- Are There 5% Deposit Mortgages in Scotland?

- Who Can Qualify for a 5% Deposit Mortgage in Scotland?

- How Much Do You Have To Save Up for a House in Scotland?

- How Much Can You Borrow with a 5% Deposit in Scotland?

- How To Get 95% Mortgages in Scotland?

- Who Offers 95% Mortgages in Scotland?

- Alternative Government Schemes for First-Time Buyers in Scotland

- Key Takeaways

- The Bottom Line

How To Secure Mortgages With 5% Deposit In Scotland?

Saving a big deposit for a house is often the biggest challenge for first-time buyers.

High living costs, stagnant wages, and unpredictable expenses – these things can make you feel like owning your first home is impossible.

However, that’s not true.

With 95% mortgages in Scotland, you can own a home and apply for a mortgage with just a 5% deposit.

Intrigued?

This guide unpacks all the information you need to secure a mortgage with a 5% deposit in Scotland.

Are There 5% Deposit Mortgages in Scotland?

Yes, there are, under what’s known as 95% LTV mortgages.

Let’s unpack that a bit. 😃

LTV, or loan-to-value ratio, is the percentage of the property’s value that the lender is willing to finance.

In simple terms, if you’re putting down a 5% deposit on a home, your mortgage lender will cover the remaining 95% of the home’s price.

However, snagging one of these deals in Scotland might be a bit trickier than in England.

The main reason is that fewer lenders are offering them. This means you’ll need to do a bit more legwork to find a suitable mortgage provider that offers high LTV mortgages, especially ones that align with the type of property you’re hoping to buy.

Who Can Qualify for a 5% Deposit Mortgage in Scotland?

Lenders take a close look at different factors of your financial health to decide if you’re a safe bet. Here’s a clear breakdown:

- Income Level – Higher income can improve your chances because it suggests you have more financial flexibility to meet your mortgage obligations.

- Employment Status – If you’re self-employed or on a zero-hours contract, it might be harder to get approved. Lenders prefer steady employment as it indicates stable income.

- Credit Score – Your credit history acts as your financial reputation for lenders. A higher credit score makes you a more attractive mortgage candidate. Because it shows lenders you’re good at managing debt.

- Debt-to-Income Ratio – This ratio compares your debt to your income. The lower it is, the better, showing lenders you’re not overburdened by debt. Lenders usually look for a ratio below 36-43% of your gross income.

- Type of Property – What you plan to buy also plays a role. New builds and flats might face more checks due to higher perceived risks. In contrast, older houses often have fewer hurdles, potentially easing the mortgage process.

- Deposit Source – Where your deposit comes from can influence your application. Savings or gifts from family are preferred. Lenders may ask for proof to verify the deposit’s legitimacy.

- Age – Being under 50 can work in your favour, as lenders often view younger borrowers as less risky due to the longer potential earning period ahead of them.

- Long-term Affordability – Lenders assess if you can keep up with payments over time. They consider potential income changes or interest rate rises to ensure long-term affordability.

How Much Do You Have To Save Up for a House in Scotland?

Let’s talk numbers. 📊

The average house price in Scotland is £190,000, according to the latest UK House Price Index. For a 95% mortgage, you’d need to save up a 5% deposit, which is about £9,500.

However, this is just an estimate. The actual amount you need can change based on the property type and location.

Here’s a table that gives you an estimate of the average house prices in Scotland:

| Property type | December 2023 | 5% Deposit |

|---|---|---|

| Detached | £349,173 | £17,458.65 |

| Semi-detached | £205,607 | £10,280.35 |

| Terraced | £159,647 | £7,982.35 |

| Flat or maisonette | £128,728 | £6,436.4 |

| All | £190,341 | £9,500 |

Remember, it’s not just the deposit you need to think about. There are other costs too, like the fee for the survey of the property, legal fees (conveyancing), and the cost of moving your stuff. All this can add up to an extra few thousand pounds.

So, how do you save up? Start by setting a CLEAR savings goal based on your target property price. Then, look at your spending to see where you can cut back and save more. Even small savings can add up over time.

How Much Can You Borrow with a 5% Deposit in Scotland?

Lenders want to know how much you can safely borrow without stretching your finances too thin. They look at a few things to decide this.

First up is your income. Generally, you might borrow up to four to five times your annual income.

Next, they check your monthly spending and debts. This helps them see if you can handle the mortgage payments on top of your other bills.

They also look at your credit score. A better score can mean you’re able to borrow more because it shows you’re good with money.

For example, if you earn £25,000 a year, you might be able to borrow between £100,000 and £125,000. This is just a rough guide, though. The exact amount can vary based on the lender and your situation.

Remember, while borrowing more might seem great, it’s important to be sure you can keep up with the repayments. Overstretching now could cause problems down the line.

How To Get 95% Mortgages in Scotland?

Applying for a 95% mortgage in Scotland, where you only need to put down a 5% deposit, involves a clear process. Here’s how you can go about it:

1. Check Your Financial Health

You can check your financial health here for FREE.

Begin by getting a clear picture of your finances.

This includes checking your credit score through agencies like Experian, Equifax, and TransUnion to ensure you’re attractive to lenders.

Remember, a good credit score is key. Also, save at least 5% of your future home’s purchase price for the deposit and budget for extra costs, such as survey fees and conveyancing.

2. Gather Necessary Documents

Prepare the paperwork needed for your mortgage application. This typically involves proof of ID (like a passport or driving licence), proof of address, recent bank statements to show your deposit, payslips or accounts for income proof, and any other evidence of financial commitments.

3. Apply for a Mortgage in Principle

Secure an agreement in principle (AIP) from a lender.

This gives you and sellers confidence in how much you can borrow and demonstrates you’re serious about buying. Watch out for hard credit checks, as they might affect your credit score.

4. Find Your Property

Search for a home that meets your needs and fits within your budget. Use your AIP to strengthen your offer through the estate agent, showing you’re ready and able to proceed.

5. Make a Formal Mortgage Application

After your offer is accepted, return to your lender to formally apply for the mortgage. Provide detailed info about your financial situation and the property. The lender will then conduct a survey to value the property.

6. Final Approval and Legal Work

Upon successful application, you’ll get a formal mortgage offer. This is the moment to check all terms before moving forward. A solicitor or conveyancer will handle the legalities, including property transfer and stamp duty payment.

7. Move In

After the legal process concludes and funds are transferred, you’ll receive the keys.

Congratulations, you’re a homeowner!

Who Offers 95% Mortgages in Scotland?

You can find these mortgages at places like the Royal Bank of Scotland (RBS) and Nationwide. But, keep in mind, who can get these mortgages depends on a few things.

You need to live in the UK, be a certain age, and buy a house at a set price. Also, for some of these deals, the house can’t be brand new.

Alternative Government Schemes for First-Time Buyers in Scotland

If you don’t qualify for a 95% mortgage in Scotland, check these government schemes for first-time buyers:

Low-Cost Initiative for First-time Buyers (LIFT)

LIFT helps first-time buyers in Scotland buy a home more easily. Since 2007, it has helped over 12,000 people become homeowners.

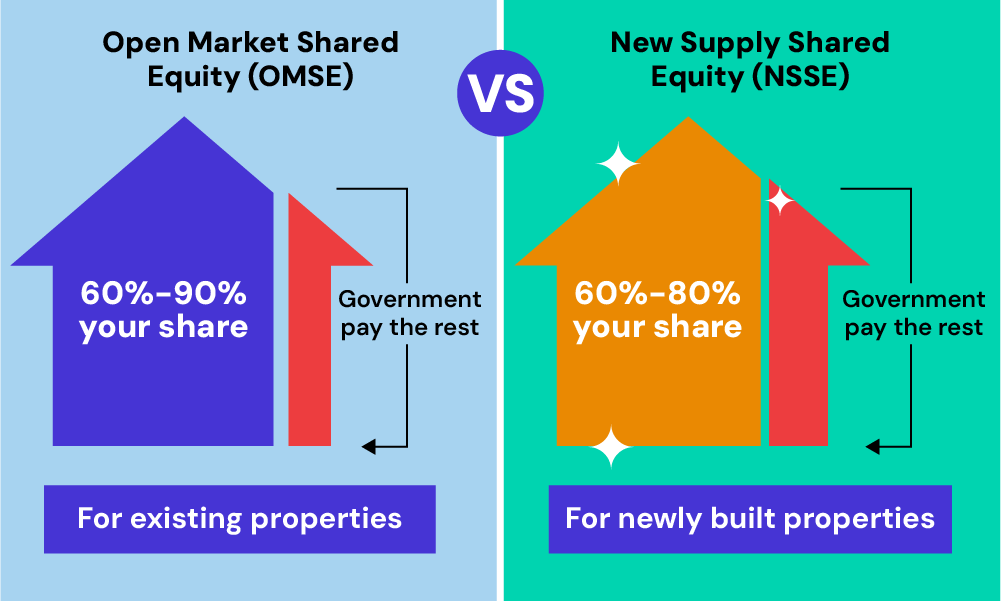

There are two key schemes under LIFT: the Open Market Shared Equity (OMSE) Scheme and the New Supply Shared Equity (NSSE) Scheme.

The Open Market Shared Equity (OMSE) Scheme lets you buy a home on the open market. You pay for part of the home’s price– typically between 60% to 90% – and the government covers the rest. This means you need a smaller deposit and loan.

Right now, the OMSE scheme is paused for 2023/24. Its budget is all spent, so it’s waiting for new funding decisions for 2024/25. We’ll keep you updated on when it might open again.

The New Supply Shared Equity (NSSE) Scheme focuses on new-build homes from councils or housing associations. Like OMSE, you buy most of the home – 60% to 80% of the cost– and the government pays for a part. You own the home outright, but the government’s share is protected by a legal agreement.

Both schemes aim to make buying a home more affordable. You start by owning part of your home and can buy more over time. This setup is perfect if you can manage regular mortgage payments but struggle with a big deposit.

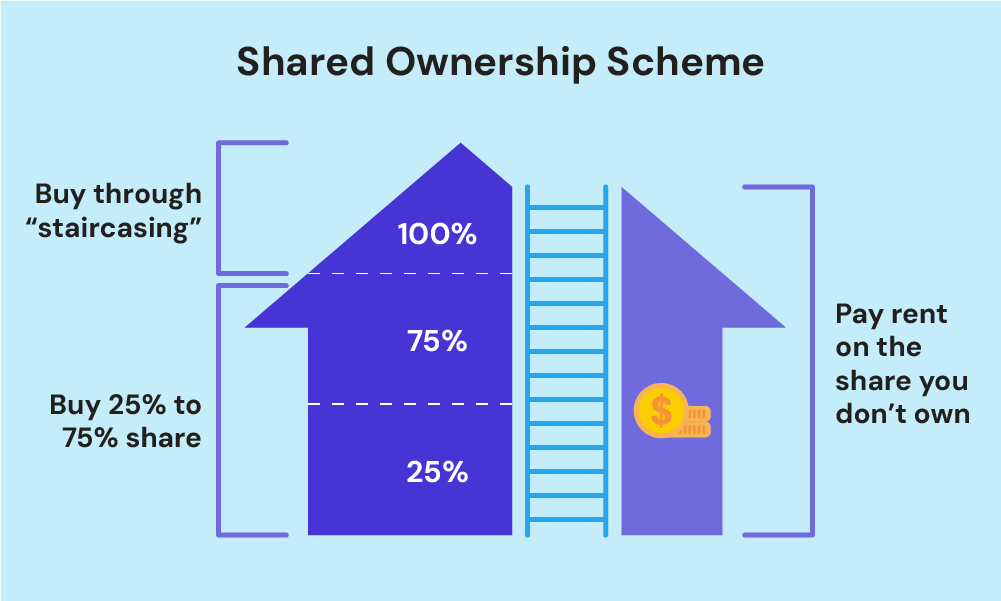

Shared Ownership

With shared ownership, you buy a portion of your home (between 25% and 75%) and rent the rest.

This scheme is flexible; you can increase your ownership share over time.

It’s open to first-time buyers, those over 60, and previous homeowners who now find full ownership unaffordable.

Key Takeaways

- You can get a 95% mortgage in Scotland with just a 5% deposit, but fewer lenders offer this compared to England.

- Lenders look at factors like your income, credit score, employment, debts, and where your deposit comes from to decide if you qualify.

- For a £190,000 home in Scotland (the average price), you’d need around £9,500 for a deposit.

- Saving for a deposit, improving your credit score, and checking your finances can improve your chances of getting approved.

- If you don’t qualify for a 95% mortgage, options like LIFT and Shared Ownership can help reduce upfront costs.

The Bottom Line

With 95% mortgages, owning a home in Scotland even if you have a small deposit is possible. However, the journey will not be easy. There will be hurdles such as strict lending rules and fewer available deals.

So, being prepared is important. Make sure to work on your finances, boost your credit score, and know your debt-to-income ratio to improve your chances.

But if you want to get started without stressing out about the process, talk to a good mortgage broker. They can help you find the right mortgage by giving advice that suits your situation.

Feeling lost? Reach out to us. We’ll arrange a quick, FREE, and no-obligation consultation with a skilled broker familiar with Scotland’s mortgage scene. They’ll guide you, making the search for your mortgage easier and less stressful.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I remortgage once I have a 95% mortgage?

Yes, you can remortgage to a different mortgage deal. This could be a good move if you find lower interest rates or if your finances get better.

But, watch out for extra costs like early repayment fees on your existing mortgage, fees for setting up the new one, and legal costs.

Always check if switching saves you money after considering these fees. To understand more, speak with a mortgage broker. They can make this process easier for you.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Can Second-Time Buyers Get 95% Mortgages?

So, you’re ready to move again. Perhaps your family’s growing or a new job calls, but you’ve hit a snag: your deposit is smaller this time. If you’re in this situation, you’ve likely searched countless lenders on the internet to find 95% mortgage deals in the UK. With few options, strict lending rules, and high-interest […]

Can You Get Mortgages with a 5% Deposit and Bad Credit?

Getting a mortgage in the UK might seem tough, especially if you’ve had financial issues before. If you’re buying your first home and worried about your credit score, there’s good news. You might be able to get a 95% mortgage, which means you only need a small deposit. This article will show you that even […]

A Quick Guide to 5% Deposit Mortgages for First Time Buyers

If you’re trying to buy your first home, you’re probably feeling the squeeze. With everything getting more expensive, saving for a big deposit can feel like climbing a mountain. But here’s the deal: mortgages that let you put down smaller deposits exist. This helps first time buyers and those struggling to save up for big deposits […]