- How Much Can You Borrow?

- How to Maximise Our Self Build Mortgage Calculator

- How Reliable Are Self Build Mortgage Calculators?

- Where to Find the Most Reliable Self Build Mortgage Calculators in the UK?

- Do Lenders Use Self Build Mortgage Calculators for Their Offers?

- Digging Deeper: Self Build Mortgages Explained

- The Bottom Line

Self Build Mortgage Calculator: No Personal Details Required

In the UK, building your own home typically costs about £1,900 per square metre. To put this into perspective, for a 100-square-metre home, you’re looking at around £190,000.

However, the final cost can vary based on your specific plans and choices.

To begin understanding your funding needs, try our self build mortgage calculator as your starting point. It provides a tailored estimate, helping you map out your budget and financial plan.

This guide will show you how to use the calculator effectively, giving you a clearer picture of your borrowing power for your self-build adventure.

How Much Can You Borrow?

Use our Self Build Mortgage Calculator for a clear picture of your finances when building your home. It’s straightforward and quick, requiring no personal details to begin.

Just enter some basic details about your project, and you’ll get an instant, personalised estimate.

Remember, this is just the starting point.

Our calculator is a useful tool for an initial overview, but it doesn’t capture every detail of your project.

For a more comprehensive understanding, consider talking to a self build mortgage advisor. They’ll take into account the unique aspects of your project and provide a clearer picture of your mortgage options.

If you’re interested, simply send an inquiry for a free, no-obligation chat with an expert who can explore your full range of options.

How to Maximise Our Self Build Mortgage Calculator

Here’s how to use the self build mortgage calculator effectively:

- Enter Financial Information. Input your build cost, land price, and deposit amount. This data is crucial to estimate how much you might be able to borrow.

- Select Mortgage Details. Choose your preferred mortgage term and any other relevant details like interest rates.

- Experiment with Different Scenarios. Feel free to adjust your figures to explore various financial outcomes. If an issue is flagged by the calculator, it’s an indication to reassess your inputs.

This calculator is a starting point, providing initial estimates based on your inputs. The more accurate your information, the more reliable these estimates will be.

Remember, each lender has unique criteria, so our figures are general guides.

For a detailed, personalised financial plan, consult with a self build mortgage advisor. They can offer in-depth, tailored advice suited to your specific project and financial circumstances.

How Reliable Are Self Build Mortgage Calculators?

Self build mortgage calculators are handy tools for giving you a basic idea of how much you might borrow for your project.

However, they are not perfect in estimating the exact amount you need. These calculators provide a general figure but overlook the nuances of your unique situation and the current housing market.

Factors such as the cost of the land, the materials you plan to use, and the overall scope of your project play a crucial role in determining your borrowing capacity.

For example, a larger and more complex construction will likely require more funds compared to a smaller, simpler project.

Moreover, personal elements like your credit history, which significantly influence loan offers, are not accounted for in these calculators.

That’s why it’s essential to treat these calculators as a starting point in your planning process. While they offer helpful initial estimates, they can’t capture every detail that affects your mortgage. For a more precise and tailored estimate, seeking professional advice is key.

A mortgage expert, with an understanding of the finer aspects of self build projects and current market trends, can provide a more accurate figure.

They can assess your circumstances and guide you to a borrowing estimate that aligns with your specific needs and project scale.

Where to Find the Most Reliable Self Build Mortgage Calculators in the UK?

You’ll find self build mortgage calculators on several UK websites. But how do you know which ones are reliable?

Look for calculators on well-known, reputable financial websites or directly on lenders’ sites. These are more likely to give you realistic figures.

When checking these calculators, consider their update frequency and whether they reflect current market conditions. A good calculator should be easy to use and provide clear, understandable results.

Don’t rely on just one calculator. Try a few from different sources and compare the results. This cross-checking helps you get a broader view of your potential borrowing.

Do Lenders Use Self Build Mortgage Calculators for Their Offers?

Yes, many UK lenders use their own self build mortgage calculators. Each lender might have a different way of working out how much you can borrow.

This is because they all have their own rules or criteria. For example, some might lend you more if you have a bigger deposit, or they might look at how much you earn differently.

When you use a lender’s calculator, it gives you an estimate based on what that lender usually offers.

To get a more realistic idea, you should use several different calculators from various lenders. This will help you see the range of what you might be able to borrow.

Digging Deeper: Self Build Mortgages Explained

What is a Self Build Mortgage?

A self build mortgage is designed for those who want to construct their own home. Unlike a regular mortgage, where you borrow money to buy an existing house, a self build mortgage provides funds in stages to build a new house.

This staged funding helps you manage your building budget and ensures you have money at each critical phase of construction.

The main difference between a self build and a standard mortgage is how the loan is paid out. In a standard mortgage, you receive the whole loan amount at once.

But in a self build mortgage, the money is released in parts as your building project progresses. This approach helps you to align your spending with each stage of the build.

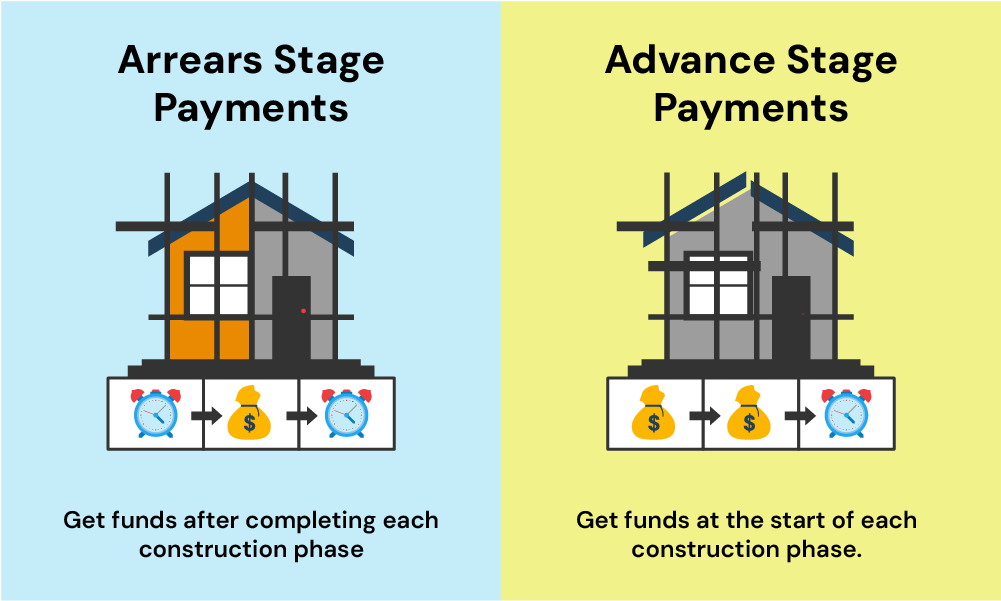

Types of Self Build Mortgages

In the UK, you’ll find two primary types of self build mortgages:

- Arrears Stage Payments – This common type releases funds after each building stage is completed. Ideal if you can cover initial costs yourself, it reimburses you upon completion of each phase, such as laying foundations or finishing interiors.

- Advance Stage Payments – Less common, this type provides funds at the beginning of each stage, helping if you lack substantial savings for upfront costs. It ensures you have the necessary cash to start each phase of your build.

Choose based on your financial situation and project management style. Both require clear plans and budgets before starting.

Benefits of a Self Build Mortgage

Why consider a self build mortgage? Here are some advantages:

- Savings on Stamp Duty. You pay stamp duty only on the land purchase if over £125,000, not on the building work, potentially saving you money.

- Budget Control. Building your own home lets you make cost-effective decisions, from materials to hiring. This could mean spending less than buying a pre-built house.

- Increased Home Value. Often, a self-built home’s final value is higher than the total spend, potentially giving you a property with greater value than its creation cost.

Challenges of a Self Build Mortgage

However, self build mortgages aren’t without challenges:

- Risk Awareness. Be prepared for cost overruns and extended construction times. Good planning is crucial.

- Higher Costs. These mortgages often require larger deposits and have higher interest rates, meaning more initial savings and potentially greater costs over time.

- Time Commitment. Building a home demands a significant time investment, from securing land to completing construction. Prepare to dedicate effort to your project.

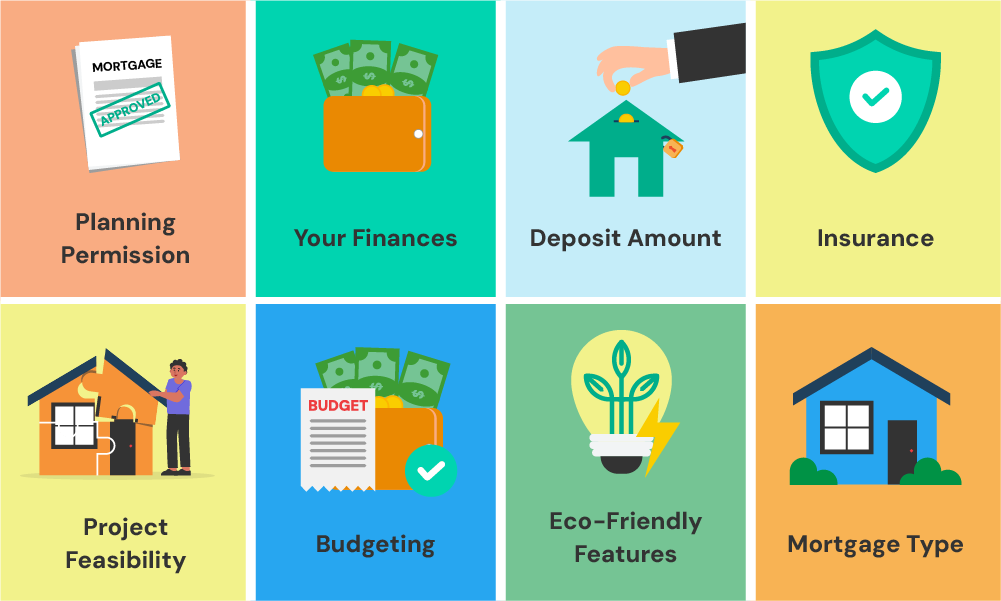

Eligibility for a Self-Build Mortgage: What You Need to Know

To get a self-build mortgage, you must meet certain criteria:

- Stable Income. Lenders need to see you have a reliable income to cover repayments. They typically use your salary, multiplied by about 4 to 4.5 times, to determine your loan amount.

- Age Requirements. Usually, you need to be at least 18 years old. Some lenders prefer applicants over 25 due to the complexity of self-build projects.

- Good Credit History. A solid credit history shows lenders you’re reliable. If you have credit issues, a mortgage broker can help find suitable lenders or improve your credit score.

- Higher Deposit. Expect to need at least 25% of the total build cost as a deposit, sometimes up to 40%, which is higher than standard mortgages.

- Planning Permission. You must have valid planning permission, proving your project meets local regulations.

- Detailed Building Plans. Your plans should be thorough, including cost breakdowns, timelines, and risk assessments.

- Professional Team. Having experienced professionals like architects and builders involved is often essential.

- Project Feasibility. Lenders will assess whether your self-build is practical and financially sensible.

Meeting these requirements shows lenders you’re ready for a self-build project and a reliable borrower.

What Paperwork is Required for a Self-Build Mortgage?

Along with standard documents like ID and proof of income, you’ll need:

- Planning Permission – to show your project is approved.

- Cost Estimates – Details of the total project cost.

- Regulations Approval – Proof that your project meets building standards.

- Construction Drawings and Specifications – Detailed plans of your build.

- Site Insurance and Structural Warranty – To cover risks during construction.

- Architect’s Cover – If required, proof of your architect’s professional indemnity insurance.

The Bottom Line

Expert advice is crucial for self build mortgages, as they’re quite specific and complex.

Finding a mortgage advisor who specialises in self builds is easy, either online or through recommendations. They’ll understand your unique needs, helping you navigate your budget and borrowing options.

While online calculators offer a good start, a specialist’s personalised advice will provide a clearer, more accurate view of your mortgage choices, ensuring you make informed decisions for your project.

To get started, get in touch with us. We’ll connect you with a professional mortgage advisor specialising in self build mortgages.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can first-time buyers get a self build mortgage?

Yes, first-time buyers can apply for a self build mortgage. It’s similar to standard mortgages, but you’ll need to show you’re ready for the challenge of building a home. This means having a solid plan and understanding the costs involved.

How much deposit do I need for a self build mortgage?

Typically, you need at least 25% of the total build cost as a deposit. Sometimes, this can be up to 40%. It’s more than what you’d usually need for a standard mortgage because building a house is seen as riskier.

Do I need professionals to help with my self build?

Yes, it’s a good idea to have experienced professionals like architects and builders. They help ensure your project is well-planned and sticks to building regulations. Plus, they can be a big help in making your mortgage application stronger.

What are LTV ratios, and how do they affect self build mortgages?

LTV, or Loan to Value ratio, is how much mortgage you have in relation to how much your project will be worth once completed. Lower LTV usually means better mortgage terms. In self builds, keeping a low LTV can be challenging but is beneficial for better mortgage rates.

Can I get a 100% self build mortgage?

100% self build mortgages are rare. Most lenders require a deposit because it reduces their risk. If you own your land outright, some lenders might consider it as part of your deposit, which can help.

Can I use my land as security for the mortgage?

Yes, if you already own the land, many lenders will accept it as part or all of your deposit. This can be really helpful in reducing the cash deposit you need to provide. Just make sure your land has planning permission, as this increases its value to the lender.

Should I have a contingency fund for a self build project?

Absolutely, it’s very important to have a contingency fund. Building projects often have unexpected costs, so having extra money set aside can cover these surprises. A good rule is to have about 10-20% of your project budget as a contingency fund. This helps you deal with any unforeseen expenses without derailing your project or finances.

Related Articles

First-Time Buyer’s Guide to Self Build Mortgages

More and more people are choosing to build their own homes these days. It’s a great way to save money and bring your dream home to life. Imagine that perfect bedroom with a walk-in closet or your ideal kitchen – it’s all within reach. But before you get lost in the excitement of planning your […]

Can You Get a Mortgage to Build a House in Your Own Land?

Building a home on your own land in the UK is an opportunity to turn your dream into a reality. It’s about more than just construction; it’s a personal journey. You get to design every detail to suit your taste and lifestyle, from the floor plan to the choice of materials. This approach not only […]

Should You Use Self-Build Mortgage Advisors?

Understanding self-build mortgages is essential if you’re considering building your own home in the UK. A self-build mortgage is different from standard mortgages, and having a specialised mortgage advisor can significantly benefit your project. These advisors have the expertise to guide you through the unique financial landscape of self-building, ensuring your project remains feasible and […]