- Can You Buy a Business with a Mortgage?

- Types of Commercial Mortgages

- Can You Get a Mortgage for Any Business?

- Who Can Apply?

- How Much Can You Borrow?

- What Are the Costs Involved in Securing a Business Mortgage?

- Should You Buy a Business with Commercial Mortgages?

- Steps To Get a Mortgage For a Business

- Alternatives to Business Mortgage Loans

- The Bottom Line

Mortgages For Businesses: A Simple Guide

Owning a space for your business can turn your dreams into reality. Yet, the journey to financing that dream is a different tale.

If you’re running a business, chances are you’ve stumbled upon this article for several reasons:

- To buy a new place to expand your operations;

- To move from renting to owning, and save money in the long run; or

- To buy properties as an investment, with plans to rent it out and earn cash.

In any case, you want to use a mortgage to buy a business. And that’s exactly what this guide will walk you through.

Let’s get started.

Can You Buy a Business with a Mortgage?

Yes, in the UK, you can use a “commercial mortgage” or business mortgage to buy a business.

These loans help you purchase, improve, or refinance properties or land for business use.

Unlike personal mortgages, this one is for properties used mainly for business. It helps businesses afford their own space without paying the full price upfront.

You pay back the loan, plus interest, over time. This way, your business can have a home, and you might even save money compared to renting.

And if you wonder whether you can get a residential mortgage for your business.

The short answer is it depends on what you’ll use the property for.

If it’s for business, like renting out apartments, then yes. But you can’t use it to buy a personal home through your business.

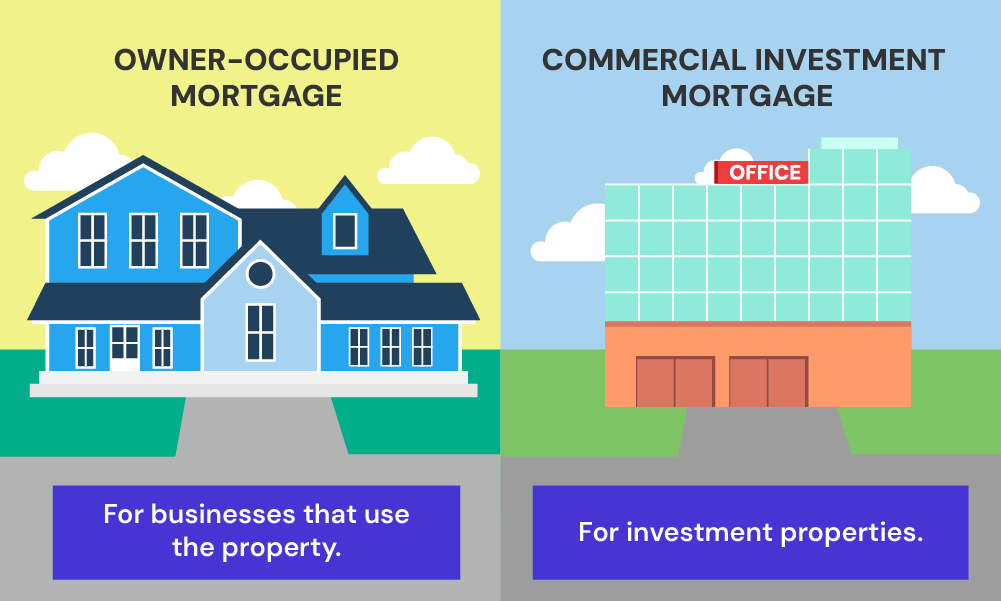

Types of Commercial Mortgages

Commercial mortgages come in two main forms: owner-occupied mortgages and commercial investment mortgages.

- Owner-occupied mortgage. This option is for buying premises where your business will be based. It’s suitable if you’re looking to acquire a space for your shop, office, or manufacturing site.

- Commercial investment mortgage. This option is geared towards those interested in property as an investment opportunity rather than a business base.

In both cases, the idea is to invest in property. Your decision hinges on whether the property will serve as the heart of your business or as a source of rental revenue.

Can You Get a Mortgage for Any Business?

The answer to this depends on three things – your business type, property type, and your lender’s criteria.

But, generally, any business property can be acceptable, this includes:

- Retail shops

- Office spaces

- Warehouses

- Schools or colleges

- Hotels or guesthouses

- Restaurants and cafes

- Apartments

- Agricultural property such as farm buildings/land

- Professional properties – solicitors, medical centres

- Special-purpose buildings like schools or nursing homes

Every business has its unique charm, and so does the property it occupies. As long as it’s a tangible property tied to your business goals, there’s a good chance it can be financed.

Who Can Apply?

Anyone who meets the lender’s eligibility criteria. Here’s what lenders typically look at:

- You must have a solid business plan.

- Your business should be earning a steady income to show you can afford the mortgage payments.

- A healthy credit history to prove you’re a reliable borrower.

- Proven business experience in your industry to show you can handle fluctuations in the business.

- Your business’s projected income shows that you can afford the loan in the long run.

- A deposit, usually 20% to 40% of the loan’s value.

- Your business earns income from renting out property that boosts your overall cash flow. (not required)

Remember, each lender has its own rules, but these are the common threads. If you tick these boxes, you’re on your way to getting that mortgage for your business.

How Much Can You Borrow?

There’s no one-size-fits-all answer.

It boils down to a few key things: your financial health, the property you’ve got your eye on, how solid your business plan is, your deposit size, and what the lender’s looking for.

First, your financial health. Lenders dive deep into your business’s numbers.

They’re looking to see if your earnings can comfortably cover the mortgage repayments, with room to spare. This includes scrutinising your profits, outgoings, and any existing debts.

Second, the type of property you want to buy. Lenders evaluate its market value and potential resale ease. Prime locations and well-maintained properties are more likely to secure higher loan amounts.

Your deposit size also affects your mortgage amount. A big deposit reduces the lender’s risk, often leading to them offering you more favourable terms and loan amounts.

Another factor is how likely is your business to succeed. Lenders love a good, strong business plan.

They want to know your business is on solid ground and has a bright future. The better your plan, the more they might be willing to lend.

Finally, every lender has their own playbook for loan amounts. Some might be more generous, while others are more cautious.

It often comes down to their assessment of the risk involved.

If you’re looking to borrow the full value of the property, you might need to offer extra security to cover the lender’s risk.

To calculate your potential repayments and total loan cost, use an online mortgage calculator. Plug in your loan amount, interest rate, and term length, and it’ll give you an estimate of your monthly repayments and total cost over the life of the mortgage.

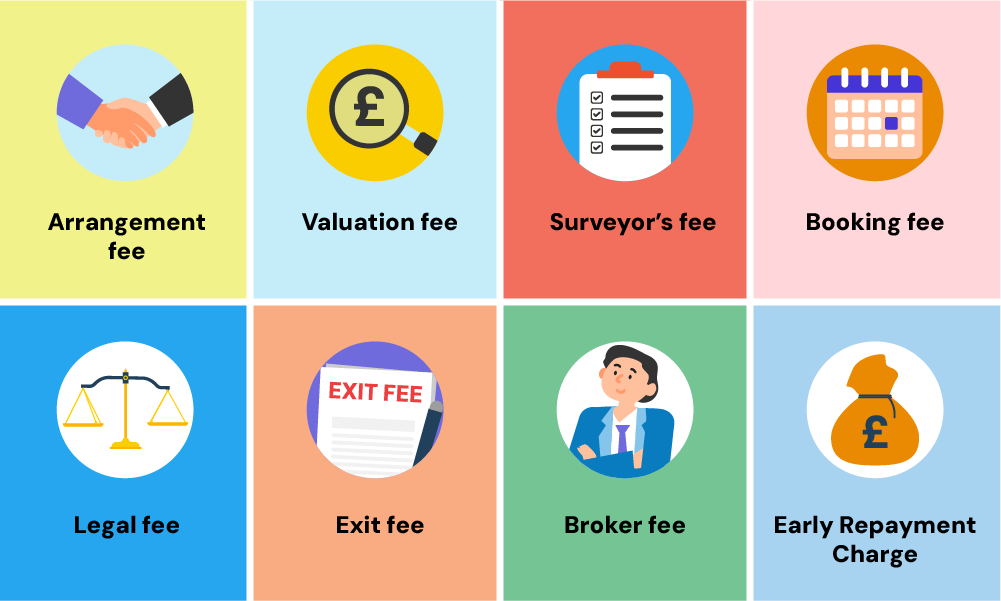

What Are the Costs Involved in Securing a Business Mortgage?

Every penny counts in business. Understanding these costs helps you plan better and ensures you find a mortgage that fits your business’s needs and budget.

Here’s a breakdown of the fees involved:

- Arrangement Fee – Lenders charge this for setting up your mortgage. It’s often 1% to 2% of the loan amount, sometimes payable upfront or added to your mortgage balance.

- Valuation Fee – This covers the lender’s cost to assess the property’s value. It can range from £500 to £1,500, depending on the property size and complexity. This fee is usually paid upfront.

- Legal Fees – You’ll need to cover the cost for a solicitor to manage the legal aspects. Expect to pay between £500 and £5,000, significantly varying based on transaction complexity. This is paid upfront.

- Surveyor’s Fee – If a detailed survey is needed, it could cost you from £400 to over £1,000, paid upfront. This fee ensures the property’s condition is thoroughly evaluated.

- Booking Fee – Some lenders might ask for a booking fee to lock in a mortgage deal, typically around £100 to £250, paid upfront.

- Early Repayment Charge – Paying off your mortgage early might incur a charge, often a percentage of the loan amount. This can vary widely, so check with your lender.

- Broker Fee – Using a mortgage broker might add a fee of £500 to £1,000 to your costs, though some brokers are paid via commission from the lender instead.

- Exit Fee – When you pay off your mortgage or switch to another lender, an exit fee of around £100 to £300 may apply.

Should You Buy a Business with Commercial Mortgages?

Yes, if the benefits align with your goals and you’re aware of the risks. Here’s a look at what this means for you:

Pros

– Owning your space means not worrying about rent hikes.

– Property could increase in value, giving you an extra asset.

– Mortgage interest might lower your tax bill.

– Knowing your monthly payments helps with budgeting.

– More borrowing power than many business loans, with lower interest rates.

– The option to generate income by leasing unused space.

– The possibility to release equity for business investment by remortgaging.

– Selling the property is an option if your business needs to change.

Cons

– Struggling to pay the mortgage can lead to losing the property.

– Upfront costs like fees and deposits are high.

– All repairs and maintenance are on you.

– If property values dip, so does your investment.

– Your cash could be tied up, limiting liquidity for other business needs.

– The process can be longer and involve more fees than renting.

Steps To Get a Mortgage For a Business

To get a mortgage for your business, here’s what you can do:

1. Partner with a Commercial Mortgage Advisor

Commercial mortgage advisors can make all the difference. They don’t just help you fill out paperwork; they:

- Offer expert advice tailored to your business needs.

- Explain complex terms in simple language.

- Help find the best rates and terms for you.

- Negotiate with lenders on your behalf.

- Save you time and stress by dealing with lenders and paperwork.

2. Prepare Your Application

A solid application is key to success. Here’s what you need:

- A Strong Business Plan

- Financial Statements (Last 2-3 Years) such as profit and loss statements and cash flow details.

- Tax Returns (Personal and Business, Last 2-3 Years)

- Recent Bank Statements (Last 6-12 Months)

- Property Details showing the location, size, and revenue potential.

- Credit Reports (Personal and Business)

- Assets and Liabilities

- Deposit Proof

Note: not all lenders are the same. Some might offer better rates for your particular business or have more favourable terms. So make sure to shop around or let your broker do the hard search for you.

3. Apply With Your Broker

Once everything is ready, your broker submits your application. Their expertise means:

- Your application showcases your business in the best light.

- You avoid common pitfalls that could delay or derail your application.

- You have a better chance of approval, thanks to their negotiation skills.

Alternatives to Business Mortgage Loans

Besides commercial mortgages, you can also consider other options. Let’s explore some alternatives:

- Bridging Loans – For a quick purchase for an auction, or to outbid competition, bridging loans fill the gap. These loans offer fast funding to buy a property before you sell another asset or secure long-term financing like mortgages. This is usually payable in 12-36 months.

- Unsecured Business Loans – This is ideal for needs under £25,000. This option can get you the funds without tying down your assets. It’s a fit for when you’ve got some capital but just need that extra push to seal the deal.

- Remortgaging for Business Finance – If you already own property, remortgaging can free up cash for your business. A good option if you have equity and want lower interest rates.

These options might fit better if you need flexibility, don’t have property to use as security, or are in between property transactions.

The Bottom Line

It’s important to look at the big picture and consider all your options.

Getting advice from a commercial mortgage broker can help you make a well-informed decision. They can offer personalised advice based on your specific circumstances.

Don’t rush into anything. Take your time, do your homework, and team up with professionals. With the right approach, you’ll find the best financial solution for your business.

Unsure where to start? Get in touch with us. We’ll arrange a quick, free, and no-obligation call with a commercial mortgage broker experienced in helping business owners looking to buy a space for their businesses.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I use a business mortgage to buy a house for mixed-use?

Yes, you can. If you plan to use part of the house for business and the rest for living, a part commercial mortgage is what you need. Just make sure to explain your plan to the lender.

Related Articles

Can You Change From Commercial Mortgage To Residential?

Since 2015, it’s been easier to switch your mortgage from commercial to residential, all thanks to the UK government’s major changes to the General Permitted Development Order (GPDO). These rules have simplified changing a building’s use from commercial to residential, offering developers more opportunities to turn unique business spaces into homes. You might be considering […]

Should You Get A Semi-Commercial Mortgage? A Guide

If you want to own a building with a shop on the ground floor and flats above, you’re the perfect candidate for a semi-commercial mortgage. This option is also great for investors looking to buy such mixed-use properties and for developers aiming to create spaces that blend living and commercial areas. Curious? This article explores […]

How To Buy A Pub With Commercial Mortgages? A UK Guide

Pubs are more than just places to drink. They’re the soul of British culture – a haven where locals gather to unwind, celebrate, or simply enjoy a quiet pint after a long day. For anyone dreaming of swapping their office view for the behind-the-bar camaraderie, the idea of running a pub might sound like the […]