- What Is Mortgage Valuation?

- How Long After Valuation to Mortgage Offer?

- What Happens During a Mortgage Valuation?

- Does a Valuation Mean My Mortgage Is Approved?

- What Causes Mortgage Applications to Fail at Valuation?

- What Should You Do If Your Mortgage Is Declined After Valuation?

- What to Do If Declined After Property Survey?

- The Bottom Line

What Should I Do If My Mortgage Declined At Valuation?

The excitement of buying your dream home can quickly turn into disappointment when unexpected hurdles arise.

Imagine finding the perfect house, prepping for an appraisal, only to receive a lower valuation than anticipated, or worse, discovering a worrisome problem revealed by a surveyor.

It’s no surprise, then, that your mortgage application could be declined, leaving you feeling like your entire journey has come to a standstill.

Trust us, we understand.

A setback like this can feel immense, but here’s the good news: it’s not the end of your story.

Your dream home is still within reach.

In this guide, we’ll explain the ins and outs of mortgage valuation, why declines happen, and most importantly, what you can do next.

What Is Mortgage Valuation?

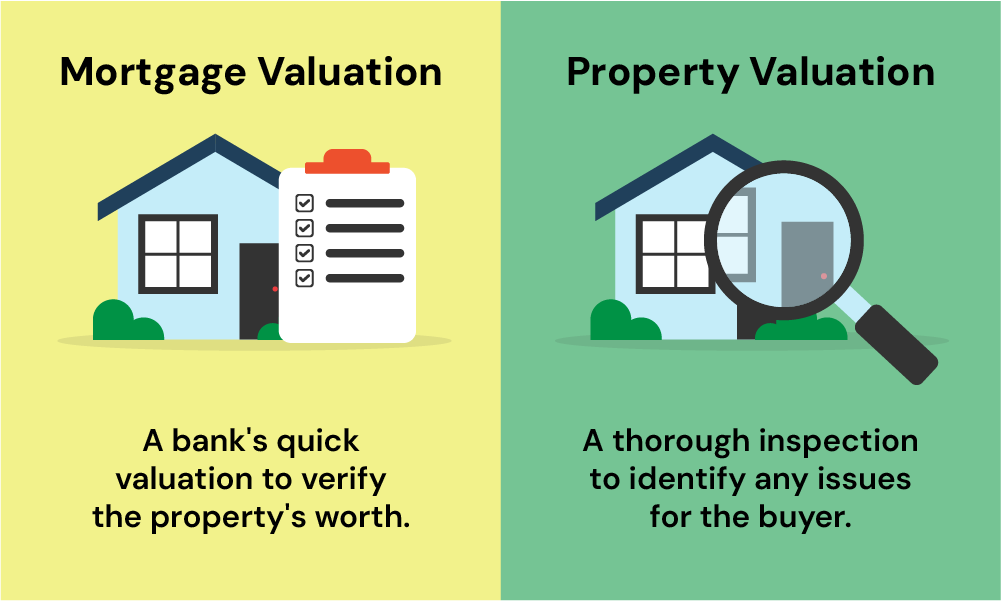

Mortgage valuation is a basic check carried out by your lender. The goal is to ensure the property you want to buy is worth the amount you’re planning to borrow.

It’s not a thorough survey. Instead, a surveyor appointed by the lender will quickly assess the property’s value based on factors like its condition, size, and location. They’ll also look at similar properties in the area.

But here’s the kicker: a mortgage valuation differs from a full property survey.

While a valuation is for the lender’s peace of mind, a full survey gives you, the buyer, a detailed report on the property’s condition.

It flags up any issues, like damp or structural problems, that could cost you down the line.

So, while a mortgage valuation is about ensuring the loan amount is safe for the lender, a full property survey is about making sure the property is a good buy for you.

How Long After Valuation to Mortgage Offer?

The time it takes to receive a mortgage offer after your property valuation can vary.

Typically, it ranges from one to two weeks. However, this timeframe isn’t fixed and can change based on a few factors.

The lender’s current workload is one of these factors – if they have many applications, it might take a bit longer. Your financial situation also plays a role; a straightforward case can be quicker to process.

Lastly, the property’s uniqueness or any issues identified during valuation may require additional time for thorough assessment.

What Happens During a Mortgage Valuation?

During a mortgage valuation, a valuer appointed by the lender assesses the property you intend to buy or remortgage.

This assessment focuses on several key elements: the size of the property, its overall condition, and any significant issues that could impact its value.

The location, including the surrounding neighbourhood and available amenities, is also taken into account.

Additionally, the valuer compares the property with similar ones in the area to ensure the price you’re paying is reasonable.

As discussed earlier, this valuation is primarily for the lender’s benefit, ensuring the loan amount is justified by the property’s worth, rather than a detailed examination of the property’s condition.

Does a Valuation Mean My Mortgage Is Approved?

Just because you’ve had a valuation done doesn’t mean your mortgage is definitely approved. This is a common misconception.

A valuation is just one part of the process. It’s the lender checking that the property is worth the price you’re paying.

This is different from a full mortgage approval, which involves more checks. The lender will look at your financial situation, credit history, and other factors before making a final decision.

So, a successful valuation is a good step, but it’s not the same as getting the green light for your mortgage.

What Causes Mortgage Applications to Fail at Valuation?

Applying for a mortgage involves various stages, and it’s crucial to understand that your application could be turned down during the valuation phase.

Let’s break down the reasons behind such rejections clearly and straightforwardly.

Property-Related Concerns

Issues uncovered during the property’s survey can also prompt lenders to reject a mortgage application. These problems might include:

- Asbestos detection.

- Cladding issues.

- Evidence of dampness.

- The presence of invasive plants like Japanese knotweed.

- Structural concerns.

Differences in Valuation and Sale Price

A prevalent cause of mortgage denials at this stage is when the property’s assessed value falls short of the purchase price you’ve agreed upon.

In such ‘down valuation‘ instances, lenders might revise the loan amount they’re willing to offer or potentially retract the offer.

Should you encounter this, you might want to:

- Attempt to negotiate a lower sale price.

- Consider raising your deposit, if possible.

- Dispute the results of the valuation report.

- Seek an alternative mortgage provider who might have a different perspective on your case.

Unique Property Builds

Properties that deviate from standard brick-and-mortar construction are often classified as ‘non-standard builds.‘ These types of properties pose a challenge for securing a mortgage since many lenders are hesitant to finance them.

Some common non-standard construction types that might hinder your mortgage application are:

- Thatched roof homes.

- Structures with steel framing.

- Timber frame constructions.

- Single brick buildings.

- High-rise apartment complexes.

But there’s hope. Mortgage brokers who focus on non-standard properties have established relationships with lenders who are more flexible in their lending criteria for such buildings. They can guide you in reapplying for a mortgage with a suitable lender.

What Should You Do If Your Mortgage Is Declined After Valuation?

When your mortgage application is declined post-valuation, it may feel disheartening, but it’s not the end of the journey. Here are steps to take to address this setback:

Understand the Reason

First, reach out to your lender for the specific reasons behind the decline. It could be related to the property’s condition, valuation discrepancies, or other issues. Pinpointing the exact reason is key to finding a solution.

Re-evaluate the Property

Review the valuation report thoroughly. Look for any factors that might have led to the decline, such as structural issues or a valuation much lower than expected. Understanding these details is crucial in determining your next steps.

Rectify Issues with the Property

If the decline is due to property-related issues, consider whether these can be addressed. This might involve repairing significant defects or even negotiating with the seller to lower the price in line with the valuation.

Improve Financial Health

Similar to improving credit for an Agreement in Principle (AIP), take steps to bolster your financial standing. This includes paying down debts and ensuring all bills are paid on time. A healthier financial profile may sway a future valuation positively.

Seek Professional Advice

A mortgage broker can be invaluable in these situations. They can review your case, advise on potential improvements, and identify lenders more likely to accept your application under the new circumstances.

Explore Alternative Lending Options

Different lenders have varied criteria and risk appetites, especially concerning property valuations. Exploring other lenders could uncover one with a more favourable view of your situation.

Don’t Hurry to Reapply

Avoid rushing into another application immediately. Instead, take the time to address the reasons for the decline. Reapplying too quickly can impact your credit score negatively and reduce your chances of approval.

Stay Optimistic and Persistent

A declined mortgage valuation doesn’t mean all doors are closed. Maintain a positive outlook and persistently work towards improving your circumstances. There’s often a path forward, even if it requires some extra steps.

What to Do If Declined After Property Survey?

If your mortgage application is declined following a property survey, it’s important to understand the difference between this and a mortgage valuation.

As we’ve mentioned earlier, a mortgage valuation is a basic check for the lender, while a property survey is a more detailed examination of the property’s condition.

If a survey reveals issues like structural problems, dampness, or other significant defects, a lender might see the property as too risky to lend on.

What should you do in this situation? First, review the survey report to understand the specific issues. Depending on the problems, you might negotiate with the seller to either have them fix the issues or reduce the property price.

Alternatively, you can seek a quote for repairs and decide if you can manage them after purchase. If the issues are too significant or costly, it might be wise to reconsider the purchase.

The Bottom Line

We’ve covered a lot in this guide about what happens when a mortgage is declined after a valuation. It’s clear that a valuation is a key part of the mortgage process, but it’s not the final decision on your mortgage application.

If your mortgage is declined after the valuation, don’t panic. Understanding the reasons why it happened is your first step. This could be due to the property’s condition, its market value, or other factors the lender considers risky.

One smart move is to use a mortgage advisor if you find yourself in this situation. They have the expertise to look at your application, understand why it was declined, and guide you on what to do next. They might suggest applying to a different lender, improving your financial situation, or even appealing the valuation.

If you’re feeling overwhelmed by the process or just want to make sure you’re doing everything right, getting professional mortgage help can be a big relief.

Need help find the right broker? Get in touch with us, and we’ll connect you with an FCA-qualified broker who’s experienced in dealing with situations like yours.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What can I expect during a remortgage valuation?

During a remortgage valuation, the lender assesses whether the property’s value still supports the mortgage amount. This is similar to a valuation for a new mortgage but focuses on any changes in the property’s value since your original mortgage.

How can I improve my property’s valuation?

To improve your property’s valuation, ensure it’s well-maintained and presentable. Address any minor repairs, improve curb appeal, and make sure all areas are clean and tidy. Upgrading certain aspects like the kitchen or bathroom can also positively impact the valuation.

Can I dispute a valuation if it leads to a mortgage decline?

Yes, you can dispute a valuation, but it’s not always straightforward. You’ll need to provide evidence to support your claim, such as recent sale prices of similar properties in your area. Engaging a professional to provide a second opinion can also be helpful. However, keep in mind that the final decision rests with the lender.

Is it possible to be declined after paying the valuation fee?

Yes, your mortgage can be declined even after you’ve paid the valuation fee. Unfortunately, this means you might lose the fee you’ve already paid. This fee is typically non-refundable, as it covers the cost of the property assessment conducted by the lender or surveyor.

Is my mortgage at risk if the valuation shows a higher property value?

It’s rare, but a higher valuation than the agreed sale price typically isn’t a cause for mortgage rejection. In these instances, lenders often proceed with the agreed loan amount.

Moreover, you aren’t required to disclose to the seller that the property’s value exceeds the agreed price. However, if there’s a significant difference between the sale price and the market value, lenders might review the situation more closely.

What is the typical cost range for a mortgage valuation?

The cost for a property valuation as part of a mortgage application varies, mainly influenced by the property’s market value and the specific type of survey conducted. Generally, the price range for this service falls between £150 and £1,500.

Related Articles

A Complete Guide To Mortgages Refused Due To Flood Risk

If you’ve ever thought about buying a home in the UK, you’ll know it’s not all about cute cottages and lovely gardens. There are a few extra challenges, like the weather. And by weather, we mean rain – lots of it. That lovely drizzle we Brits love to grumble about can sometimes lead to flooding, […]

Mortgage Approvals & Rejections: What You Need to Know

Getting a mortgage can feel like a rollercoaster ride. You’ve found your dream home, pictured yourself settled in, but then—bam! The dreaded rejection email comes through, and suddenly it feels like everything’s on hold. But don’t worry; you’re not alone in this experience. Mortgage rejections happen more often than you think, and while it’s frustrating, […]

What Should I Do If Skipton Refused My Mortgage?

Are Skipton Building Society Strict? Skipton Building Society’s mortgage lending criteria are quite comparable to other major UK lenders. They focus on essential factors such as your credit history, income, and the type of property you’re looking to buy. If you’re applying for a mortgage with them, it’s important to have a clear credit record […]