How to Remortgage on Low or Any Income Type: A Full Guide

Thinking about remortgaging but worried about how your type of income might affect the process?

Whether you’re looking to use your home’s equity for more funds or to lower your monthly payments, having a lower or varied income doesn’t mean it’s impossible.

In this guide, we’ll show you that remortgaging with a low income is quite possible and even straightforward.

We’ll also explain how working with a specialised broker can make the process easier and increase your chances of getting a good deal.

How Various Income Types Affect Your Remortgage

Different types of income can change how lenders see your remortgage application.

If you earn a regular monthly salary, lenders usually find it easier to assess your application. This steady income gives them confidence in your ability to pay back.

But, if you’re a freelancer or a landlord, your earnings might change from month to month. This can mean lenders will ask you for more proof of your earnings.

So, if you’re in this group, always have your documents ready to show a stable income.

It’s also key to remember that every lender views income types differently. Knowing this can help you pick the right lender for your needs. This choice can make your remortgage process smoother and more straightforward.

To get further understanding, let’s break down how various income types can influence your chances and what you can do to make things go smoothly.

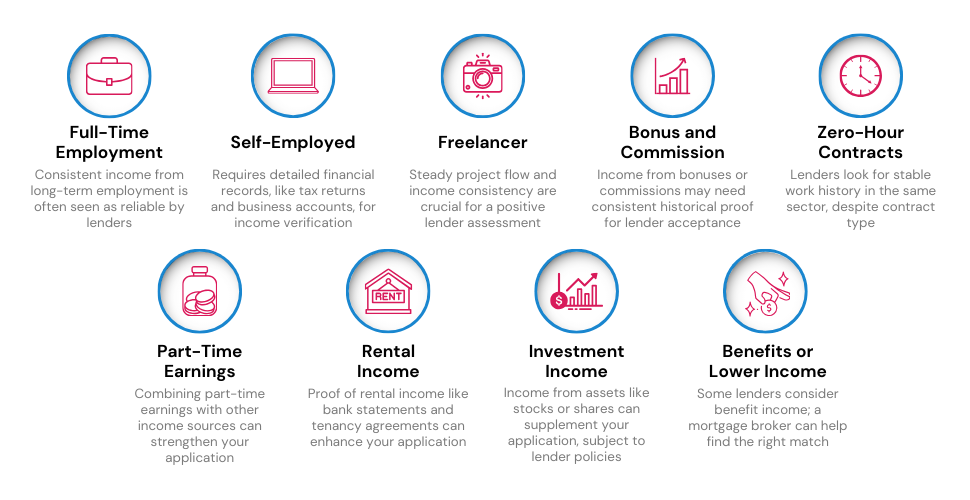

Remortgaging on Full-Time Employment

If you have been working full-time with the same company for at least three years, you are in a good position when it comes to most mortgage lenders.

This steady job and regular monthly income usually mean a simpler assessment process for lenders. Generally, showing your last three months’ payslips as proof of your steady salary is enough.

Remortgaging while Self-Employed

When you switch from a full-time job to being self-employed since you first got your mortgage, this can change a few more steps if you want to remortgage.

The main change is in the type of income proof you need to show. Some lenders might avoid offering remortgages to self-employed individuals due to the detailed checking process, but others specialise in helping people like you.

If you are self-employed and considering remortgage, prepare to show documents like:

- SA302 self-assessment tax returns

- Your finalised business accounts

- Payslips from your company, if you have them

If you’re newly self-employed, some lenders may accept less than 2 years of accounts, or even 1 year, if you are a professional in certain fields.

Remortgaging as a Freelancer

As a self-employed freelancer, remortgaging can be a bit challenging. However, it is still possible if you can show lenders that you have a reliable flow of income.

The key factors that lenders will consider are your earnings and the stability of your income.

If you can show that you have a steady stream of income, such as through contracts with a good amount of time left on them or repeated renewals, you will be in a stronger position.

Your income stability is what will mainly influence your remortgage prospects. Lenders will want to see that you are able to make your mortgage payments reliably, even if your income fluctuates.

Dealing with Bonus and Commission for Remortgages

If your income consists of commissions, bonuses, or overtime, it is important to plan your remortgaging approach. Different lenders may have different reactions to this type of income, as it can be variable.

However, remember that you have choices. Your goal should be to find a lender who will accommodate your payment terms, whether it is monthly, weekly, quarterly, or annually.

This will ensure that you can use your entire income stream to secure the most cost-effective remortgaging deals.

Remortgages on Zero-Hour Contracts

Zero-hour contracts do not necessarily exclude you from remortgaging options, but you should expect limited choices.

Lenders will look favourably at consistency in employment, such as having worked for the same employer for over a year or having a steady work record in the same sector.

Meeting other eligibility conditions can sometimes get you remortgaging rates that are on par with those who have full-time contracts.

Remortgaging on Part-Time Earnings

If you are on a part-time contract, don’t be discouraged from remortgaging.

Lenders will consider your income stability and property equity more than the number of hours you work.

To improve your remortgage application, you can combine your part-time earnings with other assets or income sources, which will strengthen your financial position and make the remortgaging process smoother.

Utilising Rental Income in Remortgages

As a landlord, you can maximise your rental income in the remortgage process by providing lenders with strong documentation, such as bank statements and tenancy agreements.

The more documents you can present, the more options you will have for remortgaging.

But, it is important to note that not all lenders will consider rental income when assessing your remortgage application.

Therefore, it is wise to consult with a good mortgage broker who can help you find lenders who are more flexible in this regard.

Using Investment Income to Remortgage

If you have investments that generate income, such as stocks, shares, or other revenue-generating assets, you can use them to your advantage during the remortgage process.

This income can be a lucrative supplement to your regular income, making you a more attractive borrower to lenders.

However, not all lenders will consider investment income when assessing your remortgage application. It is important to check with the lender before you start the process to make sure that they will accept your investment income.

Another option is to approach a private bank for an evaluation of your assets. This could give you the possibility to secure a loan against your assets without having to sell or liquidate them.

Remortgaging on Benefits or Lower Income

If you are on a low income or receive benefits, it is important to choose the right lender when remortgaging.

Some lenders will consider your benefit income as part of your total income, but not all of them. It is important to make sure that the lender you choose will accept your benefit income in full or in part.

There are many different types of benefits available, and each lender has different criteria for considering them as part of your income.

A seasoned mortgage broker can help you navigate the different lender requirements and find a suitable match for your specific circumstances.

How to Remortgage with Complex Income Types: A Step-by-Step

After identifying which income type you have, follow these steps to secure the best terms when seeking a remortgage with a complex income background:

Step 1: Gather your Documents – Prepare documents that showcase your varied income streams. This may include proof of income from freelance work, part-time jobs, rental proceeds, and investment returns.

Step 2: Understand Lender Criteria – Familiarise yourself with the varying criteria of different lenders. It’s essential to know that lenders have differing viewpoints on complex income structures, with some being more accommodating than others.

Step 3: Consult with a Broker – Engage the services of a knowledgeable broker to identify the most compatible lenders for your case. Utilising a broker can streamline the process, helping to avoid potential pitfalls and delays.

Being well-prepared and seeking the right assistance are vital elements in successfully securing a remortgage with a complex income profile.

Pro Tip

Improving your credit score can make you more attractive to lenders when remortgaging with complex income.

If you have questions about your credit score or are dealing with bad credit, please feel free to contact us. We will pair you with a good mortgage advisor who can help you address your concerns.

Can Pension Income Help in a Remortgage?

Yes, your pension income can help you remortgage, but it depends on your retirement situation. Lenders will consider your pension income, whether it is from a state or private source when assessing your application.

You can discuss your options for a repayment or interest-only mortgage with a lender based on your pension income.

If you are over 55 and have a small pension income, you may want to consider exploring equity release options.

Here are some specific things to keep in mind when considering your pension income for a remortgage:

- The amount of pension income you receive.

- The stability of your pension income.

- The length of time you have until you reach retirement age.

- Your other sources of income.

- Your overall financial situation.

It is important to speak to a good mortgage broker to get advice on how your pension income can help you remortgage. They can help you find a lender that is likely to accept your pension income and can help you get the best possible deal.

Can You Remortgage with Low Income?

Yes, you can. While some lenders require a minimum income between £10,000 and £20,000, many do not have such demands.

The possibility of getting a remortgage often depends on your total income picture and the size of the remortgage.

Is Remortgaging Possible Without a Job?

Getting a remortgage without a job can be tough, but there are options to consider, such as moving to a guarantor mortgage.

The goal is to find a solution that matches your current financial situation.

Why Expertise Matters in Remortgaging

Having a complex income, whether from self-employment, low income, benefits, or even unemployment, can make remortgaging feel overwhelming. But remember, the right guidance can make this journey smoother and more successful.

When you’re dealing with diverse income sources, the remortgaging process can feel like a maze. That’s where the importance of an expert comes in.

With their assistance, you’ll have a clear path straight to lenders who understand and cater to varied incomes, saving you both time and potential rejections.

Experts have their fingers on the pulse of the remortgage market. They can break things down into simple terms, guide you seamlessly, and ultimately boost your chances of landing a great deal.

The beauty of seeking professional help? You’re never walking this path alone. They dive deep into your financial situation, bringing to the surface the best options tailored just for you. It’s about making smart, informed choices with less stress.

Imagine cutting down your research time significantly, bypassing potential pitfalls, and securing a deal that feels just right for you. That’s what expert advice can offer.

Ready to take the leap? Just fill out this form. Once we get a glimpse of your financial picture, we’ll introduce you to a top-notch remortgage advisor who’s ready to craft solutions specific to your needs.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

Can I remortgage if I have multiple sources of income?

Yes, you can remortgage with multiple income streams. However, lenders may have different criteria on how they assess varied income types, so expert advice can be beneficial in these cases.

How can I improve my chances of remortgaging with an irregular income?

To improve your chances, make sure to have all necessary documents showcasing your income history and work with an experienced broker who can guide you to lenders more accommodating of irregular incomes.

What kind of documentation will I need for remortgaging with rental income?

If you are relying on rental income for remortgaging, you may need to provide rental agreements, bank statements showing rent payments, and potentially a history of stable rental income over a certain period.

Can I remortgage for a lower amount?

Yes, you can opt to remortgage for a lower amount than your current mortgage, which might help reduce your monthly repayments or the mortgage term.

How much can I borrow if I remortgage?

The amount you can borrow depends on various factors including your income, credit score, and the value of your property. It’s best to consult with a remortgage expert to get precise figures.

What happens if you remortgage?

When you remortgage, you switch your current mortgage for a new one, either with your existing lender or a different one. This can help you find better interest rates or release equity in your home.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Do I Need To Pay Solicitor Fees When Remortgaging?

Remortgaging your home can be a smart way to reduce your monthly mortgage payments or tap into your property’s equity. But the process isn’t always straightforward. One potential cost that often confuses homeowners is solicitor fees. Do you actually need to pay for a solicitor when remortgaging? Let’s take a closer look. When Do You […]

Unencumbered Mortgage: How To Remortgage a Fully Owned Home?

Owning a property without any debts hanging over it – sounds liberating, doesn’t it? And with that freedom, you might be thinking about the different ways to make the most of your fully paid property. Maybe it’s time to fix up the house or invest in a new opportunity? In this article, we’ll break down […]

How to Remortgage to Buy a Car: A Complete Guide in 2025

Car financing options like auto loans and leasing agreements typically come with scary double-figure interest rates. This coupled with the escalating car costs can discourage you from even dreaming of buying a new vehicle. But whether you’re eyeing a sleek electric sports car or a vintage camper van, getting behind your dream wheels isn’t out […]