- What is Build to Let Mortgage?

- How Does Build to Let Finance Work?

- Who is Build to Let Finance For?

- Types of Build to Let Finance

- Eligibility Criteria for Build to Let Finance

- Documents for Your Build to Rent Finance Application

- Pros and Cons of Build to Rent

- What You Must Know Before Opting for Build to Rent Financing

- Other Avenues to Explore in Build to Let Investments

- Key Takeaways

- The Bottom Line

How To Invest In The UK Market With Build To Let Mortgages?

You might’ve heard that property can offer solid returns over the long term. But here’s the catch—how do you finance such a venture without breaking the bank?

If that’s a puzzle you’re trying to solve, you’ve come to the right place.

This guide aims to shed some light on that very dilemma. We delve deep into the Build to Let mortgages, examining the pros, the cons, and the essentials in between.

Whether you’re a seasoned investor or a newcomer keen to dip your toes in the property market, get ready for a crash course that could change the way you look at real estate investments in the UK.

What is Build to Let Mortgage?

A Build to Let mortgage is a special loan for property developers who want to build homes or flats to rent out.

In simple terms, it’s a loan that helps you pay for the land and the cost of building the property from scratch.

The goal isn’t to sell the property once it’s built—it’s to keep it and earn steady rental income over time.

It’s a bit like a Buy to Let mortgage, but instead of buying an existing house to rent out, you’re building the property yourself.

This makes it a great choice for bigger projects, like blocks of flats or housing estates, where you can design everything to fit what renters want.

How Does Build to Let Finance Work?

First, you apply for the loan, providing all the essential details like your project plan, estimated costs, and projected rental income. The lender then takes some time to evaluate the project. They’ll look at your experience, your financial situation, and how profitable your project could be.

Once you get the green light, you and the lender agree on the terms. This includes how much you’ll borrow, the interest rate, and how you’ll pay it back.

Funds are then released in stages, aligned with key milestones of your project. For instance, you might get an initial sum for buying the land and later disbursements as construction progresses.

When your property is up and running and you start collecting rent, that’s when you begin repaying the loan.

Many developers use the rental income itself to make these repayments. Eventually, you’ll either sell the property to pay off the loan in a lump sum or switch to a long-term mortgage, which often has a lower interest rate.

Both of these options help you transition from being a developer to becoming a landlord with a consistent income stream. It’s a clever way to build your property portfolio while also securing a steady cash flow.

Who is Build to Let Finance For?

Build to Let Finance mainly suits professional property developers and landlords. If you’re planning to build multiple properties for the rental market, this is for you.

It also acts as a useful bridging solution, covering your development costs until your tenants start paying rent. So, in a nutshell, it offers a financial cushion from the start of your project to the point where you’re earning regular rental income.

Types of Build to Let Finance

When it comes to Build to Let Finance, one size doesn’t fit all. You can choose from various types based on your specific needs and the kind of property you’re developing.

Here are the three main categories:

- Residential Build to Let Finance. This is for you if you’re building residential properties like single-family homes, flat blocks, or larger housing estates. This loan covers your building costs and you start repaying it once you’ve got tenants and the rent is coming in.

- Commercial Build to Let Finance. If you’re focused on commercial spaces like offices, shops, or industrial buildings, this is your go-to option. The loan covers your construction costs, and you’ll start repayments when your commercial spaces are leased.

- Mixed-Use Build to Let Finance. For those complex projects that feature both residential and commercial spaces—think flats above a row of shops—this is your best bet. This finance type is flexible, combining aspects of both residential and commercial loans, and again, you’ll start repaying it once your properties are occupied and generating income.

Eligibility Criteria for Build to Let Finance

If you’re thinking about trying Build to Let Finance, there are a few things you’ll need to check off your list to get approved by lenders. The better prepared you are, the higher your chances of success.

First, it helps if you’ve already got experience as a property developer or landlord. Lenders aren’t impressed by vague ideas—they want solid rental projections and a clear business plan.

Next, your project plan needs to be detailed and well-thought-out. Lenders aren’t impressed by vague ideas—they want solid rental projections and a clear business plan.

You’ll also need planning permission sorted before lenders even look at your application. It’s a must-have for getting started.

When it comes to money, most lenders will expect you to have a deposit of at least 25% to 40% of the project’s cost.

A bigger deposit can make your application stronger, but some lenders might even offer full financing if you can use other assets, like property, as security.

Finally, your credit score doesn’t need to be perfect, but it shouldn’t cause any red flags. A good score can make the process much smoother.

Documents for Your Build to Rent Finance Application

When you’re getting ready to apply for Build to Rent finance, paperwork is a big part of the process. Lenders need to see specific documents to gauge whether you’re a good fit for a loan.

Here’s a quick list of what you’ll generally need:

- Comprehensive Business Plan – Your business plan should detail what you aim to achieve with your development project. It should include cost estimates, timelines, and how you plan to manage the development.

- Financial Forecasts – This should outline your projected income from the rental properties, as well as any other relevant financial information.

- Past Experience – Lenders like to see a track record of successful projects. Provide details of your past developments or property management experience.

- Property Information – Details about the property or properties you plan to develop, including location, size, and planning permissions, can be crucial for your application.

- Exit Strategy – You need a clear plan for how you intend to repay the loan. Whether it’s through rental income, selling the properties, or another method, make it clear.

- Tenant Information – If the property is pre-let, offering details about your tenants can bolster your application. Lenders use this information to gauge whether your project will meet the criteria for buy-to-let or commercial mortgages.

Each lender may have their unique set of document requirements. So, it’s a good idea to check what you’ll need before diving into the application process. This way, you’re not caught off guard and can gather everything you need in advance.

Pros and Cons of Build to Rent

Like everything, Build to Rent has its good and bad sides. Let’s break it down:

Pros

- Steady Money Coming In. With long-term rentals, you can count on steady income. It’s a great way to invest and build financial security.

- Help from the Government. Some lenders offer access to government schemes, which can make it easier and less stressful to get started.

- Improves Neighbourhoods. Build to Rent projects can make areas look better and increase property values, benefiting both you and the community.

- Lower Upfront Costs. Some lenders might cover most of the project, so you won’t need to put in a huge amount of money upfront.

Cons

- Harder to Sell Later. Big rental properties can be tough to sell later. This means you’ll need to commit for the long term, and it could take a while to see big profits.

- Expensive to Start. Getting started can be pricey. If you don’t have access to the right loans, it can be hard to find the money to begin.

- Complicated Loans. Build to Rent loans often come with tricky conditions and fees. If you don’t fully understand the details, it could cost you more in the long run.

- Not Many Lenders. Many regular banks don’t offer Build to Rent loans, and when they do, it can take ages to process. This might delay your project and blow up your budget.

Understanding the benefits and risks can help you make the right choice. If you’re still unsure, getting expert advice can make everything clearer.

What You Must Know Before Opting for Build to Rent Financing

Before plunging into Build to Rent financing, it’s essential to be fully prepared.

The first step is crafting a solid business plan. This should outline your expected expenses, the development timeline, and the projected rental revenue.

Your exit strategy comes next. Determine how you plan to pay back the loan — be it from rental income, a property sale, or refinancing. This is crucial as lenders will scrutinise your exit plan.

Lastly, scrutinise the loan terms carefully. Make sure you understand the repayment timelines, interest rates, and any penalties for missed or late payments.

Given that property development is a sizable investment, taking time to make well-informed decisions is a must. Consulting a financial advisor could be a smart move.

Other Avenues to Explore in Build to Let Investments

Build to Rent financing is a robust option, but it’s not the only path available. Here are some other avenues you might consider:

- Purchase Existing Properties. Buying and renting out existing properties can be quicker and less complicated. However, this route may offer less potential for profit because you can’t add value through construction or renovation.

- Commercial mortgages. These are generally for properties or building projects that will generate profit through capital gains or rental income. They’re usually short-term and more flexible but can be more difficult to secure.

- Bridging loan. This is a short-term financing option designed to bridge the gap between the purchase of a new property and the sale of an existing one. They can be secured quickly but usually have high interest rates.

- Consider a Joint Venture. Partnering with another developer, investor, or housing association can help to spread the risk. It can also provide you with extra resources and expertise that you may not have on your own.

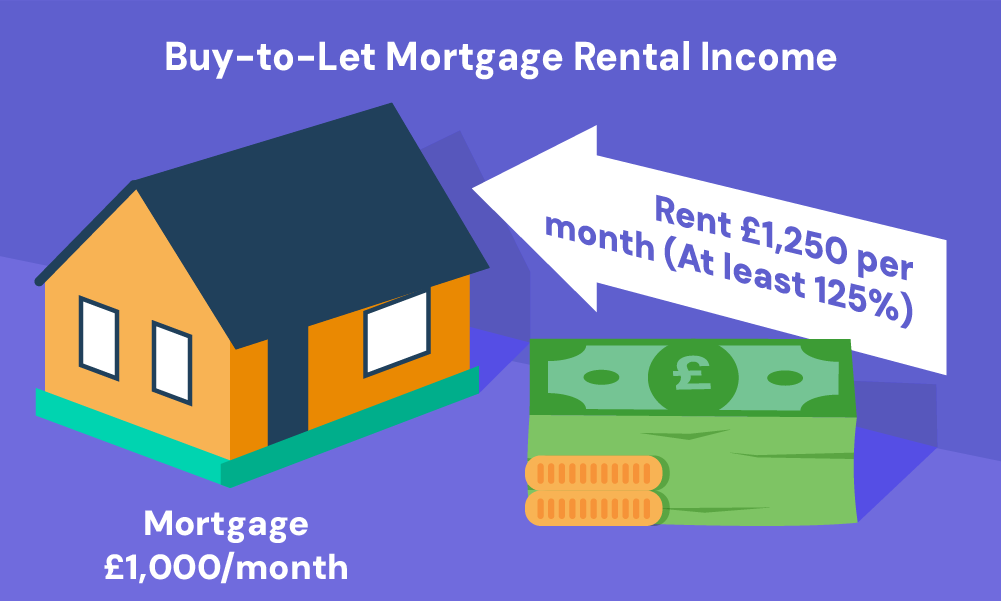

- Buy-to-let mortgage. This is a loan specifically for buying property to rent out. You’ll need a significant down payment, and the rent you charge will typically need to be 25–30% higher than your mortgage payments.

Key Takeaways

- A Build to Let mortgage is a loan that helps you pay for land and construction to build homes or flats to rent out. You can repay these loans using rental income, selling the property, or switching to a long-term mortgage.

- To get approved, you’ll need planning permission, a detailed plan, a deposit of 25–40%, and some experience in property development can help.

- Build to Rent provides steady rental income and improves neighbourhoods, but it can be expensive to start and comes with tricky loan terms.

- If Build to Rent isn’t right for you, options like buy-to-let mortgages or partnering with others may work better.

The Bottom Line

Getting a build-to-let mortgage isn’t as simple as filling out a form and hoping for the best. You need to be prepared and do a bit of homework first.

Make sure you know your credit score, have all the right documents ready, and understand the property market in the area you’re targeting. The more you know, the better your chances of getting approved.

That said, things don’t always go smoothly. You might face strict lender requirements, competition for the best properties, or unexpected challenges that could mess with your plans.

This is where a development finance broker can help. They know what lenders want, can negotiate better deals for you, and handle the paperwork so you don’t have to stress.

If you’re serious about building properties to rent, don’t do it all on your own. Reach out to us, and we’ll connect you with a broker who can make the whole process easier.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Is Build to Let Finance a wise choice?

The answer largely depends on your situation. If you’re keen on developing properties for long-term letting, Build to Let finance might be just what you need.

These loans are specially crafted to back your project, offering a personalised and flexible way to fund your development. However, make sure to assess your financial status, loan conditions, and potential risks before making your decision

How does Build to Let differ from regular buy-to-let?

Regular Buy-to-Let mortgages are loans aimed at individuals or small investors for acquiring a property to rent out. Commercial Buy-to-Let, in contrast, is tailored for larger property projects or commercial estates.

The primary difference lies in the scope and intricacy of the ventures. Commercial Buy-to-Let is geared for more elaborate projects, whereas a regular Buy-to-Let mortgage suits smaller, simpler investments.

Related Articles

Residential Development Finance: A Complete Guide

If you’re eyeing a property development opportunity, chances are you’re also wondering how to finance it. It’s rare for anyone to have enough upfront cash to cover all the costs, and that’s precisely why residential development finance is invaluable. This specialised loan could be the linchpin that holds your project together, setting the scope and […]

How To Get Better Development Finance Rates In The UK?

Did you know that even a small change in interest rates can cost you a lot of money? For example, if you borrow £1 million for a property project and the interest rate goes up by just 1%, you’ll pay an extra £10,000 each year. Over a three-year project, that adds up to £30,000 more! […]

Development Finance Calculator: Get A Quick Quote

In development finance, the borrowing range is expansive, stretching from £200,000 to as much as £50 million, depending on your chosen lender. However, unlike more straightforward loan types, what you can borrow is influenced by unique factors such as the projected profitability of your development, the loan-to-cost (LTC) ratio, and even planning permissions. That’s where […]