- What Constitutes a Second Home?

- What is a Second Home Mortgage?

- Is It a Good Idea To Get a Second Home?

- How Much Can You Borrow for a Second Property?

- Your results

- How Much Deposit Do I Need?

- Your results

- Are Second Home Mortgage Rates Higher?

- What About Extra Costs for a Second Home?

- How To Get a Second Home Mortgage?

- Can You Use Equity in Your Current Home to Buy a Second Property?

- New Mortgage

- Your results

- The Pros and Cons of Having a Second Property

- The Bottom Line

Calculate Your Second Home Mortgage in the UK

Thinking about buying a second home? Maybe it’s a cosy cottage by the coast or a city apartment for those weekends away.

It’s an exciting idea, but it also makes you wonder—can you really afford it?

Luckily, using a second home mortgage calculator can help you find out if this dream is possible.

In this guide, we’ll make it super easy for you to understand how second home mortgages work, how much you can borrow, and what kind of extra costs are involved.

We’ve even included some handy calculators to help you along the way.

Let’s get started!

What Constitutes a Second Home?

According to UK tax law, a second home is a property you own in addition to your main residence.

This includes holiday homes, city crash pads, homes for dependents, and shared family holiday homes.

Properties fully rented out are classed as buy-to-let investments, not second homes.

What is a Second Home Mortgage?

A second home mortgage is simply a loan you take out to buy a second property. It could be a holiday home, an investment, or even a place for a family member to live in.

Just like your first mortgage, you borrow money from the bank to buy this second property, and then pay it back over time.

But remember, getting a second mortgage is a bit different from buying your first home.

Lenders might see it as a riskier move, so it’s important to know what you’re getting into and make sure you’re fully prepared.

Is It a Good Idea To Get a Second Home?

Getting a second home can be a wonderful thing—it gives you more space, maybe a holiday spot, or a way to invest your money.

But it’s also a big decision that comes with responsibilities. You need to consider if you can afford the extra payments and whether you’re okay with the costs that come along.

If you’ve done your calculations and feel confident, then a second home could be a great addition.

But let’s make sure you’ve got all the numbers right before you jump in.

How Much Can You Borrow for a Second Property?

The answer depends on several things: your income, your current debts, and how much of a deposit you have saved up.

Most banks will let you borrow up to 4.5 times your annual income, but it could be more if your finances are in really good shape.

Lenders comprehensively assess your income, existing commitments, and outgoings to determine what you can realistically afford to repay.

In some cases, if you have a strong credit history and stable income, you may even be eligible to borrow up to 6 times your income.

They also want to make sure you can afford to pay both your current mortgage and the new one, so they’ll check that all your monthly payments together aren’t more than 40% of your gross monthly income.

To find out how much you could borrow, use the mortgage affordability calculator below.

Mortgage Affordability Calculator

Number of applicants*

Applicant 1

Your results

Based on the figures you provided, you can expect to borrow between:

This calculator shows how much you might be able to borrow for a mortgage based on your income. Just enter your annual income, and it will give you an idea of what you could afford.

How Much Deposit Do I Need?

To buy a second home, you’ll need a bigger deposit than for your first home.

Most lenders will expect at least 15–20% of the property price, and sometimes even more if they think lending to you might be risky.

The bigger your deposit, the better your mortgage deal will be.

Building your deposit could involve:

- Existing property equity

- Savings accounts

- Inheritances

- Sale of assets like investments

- Family gifts

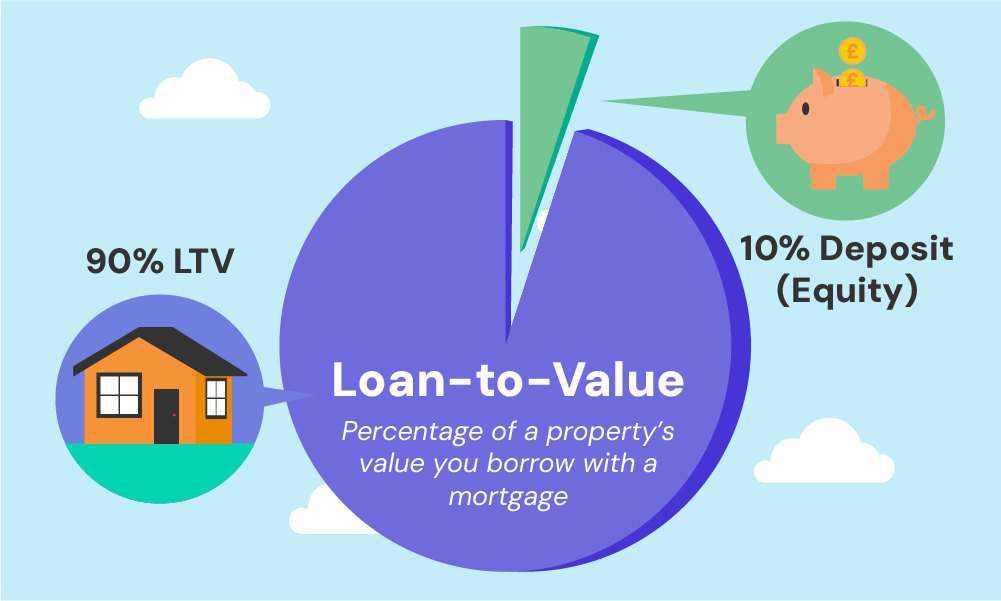

This deposit amount connects to something called the Loan-to-Value (LTV) ratio, which is the amount you’re borrowing compared to the value of the property.

For a second home, lenders often set the LTV limit at 75%. This means you’ll need to pay a 25% deposit upfront.

Here’s why it matters: a larger deposit means a lower LTV, which makes you less risky in the eyes of lenders.

Lower risk can lead to better mortgage rates, saving you money on interest over time.

For example, if you’re buying a £200,000 property and put down £50,000 (25%), your LTV ratio is 75%.

But if you save more and put down £60,000, your LTV drops to 70%, which might get you a better deal.

Need help figuring it all out? Use the Loan-to-Value Ratio Calculator below to see where you stand and what options you have as a borrower in the UK.

First, figure out how much money you can save, then plug the numbers into the calculator to get results.

Loan To Value Ratio Calculator

Your results

Based on the figures you provided, here are your results:

Get started with an expert broker to find out how much they could help you save on your

mortgage repayments.

Get Started

Get Started

Are Second Home Mortgage Rates Higher?

Yes, the rates are usually a bit higher for a second home. Lenders see it as riskier since if things get tight, you’re more likely to keep up payments on your main home rather than the second one.

Expect your rate to be about 0.5% to 1% higher than a standard first mortgage. But don’t let that scare you.

There are still good deals out there, and a bigger deposit or a good credit score may help you get a better rate.

What About Extra Costs for a Second Home?

When you buy a second home, you have to think about more than just the mortgage. There are a few extra costs you need to factor in:

- Stamp Duty: In the UK, you need to pay an extra 5% stamp duty on top of the usual rates when buying a second property. Remember, this can add quite a bit to your upfront costs. To check how much extra you’ll need to pay, use our stamp duty calculator.

- Insurance: Insurance is likely to cost more for a second home, especially if it’s left empty for long periods.

- Council Tax: You’ll have to pay council tax on both homes, and there aren’t usually discounts for second properties. Some councils might offer a discount for holiday homes, but it varies, so it’s always worth checking.

- Capital Gains Tax: If you decide to sell your second home for a profit, you might need to pay Capital Gains Tax on it.

- Maintenance and Upkeep: Remember, owning another property means taking care of it—repairs, maintenance, and other ongoing costs can add up.

How To Get a Second Home Mortgage?

Getting a mortgage for a second home is pretty similar to getting one for your first home, but there are a few extra things to consider.

Here’s a step-by-step guide to help you get started:

Check Your Credit Score

Lenders want to see that you’re reliable and that you pay your bills on time. Your credit score tells them if you’re good with money.

You can check your credit score online for free. If it’s not great, try paying off some debts or making sure all bills are paid on time to improve it.

Gather Your Documents

Next, you need to get all the paperwork ready. Lenders will ask for things like payslips, bank statements, and tax returns to make sure you can afford the loan.

Having everything ready in advance will make things go much faster and smoother.

Analyse Your Budget Carefully

Understand your income, outgoings, and whether you can comfortably afford two mortgage payments.

Write down all the money you have coming in each month and all your expenses. Don’t forget about things like food, bills, and other loans.

Lenders will want to see proof that you can handle both your current and new mortgage payments, so the more prepared you are, the better.

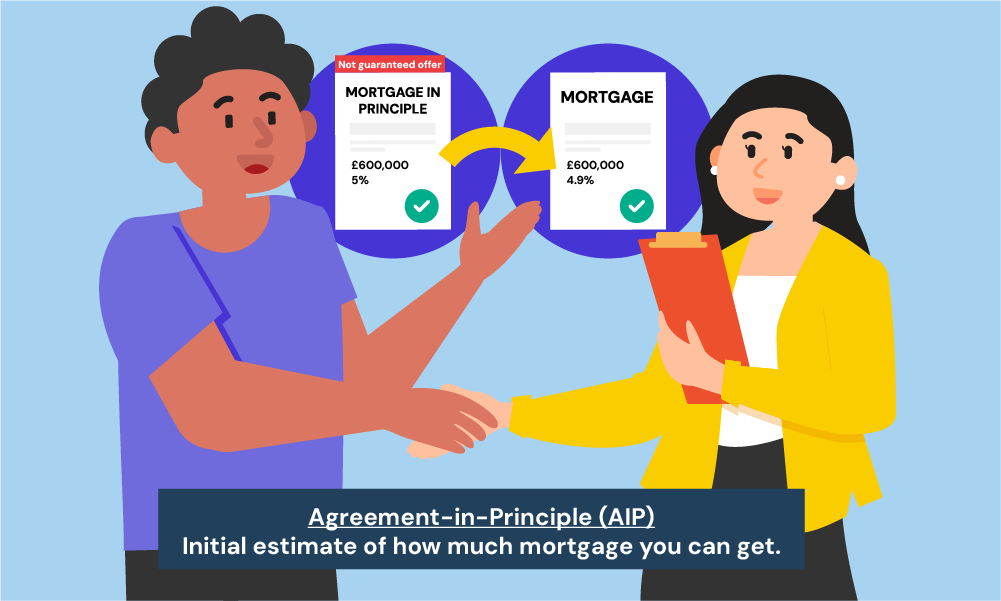

Get a Decision in Principle (DIP)

A Decision in Principle is like a promise from the lender that they would lend you a certain amount of money, based on your details.

It’s not a full mortgage offer, but it shows you’re serious and can help when you’re making offers on a property.

Find the Right Property

Once you have your budget and DIP, start looking for the right second home.

Make sure it fits within your budget and that you’ve thought about all the extra costs that come with owning a second home.

Apply for the Mortgage

Once you find the property you like, it’s time to apply for the mortgage.

Your broker or lender will help you fill out all the forms, and you’ll need to send in the documents you’ve gathered, like payslips and bank statements.

Valuation and Legal Work

After you apply, the lender will want to check the property’s value to make sure it’s worth what you’re paying.

They’ll also ask a solicitor to handle all the legal paperwork, like checking who owns the property.

Get Your Mortgage Offer

If everything goes well, you’ll get a formal mortgage offer from the lender. This will outline all the terms of your mortgage, like how much you’re borrowing and what the interest rate will be.

Exchange Contracts and Complete

Finally, your solicitor will exchange contracts with the seller’s solicitor. This means the sale is legally binding.

Then, on completion day, the money will be transferred, and the keys to your new home will be yours!

Can You Use Equity in Your Current Home to Buy a Second Property?

Yes, you can use the equity you’ve built up in your current home to help buy a second property.

Equity is simply the difference between how much your home is worth and how much you still owe on your mortgage.

If you’ve paid off a good chunk of your mortgage or if your home has gone up in value, you could have quite a bit of equity.

Remortgaging is when you take out a new loan on your current home to release some of that equity.

You can then use this cash as a deposit for your new property.

It’s like borrowing against the value of your home, which can be a really smart way to make use of what you already own.

But, remortgaging depends on your finances, meeting the lender’s criteria, and the options available in the market.

Not everyone will qualify, so it’s important to check if this is a realistic choice for you.

If you’re thinking about remortgaging, use our Remortgage Calculator below to see how much money you could release and what your new repayments might look like.

Remortgage Calculator

Your results

Based on the figures you provided, here are your results:

- New Monthly Payment:

- New Loan-to-Value (LTV):

- Monthly Payment Savings:

- Yearly Payment Savings:

- Total Lifetime Savings:

Get started with an expert broker to find out how much they could help you save on your

mortgage repayments.

Get Started

Get Started

This can be a great way to use your assets, but keep in mind that it also means you’ll be borrowing more on your first home, which will increase your monthly payments.

Affordability assessments will still apply to make sure you can handle repayments on both mortgages comfortably.

The Pros and Cons of Having a Second Property

Here’s a quick breakdown of the pros and cons to help you decide if a second property is right for you:

Pros:

- Extra space for holidays or family.

- A potential rental income.

- A long-term investment that could grow in value.

- Your own vacation spot anytime you want.

- Possible tax benefits if rented out as a holiday home.

Cons:

- Higher mortgage rates and extra costs.

- More responsibility and bills to keep track of.

- Risk of property value not increasing.

- Extra taxes like stamp duty and council tax.

- Harder to sell in a slow market.

- Vacant times can be costly if relying on rental income.

The Bottom Line

If you’re prepared for the costs and confident you can manage two properties, a second home could be a fantastic addition to your life.

While using an online calculator can give you a rough idea of what you might afford, talking to a mortgage expert is key to getting the full picture.

They’ll look at your money situation and find the best lenders and options for you. This makes the process much simpler and helps you get closer to owning that second home.

Ready to get started? Reach out to us, and we’ll connect you with an expert who can guide you every step of the way.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Do online calculators give accurate results?

Online calculators provide ballpark estimates only. For accurate figures tailored to your situation, a broker’s customised advice is essential.

What details do I need to use the calculators?

Key inputs like income, current debts, deposit amount, potential property value and more. The more precise your information, the better the estimate.

Should I rely solely on the online calculator results?

No, while useful guidance, the results are not definitive. To determine your true borrowing potential, consult a broker who can analyse your specific financial circumstances.

Can I borrow more than the calculator suggests?

Possibly, if a broker can demonstrate greater affordability to lenders based on your situation. But equally, you may have to borrow less than the calculator estimate. Broker expertise is invaluable.

What should I do after using the calculator?

The best next step is to consult with a good mortgage broker. They can provide customised calculations, product recommendations, and ongoing support to turn your second home dreams into reality.

Drop us a line and get matched with one of our specialist brokers.

How many mortgages can I have?

There’s no set limit on the number of mortgages you can have, but it depends on your financial circumstances and creditworthiness. Lenders will assess your ability to manage multiple mortgage repayments alongside your other financial commitments.

Consulting with a broker can provide clarity on how many mortgages you could realistically manage.

Related Articles

What Is Classed As A Second Home In The UK?

Thinking about buying a second property? Maybe a cosy cottage in the countryside for weekend escapes, a chic city flat for rental income, or even a seaside retreat for family holidays. Whatever your plan, you need to know how the UK classifies second homes. This isn’t just about ticking boxes – different tax rules, mortgage […]

How To Get Consent To Let To Buy Another Property?

Renting out your current home to become a landlord is tempting, especially if you’re moving, your family needs more space, or you want to try property investment. But before you put up “For Rent” signs, check with your mortgage lender. You’ll likely need their permission to rent out your property. While it can be a […]

Second Home Mortgage Rules and Requirements in the UK

Purchasing a second home can be an exciting milestone. Perhaps you want a holiday getaway, maybe you’re looking to invest in property, or you simply need more space for a growing family. Whatever your reasons, a second home mortgage opens doors to new possibilities. But, second home mortgages have unique rules and requirements you must […]