- How Do Guarantor Mortgages Work?

- Who Can Be a Guarantor?

- What Types of Guarantor Mortgages Are Available?

- Who Are Guarantor Mortgages For?

- What Are The Benefits of Guarantor Mortgages?

- What Are the Risks Involved?

- How Much Can I Borrow?

- Where Can I Get a Guarantor Mortgage in the UK?

- Can I Get a Guarantor Mortgage With Bad Credit?

- Are There Alternatives to Guarantor Mortgages?

- The Bottom Line: Is a Guarantor Mortgage Right for Me?

What Are Guarantor Mortgages? A Complete Guide

Struggling to get on the property ladder? 🏠

A guarantor mortgage could be your way in – even with no deposit or poor credit history.

With this type of mortgage, someone else (usually a parent or close relative) agrees to cover your repayments if you can’t make them.

Interested to learn more? Let’s dive into how guarantor mortgages work.

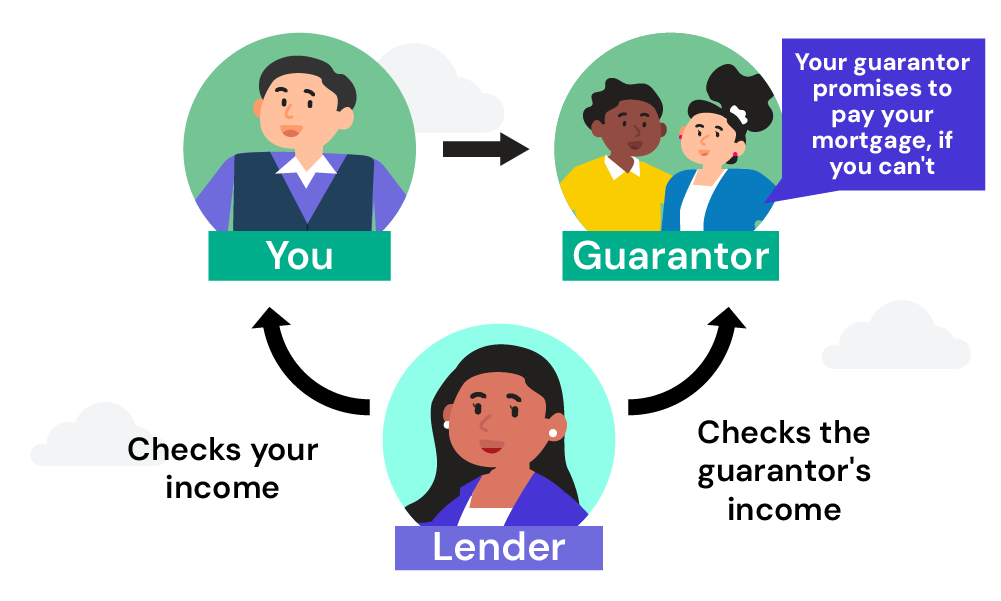

How Do Guarantor Mortgages Work?

Guarantor mortgages offer extra security to lenders.

Unlike a normal mortgage where just the house is security, a guarantor adds their own home (or savings) as a backup.

Here’s how it works:

The lender gets your guarantor to sign a legal agreement. This means if you miss repayments, the GUARANTOR must cover them.

The guarantor’s property is then linked to the mortgage. If neither you nor the guarantor can pay, the lender can force the sale of the guarantor’s home to get their money back.

This lowers the risk for the lender, so they’re more likely to approve you for a mortgage even if you have a small deposit or bad credit.

Essentially, your guarantor is putting their own financial neck on the line to help you get a mortgage.

Who Can Be a Guarantor?

Almost anyone can be a guarantor, but lenders prefer someone with a strong financial position to back you up. This is typically:

- A parent or close family member with a stable income.

- Someone who owns their own home outright or has a lot of equity in it (meaning most of the mortgage is paid off).

- Someone with a good credit score.

- Ideally, a close relative like a parent or sibling (some lenders require this).

Being a guarantor is a serious commitment, so think carefully and get legal advice before saying yes

What Types of Guarantor Mortgages Are Available?

The main types you’ll find on the market are:

- Using Property as Security – This means the lender can repossess the guarantor’s home if you don’t keep up with repayments. This is a big risk for the guarantor, so choose someone very carefully.

- Savings as Security – The guarantor puts a lump sum of cash into an account the lender holds. This pot can then be accessed if you default. The good news is the guarantor gets interest on the money, but the bad news is they might not be able to access it for a long time.

- Family Offset – The guarantor’s savings offset against the mortgage balance, reducing the amount of interest you pay each month. Their money is still secure unless you miss payments.

- Family Link – You borrow most of the money (90%), and your guarantor takes a smaller loan for the rest (10%) secured on their property. They have to repay this smaller loan within 5 years. If you default, your guarantor is only responsible for that 10%.

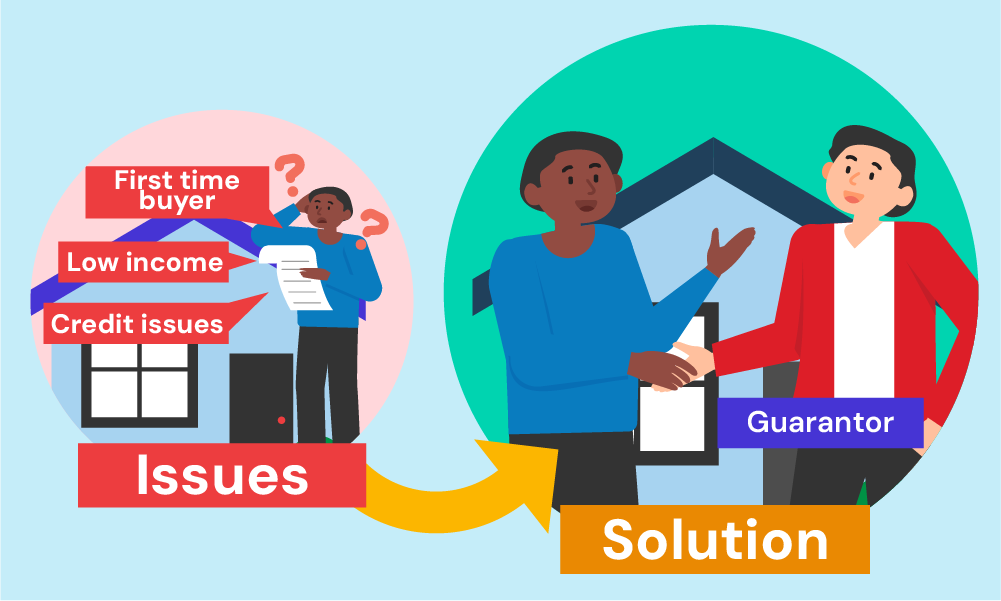

Who Are Guarantor Mortgages For?

A guarantor mortgage could be ideal if:

- You have a low deposit (or none at all) saved up

- Your credit file is thin or marred by issues like defaults

- You’re a young first-time buyer struggling to get approved normally

Adding a guarantor helps you bypass some borrowing restrictions. You might even get a 100% mortgage with no deposit from some lenders.

Of course, you’ll still need to show you can afford the mortgage:

- Regular income to cover at least the interest payments

- Proof of employment or stable self-employment income

There are also some basic requirements:

- You (usually) need to be 18 or older, and some lenders have a maximum age limit.

- Your guarantor needs a good credit score, strong property equity, or other assets to back you up.

- Both you and your guarantor must be UK residents.

These checks make sure you and your guarantor are ready for the financial commitment.

What Are The Benefits of Guarantor Mortgages?

Guarantor mortgages offer a helping hand to get on the property ladder, especially if you’d struggle with a regular mortgage. Here’s how:

- Easier to get approved. You can qualify even with a small deposit or no credit history. The guarantor’s backing reassures the lender.

- Borrow more. As we’ve discussed, with a guarantor’s guarantee to cover missed payments, lenders might offer a larger loan or even 100% of the property value, so you don’t need a deposit.

- Potentially lower interest rates. The guarantor reduces the risk for the lender, so you might get a better interest rate.

- Build your credit .If you have no credit history, making repayments on time helps build a good credit record for the future.

- No big deposit needed. Guarantor mortgages can reduce or remove the need for a large deposit, making buying a home quicker and easier.

- Flexible choice of guarantor. Your guarantor doesn’t have to be a parent. It can be a relative, friend or anyone willing and financially able to take on the responsibility, as long as the lender approves them.

What Are the Risks Involved?

For the Borrower

The obvious risk is that if you persistently miss mortgage payments, you’ll likely lose your home.

On top of that, your credit record will be severely damaged.

For the Guarantor

Being a guarantor is a BIG commitment.

By agreeing, your guarantor is taking on FULL legal responsibility to make the repayments if you hit financial troubles.

Failure to do so means they risk:

- The forced sale of their property

- Damage to their own credit file

- Potential bankruptcy if insufficient funds to cover the debt

So while being a guarantor means helping out a loved one, it’s not a decision to be taken lightly. Thorough financial and legal checks are a must.

How Much Can I Borrow?

Like regular mortgages, guarantor mortgages depend on how much you earn and your expenses. Your guarantor’s finances also count.

This mix helps the lender decide how much money they can safely lend you.

Most guarantor mortgages let you borrow a lot of the property’s price. Often, you can get loans for up to 95% or even 100% of the home’s value.

This means you might not need a big deposit, or any deposit at all. Always talk to a mortgage expert to find the best option for you.

Where Can I Get a Guarantor Mortgage in the UK?

Although not as common as mainstream mortgages, there are still a number of high street banks, building societies and more specialist lenders that offer guarantor mortgage products across the UK, such as:

- Barclays

- Bath Building Society

- Buckinghamshire Building Society

- Cambridge Building Society

- Family Building Society

- Furness Building Society

- Hinckley & Rugby Building Society

- Leeds Building Society

- Loughborough Building Society

- Marsden Building Society

- Newbury Building Society

- Scottish Building Society

- Vernon Building Society

As with any mortgage, it’s wise to seek advice from an independent broker who can compare deals from the whole market to find the most suitable guarantor mortgage for your personal circumstances.

Can I Get a Guarantor Mortgage With Bad Credit?

Yes, it’s possible to get a guarantor mortgage with bad credit.

Having a guarantor with strong finances and valuable assets, like savings or property, significantly improves your application’s chances.

Remember, the final decision depends on your overall financial health and the guarantor’s ability to make payments if you default.

Are There Alternatives to Guarantor Mortgages?

If acting as a guarantor sounds too risky, there are alternatives that may suit your situation:

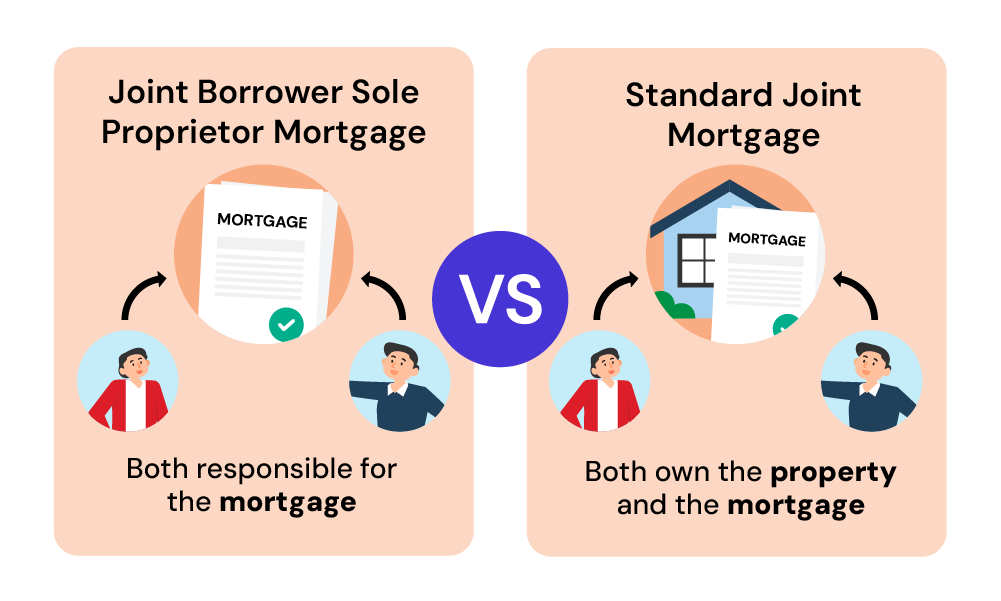

Joint Borrower Sole Proprietor Mortgage

With a joint borrower sole proprietor (JBSP) mortgage, your income is assessed alongside the joining applicant’s (e.g. parents) – but only you acquire ownership of the property.

Extra affordability from two incomes can increase the mortgage amount.

Standard Joint Mortgage

By jointly owning the property with another applicant like a partner or parent, you may be able to borrow more than applying alone.

Just bear in mind the co-owner will also be tied legally to the mortgage debt.

Other Family Mortgage Schemes

Some lenders offer family mortgage products like Barclays’ Family Springboard where a relative provides 10% of the property value as security for several years – after which it is released back to them.

The Bottom Line: Is a Guarantor Mortgage Right for Me?

There’s no one-size-fits-all answer.

These mortgages can be tricky and risky for both you and the guarantor. But done right, they can help you buy a home when you wouldn’t otherwise qualify.

If you really want to own a home but lack a big deposit or have bad credit, a guarantor could be your key.

The important thing is to be upfront about what’s involved for everyone and have a clear plan to get out of the guarantor agreement over time.

For many, a guarantor’s help is worth it to achieve their dream of homeownership. But guarantor mortgages are a big decision – talk to an independent mortgage advisor before going ahead.

Looking for the right broker? We can help – simply, reach out to us. We’ll connect you with a qualified mortgage advisor who can help you make the best decision for your mortgage.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Do guarantors get credit checked?

Lenders will credit check guarantors to make sure they can afford to cover the mortgage if needed.

This is usually a soft check that won’t hurt the guarantor’s credit score, but it helps the lender decide if they’re a good choice. A good credit score makes it more likely the mortgage will be approved.

Can guarantor mortgages help me borrow more?

Yes, guarantor mortgages can help you borrow more. With a guarantor backing you up, lenders might be happy for you to borrow more than with a normal mortgage.

In some cases, you could even get a 100% mortgage, so you wouldn’t need any upfront savings.

Can retired parents act as a guarantor mortgage?

Yes, retired parents can be guarantors if they have enough savings or own their home entirely.

However, consider their age as some lenders might be cautious if the guarantor is very old. Always check the specific requirements of the lender as these can vary.

What happens if my guarantor dies?

There are a few possibilities if your guarantor dies. You may need to find a new guarantor.

If you’ve made significant mortgage payments or your finances have improved, you might be able to remortgage without a guarantor.

Additionally, if you inherit money from the guarantor’s will, you could potentially use it to help pay off the mortgage.

Can a guarantor mortgage be used for buy-to-let properties?

Guarantor mortgages for buy-to-let properties aren’t as easy to find.

Most lenders will only offer them if the rent from the property is expected to comfortably cover the mortgage repayments. This makes the whole thing less risky for them.

What happens if a guarantor can no longer pay?

If your guarantor can’t pay, it’s usually because something unexpected hit their finances hard.

Your lender will discuss the next steps to you and your guarantor. They’ll try to find out why they can’t pay and might take legal action if they’re breaking the agreement.

But this is uncommon because lenders check guarantors carefully before approving the mortgage.

Can you stop being a guarantor?

You can sometimes get out of being a guarantor, but it depends.

Some lenders might let you off the hook if the borrower’s finances improve a lot, or if a big chunk of the mortgage has been paid off. The exact terms will vary though, so check with the lender first.

How do I get a guarantor mortgage?

There are two main ways to get a guarantor mortgage:

- Talk to lenders directly.

- Use an independent mortgage broker.

Most people go with a broker because they can find you the best deal from a wide range of lenders, considering both your situation and your guarantor’s.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Who Can Be A Guarantor For Your Mortgage?

Buying property can be challenging if you don’t have a long credit history or high income. Maybe you’re young and just starting out, new to the UK, or a freelancer whose income varies. Whatever your reasons–one thing is true: you’re struggling to secure a mortgage. In this case, a guarantor mortgage can help. But, what […]

How Much Can I Borrow With a Guarantor Mortgage?

Ever dreamed of owning your OWN home but your income just doesn’t seem to stretch far enough? A guarantor mortgage could be the solution that gets you on the property ladder. But how much can you actually borrow with this type of mortgage? Let’s take a look. 🔎 What’s a Guarantor Mortgage? A guarantor mortgage helps […]