- Can Freelancers Get Mortgages?

- How Do Lenders Assess Freelance Income?

- What Specific Documents do I need?

- How Much Can I Borrow as a Freelancer?

- How To Get Mortgages as a Freelancer?

- How Can I Increase My Chances of Approval?

- Which Lenders Are Open to Freelancers?

- How Does a SEISS Grant Affect My Application?

- The Bottom Line

A Guide To Getting A Mortgage As A Freelancer

The freedom and flexibility of freelance work are undeniably appealing. But when it comes to buying a home, the dream can suddenly hit a mortgage hurdle.

Can your freelance income unlock the door, or will lenders slam it shut?

The good news: freelancers can secure mortgages. However, the process might differ slightly compared to traditional employment.

That’s why this guide unpacks everything you need to know about mortgages for freelancers in the UK.

Can Freelancers Get Mortgages?

Yes, freelancers can absolutely get mortgages!

However, the process is typically stricter compared to salaried individuals.

This is because lenders require evidence of consistent income, and freelance income can fluctuate more than regular salaries.

The good news is that there are a growing number of lenders willing to consider freelancers, recognising the increase in self-employed work.

Still, thorough preparation and a well-structured application are crucial for success.

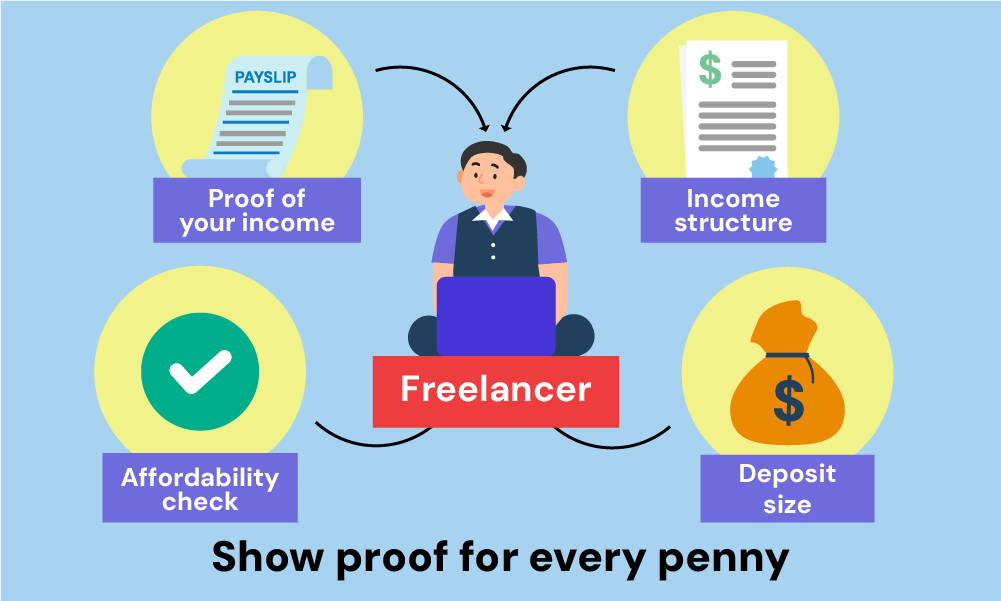

How Do Lenders Assess Freelance Income?

While salaried individuals have straightforward payslips, freelance income can be more complex.

Lenders want to see a clear picture of your income stability, so they typically ask for:

- Proof of your income. Typically, lenders will request 2-3 years of tax returns or business accounts (some might accept 1 year). This helps them understand your income flow.

- Income structure. Your income structure matters. As a sole trader, they’ll assess your net income. Limited company directors will need to show salary and dividends, while others might show project values or daily rates.

- Affordability check. Don’t worry, they don’t just look at your best year ever. Lenders usually average your income over a period to assess your borrowing capacity.

- Deposit size. A larger deposit shows financial stability and commitment. This can increase your approval chances and unlock better interest rates.

What Specific Documents do I need?

Gather these key pieces to smoothen the process:

- 2-3 years of tax returns or SA302 (some lenders may accept 1 year)

- 2-3 years of company accounts for limited companies. (some lenders may accept 1 year)

- 3-6 months of personal and business bank statements.

- Contracts outlining future work (if available).

- Copies of invoices or other documentation to prove income stability and consistent track record.

- Proof of identity and address such as passport, driving licence, utility bills

- Depending on your circumstances, you may also be required to provide additional documents, such as:

- A business plan

- Letters of recommendation from clients

- Proof of self-employment insurance

- Evidence of your deposit such as a bank statement or confirmation from your solicitor.

It is important to note that this is not an exhaustive list and the specific documents you will need may vary depending on your circumstances and the lender you choose.

It is always best to speak to a mortgage broker to get specific advice on what documents you will need to provide.

How Much Can I Borrow as a Freelancer?

Freelancers can generally borrow similar amounts to employed individuals, typically based on a multiple of their annual income.

This often ranges from 4 to 4.5 times your yearly earnings, but some lenders might even consider 5 to 6 times.

Here’s an example: Imagine your annual freelance income is £40,000. Using a 4.5 multiple, you could potentially borrow up to £180,000 (4.5 x £40,000). Remember, this is just an estimate, and the actual amount you can borrow will depend on various factors like:

To get a rough idea of how much you might be able to borrow, use a self-employed mortgage calculator online.

How To Get Mortgages as a Freelancer?

1. Sort Your Finances First

Before you dive into house hunting, make sure your finances are in tip-top shape.

Start by checking your credit score through agencies like Experian, Equifax, and TransUnion. A good score can make a big difference, so address any issues you find.

You can also take this time to boost your deposit. The more you save, the better. Aim for 20% or more of your home’s price. To increase your deposit, consider:

- Opening a high-interest savings account

- Taking on extra work for more income

- Cutting back on unnecessary spending

- Looking into a Lifetime ISA to get a 25% government boost on your savings

2. Get an Agreement in Principle (AIP)

An AIP tells you how much you might be able to borrow and can make you a more attractive buyer. It’s not a must, but it’s a smart move.

Just watch out for hard credit checks that might impact your credit score. An AIP typically lasts 30 to 90 days.

3. House Hunting Time

With your AIP in hand, start looking for your perfect home.

Stay within your budget and take your time. Once you find a place, make your offer through the estate agent.

4. Apply for Your Mortgage

If your offer is accepted, apply for your mortgage. You can go directly to a lender or use a mortgage broker to help compare deals.

You’ll need a property survey to assess the home’s value and condition. The whole process usually takes about 4-6 weeks.

5. Final Steps with a Solicitor

A solicitor or conveyancer will handle the legal aspects of your purchase. They’ll take care of things like the land registry and exchanging contracts.

Once everything’s signed, you’ll be ready to get the keys to your new home.

For freelancers, getting a mortgage might seem tricky, but with the right preparation and understanding, it’s definitely achievable.

If you’re feeling overwhelmed, consider speaking to a mortgage broker. They can guide you through the process, making it easier to secure a mortgage that suits your freelance income.

Note: Your home is at risk if you don’t keep up with mortgage repayments, so think carefully and plan.

How Can I Increase My Chances of Approval?

Here are some key steps to increase your chances of securing a mortgage as a freelancer:

- Save a large deposit. Aim for at least 25%, but ideally 30-40% of the property’s value. This demonstrates financial commitment and reduces the amount you need to borrow.

- Show a strong income track record. Provide consistent tax returns and income documentation for at least 3 years, showcasing your financial stability.

- Build a Good Credit Score. A strong credit score indicates responsible financial management and makes you a more attractive borrower to lenders.If your score isn’t where you’d like it, focus on paying bills on time, reducing your credit utilisation, and clearing any outstanding debts.

- Explain any employment gaps clearly. Be upfront about any periods without income and explain the reasons.

- Project future income. If you have signed contracts or future projects lined up, share them with lenders to demonstrate future income stability. This helps build confidence in your ability to repay the loan.

- Leverage guarantors. In some cases, having a guarantor with a strong financial history can increase your eligibility and potentially even improve your loan terms. This option should be carefully considered and discussed with both parties involved.

- Seek help from a specialist broker. A mortgage broker experienced with freelancers can guide you through the process, find lenders suited to your situation, and present your application effectively.

Which Lenders Are Open to Freelancers?

While there aren’t specific “freelancer mortgages,” many lenders consider self-employed individuals, but their requirements and acceptance criteria vary.

Here’s a breakdown:

- Mainstream Lenders. These often require stricter documentation, like 3 years of accounts.

- Examples include NatWest (2 years), Kent Reliance (3 years), and Stafford Railway Building Society (1 year if recent).

- Specialist Lenders. They might be more flexible, potentially accepting 1-2 years of accounts. Options like Norton Home Loans and Together might consider projections from your accountant in place of full historical data.

- Regional Building Societies. Some, like Loughborough Building Society, might be more open to specific professions and offer competitive rates tailored to them.

Note: Each lender has different criteria, so shop around and compare their requirements.

It’s important to not rely solely on online information. Talk to mortgage advisors with freelancer experience for personalised guidance.

How Does a SEISS Grant Affect My Application?

Not all lenders treat it the same.

Some see them as a testament to your business’s resilience, while others might not be so accommodating. Checking directly with lenders is essential to understand their stance on SEISS grants.

Regardless, a consistent income track record, both pre-and post-pandemic, can significantly boost your application, SEISS grant or not.

The Bottom Line

Securing a home as a freelancer is exciting, but the mortgage process can feel overwhelming. But, don’t worry.

Here’s the key: Preparation.

Freelance income can vary, and lenders need to assess your financial stability. Being organised and having your documents ready makes the process smoother.

If you need extra help with this, consider consulting a mortgage advisor experienced with freelancers. They understand your unique income situation and can guide you towards lenders more likely to approve your application.

Finding the right advisor can be easy, simply contact us today! We will arrange a free, no-obligation consultation with a dedicated freelance-mortgage advisor. They’ll guide you through the process, explain your options, and find the best fit for your situation.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Are mortgages for freelancers different from regular mortgages?

Technically, there aren’t specific “freelancer mortgages.” However, the application process and requirements can differ slightly compared to traditional employment due to the nature of freelance income. Freelancers typically need to demonstrate a strong and stable income history, often with more documentation than someone in a salaried position.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

A Guide to Using Bonuses and Commissions for a Mortgage

Are you finding it tough to get lenders to look at your full income? We know that bonuses and commissions can change, and this can make some lenders a bit wary. But, don’t worry – having a variable income doesn’t mean you can’t get a good deal on a mortgage. There are lenders out there […]

Umbrella Company Mortgages Explained

Struggling to buy a house while working for an umbrella company? You’re probably worried that your job setup will make getting a mortgage a bit trickier. Here’s some good news – securing a mortgage is totally doable for umbrella company workers. This quick guide will show you how to successfully ace your mortgage application. Let’s get […]

How To Get A Student Mortgage in the UK: A Guide

Being a student can make securing a mortgage challenging. Lenders are often cautious due to your limited credit history and fluctuating income. But, here is the deal – it’s not impossible. With the right guidance, you can get on the property ladder while being a full-time student. Curious, how? This article will show you how […]