A Definitive Guide To Home Buying and Mortgage Process

Buying a house in the UK is a brilliant idea, but let’s not sugarcoat it—the process can be a bit stressful 😰.

You might worry about what could go wrong and wonder what you should do at each stage.

The good news is, you don’t have to face it alone.

This guide is here to simplify the process. We’ll take you through each stage, ensuring you’re prepared and confident every step of the way.

How To Buy a House in the UK? Step-by-Step

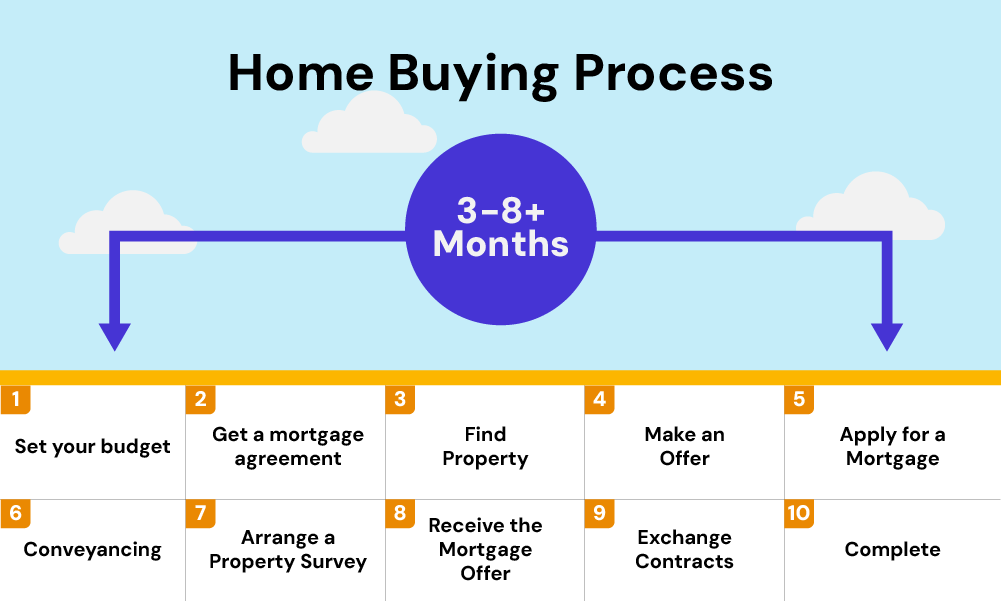

Here’s a quick overview of what you need to do:

- Set your budget to know how much you can afford

- Get a Mortgage Agreement in Principle (AIP).

- Start house hunting and visit properties that match your criteria.

- Make an offer through the estate agent, considering your budget.

- Apply for a mortgage once your offer is accepted.

- Instruct a solicitor or conveyancer for legal work and property searches.

- Arrange a property survey and allow the lender to carry out their valuation.

- Get a formal mortgage offer from your lender.

- Exchange contracts, pay your deposit, and arrange building insurance.

- Complete the purchase, register the property, and move in.

We’ve laid it all out below, so you’ll feel like a home-buying expert in the UK. 😎

Ready?

1. Set Your Budget (1-2 Days)

Before you start house hunting, it’s important to know how much you can afford.

Use a mortgage affordability calculator to estimate the biggest mortgage you could get based on your income and expenses.

This stops you from falling in love with a home you can’t afford.

Work out how much you can save for a deposit and set aside money for upfront costs like legal fees, Stamp Duty, and moving expenses.

To estimate your Stamp Duty costs, use our Stamp Duty tax calculator. This ensures you’re prepared and won’t face any surprises later.

Also, check your credit report for any errors before applying for a mortgage—lenders will be looking at it, so make sure your financial profile is in good shape.

To boost your chances of getting your dream home, consider getting an Agreement in Principle (AIP).

This tells sellers and estate agents you’re serious about buying and have the money to do it.

That brings us to step 2 – get an AIP.

2. Get a Mortgage Agreement in Principle (AIP) (1-3 Days)

Many home buyers ask this question “Do I really need an AIP?”

The short answer is YES. And here’s why:

An Agreement in Principle (AIP), sometimes called a ‘decision in principle’ or a ‘mortgage in principle’, is a quick and easy way to find out how much you could borrow.

It’s like a mini-application where the lender checks your information and credit file.

Having a MIP gives you a big advantage when making an offer on a house. It shows sellers you’re serious and can afford the property, which is great in a competitive market.

Remember, an AIP isn’t a guaranteed mortgage.

The lender could change their mind if they don’t like the property, if you don’t provide the right documents, or if they find something wrong with your application.

3. Find the Right Home (1-3 Months)

Once you know what you can afford and have an AIP in hand, it’s time to find your dream home. 🏠

This part can be fun, but it can also be tricky. Because it’s not just about finding the house you like.

You also need to think about – location, property type and condition, future resale value, and the community’s overall appeal.

Take your time and do lots of research. Explore different areas, visit lots of homes, and think about what’s important to you, like how close it is to work, schools, and transport.

Spend time walking around different neighbourhoods at different times of the day to get a feel for the place. Check how long other homes in the area take to sell.

If they sell quickly, it’s probably a popular spot. If they take ages, there might be reasons why.

Don’t hesitate to ask the seller or estate agent about any fixtures and fittings included with the property, like kitchen appliances or light fixtures.

Getting these details in writing can prevent surprises later.

Also, ask about any planned developments nearby, as these could impact your quality of life or the property’s future value.

Finally, trust your gut. If something feels off, dig deeper or move on.

Your home is a big investment, so choose wisely.

4. Make a Good Offer (A Few Days)

Deciding how much to offer on a property can be stressful. You don’t want to overpay, but you also don’t want to lose out to another buyer.

A good starting point is to compare the asking price with similar properties in the area. Also, consider the condition of the property and whether any repairs or updates will be needed.

It’s often helpful to get advice from forums or other buyers who have been through the process. They can offer insights and help you avoid common pitfalls.

Remember not to spend more than you can afford. Consider all the additional costs, like legal fees and Stamp Duty, so you don’t overextend yourself.

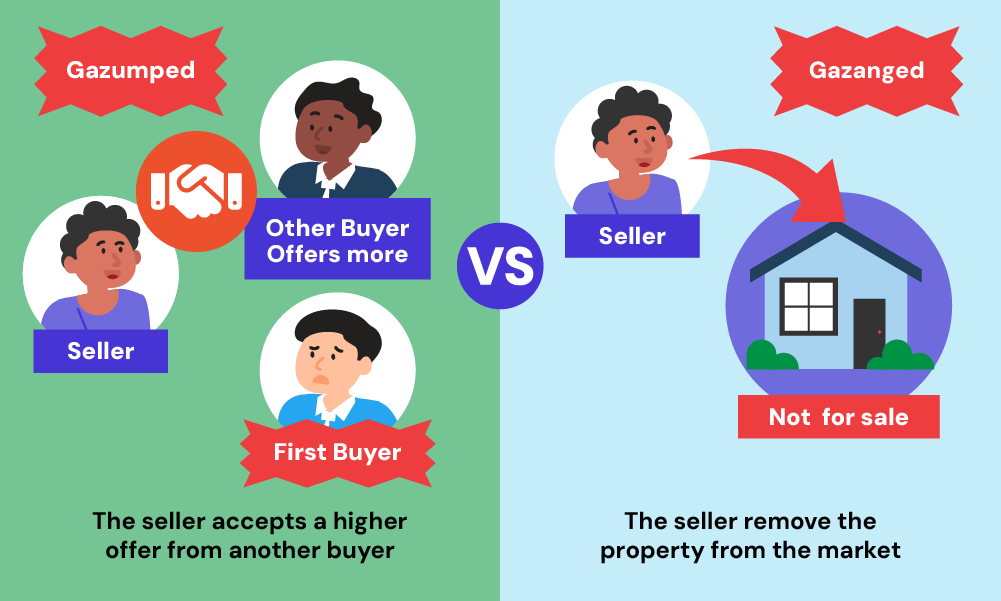

Just remember that, until contracts are exchanged, there’s always a risk of being gazumped (when another buyer offers more and the seller accepts their offer instead) or gazanged (when the seller decides to take the property off the market).

5. Apply for a Mortgage (2-6 Weeks)

If your offer is accepted, congratulations! 🎉

But don’t get too carried away just yet—there’s still a lot to do before you can call the place your own.

First, check if your AIP has expired (they’re usually valid for 30-90 days), you may need to reapply.

If you didn’t get an AIP initially, you can apply directly for a full mortgage.

Consider using a whole-of-market mortgage broker to make the process smoother and quicker.

A good broker can compare deals, handle the application, and guide you through each step, increasing your chances of approval.

They can help you find the best lenders and deals for your situation. They can also provide personalised mortgage illustrations detailing the key features of your mortgage.

Once you’ve applied, it can take a few weeks to over a month to get a formal offer, as the lender checks that both you and the property meet their criteria.

Be patient during this stage, as the process can take time. ⏰

Remember, don’t just rely on your bank—shop around to find the best deal, as interest rates and mortgage products can change daily.

6. Instruct a Solicitor for Legal Work & Property Searches (6-12 Weeks)

Conveyancing is the legal process of transferring a property’s ownership from the seller to you. You’ll need a licensed conveyancer or solicitor to handle this.

They’ll check the property’s history, identify any legal issues, and generally ensure everything’s in order.

Here are tips when it comes to choosing a solicitor:

- Get Multiple Quotes – Don’t automatically use the estate agent’s conveyancer. Get quotes from several firms and ask friends or family for recommendations.

- Consider Online Options – You don’t need a local solicitor. Online conveyancers can be efficient and often cheaper.

- Check Lender’s Panel – Choose a solicitor on your mortgage lender’s panel to avoid delays.

- Review Fees Carefully – Check the solicitor’s fees for hidden extras like bank transfers, Stamp Duty forms, and Land Registry fees.

- Ensure Regulation – Always check if your solicitor is regulated by the Law Society or the Council for Licensed Conveyancers. This gives you protection if something goes wrong.

- Stay in Contact – Conveyancing can be slow, so stay in touch with your solicitor. If there are delays, chase them up. Make sure they’re available, especially around important dates.

- Look for Added Value – Some solicitors offer free will as part of their service.

Once you’ve chosen a solicitor, they will start property searches while your mortgage application is reviewed.

These searches include local authority checks for building control issues, drainage, and environmental concerns. This helps avoid unexpected problems with your new property.

These searches are typically part of a ‘search pack’ costing £150 to £300. Budget for this early in the process.

7. Arrange a Property Survey (1-2 Weeks)

A survey reveals a property’s condition, uncovering problems hidden from view during viewings.

Even perfect-looking properties can have hidden defects like structural issues, damp, or faulty electrics. A survey provides peace of mind and can save you money.

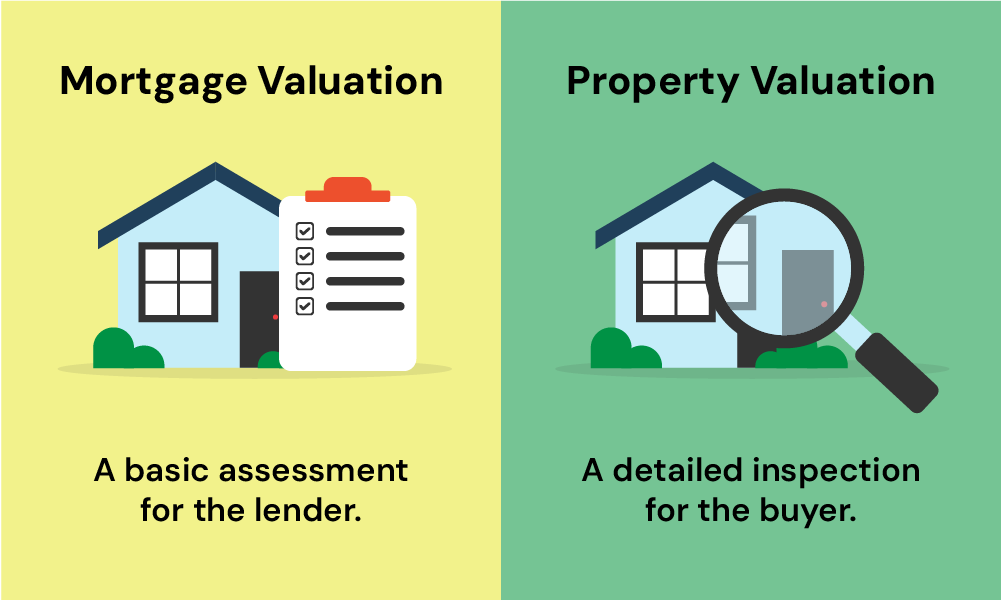

Remember: A mortgage valuation is not a property survey. The lender uses a valuation to check the property’s worth, not its condition.

It won’t highlight potential problems. Relying solely on the valuation could leave you with unexpected costs later.

Here are the types of surveys you can choose from:

- Homebuyers Report – This is suitable for conventional properties in reasonable condition. Highlights major issues and provides a general overview. Costs around £500 to £1,000. You can sometimes arrange this with your mortgage lender.

- Full Structural Survey (Building Survey) – Ideal for older or unusual properties. Offers a detailed assessment of the property’s structure and condition. It costs up to £1,500 but can help you negotiate the price if you find serious problems.

- Snagging Survey – For new-build homes. Identifies defects or unfinished work. Costs around £400 to £600. You can also use an online snagging list to check for problems yourself.

How to Arrange a Survey?

Ask your solicitor or estate agent for surveyor recommendations. Alternatively, search for accredited surveyors through organisations like the Royal Institution of Chartered Surveyors (RICS).

Book your survey early to allow time for review before exchanging contracts.

Using the survey findings helps with negotiating with the seller. This might involve requesting repairs or negotiating a lower price.

The survey helps you decide whether to proceed with the purchase, request changes or withdraw your offer.

8. The Mortgage Offer (2-20 Days)

Receiving a formal mortgage offer is a big step in buying a home. It means the lender will give you the money to buy your chosen property.

However, before celebrating, carefully check the offer.

Compare the mortgage offer to the mortgage illustration you got earlier. Make sure all the details match, like the loan amount, interest rate, and repayment terms.

Also, double-check your personal information and all the numbers are correct. Even small mistakes can cause delays or the offer to be withdrawn.

Pay close attention to the conditions in the mortgage offer. You must meet these conditions before the lender gives you the money.

Work closely with your solicitor to make sure everything is okay. If you find any mistakes or problems, contact your mortgage broker or lender straight away.

By checking everything carefully now, you’ll avoid problems later and have a smoother home buying process.

9. Exchange of Contracts (1-2 Weeks)

Once your solicitor confirms that all mortgage conditions are met and legal checks complete, you’re ready to exchange contracts.

This is a crucial step because it LEGALLY binds both you and the seller to the property purchase. Backing out after this point carries significant financial risk.

Before exchanging contracts, arrange building insurance for your new home.

While this may seem premature, it’s essential.

Once contracts are exchanged, you become responsible for the property, and insurance protects you against potential damage.

Your solicitors will agree on a date and time for the exchange, typically via a phone call.

Both solicitors review the contracts to ensure they match before confirming the exchange. You’ll then pay a deposit, usually 10% of the purchase price, to the seller’s solicitor.

After the exchange, your solicitor conducts final checks to verify the seller’s ownership and that no new issues have arisen.

They also prepare the transfer deed, the legal document transferring ownership to you. You’ll need to sign this deed.

With contracts exchanged, you’re in the final stages.

The completion date, agreed upon during the exchange, is when you pay the remaining balance and receive your keys. 🔑

What Happens Before Completion?

Your solicitor will give you a completion statement detailing all the money you owe, including the purchase price, stamp duty, and fees.

They’ll also check if the seller still owns the property and if there are no new financial problems.

10. Completion Stage (Instantly to 4 Weeks)

Completion is when you officially take ownership of the property and get the keys to your new home.

On the agreed completion date, your solicitor will transfer the remaining funds to the seller’s solicitor.

If you’re using a mortgage, your lender will release the funds to your solicitor to complete the payment.

This includes paying off the seller’s existing mortgage, if needed, and transferring the title deeds to you or your mortgage lender.

Once all payments are confirmed, the property is legally yours, and you can collect the keys and move in.

Since you’ll receive the keys on the same day, it’s a good idea to plan your moving arrangements in advance for a smooth transition.

Payment of Stamp Duty

Your solicitor will handle the payment of stamp duty on your behalf. This must be paid to HM Revenue & Customs (HMRC) within 14 days of completion.

Your solicitor will ensure it’s done on time and will include the amount in the completion statement they give you.

What Happens After Completion? Move In 🎉

There are a few final steps after completion.

Your solicitor will get the title deeds from the Land Registry, proving you own the property. This costs around £250-£500.

If you have a mortgage, your lender will keep these deeds. Otherwise, your solicitor can hold them for you.

Now that you’re a homeowner, it’s time to settle into your new home.

You’ll need to arrange for utilities, update your address with all relevant parties, and start making any changes or improvements you’ve planned.

And, of course, you’ll begin your mortgage repayments, which is a long-term commitment that comes with homeownership.

How Long Does the Homebuying Process Take?

Buying a house can take time.

It depends on factors like the house itself, the seller’s situation, and how quickly your mortgage and solicitor work.

On average, it can take anywhere from 3 to 8+ months. But be prepared – it could be longer. Just stay patient!

Key Takeaways

- Know what you can afford. Use online tools to see how much you can borrow. Start saving for your deposit and work on improving your credit score. It’s a good idea to get a mortgage in principle (AIP) to show sellers you’re serious.

- Find your dream home. Do your research, visit houses, and imagine your life there. Consider the location, the house itself, and the neighbourhood. Trust your gut, and make sure to get everything in writing.

- Make an offer. Decide how much to offer based on the house’s condition and what other homes are selling for. Be careful not to get outbid or have the seller change their mind.

- Secure your mortgage. Apply for a mortgage (or reapply if your AIP has expired). A mortgage broker can help you find the best deal. Be patient, as getting approved takes time.

- Get legal help. Find a solicitor or conveyancer to handle the legal side of things. Keep in touch with them and be ready to pay for property searches.

- Check the house out. Get a survey to spot any problems with the house. Use what you find to negotiate the price.

- Finalise your mortgage. Carefully read your mortgage offer and make sure everything is correct.

- Exchange contracts and move in. Once you exchange contracts, the sale is official. Get home insurance and get ready for completion day – that’s when you get the keys!

The Bottom Line: What To Keep in Mind as a New Homeowner

Becoming a homeowner is a big responsibility, but it’s also incredibly rewarding. ✨

Make sure to keep up with your mortgage payments and stay on top of any maintenance or repairs to keep your property in good shape.

It’s also wise to regularly review your mortgage deal.

You might be able to remortgage in the future to get a better interest rate or release equity for home improvements.

Most importantly, take the time to enjoy your new home. Whether it’s your first property or an upgrade, it’s a significant achievement, and you should be proud of reaching this milestone. 🎉

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

When is the best time to buy a house in the UK?

The UK housing market is busier in spring and early summer, with more properties available and more competition. Prices might be higher then.

In winter, the market slows down, so you might find better deals.

What extra costs should I expect when buying a home?

Beyond your deposit and Stamp Duty, be ready for other costs like moving, repairs, service charges (if it’s a leasehold property), home insurance, and utility bills.

What should I think about if I want to buy a property to let?

If you’re looking at a buy-to-let property, consider the potential rental income, managing tenants, extra taxes like higher Stamp Duty, and the rental demand in the area.

You might also need to fix up the property to attract tenants.

What if the property I’m buying is part of a chain?

Buying a property in a chain means your purchase depends on other buyers and sellers completing their transactions, which can cause delays.

Stay in touch with everyone involved and be prepared for setbacks.

Can I negotiate my solicitor’s fees, and what should I look for?

Yes, you can negotiate solicitor fees. Ask for a breakdown of their costs and check for hidden fees like document handling.

Make sure your solicitor is experienced in property transactions and quick to respond to your queries to keep things moving smoothly.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]