- What Factors Affect Mortgage Approval?

- How to Improve Your Chances of Getting a Mortgage?

- Is It Hard for First-Time Buyers to Get a Mortgage?

- Getting a Mortgage With Bad Credit – Is It Possible?

- Is It Harder Getting a Buy-to-Let Mortgage?

- How About Getting a Second Home Mortgage?

- Can I Easily Remortgage to a Better Deal?

- The Bottom Line: Get Expert Help for an Easy Mortgage Journey

How Hard Is It To Get A Mortgage In The UK?

Looking to take that exciting next step and get on the property ladder? Or perhaps you’re already a homeowner but want to remortgage or buy an investment property.

Whatever your situation, the big question is–how hard will it be to actually get approved for a mortgage? 🤔

Don’t worry, in this comprehensive guide, we’ll cover everything you need to know about getting a mortgage in the UK.

From boosting your chances of approval to navigating the application process smoothly, consider this your go-to resource.

What Factors Affect Mortgage Approval?

Before we dive into the details, it’s important to know the key factors that lenders assess when you apply for a mortgage:

Your Deposit Size

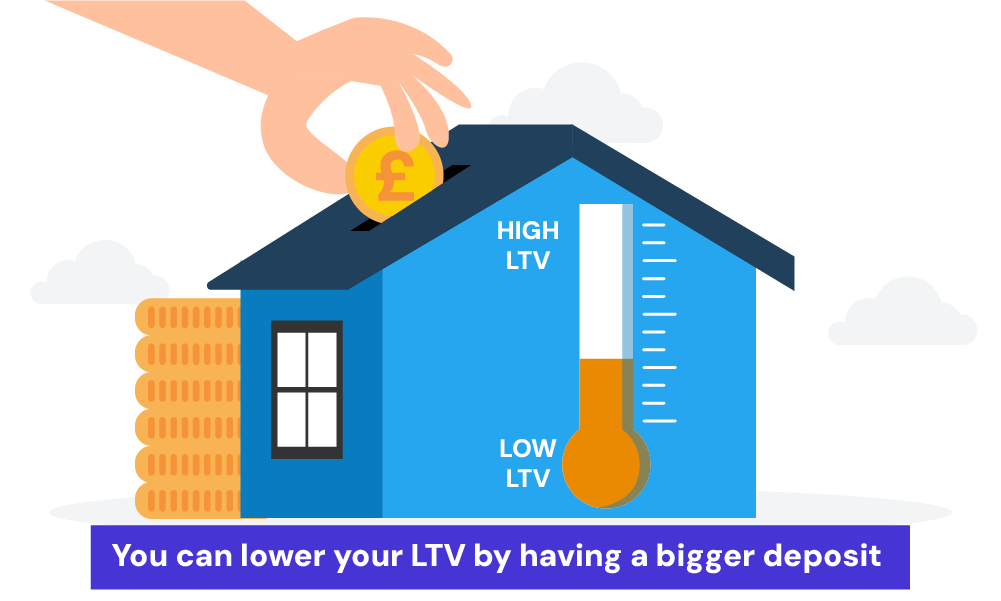

One of the most critical factors is the size of your deposit. Generally, the larger your deposit, the more favourable your mortgage terms will be.

Lenders use the loan-to-value (LTV) ratio to assess the risk of lending to you. A lower LTV ratio (meaning a larger deposit) is seen as less risky.

For example, a 20% deposit on a £200,000 property gives you an LTV of 80%.

Credit History

Your credit history plays a vital role in the mortgage approval process. Lenders will review your credit report to evaluate your financial reliability.

A good credit score can open the door to better mortgage rates, while a poor credit score might limit your options or result in higher interest rates.

It’s a good idea to check your credit report from agencies like Experian, Equifax, and TransUnion before applying.

Employment Status and Income

Stable employment and a steady income are key factors. Lenders want to ensure you can make your monthly payments without financial strain.

Typically, you’ll need to provide proof of income, such as pay slips or tax returns if you’re self-employed.

Having a consistent income stream over the past two years can significantly boost your application.

Debt-to-Income Ratio

Lenders assess your debt-to-income ratio to determine if you can handle the mortgage payments alongside your existing debts.

This ratio is calculated by dividing your total monthly debt payments by your gross monthly income.

A lower ratio indicates better financial health and increases your chances of approval.

Age

Age can affect your mortgage application in two ways.

Younger buyers can typically secure longer terms, which lowers their monthly payments. On the other hand, older applicants might face limitations on mortgage term lengths.

They may also need to show a strong repayment plan, especially if the mortgage stretches into their retirement years.

Since lenders want to be sure you can make payments after retirement, having a reliable source of income during that time is essential.

Property Type

The type of property you’re looking to buy can influence your mortgage approval.

Standard residential properties are generally easier to finance.

But if you’ve set your sights on something less conventional, like a historic building, a property with a short lease, or one built with unusual materials, lenders might be more wary.

These properties can be trickier to sell on and may require specialist surveys and higher deposits.

Overall, the stronger your overall financial profile, the easier your mortgage journey will be. But don’t get discouraged if some areas need work–there are tactics to improve your chances that we’ll cover.

How to Improve Your Chances of Getting a Mortgage?

Even if your situation is less than perfect on paper, there are smart ways to boost your chances of getting a mortgage. Here are some tips to boost your chances:

Build Your Credit Score. Your credit report and score are a huge part of a lender’s decision. Take time to get your credit in top shape. Here are some tips:

- Pay Bills on Time – Consistent on-time payments can improve your score.

- Reduce Outstanding Debt – Pay down existing debts to lower your debt-to-income ratio.

- Avoid New Credit – Don’t apply for new credit cards or loans close to your mortgage application date. Be cautious about new applications that result in hard searches.

- Check Your Credit Report – Review reports from Experian, Equifax, and TransUnion for errors and correct them promptly.

Increase Your Deposit. A larger deposit means borrowing less overall, improving affordability in the lender’s eyes. Even going from 10% to 15% could qualify you for better rates.

Use government schemes, get support from family, or keep saving if possible.

Consider setting up a dedicated savings account and automating your savings to build up your deposit faster.

Reduce Existing Debts. From car finance to credit cards – clear as much existing debt as possible before applying. This will lower your debt-to-income ratio and boost affordability calculations.

Register to Vote. Being on the electoral roll helps with identity checks and can improve your credit score. Register to vote if you haven’t already.

Correct Credit Report Errors. Check your credit report for errors and correct them immediately. Even small mistakes can impact your credit score and mortgage approval chances.

Avoid Major Financial Changes. Avoid significant financial changes before applying for a mortgage. Don’t make large purchases, take on new debts, or change jobs.

Manage Your Spending. Lenders will scrutinise your spending habits. Avoid excessive spending in the months leading up to your application. Show that you can manage your finances responsibly.

Close Unused Credit Accounts. Close old, inactive accounts to lower the risk of fraud and simplify your credit profile. However, keep older accounts with good histories open as they positively impact your credit score.

Consider a co-borrower. Having a spouse, partner or other co-borrower on the mortgage can increase your combined income and help qualify.

Speak to a Mortgage Broker. Brokers have in-depth knowledge of lenders’ criteria and the entire mortgage market at their fingertips. They’ll provide invaluable advice to place your application in the best possible light for approval.

The more ready you are for a mortgage, the easier you’ll find getting a mortgage. A little planning can save you time, money, and stress in the long run.

Is It Hard for First-Time Buyers to Get a Mortgage?

One of the most common questions–and for good reason!

Stepping onto the property ladder for the first time can feel like an uphill battle. The great news is lenders are very welcoming of first-time buyers in the current market.

Government schemes like the Mortgage Guarantee Scheme even allow you to buy with only a 5% deposit. There are also special deals from lenders for those who can’t save a large amount upfront.

As long as you have a steady income, reasonable credit score, and evidence you can afford the repayments – getting that first mortgage is achievable with the right preparation.

Here are some ways to make things even easier:

- Guarantor mortgages: This type allows someone to agree to cover your repayments if you can’t.

- Family springboard mortgages: A family member helps with a deposit using a secured loan against their own property.

- Joint application mortgages: Buy with someone else to share the deposit and mortgage.

- Shared ownership: You buy a share of a property and pay rent on the rest.

- Professional mortgages: Designed for certain professions like doctors or teachers, with special features.

- Low deposit mortgages

Getting a Mortgage With Bad Credit – Is It Possible?

Having bad credit can make it harder to get a mortgage in the UK, but it’s not impossible.

While high-street lenders may reject your application, specialist bad credit mortgage providers can still offer you competitive deals.

The application process may involve a stricter assessment of your finances and a bigger deposit, usually between 15% and 20%.

But with a mortgage advisor who knows bad credit mortgages, you can still become a homeowner.

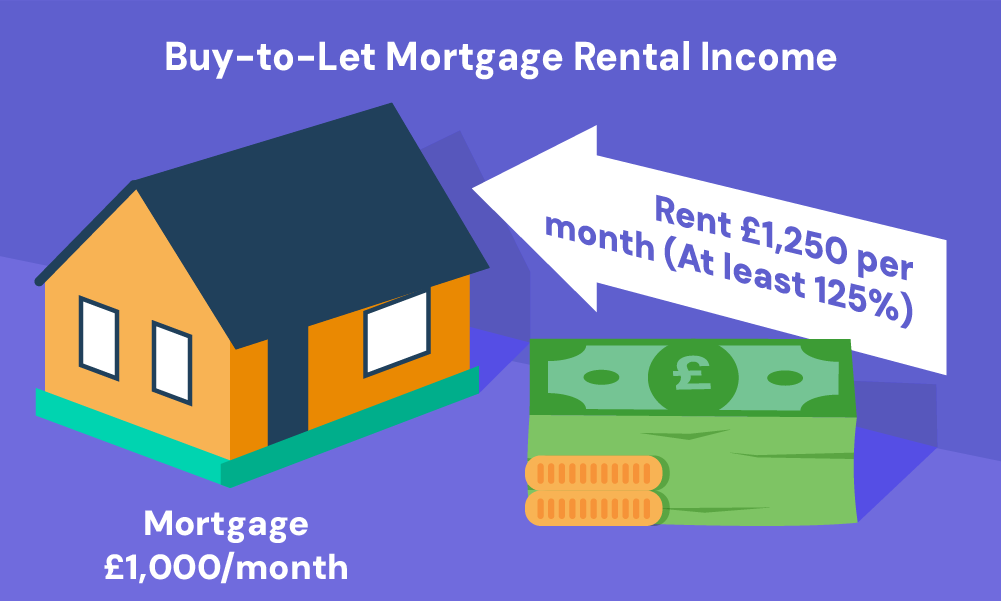

Is It Harder Getting a Buy-to-Let Mortgage?

Buying a property purely as an investment to rent out often comes with added hurdles compared to a typical residential mortgage.

Lenders view buy-to-let as higher risk, so their criteria around income, deposit, and interest rates tend to be stricter.

Most BTL mortgages require:

- A minimum 25% deposit

- Rental income to exceed monthly mortgage payments by 25-30%

- The applicant to already be a homeowner

While certainly possible with the right preparation, getting approved for a buy-to-let deal can be more of a challenge. Enlisting the expertise of a specialist broker is wise to fully understand your options.

How About Getting a Second Home Mortgage?

Getting a mortgage for a second home in the UK can be trickier than you might think.

Lenders will scrutinise your income, debts and overall ability to afford two mortgages. They want to be sure you can comfortably handle the repayments on both properties.

The process is much easier if you have a high income, excellent credit score, and a large deposit (at least 25%).

Even then, it’s always recommended to talk to a mortgage advisor to get the best deals.

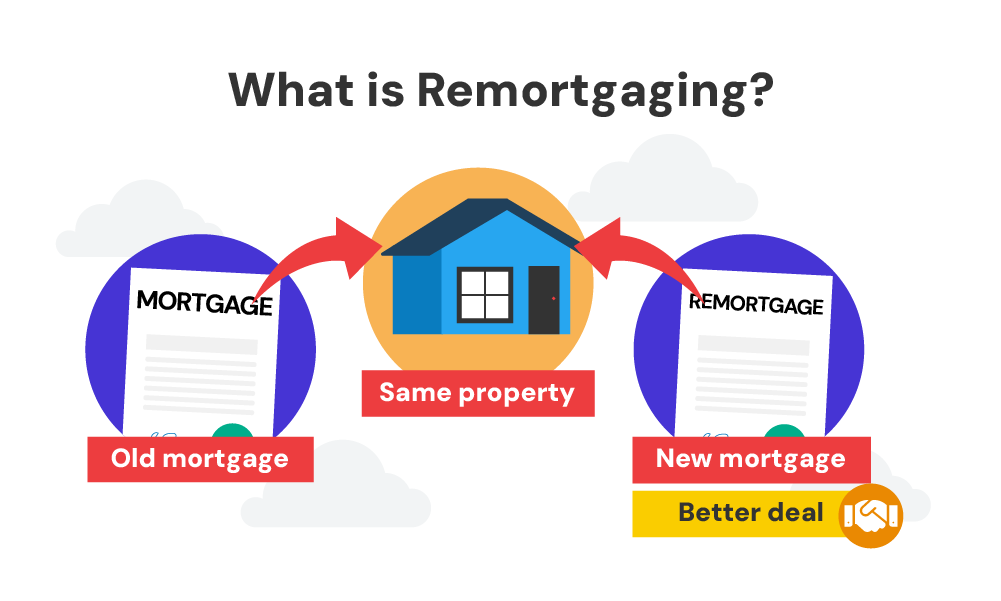

Can I Easily Remortgage to a Better Deal?

Remortgaging to a better deal can be a simple process, especially if you stay with your current lender.

You’ve already been approved for a mortgage with them, so getting a new deal at the end of your term usually involves minimal hassle.

The lender will check your income, credit score, and remaining mortgage balance again.

But as long as your financial situation hasn’t gotten considerably worse, approval should be straightforward.

Many people remortgage to get a lower interest rate or switch to a different type of mortgage. Here are some mortgage types to consider:

- Fixed-Rate offers stable payments as the interest rate stays the same for the agreed term.

- Tracker Mortgages follows the Bank of England’s base rate, which can rise or fall, affecting your payments.

- Discounted Variable has an interest rate set below the lender’s standard variable rate, changing when the SVR changes.

To find out how easy it could be to switch mortgage lenders, consider consulting a mortgage broker. They can guide you through the process and help you find the best deal.

The Bottom Line: Get Expert Help for an Easy Mortgage Journey

Getting a mortgage can be easier or trickier depending on your situation. Whether you’re a first-time buyer, remortgaging, or looking for a buy-to-let option, the requirements will differ.

But there’s good news, a mortgage advisor can simplify the entire process and help you get the best possible deal.

They’ll assess your finances and credit score, and then find the perfect lender for you. They’ll even guide you through your application from beginning to end.

Need a broker? Simply, get in touch. We’ll connect you with a qualified mortgage broker who can make mortgage approval easier.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Is it hard to get a mortgage if you’re self-employed?

Getting a mortgage when you’re self-employed can be challenging, but it’s definitely possible.

Lenders will want to see proof of stable income over at least two years. You’ll need to provide tax returns, bank statements, and possibly a statement from your accountant. A strong credit history and a substantial deposit can also improve your chances.

Using a mortgage broker can help find lenders who are more flexible with self-employed applicants.

Can you easily terminate a mortgage before its term ends?

Terminating a mortgage before its term ends, also known as early repayment, is possible but may incur early repayment charges (ERCs). These fees can be significant, depending on your lender and the terms of your mortgage agreement.

It’s important to check your mortgage terms and consult with your lender to understand any costs involved.

In some cases, switching to a different mortgage product with your current lender might be a better option.

How challenging is it to get a mortgage with a high LTV ratio?

Getting a mortgage with a high loan-to-value (LTV) ratio, such as 95% or higher, can be more challenging. Lenders see high LTV ratios as riskier since you have less equity in the property.

You’ll likely face stricter eligibility criteria and higher interest rates. To improve your chances, ensure your credit score is high, minimise other debts, and provide comprehensive documentation of your income.

How accessible are mortgages for purchasing land?

Getting a mortgage for land is trickier than a regular mortgage for a house. Land is seen as a riskier investment by lenders, particularly if it doesn’t have permission to build on it.

You’ll likely need a much bigger deposit, often 25% or more of the land’s value, and you might be facing higher interest rates too.

However, your chances improve if you have a clear plan for the land, like building houses with the proper permits already in place.

Is it simpler to get a small mortgage compared to a larger one?

Yes, it is generally simpler to get a small mortgage compared to a larger one. Lenders see smaller loans as less risky because the monthly repayments are more manageable.

However, the approval process still depends on your overall financial situation, including your credit score, income, and existing debts.

Ensure you have a good credit history and stable income to increase your chances of getting approved for a small mortgage.

Why is it too hard to get a mortgage in the UK?

Getting a mortgage in the UK can be hard due to several factors. Lenders have strict criteria to ensure borrowers can afford repayments.

They assess your credit history, income, debt levels, and employment stability. High property prices also mean larger deposits are required, which can be challenging to save.

Economic factors and regulatory requirements also play a role. Improving your financial situation and seeking advice from a mortgage broker can help navigate these challenges.

What is the hardest part of getting a mortgage?

The hardest part of getting a mortgage is often meeting the lender’s affordability and credit criteria. Lenders scrutinise your income, employment history, debt levels, and credit score.

Saving for a large enough deposit can also be challenging, especially with high property prices. Additionally, the extensive paperwork and documentation required can be daunting.

What are my chances of getting a mortgage?

Getting a mortgage approval depends on a few things:

- your credit score

- how steady your income is

- how much debt you have

- how big of a deposit you saved

A strong credit score and a reliable income make it much more likely you’ll be approved. Paying down some debt and saving a bigger deposit can also improve your chances.

A mortgage broker can help you find lenders that match your financial situation, which can give you an extra edge.

Since every lender has different requirements, it’s important to shop around and be well-prepared before applying.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]