- How Much Can I Borrow with £3,000 a Month?

- Does the Mortgage Term Affect How Much You Can Borrow?

- What Else Affects How Much You Can Borrow?

- How Job Status Affect Mortgage Application

- Can I Afford a £3,000 Mortgage with a lower income?

- What Proof of Income Do Lenders Require?

- What Loan-to-Value Ratio Can I Get with £3,000 a Month?

- Other Costs to Think About

- How Mortgage Brokers Can Help You

- Key Takeaways

- The Bottom Line

How Much Mortgage Can You Get with £3,000 a Month?

Investing £3,000 a month in your mortgage is a bold move—and one that can open doors to your dream home.

Whether it’s thanks to a recent pay rise, a desire to live in a prime location, or a goal to pay off your mortgage faster, it’s a commitment that can really pay off.

But how much can you actually borrow with a £3,000 monthly payment? 🤔

This guide explains the numbers, showing you exactly what your £3,000 a month can unlock in the property market.

How Much Can I Borrow with £3,000 a Month?

The amount you can borrow depends on a few things:

- How much you earn,

- How long you want the mortgage to last, and

- The interest rate you get

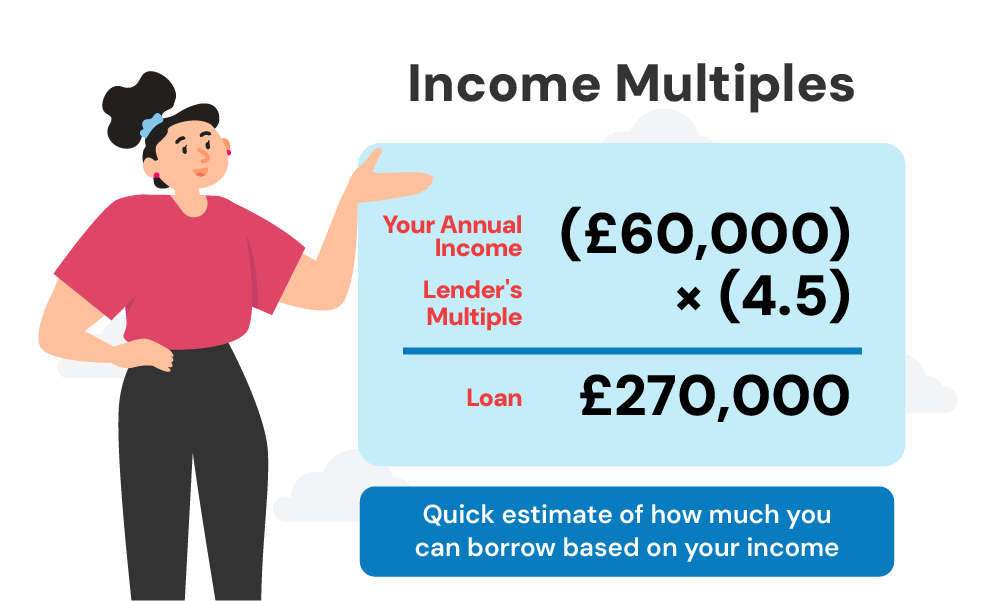

Lenders often use a simple rule of thumb: they multiply your yearly income by a number between 4.5 and 6.

This gives you a rough idea of how much you could borrow.

For example, if you earn £90,000 a year, you might be able to borrow between £405,000 and £540,000.

But remember, this is just a starting point.

- With a 25-year mortgage at 4% interest, a £3,000 monthly payment could get you a mortgage of around £568,400.

- If the interest rate goes up to 5%, you might only be able to borrow about £513,200.

As you can see, even a small change in the interest rate can affect how much you can borrow.

That’s why it’s important to shop around for the best mortgage deal.

Want to find out exactly how much you could borrow? Use a mortgage calculator online or speak to a mortgage advisor.

Does the Mortgage Term Affect How Much You Can Borrow?

Yes, the mortgage term has a big impact on how much mortgage you can get.

A longer mortgage term, such as 30 years, will lower your monthly payments, allowing you to borrow more money.

But, this also means you’ll pay more in interest over the life of the loan.

For example:

- With a 30-year mortgage at 4% interest, you might be able to borrow around £628,500 if you can afford £3,000 a month.

- But if you shorten it to a 20-year mortgage with the same payments and interest rate, you might only be able to borrow about £495,000.

A longer mortgage means you can borrow more now, but you’ll pay more in the long run.

A shorter mortgage means you’ll pay less overall, but you’ll need to find a bigger deposit or afford higher monthly payments.

What Else Affects How Much You Can Borrow?

It’s not just your income and how long you want your mortgage to last that matters.

Lenders look at your whole financial picture.

This includes your spending, debts, and how you’ve handled money in the past.

Your spending and debts

Lenders want to see how much money you have left after paying your bills each month.

If you have a lot of debt or high bills, you might be able to borrow less.

This is because lenders want to make sure you can afford your mortgage on top of everything else.

Credit History

How well you’ve handled money in the past can make a big difference to your mortgage.

Lenders look closely at your credit score.

A good credit score shows you’re good with money, which can help you get a better interest rate and borrow more.

But if your credit score isn’t great, you might end up paying more interest or finding it harder to borrow.

Deposit Size

How much you can put down as a deposit also affects your mortgage.

The more you can save up, the better.

A bigger deposit means you need to borrow less, which can help you get a better mortgage deal.

Most lenders want you to put down at least 5-10% of the property’s price, but saving more can give you more choice and possibly a lower interest rate.

Age

Younger people often get offered longer mortgage terms, meaning lower monthly payments and the chance to borrow more.

As you get older, your options might be shorter terms, which could mean borrowing less.

Lenders also think about how close you are to retirement when deciding how much you can borrow.

Property Type

Some homes, like old buildings or flats above shops, can be trickier to get a mortgage for.

Lenders might see these as riskier, so you might need a bigger deposit or find it harder to borrow as much.

Profession

If you have a steady job, especially in a stable industry, lenders are usually happier.

But if you’re self-employed or your income isn’t regular, it can be harder to borrow. You might need to show more proof of your earnings.

Dependents

Having kids can also affect things. Lenders know that looking after children costs money. This means you might have less money left over for your mortgage.

Debt-to-income (DTI) ratio

Your debt-to-income ratio shows how much of your money goes towards paying off debt. Lenders like to see if you can handle more debt, like a mortgage.

Most lenders want to see that less than 36% of your income goes on debt, and less than 28% on housing costs.

If you owe a lot compared to what you earn, you might find it harder to borrow.

Want to see where you stand? Try our debt-to-income ratio calculator.

How Job Status Affect Mortgage Application

Your job plays a big part in whether you can get a mortgage. Lenders like it when you have a steady job with a regular paycheque.

If you’re employed and get paid through PAYE, things are usually simpler.

But if you’re self-employed, lenders will want to see your accounts or tax returns for the past two years to check your income.

Even if you earn a good amount, if your income isn’t regular or easy to prove, it might be harder to borrow what you want.

Can I Afford a £3,000 Mortgage with a lower income?

It might be tricky to get a mortgage for £3,000 a month if your income is on the lower side.

But don’t worry, there are a few things you could try:

- Spread it out – You could choose a longer mortgage term. This means your monthly payments will be smaller, but you’ll pay more interest overall.

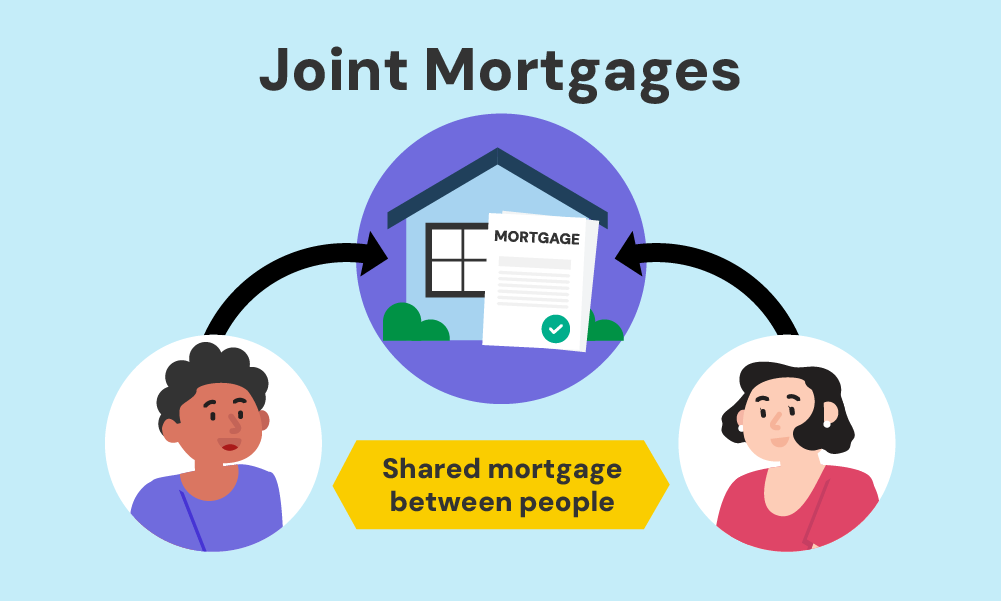

- Team up – Getting a joint mortgage with someone else could help. You’d combine your incomes, which might mean you can borrow more. Just remember, you’re both responsible for the mortgage.

It’s a good idea to talk to a mortgage advisor to see what your options are.

What Proof of Income Do Lenders Require?

Lenders need to see proof that you can afford a mortgage. Here’s what they usually ask for:

- P60 or contract: This shows how much you earn and that you have a job.

- Payslips: You’ll need to show the last few months’ pay to prove your income.

- Bank statements: These show how you spend your money and if you can manage a mortgage.

- ID: You’ll need a passport or driving licence to prove who you are.

If you’re self-employed, you’ll need to show more things like your tax returns and business accounts.

What Loan-to-Value Ratio Can I Get with £3,000 a Month?

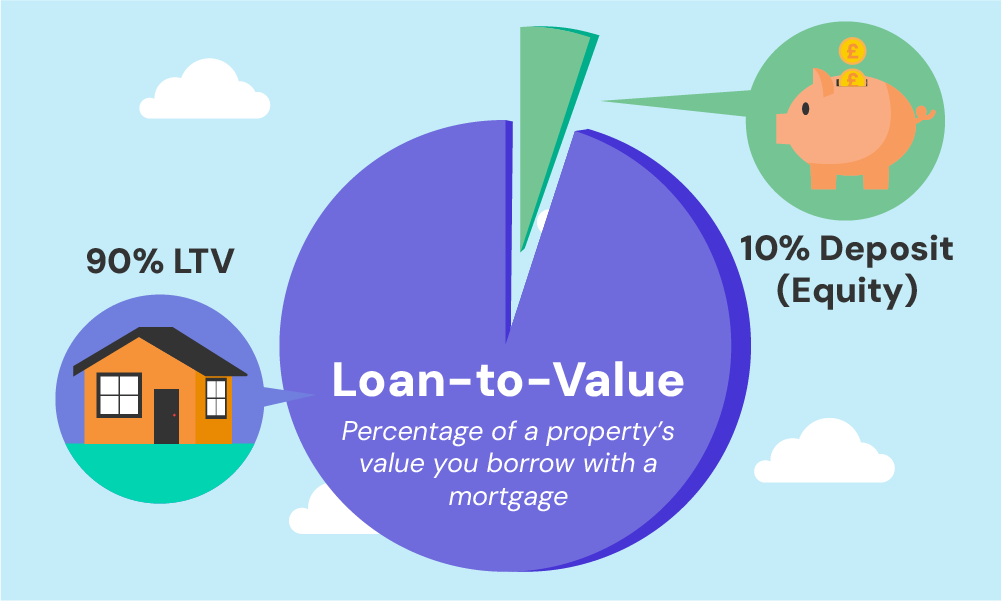

Your Loan-to-Value (LTV) ratio is basically how much you borrow compared to the house price.

For example, if you want to buy a £500,000 house and you have a £50,000 deposit, you’re borrowing £450,000.

That’s 90% LTV.

The lower your LTV, the better. Most lenders want you to put down at least 5-10% of the house price.

If you can save more, you’ll get a better deal on your mortgage, often with a lower interest rate.

But remember, things like your age or credit score can affect how much you need to save.

If you’re seen as a bigger risk, you might need a bigger deposit.

Other Costs to Think About

It’s easy to focus just on your monthly mortgage payment when you’re buying a home, but there are other costs you need to think about.

These can add up quickly, so it’s important to plan ahead.

- Arrangement fees – This is a charge from the lender to set up your mortgage. It can be anything from £0 to £1,499. You can usually add it to your mortgage, but this will mean paying more interest in the long run.

- Valuation fee – The lender will want to check if the house is worth what you’re paying. This usually costs around £300, but can be more for expensive homes.

- Legal fees – You’ll need a solicitor to handle the paperwork. This typically costs between £800 and £1,500, depending on how complicated things are. This covers things like checking the property and registering the ownership.

- Stamp Duty – This is a tax you pay to the government when you buy a property. How much you pay depends on the price of the house and if you’ve owned a home before.

- Survey – You might want to get a survey done to check the house is in good condition. This can cost a few hundred pounds.

- Insurance – You’ll need buildings insurance to protect the house. You might also want contents insurance for your belongings and life insurance to protect your family if something happens to you.

- Removal Costs – Getting your stuff from one place to another can cost money. Hiring a removal company can be anything from £300 to over £1,500, depending on how much you’re moving and how far you’re going.

- Mortgage broker – If you use someone to help you find a mortgage, they might charge a fee. This can be a fixed amount or a percentage of your mortgage.

It’s important to think about these costs when you’re working out how much you can afford.

How Mortgage Brokers Can Help You

Finding the right mortgage can be a real headache.

There are so many options out there, and it’s hard to know where to start, especially if you’re trying to stick to a £3,000 monthly payment.

That’s where a good mortgage broker can be a lifesaver.

A good broker is like your personal mortgage expert.

They’ll look at your finances and find the best mortgage deal for you. They know about all the different options, even ones you might not have heard of.

The best part?

Good brokers can do a lot of the hard work. They’ll sort through all the paperwork and deal with the lenders, saving you time and stress.

Key Takeaways

- With a £3,000 monthly budget, you could borrow around £568,400 with a 25-year mortgage at 4% interest, though higher rates reduce this amount.

- Lenders assess your income, debts, spending, credit history, deposit size, job status, and dependents to determine how much you can borrow.

- Factor in extra costs like arrangement fees, valuation fees, legal fees, Stamp Duty, surveys, insurance, removal costs, and broker fees.

- Save a larger deposit to lower your Loan-to-Value (LTV) ratio and secure better mortgage terms.

- If your income is low, extend the mortgage term or consider a joint mortgage to boost your borrowing capacity.

The Bottom Line

A £3,000 monthly mortgage can bring you closer to your dream home. But it’s important to understand all the things that affect how much you can borrow.

From your income and how long you want the mortgage to last, to interest rates and extra costs, there’s a lot to think about.

Getting expert advice is really helpful, especially if you’re struggling after a house valuation or aren’t sure what to do next.

A good mortgage advisor can find you the best deal.

Want to save time and stress? Get in touch with us. We can connect you with a trusted mortgage advisor who can help you find the perfect mortgage.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I get a buy-to-let mortgage for £3,000 a month?

Yes, you can, but buy-to-let mortgages are usually interest-only and based on rental income rather than your personal income. Lenders typically require rental income to be 125%-145% of the monthly mortgage payment.

What happens if interest rates rise?

If you’re on a fixed-rate mortgage, your payments won’t change until the fixed period ends. If you’re on a variable-rate mortgage, your payments could increase if interest rates rise.

Related Articles

Getting a Mortgage with Student Loans: What to Know

As someone looking to get on the property ladder, you already know how important it is to have your finances in order. For many, student loans are a big part of that picture, especially when the average student debt for recent graduates in the UK is £45,600. While it may sound like a lot, student […]

Does Overdrafts Affect Your Mortgage Application?

When you’re on the path to homeownership, every financial detail matters. From saving for a deposit to ensuring your credit score is in top shape, the journey is full of hurdles. But what about that overdraft you’ve been dipping into? Can it really affect your mortgage application? Let’s break it down. Can an Overdraft Impact […]

Does Renting Affect Your Mortgage Application?

In today’s housing market, many people find themselves renting for longer periods before making the leap to homeownership. But what happens when your renting history includes missed payments? Can these rent arrears affect your ability to get a mortgage? This article delves into how rent arrears could influence your mortgage application and what you can […]