- What is a Default?

- Can I Get a Mortgage After a Default?

- Will the Type of My Default Affect My Mortgage Application?

- How Long Does a Default Stay on Your Credit File?

- When Can I Apply for a Mortgage After a Default?

- How Much Can I Borrow with Defaults on My Credit File?

- How to Secure a Mortgage With Default?

- Does a Satisfied Default Improve My Mortgage Chances?

- What if I Have Other Credit Issues Alongside Defaults?

- How Can My Earnings Help in Getting a Mortgage with Defaults?

- Key Takeaways

- The Bottom Line

How To Get a Mortgage With a Default? A Comprehensive Guide

Obtaining a mortgage with a default can frequently lead to rejections.

Especially when approaching mainstream lenders who usually demand good credit histories.

But, this doesn’t imply that this is an impossible task. There exist mortgage providers that are open to applications from individuals with defaults.

These specialist lenders are better aligned to serve those confronted with defaults and other credit-related challenges.

If you have questions about your default, its impact on your mortgage application, or even just the basics like how long a default stays on your credit file, you’re in the right place.

In this guide, we’ll address all these concerns, ensuring you’re well-informed and confident in your next steps.

What is a Default?

A default occurs when a borrower fails to meet the legal obligations of a loan, often by not making the required payments. But, this situation is not just limited to mortgage loans.

Here are a few examples of how defaults can occur:

- Missing a credit card payment.

- Failing to pay your mobile phone bill.

- Skipping mortgage repayments.

- Not paying back a personal loan on time.

Each of these instances results in a default, which gets recorded on your credit file. This tells potential lenders that you’ve had trouble managing debt in the past, which might make them wary about lending to you in the future.

Can I Get a Mortgage After a Default?

Yes, you can. But, defaults on your credit file can make the mortgage process more challenging, as lenders may view them as a sign of higher risk.

That said, having a default doesn’t necessarily close the door on your homeownership plans.

Some specialist lenders are more open to applicants with credit issues, and working with a broker can help identify these options.

But, even with a broker’s support, your mortgage choices may still be fewer compared to someone with good credit.

Success relies on your financial situation, meeting the lender’s criteria and presenting a strong application.

Will the Type of My Default Affect My Mortgage Application?

It’s crucial to understand that not all defaults are viewed equally. Lenders often differentiate based on the type and severity of the default in question.

For instance, a default on a mobile phone contract might not carry the same weight as a default on a secured loan, the latter being viewed as more severe.

Understanding this distinction is key when applying for a mortgage. By aligning yourself with lenders who are more amenable to the specific type of default you have on your credit history, you can increase your chances of approval.

How Long Does a Default Stay on Your Credit File?

A commonly held belief is that a default must be off your credit file, usually after six years, before you can apply for a mortgage. This belief, however, doesn’t align with reality.

Defaults can remain on your credit file for six years. But this doesn’t mean you have to wait out this period before contemplating homeownership.

Even within this six-year window, you can apply for a mortgage. Recent defaults can make the process more challenging, but they don’t eliminate your chances.

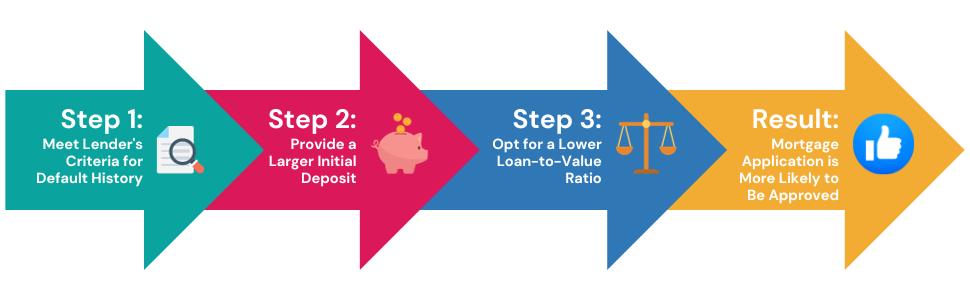

When Can I Apply for a Mortgage After a Default?

As mentioned earlier, you can apply during the 6-year window of your default. But, note though that there’s no one-size-fits-all answer.

The timing depends on many factors like the criteria of lenders and your circumstances. That said, more recent defaults can make the process more challenging. But, it’s not impossible.

Some lenders are even willing to consider applications from borrowers with active defaults. The conditions surrounding these cases can be quite specific and usually require a larger deposit or a lower loan-to-value ratio. It’s not the most straightforward route to a mortgage, but it is an option for some.

How Much Can I Borrow with Defaults on My Credit File?

Credit defaults may impact the total amount you can borrow for a mortgage. Lenders often look at credit history to assess how much of a risk it might be to loan money.

The presence of defaults can sometimes lead to lenders offering a lower maximum loan. They may lend between 3 and 5 times your income. But, each lender has their own criteria for assessing risk.

Some lenders are more comfortable with certain types of defaults and may be willing to loan a higher amount, while others may be more conservative.

So, the impact of defaults on your borrowing capacity can vary quite a bit from lender to lender.

How to Secure a Mortgage With Default?

If you’re thinking about applying for a mortgage with a default on your record, the process might seem a bit more complex. However, by taking the right steps and with careful preparation, you can enhance your prospects.

Here are some steps you can take to secure a mortgage with default:

1. Check Your Credit Report

It’s essential to be aware of what’s in your credit report. By understanding its details, you’ll be able to foresee any potential issues that may arise during the mortgage application process.

You can check your credit report through Credit Report Agencies like Experian, Equifax, and TransUnion. If you find an error or suspect fraudulent activity, contact the CRA to have it corrected. This could involve giving further evidence or documents.

2. Choose the Appropriate Lender

Remember, each lender has unique criteria when it comes to defaults. It’s beneficial to find a lender whose criteria align well with your specific circumstances.

3. Boost Your Initial Deposit

Having a more substantial deposit to offer can often tilt the balance in your favour, even when there’s a default on your record.

4. Show Financial Stability

Demonstrating a steady income and responsible financial behaviour can balance out any concerns caused by a default on your credit history.

5. Identify Lender’s Criteria

Each lender will have its own unique set of checks, understanding these can enhance your chances of successful application.

For example, if one lender does not accept borrowers with defaults in the past three years, but another does, an experienced advisor can guide you towards the latter.

A professional’s advice can be your key in this process. Skilled mortgage brokers can guide you through these steps, helping match you with appropriate lenders and improving your application’s likelihood of approval.

Does a Satisfied Default Improve My Mortgage Chances?

Paying off a default can increase your chances of securing a mortgage. While the default will still appear on your credit report, lenders often perceive satisfied defaults as a positive step towards financial responsibility.

But, there’s a common misconception that one must satisfy all defaults before applying for a mortgage.

While satisfying defaults improves your prospects, certain lenders are open to working with applicants who have unsatisfied defaults.

Therefore, it’s essential to explore all options and seek professional advice to understand your unique situation.

What if I Have Other Credit Issues Alongside Defaults?

Applying for a mortgage can get a bit tricky when you’re dealing with more than just defaults. Factors like County Court Judgements (CCJs), bankruptcy, and other credit concerns paint a bigger picture that lenders assess to measure risk.

Just remember, even if you’ve had multiple credit issues, getting a mortgage isn’t impossible. A lot hangs on factors like the age of these issues, how severe they were, and whether there were any extenuating circumstances.

To give you a better idea, let’s consider how different credit issues could impact your mortgage application.

We’ve arranged them in a table below, noting the severity and potential consequences:

| Credit Issue | Severity | Potential Mortgage Impact |

|---|---|---|

| Repossession | High | This could lead to application declines. Impact lessens as time passes. |

| Defaults | Medium | Smaller or older defaults are less problematic. Impact lessens over time. |

| Late Payments | Low | Regular or recent late payments could cause concern. |

| CCJs | High | Often seen as severe but manageable if paid and not recent. |

| IVA | High | Most lenders wait until an IVA is fully satisfied. |

| Bankruptcy | High | This can be a significant issue, particularly if recent. |

This table helps illustrate that not all credit issues carry the same weight. But remember, different lenders may have different views on these matters.

If you’re dealing with multiple credit issues, getting advice from a good mortgage advisor can be invaluable in understanding where you stand.

How Can My Earnings Help in Getting a Mortgage with Defaults?

Your income can play a significant role in securing a mortgage, even if there are defaults on your credit file. A strong income can indicate to lenders that you have the means to meet your mortgage repayments, which can help to offset the risk associated with any defaults.

Different lenders consider income in different ways, and may also take into account other financial commitments you have, such as debts or dependents.

For instance, some may only consider basic salary, while others may include overtime, bonuses, or other income sources.

Key Takeaways

- A default occurs when you miss payments on loans, bills, or credit cards, and it stays on your credit record for six years. This can make it harder to get a mortgage, but it’s not impossible.

- Specialist lenders may offer mortgages to those with defaults, but you might need a larger deposit, fewer borrowing options, or face higher interest rates.

- Defaults on smaller bills (e.g., mobile phone contracts) may be less severe to lenders than defaults on bigger loans, but recent defaults or multiple defaults can make approval more difficult.

- Working with a specialist broker can help you find lenders willing to consider your situation and improve your chances, even if the default is unsatisfied.

The Bottom Line

Getting a mortgage with defaults isn’t just a theory – it’s a reality for many. Defaults may affect your application, but they don’t have to halt it completely.

The secret to making this a reality is being well-prepared, knowing what lenders look for, and, crucially, seeking expert advice.

Everyone’s financial situation is different and needs a tailored approach. The kind, severity, and timing of your defaults, along with your income and current financial commitments, all play their part in the mortgage process.

With all these aspects to consider, getting professional advice can be hugely helpful. So, don’t let credit defaults hold you back from owning a home.

Get in touch with us today. We’re here to help you find the right broker, someone who gets your situation and is committed to finding the best way forward for you.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What is a default notice?

A default notice is a formal letter from a lender informing you that you’ve failed to keep up with the repayments on a credit agreement. It’s typically sent after multiple missed payments and outlines the steps you need to take to rectify the situation.

What stops you from getting a mortgage after a default?

A default can complicate the mortgage application process, as it may signal to lenders that you’re a higher risk. This can lead to fewer mortgage options or higher interest rates. Other factors, such as multiple defaults, the recency of the default, other credit issues, and overall financial health can also impact your ability to secure a mortgage after a default.

What happens if you default on a mortgage in the UK?

If you default on a mortgage in the UK, your lender may start the repossession process. But, this is typically a last resort. Lenders often prefer to work out a payment plan to help you catch up on missed payments.

How long does a default stay on my credit report in the UK?

In the UK, a default will stay on your credit report for six years, regardless of whether you’ve paid off the debt.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How To Remortgage With a Bad Credit: A Complete Guide

Thinking of renovating the kitchen, building an extension, or finally booking that dream family holiday? If bad credit’s been holding you back from remortgaging to free up cash, you’re not alone. Many people worry that their past financial mistakes might prevent them from using their home’s value. But good news: it’s possible to remortgage even […]

How To Improve Mortgage Credit Score? 10 Best Tips in 2025

When you’re applying for a mortgage, your credit score is like a summary of your financial behaviour. It shows how well you’ve managed credit in the past, and lenders use it to decide if they’ll approve your application. Your credit score doesn’t just affect approval—it also impacts the interest rate you’ll be offered. A higher […]

How To Get Subprime Mortgages in the UK: A Complete Guide

History has a funny way of shaping where we end up, and mortgages are no exception. If you remember the subprime mortgage crisis of 2007-2008, it was a huge shake-up that left lenders no choice but to tighten their rules and be far more careful. These days, things are a lot different. While borrowing money […]