What is a Long-Term Fixed Rate Mortgage?

A long-term fixed rate mortgage allows you to lock in an interest rate for an extended period, often 5 years or longer.

With a traditional fixed rate deal, your interest rate is only set for 2-5 years before you need to remortgage. But with a long-term fixed, you can secure your rate for 10, 15, 20 years or more.

So what exactly are the benefits of these lengthy fixed rate periods? And are there any downsides to consider?

Let’s explore long-term fixes in depth.

Why Choose a Long-Term Fixed Rate Mortgage?

One of the primary advantages of a long-term fixed rate is budgeting certainty.

With your interest rate locked for 10+ years, you know exactly what your monthly mortgage payments will be during that time frame.

This makes it much easier to plan your finances long-term without ANY surprises from rate hikes.

Rate security is another big draw. While no one can predict future interest rates with certainty, most economists expect them to rise from current lows over the next decade.

Fixing for 10 or 15 years allows you to SKIP any rate increases and potential payment shocks during that period.

Additionally, long-term fixes can SAVE you money in the long run.

With shorter fixes, you’d have to keep remortgaging every few years to avoid switching to the lender’s variable rate, which can be pricier.

Each remortgage comes with fees, often over £1,000. A long-term fix means potentially just one remortgage, or even none at all, saving you a chunk of cash.

But it’s not just about the money. A long-term fixed rate mortgage brings peace of mind.

You won’t be glued to the financial news, stressing about rate changes. Instead, YOU can relax, focus on life, and leave the mortgage juggling to someone else.

Image to show the benefits of long term fixes

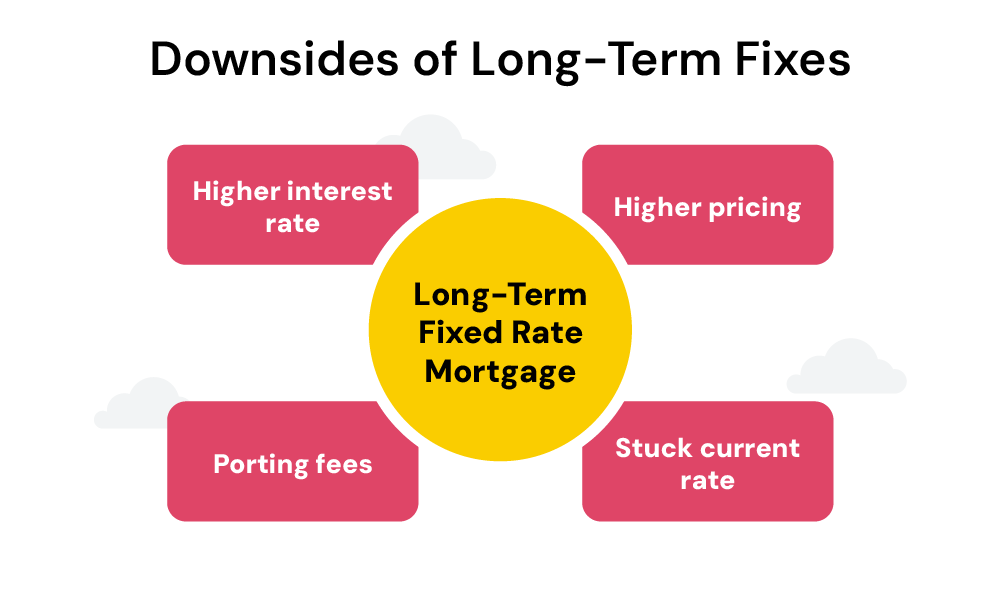

The Potential Downsides of Long-Term Fixes

The big trade-off with longer fix periods is that the interest rate is typically HIGHER than a short-term fixed rate deal.

Lenders charge a premium for the additional rate security. However, the gap between short and long-term pricing has narrowed in recent years.

Another thing to consider is that you miss out if interest rates drop overall. If that happens, you’re stuck with your current rate until the fixed term ends. (No sweet savings for you 😞).

Also, if you want to pay extra off your mortgage early, you might get hit with BIG early repayment charges (ERCs), especially with a long fix.

These typically apply if you pay more than a certain amount, like 10% of your balance in a year. So think carefully about whether you plan to smash through those payments early on.

Finally, if you think you might move and want to take your mortgage with you (called porting), it can be trickier and pricier with a long fix.

Porting fees can sting a bit, and you get more flexibility with shorter fixed terms. So weigh up how long you plan to stay put before locking in for the long haul.

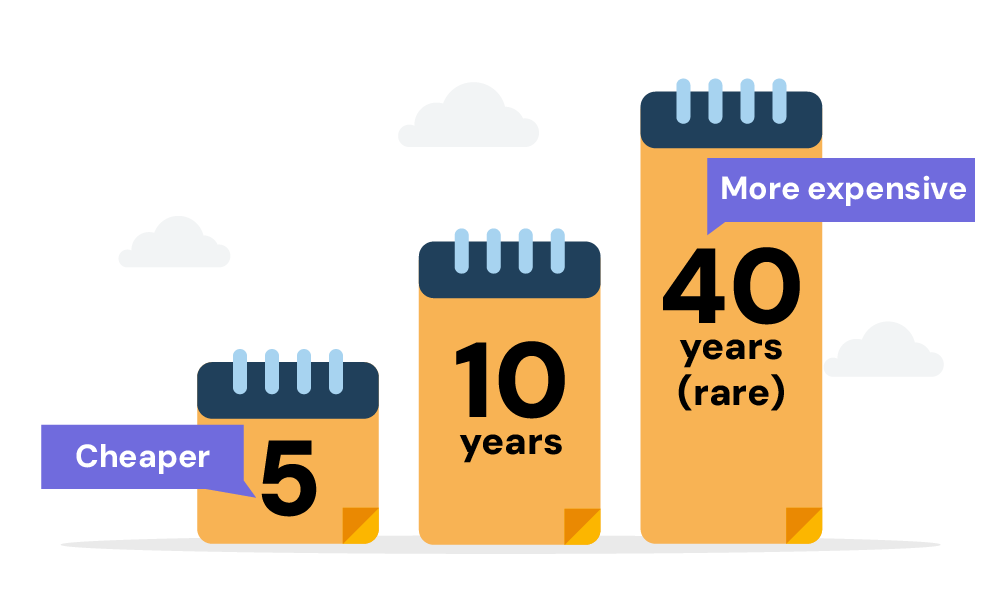

How Long Can You Fix Your Rate For?

Most UK lenders allow you to fix for a maximum of 10 years currently. Some may offer 15 or even 20-year options.

At present, the longest widely available fixed rate mortgage in the UK lets you secure your interest for 40 years until the very end of your mortgage term. However, this is incredibly rare.

Historically, most borrowers have chosen 2 or 3-year fixed rate periods. But with longer rates being more competitive these days, folks are increasingly going for 5 years or more.

The idea is to get some peace of mind knowing EXACTLY what your mortgage payments will be for a LONG time.

Is a Long-Term Fixed Rate Right for You?

Long-term fixed rate mortgages lock in your interest rate for over 10 years, which is a smart move for most homeowners planning to stay put. If rates are really low right now, you can snag cheap monthly payments for over a decade.

Hold on though, if you think you might move soon, these mortgages can sting with hefty exit fees. Also, if you’re sure rates will keep dropping, a shorter fixed term might be better to grab even lower rates later.

But for most folks who just want peace of mind and protection from future rate hikes, a long-term fix is a great option. It lets you relax and focus on life, knowing your mortgage payment won’t jump on you.

The Bottom Line

Long story short, long-term fixed rates give you peace of mind – you know exactly what you’ll be paying for years to come, with no nasty rate surprises.

Whether you fix for 10 years or even longer, you can budget for the future with certainty, knowing one of your biggest bills is locked in.

But, no matter what time frame you’ve fixed your mortgage, it’s smart to assess ALL your options. 😎

Different lenders have different rates and fees, so the flashiest deal might not actually be the cheapest in the long run.

This is where a whole-of-market mortgage broker can be your best mate.

They see all the deals from all the lenders, so they can find the best fit for you, taking into account all the costs. They basically do the legwork so you don’t have to wade through a swamp of options.

Looking for the best broker? We can help you. Simply, get in touch, and we’ll pair you with a qualified mortgage advisor who can help you find and get the BEST mortgage deals.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

Are long term fixed-rate mortgages a good idea?

Long-term fixed-rate mortgages are great if you like knowing exactly what your bills will be. You lock in a rate for years (usually 5 years or more), so even if interest rates go up in general, your mortgage payment stays the same.

That’s a big plus if you plan to stay put in your home for a long time. The downside is that these mortgages might have a slightly higher interest rate than shorter ones, and they can be less flexible if your life takes an unexpected turn.

In the end, whether a long-term fixed-rate mortgage is right for you depends on your finances and what you see happening in your future.

What's the longest fixed term mortgage?

In the UK, the longest fixed-term mortgages can extend up to 40 years. These are less common than shorter terms and are typically offered by a select few lenders.

This might be right up your alley if you crave guaranteed payments for decades and don’t mind locking into one interest rate for the whole ride.

Can I get a 40 year fixed-rate mortgage?

You can definitely grab a 40-year fixed-rate mortgage in the UK, although they’re not widely available like shorter ones.

These super-long deals are great if you want rock-solid payments for decades and are happy sticking with one interest rate the whole time.

But before diving in, shop around with different lenders to make sure it fits your wallet and plans.

How many years is the best fixed-rate mortgage?

There’s no one-size-fits-all answer for the best fixed-rate term, it depends on your life situation.

Shorter fixes, like 2 or 3 years, typically come with lower rates and more flexibility, but you’ll need to remortgage more often, which can mean extra fees.

Longer fixes, like 5, 10, 20 or even 40 years, lock you in for a longer period with more predictable payments, but the interest rate might be a bit higher.

Think about how risk-averse you are, how stable your finances are, and how long you plan to stay in your home.

Talking to a qualified mortgage broker can help you pick the term that’s best for your situation.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How Long Should I Fix My Mortgage For? 2,3, or 5 Years?

For homebuyers and owners in the UK, deciding whether to fix your mortgage interest rate can be a tough decision. With rates RISING rapidly over the past year, securing a fixed rate deal protects you from further hikes – but it also locks YOU into a deal if rates start to fall again. This guide […]

What Happens When Your Fixed-Rate Mortgage Ends?

As your fixed rate mortgage draws to a close, it’s natural to ponder what lies ahead. 🤔 Whether your deal was locked in for 2 years or stretched out over 5, the end of this period marks a significant turning point in your mortgage journey. Let’s explore what’s in store when your fixed term is […]

Should I Get A Fixed Or Variable Rate Mortgage?

Right, so you’re taking out a mortgage – exciting times! But a big decision you need to make is whether to fix your interest rate or let it vary. This choice affects your monthly payments and the total cost of the mortgage for years to come, so it’s worth getting it right. Let’s break down […]