be cheaper. It’s a bit of a gamble if rates go up, but you could save some cash in the short term.

People who are comfortable with interest rates going up and down, and those who are a bit more adventurous with their money, might also consider a variable rate. This lets you lock into a fixed rate later if you want to play it safe.

Another reason to skip the fixed rate is if you expect your income to change soon, such as after starting a family. It might be better to wait until your finances are more settled before locking into a long fixed term.

Fixed rates give you peace of mind, but they can cost you more.

If you’re looking for the absolute lowest rate or need maximum flexibility, a variable or tracker deal could be the way to go.

Key Takeaways

- Fixed rate mortgages give you stable monthly payments, protecting you from rising interest rates.

- Common fixed periods are 2, 3, or 5 years, with shorter terms offering lower rates and more flexibility, while longer terms provide extended security.

- A 10-year fixed rate provides long-term stability but could cost you more if rates drop.

- If you leave your fixed deal early, you might face early repayment charges (ERCs), so weigh the costs before switching.

- Fixed rates may not suit you if you want flexibility or expect your finances to change soon.

The Bottom Line

In conclusion, the decision to fix your mortgage rate depends on YOUR priorities.

Fixing offers security but may cost more in the long run if rates fall. Variable or tracker mortgages could be cheaper for short-term ownership or if you expect rate cuts.

Consider your risk tolerance and financial plans to choose the best option for you. Choose the option that lets you sleep soundly at night.

To make the best decision, talk to a good mortgage broker. They can guide you through the process and help you find the right lender and the best mortgage deal for you.

Need help finding a qualified broker? We can help, simply contact us and we’ll connect you with an expert who can help with your mortgage.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Is it best to fix your mortgage for 2 or 5 years?

Choosing between fixing your mortgage for 2 or 5 years depends on your financial goals and expectations about interest rate changes.

A 2-year fix usually offers lower rates and flexibility, but a 5-year fix provides longer stability, which might be preferable if you expect rates to rise.

For personalised advice, get in touch with us and we’ll arrange a free, no obligation consultation with a good mortgage advisor.

Should I fix my mortgage now in 2024?

Fixing your mortgage in 2024 could be wise if you want to guard against potential future rate increases. Current forecasts and economic conditions suggest that locking in a rate now could provide financial security as rates might fluctuate.

Will interest rates go down in 2024?

Mortgage rates might gradually fall throughout 2024 and beyond, depending on the economy and financial markets. But these predictions can change due to global events, so keep an eye on the latest financial news.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

What Happens When Your Fixed-Rate Mortgage Ends?

As your fixed rate mortgage draws to a close, it’s natural to ponder what lies ahead. 🤔 Whether your deal was locked in for 2 years or stretched out over 5, the end of this period marks a significant turning point in your mortgage journey. Let’s explore what’s in store when your fixed term is […]

What is a Long-Term Fixed Rate Mortgage?

A long-term fixed rate mortgage allows you to lock in an interest rate for an extended period, often 5 years or longer. With a traditional fixed rate deal, your interest rate is only set for 2-5 years before you need to remortgage. But with a long-term fixed, you can secure your rate for 10, 15, […]

Should I Get A Fixed Or Variable Rate Mortgage?

Right, so you’re taking out a mortgage – exciting times! But a big decision you need to make is whether to fix your interest rate or let it vary. This choice affects your monthly payments and the total cost of the mortgage for years to come, so it’s worth getting it right. Let’s break down […]