- What Are Asset Based Mortgages?

- Am I Eligible for an Asset-Based Mortgage?

- What Assets Can Be Used as Mortgage Security?

- What Are Typical Loan-to-Values (LTVs)?

- How Much Can I Borrow Against My Assets?

- What Rates and Fees Apply?

- Can I Remortgage Onto an Asset-Based Loan?

- Combining Asset-Based and Income-Based Mortgages

- Is Asset-Based Lending Right For Me?

- Where Can I Get An Asset-Based Mortgage?

- Key Takeaways

- The Bottom Line

The Complete Guide To Asset Based Mortgages In the UK

Lenders often seem to miss the bigger picture when it comes to wealth.

You could have millions in property, shares, or investments, but if your income doesn’t tick their boxes, they might still turn you down for a mortgage.

That’s where asset-based mortgages come in. Instead of focusing on your income, these mortgages consider the value of your assets, giving you more borrowing options.

They’re designed to bridge the gap for people who have significant wealth but don’t fit the mould of traditional mortgage criteria.

In this guide, we’ll cover how these mortgages work, the types of assets you can use, and who they’re best for.

You’ll also learn how brokers can help you find deals that make the most of your financial situation.

What Are Asset Based Mortgages?

Asset-based mortgages, also called securities-backed mortgages, let you use your investments or savings as collateral for a loan.

This means you can borrow money based on the value of things like shares, cash deposits, or even gold instead of relying on income alone.

They’re a great option if your income isn’t straightforward. For example, maybe you’re a business owner with irregular earnings, retired, or paid in foreign currencies.

With this type of mortgage, lenders focus on what you own rather than how much you earn.

The best part? You don’t need to sell your investments to access funds.

Your portfolio stays intact, so it can keep growing, while you use your wealth to fund your property plans. It’s a smart way to make your money work harder for you.

Am I Eligible for an Asset-Based Mortgage?

Asset-based mortgages aren’t your typical home loan—they’re specially designed for high-net-worth individuals. According to the Financial Conduct Authority (FCA), you fit the bill if you have:

- An net annual income over £300,000, or

- Net assets worth over £3 million

But that’s not all. Lenders have their own criteria too, which often include:

- Being a UK resident

- Offering UK property as security

- Having a minimum asset portfolio value (usually £500,000 or more)

- Providing proof of your high-net-worth status

To keep things formal, lenders will likely ask for documents like an accountant’s certificate to confirm your income and assets.

What Assets Can Be Used as Mortgage Security?

Lenders are pretty flexible when it comes to the types of assets they’ll accept. Here’s a quick list of what’s usually eligible:

- Publicly traded stocks and shares

- Investment trust and fund portfolios

- Cash savings

- Physical gold or silver

- Fine art and collectibles

- Classic or prestige cars

- Cash value life insurance

- Luxury yachts or sports cars

Essentially, if your asset has good resale value, it might qualify.

As a general rule, the easier it is to sell the asset, the more you can borrow against it. For example, cash is considered super safe, so you’re likely to get the best loan-to-value (LTV) ratio for it.

On the other hand, non-liquid assets like property usually don’t make the cut for this type of mortgage.

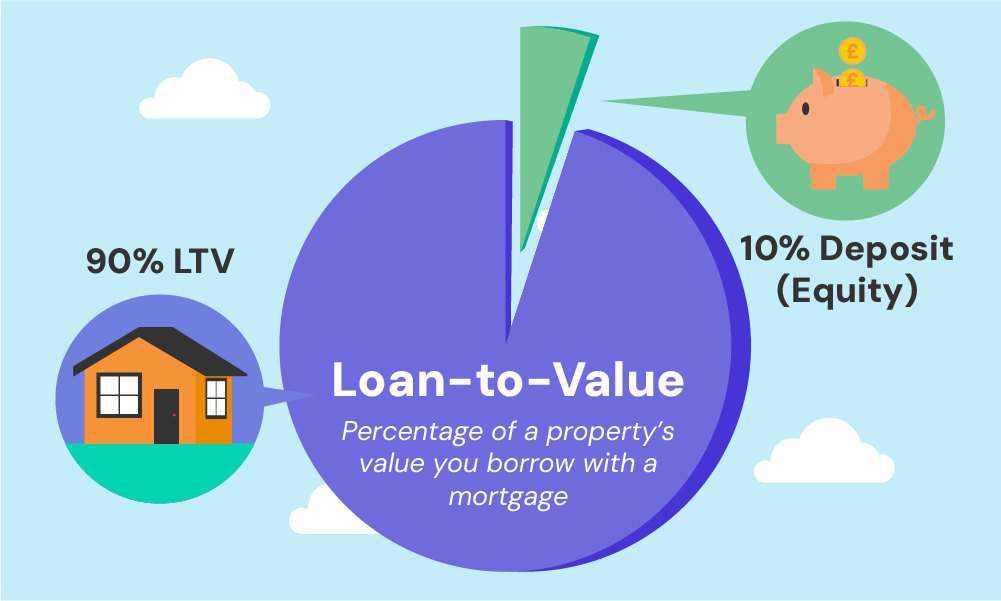

What Are Typical Loan-to-Values (LTVs)?

With an asset-based mortgage, you can usually borrow up to 50% of your portfolio’s value. But this isn’t set in stone—it depends on a few key factors:

- Your Portfolio. The lender will check out what’s in it and how risky those investments are. If your portfolio leans towards safer options, you could borrow more.

- Investment Performance. Lenders like to see a solid track record. If your investments have grown steadily, that’s a big plus.

- Lender’s Appetite for Risk. Some lenders play it safe and offer less, while others are more willing to take a gamble if they see potential.

- Market Conditions. The economy matters! When times are good, lenders tend to be more generous.

The type of assets in your portfolio also plays a big role. Safer investments like cash might let you borrow up to 80-90% of their value.

But if you’re holding riskier assets, like stocks, lenders might cap it at 25-30% to play it safe.

Each deal is personalised. If you have a strong, diverse portfolio, some lenders might even stretch the limits for you. It’s all about finding the right fit.

To calculate your LTV, use the loan-to-value ratio calculator.

If this feels like a lot to figure out, don’t worry. A broker can help you make sense of it all and find the best deal for your situation.

How Much Can I Borrow Against My Assets?

There’s no set maximum for how much you can borrow.

If you’ve got substantial wealth, lenders might offer loans worth millions. It all boils down to how comfortable they are with your portfolio and financial situation.

That said, most lenders start at a minimum loan amount. Traditional asset-based lenders often begin at around £100,000, while specialist ones may have a higher starting point, typically £500,000 or more.

The actual amount you can borrow depends on three things:

- The value of your assets.

- How much the lender is willing to lend against them (your LTV).

- The level of risk the lender is happy to take.

Since these details can get a bit complicated, having a knowledgeable broker on your side makes a big difference.

They’ll help you navigate the options and find a loan that works perfectly for you.

What Rates and Fees Apply?

When it comes to asset-based lending, interest rates aren’t set in stone. They’re tailored to you, based on your assets, financial history, and credit score.

The good news? Because your assets act as security, the rates are often more competitive than a standard mortgage.

If your loan is backed by something like stocks, you’ll typically see interest rates around 2-4% per year.

Got cash as your security? Even better—you might score a rate below 1%. But let’s not forget the fees.

Most lenders charge an arrangement fee, usually 1-2% of the loan amount. This covers the work they do, like getting independent valuations of your assets and putting your loan together.

Can I Remortgage Onto an Asset-Based Loan?

Yes, you can.

Asset-based mortgages usually have a one-year term, which can be renewed annually. But if you want to make changes, remortgaging could be the way to go.

For example, if the value of your mortgaged assets has increased, you might borrow more against their new, higher value.

Or, if your financial situation has changed, you might switch to a standard mortgage based on income.

To get the best deal, it’s smart to work with a specialist broker. They’ll help you handle your options and find a mortgage package that fits your unique needs perfectly.

Combining Asset-Based and Income-Based Mortgages

If you have both an income and valuable assets, some lenders let you combine them to get the best of both worlds.

This can be handy if your income isn’t enough for the mortgage you want, or if you’d rather not tie up all your assets in one go.

Here’s how it works: the lender considers part of your assets alongside your income when deciding how much you can borrow. This gives you a bit more flexibility without risking everything you own.

Already have an asset-based mortgage? No worries. You can refinance to switch to a combined option if that suits you better.

The key is to find the right mix for your situation, so your finances work smoothly together.

Is Asset-Based Lending Right For Me?

Asset-based lending can be a helpful option if you want to borrow money without relying on your income. But before jumping in, it’s good to weigh the pros and cons:

Pros:

- Borrow More Money. You can often borrow more than with a standard mortgage because it’s not just based on your income.

- Lower Interest Rates. These loans sometimes have better rates than traditional mortgages.

- Keep Your Investments. You don’t have to sell your assets to access funds.

- Quick Approvals. Decisions can be faster than with regular banks.

Cons:

- Risk of Value Drops. If your assets lose value, it could cause problems.

- Margin Calls. If values drop too much, the lender might ask for more security or repayment sooner than planned.

- Less Protection. These loans don’t have as much consumer protection as standard mortgages.

- Repayment Risks. If you struggle to pay back the loan, your options might be limited.

In simple terms, asset-based lending can give you more flexibility and borrowing power, but it comes with risks like changes in asset value and less regulation.

It’s about finding the right fit for your finances and deciding if you’re okay with the risks involved.

Where Can I Get An Asset-Based Mortgage?

In the UK, when you’re looking into asset-based mortgages, you’ll usually find them through private lenders.

These lenders aren’t typically out in the open for everyone. To get in touch with them, you generally need a broker’s help.

Private lenders are pretty useful for folks who have a fair bit of money. They have more room to manoeuvre compared to your standard banks, especially for those with higher net worth.

This means they can sometimes offer bigger loans and tailor their deals to fit specific needs.

It’s not common to approach these private lenders directly. If you do find one, going straight to them might not be your best bet.

There’s a chance they might talk to you, but you could end up missing out on a better deal somewhere else. That’s where having a broker can be handy. They know a lot of these private lenders and understand how they work.

A broker can shop around for you, comparing different lenders to see who offers what. This way, you get a clearer view of your options and can make a more informed decision.

Key Takeaways

- Asset-based mortgages let you borrow money using things you own—like stocks, cash, or even gold—rather than just relying on your paycheck. They’re perfect if you have big savings or investments, especially if you’re worth over £3 million or earn more than £300,000 a year.

- Lenders accept a range of assets, including stocks, savings, fine art, or even luxury cars. Assets that are easier to sell, like cash, usually let you borrow more.

- The amount you can borrow depends on your assets’ value, the lender’s rules, and how risky your portfolio is. Loan-to-values typically range from 25-90%.

- Interest rates can be super low—sometimes below 1% for cash-backed loans—but lenders often charge arrangement fees of 1-2%.

- You can mix asset-based and income-based mortgages for more flexibility, combining your earnings and assets to borrow what you need.

The Bottom Line

If you’re well-off but don’t fit the usual income box for a standard mortgage, asset-based lending can be a smart choice.

It’s a way to get the money you need for property, using assets you already have and want to keep.

But here’s a key point: working with a broker can make a big difference. They know the ins and outs of this type of lending.

They can find deals you might not get on your own and guide you through the process, making sure everything’s tailored to suit you.

If this sounds like it could work for you, get in touch. We’ll arrange a free, quick chat with a broker, with no obligation. They’re here to help you figure out if asset-based lending is the right move for you.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

How long does it take to pay an asset based mortgage?

The repayment period for an asset-based mortgage can vary significantly, depending on the specific terms agreed upon with the lender.

Generally, in the UK, most asset-based mortgages are structured with an initial one-year term, which can be renewed annually. This flexible structure allows borrowers to adapt their repayment schedule to suit their financial situation.

Related Articles

Private Mortgage Lenders Explained

You didn’t get where you are by settling for ordinary, so why start now? Regular mortgages might work for most people, but when you’re dealing with serious wealth, they just don’t measure up. Private mortgages, on the other hand, are in a league of their own. Whether it’s a stunning countryside estate, a sleek London […]

Securing High Net Worth Mortgage In The UK

If you’re wealthy, regular mortgages probably don’t work for you. You need something designed to match your lifestyle and financial goals. The good news? With the right mortgage advisor, buying a high-value property or using your assets for smart investments can be simple. This guide breaks down high-net-worth mortgages in 2025, so you can see […]

Can You Get a £6 Million Mortgage or More in the UK?

Dreaming of owning a jaw-dropping luxury home? Let’s talk about big money. Most homes in the UK cost under a million pounds, but luxury properties are in a league of their own—we’re talking mansions and one-of-a-kind homes with price tags in the millions. If you’re aiming for a house like this, you’ll likely need a […]