- What Are Commercial Mortgage Rates?

- What Factors Influence Commercial Mortgage Rates?

- How Do Fixed and Variable Rates Differ?

- How To Know If I Can Afford a Commercial Mortgage?

- What Are My Repayment Options?

- What Fees Should I Expect?

- How Do I Apply for a Commercial Mortgage?

- How Do I Get the Best Commercial Mortgage Rate?

- Key Takeaways

- The Bottom Line

How Commercial Mortgage Rates Work: A Full Guide

When considering mortgages, it’s always important to compare rates and do proper research.

After all, mortgages are huge commitments. You don’t want to end up with the wrong deal, especially for your business.

As much as possible, you want to find the best rate that can save you a lot of money over time.

In this guide, we’ll explore everything you need to know about commercial mortgage rates – from how they’re determined to ways to get the best rates for your business.

What Are Commercial Mortgage Rates?

Commercial mortgage rates are the interest you pay on a loan to buy business property.

Generally, these rates vary between 2% and 12% above the Bank of England Base Rate each year, influenced by a mix of factors.

For example, if the Bank of England Base Rate is at 5.25%, and you’re looking at a commercial mortgage rate of 2% above this base rate, your total interest rate would be 7.25% annually.

This percentage might vary based on how lenders assess the risk and value of your property.

In addition, several factors determine the rate you get. This includes:

- The credit scores of your company and its directors.

- The financial health of your busine ss and the amount you need to borrow.

- The sector your business operates in.

- The specific requirements set by your lender.

- How quickly you need access to the funds.

- The condition and location of the property you intend to purchase.

- Whether you’re offering collateral and the terms of repayment.

It’s important to understand these factors. This way, you can work towards securing a better rate for your business mortgage.

What Factors Influence Commercial Mortgage Rates?

Several key factors can affect the interest rate you’re offered on a commercial mortgage:

Credit Score

Having a high credit score, especially over 700, makes a big difference. You’re seen as less risky and can get lower rates.

But, don’t worry if your score isn’t perfect. Some lenders specialise in helping businesses with lower scores, though you might pay more.

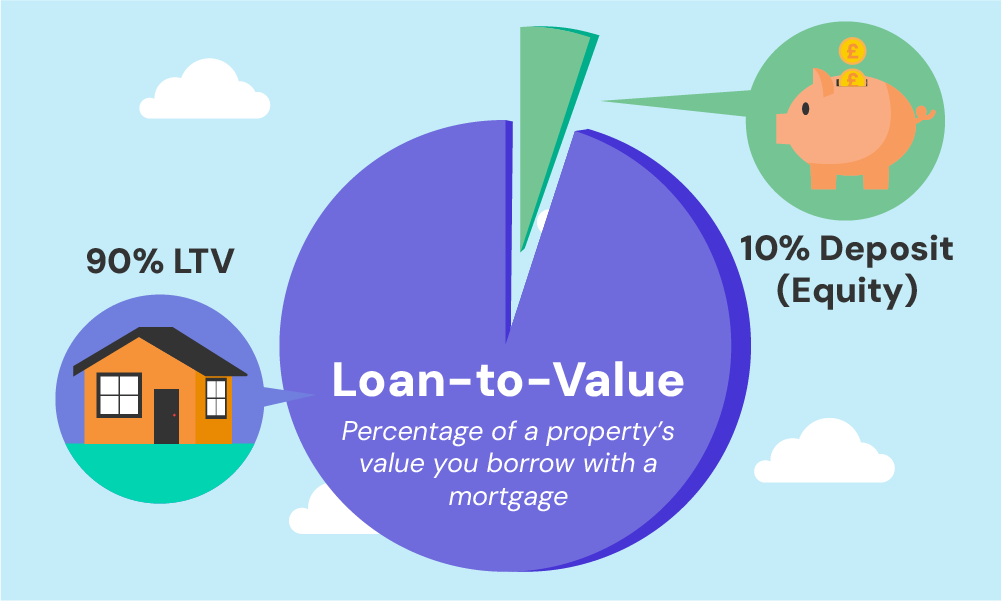

The loan-to-value ratio is critical. Aim to keep this ratio as low as possible, ideally below 75%. The less you need to borrow in proportion to the property’s value, the better the rates you’re likely to get.

Loan Term Length

The length of your loan can also affect your rate. Shorter loan periods typically attract lower interest rates since the lender’s money is at risk for a shorter time.

On the flip side, loans extending beyond 25 years usually come with higher rates due to the increased risk to the lender over time.

Property Value and Location

The value of your property and where it’s located can affect your rate. High-value properties or those in sectors seen as less risky, like industrial, generally get better rates.

Properties in top locations, such as London, also tend to secure lower rates compared to those in rural areas.

Property Type

The kind of property you’re financing plays a role too. Industrial properties might get lower rates, while retail spaces are often seen as higher risk.

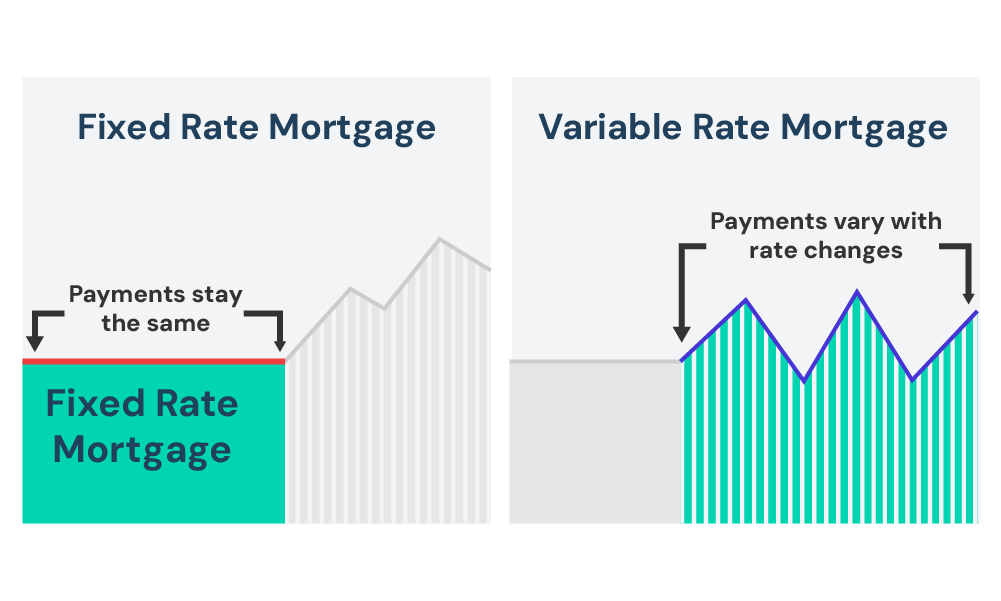

How Do Fixed and Variable Rates Differ?

Fixed rates offer predictability. If you choose a fixed rate, your interest rate stays the same for a set period. This makes planning your finances easier because your payments won’t change.

Pros

- Predictable payments can give you peace of mind

- Easier budgeting

- Protection against interest rate rises that affect variable rates.

Cons

- More expensive than variable-rate mortgages

- You may be stuck with the higher rate if interest rates fall

- You’ll usually have to pay an early repayment charge if you switch to another mortgage deal before your current deal ends.

Variable rates, on the other hand, are flexible. They can go up or down based on the lender’s standard variable rate.

This means your payments could change over time. If rates go down, you pay less. But if they go up, you’ll pay more.

Pros

- Less expensive than fixed-rate mortgages

- Pay less if interest rates are particularly low

- Less likely to have early repayment charges, so if you want to switch mortgage deals or pay in advance, you won’t be charged for doing so.

Cons

- Uncertainty.

- Paying more if interest rates are high

For businesses, the choice between fixed and variable rates depends on your appetite for risk and your financial stability.

How To Know If I Can Afford a Commercial Mortgage?

To determine if you can afford a commercial mortgage, you get an Agreement in principle (AIP) from a lender to know your options.

This is not a guaranteed offer, but it helps you plan better and show that you’re serious about buying a property.

Additionally, lenders evaluate your business’s income and the property’s potential rental earnings.

They apply metrics known as income multiples and interest cover ratios to make this assessment.

For instance, if a lender uses an income multiple of 5x and your business earns £100,000 annually, you could potentially borrow up to £500,000.

Meanwhile, an interest cover ratio (ICR) compares your rental income to your interest payments.

If your potential rental income is £50,000 a year and the mortgage interest payments are expected to be £25,000, your ICR would be 2x, indicating you earn twice as much as you need to cover the interest, which makes you a more appealing borrower.

As a rough guide, use the calculator below to get an initial idea of your potential mortgage costs.

[EMBEDDED COMMERCIAL CALCULATOR]

While calculators give you a quick snapshot, they have limitations. They might not include all fees or reflect the exact rates you’ll get.

That’s why it’s important to also seek expert advice. A mortgage broker can provide insights beyond what a calculator shows. They can help you understand the full scope of your costs and options.

What Are My Repayment Options?

You can choose between paying back your mortgage in two main ways: repayment or interest-only.

Repayment Mortgages

With this choice, you chip away at both the loan and interest each month. This method means your debt gets smaller over time, leading to a clear endpoint when you’ve paid off everything.

The catch is that monthly payments are higher compared to the interest-only option.

Interest-Only Mortgages

For this option, you only cover the interest each month. This keeps your monthly costs down, but you’ll need a solid plan to pay off the loan’s balance when the term ends.

You might plan to sell the property or use other funds to clear the debt. It’s crucial to think this through to keep things affordable.

Flexible Options

- Roll-Up Mortgages – Best for properties you’re fixing up, this option lets you add the interest to the loan’s balance and pay it all at the end. It’s a way to keep cash flow steady while you’re developing the property.

- Offsets – If your mortgage has this feature, the rent you earn can directly lower your interest payments each month. This is handy for managing your money, especially with good rental income.

The length of your mortgage also affects how much you pay monthly and the interest rate you get.

Shorter mortgages (10-15 years) usually mean higher monthly payments but lower interest rates. Longer ones (up to 25 years) can lower your monthly payments but cost you more in interest over time.

What Fees Should I Expect?

When you get a commercial mortgage, you’ll pay more than just the interest. Common fees include:

- Arrangement Fee – Lenders charge this for setting up your mortgage. It’s often 1% to 2% of the loan amount, sometimes payable upfront or added to your mortgage balance.

- Valuation Fee – This covers the lender’s cost to assess the property’s value. It can range from £500 to £1,500, depending on the property size and complexity. This fee is usually paid upfront.

- Legal Fees – You’ll need to cover the cost for a solicitor to manage the legal aspects. Expect to pay between £500 and £5,000, significantly varying based on transaction complexity. This is paid upfront.

- Surveyor’s Fee – If a detailed survey is needed, it could cost you from £400 to over £1,000, paid upfront. This fee ensures the property’s condition is thoroughly evaluated.

- Booking Fee – Some lenders might ask for a booking fee to lock in a mortgage deal, typically around £100 to £250, paid upfront.

- Early Repayment Charge – Paying off your mortgage early might incur a charge, often a percentage of the loan amount. This can vary widely, so check with your lender.

- Broker Fee – Using a mortgage broker might add a fee of £500 to £1,000 to your costs, though some brokers are paid via commission from the lender instead.

- Exit Fee – When you pay off your mortgage or switch to another lender, an exit fee of around £100 to £300 may apply.

These fees can add a lot to the total cost of your mortgage.

To keep costs down, compare fees from different lenders and ask if any can be reduced or waived. Understanding these fees helps you see the true cost of your mortgage.

How Do I Apply for a Commercial Mortgage?

Applying for a commercial mortgage involves several steps:

- Get Your Finances in Order. Lenders will look at your business’s financial health. Make sure your accounts are up to date and reflect your business accurately.

- Know What You Need. Understand how much you need to borrow and why. This helps lenders see you have a clear plan.

- Gather Required Documentation. You’ll need financial statements, business plans, and details about the property. Having these ready speeds up the process.

- Property Valuation. The lender will assess the property’s value. This ensures the loan amount is appropriate for the property’s worth.

- Credit Checks and Affordability Assessment. Lenders will check your credit score and assess if you can afford the loan. They look at your income and how the property will generate money.

- Application Submission. With everything in place, submit your application. Include all required documents and any additional information the lender needs.

Getting everything ready and understanding what lenders are looking for makes the application process smoother.

It shows you’re serious and well-prepared, which can help your chances of approval.

>> More about Commercial Mortgages

How Do I Get the Best Commercial Mortgage Rate?

To land a great rate on your commercial mortgage, it’s important to have a robust application.

Ensure your business’s financial health is well-documented, showing off your strong revenue and credit history.

Here’s how you can further improve your chances:

- Boost Your Deposit. Aim for a deposit covering 25-30% of the property’s value. This reduces your loan-to-value ratio, presenting you as a safer bet to lenders.

- Check Your Credit. As a company director, ensure your credit is excellent, ideally above 750, as it influences the rates you receive.

- Research Broadly and Wisely. Explore options across high street and specialist lenders to find the best terms, as each operates with different lending criteria.

- Choose the Right Rate. Decide if a fixed or variable rate best suits your business. Fixed rates offer stability, whereas variable rates can reduce costs when interest rates fall.

- Seek Out Incentives. Look for lenders providing perks, such as free property valuations or legal services, to reduce mortgage costs.

- Prepare Your Documentation. Gather all necessary paperwork, like business accounts and tax forms, beforehand to expedite the application process.

- Consult a Broker. Engage a commercial mortgage broker for expert advice and access to exclusive deals, enhancing your chance of securing a favourable rate.

Key Takeaways

- Commercial mortgage rates depend on things like your credit score, how much of the property’s price you can pay upfront, and the type of property you want to buy. Lower risk means better rates.

- Fixed rates stay the same, so your payments don’t change, while variable rates can go up or down depending on the market. Pick what works best for your budget.

- To get a good deal, save up a bigger deposit, keep your finances in good shape, and ask a mortgage expert for help finding the best options.

The Bottom Line

Commercial mortgages help your business grow. They let you buy or expand property without spending all your cash. This frees up money for other growth activities, like marketing or developing new products.

For example, a shop could open a second location, or a factory might buy a bigger warehouse to make more goods. Actions like these can greatly increase your business’s success and earnings.

However, the process to secure these mortgages can be complex.

Luckily, you don’t have to do it alone.

Specialist commercial mortgage brokers have deep knowledge of the mortgage market and can offer personalised advice based on your business’s unique needs.

Mortgage brokers can save you time and money. They compare rates from multiple lenders, helping you find the best deal. They also understand the intricacies of commercial mortgages, which can be essential for getting favourable terms.

Need help in finding the right broker? Get in touch with us. We’ll arrange a free, no-obligation consultation with a good commercial mortgage broker to help you get started.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Are commercial mortgage rates always higher than residential mortgage rates?

Yes, typically. Commercial mortgages usually have higher rates because they’re considered riskier by lenders. This is due to factors like the potential for variable income from the property and the complexity of assessing business finances.

Can I switch my commercial mortgage to another lender for a better rate?

Absolutely. Just like with residential mortgages, you can remortgage to take advantage of better rates or terms offered by another lender. But, be mindful of any early repayment charges or fees that might apply when switching.

How often do commercial mortgage rates change?

Commercial mortgage rates can change often, influenced by factors like the Bank of England’s base rate, market conditions, and changes in the economy. Fixed-rate mortgages lock in your rate for a set period, while variable rates can fluctuate, reflecting these changes.

Is it harder to qualify for a commercial mortgage compared to a residential mortgage?

It can be, mainly because the assessment process is more complex. Lenders will look closely at your business’s financial health, the property’s potential to generate income, and your business plan, among other factors.

Can I get a commercial mortgage with a low deposit?

It’s possible, but a lower deposit usually means a higher interest rate and may limit your lender options. Most lenders prefer a loan-to-value (LTV) ratio of 75% or lower, meaning you should aim to provide at least a 25% deposit for the best rates and terms.

Do I need a business plan to get a commercial mortgage?

Yes, most lenders will want to see a solid business plan. It should detail your business’s current financial state, how you plan to use the property, and how you anticipate it will contribute to your business’s growth. This reassures lenders that you have a clear strategy for repaying the mortgage.

Are there fixed-rate commercial mortgages?

Yes, fixed-rate options are available for commercial mortgages, offering stability by locking in your interest rate for a set period. This can be particularly beneficial for budgeting and financial planning in the early years

Related Articles

Can You Change From Commercial Mortgage To Residential?

Since 2015, it’s been easier to switch your mortgage from commercial to residential, all thanks to the UK government’s major changes to the General Permitted Development Order (GPDO). These rules have simplified changing a building’s use from commercial to residential, offering developers more opportunities to turn unique business spaces into homes. You might be considering […]

Should You Get A Semi-Commercial Mortgage? A Guide

If you want to own a building with a shop on the ground floor and flats above, you’re the perfect candidate for a semi-commercial mortgage. This option is also great for investors looking to buy such mixed-use properties and for developers aiming to create spaces that blend living and commercial areas. Curious? This article explores […]

How To Buy A Pub With Commercial Mortgages? A UK Guide

Pubs are more than just places to drink. They’re the soul of British culture – a haven where locals gather to unwind, celebrate, or simply enjoy a quiet pint after a long day. For anyone dreaming of swapping their office view for the behind-the-bar camaraderie, the idea of running a pub might sound like the […]