- How Much Can You Borrow?

- How to Get the Most Out of Our Development Finance Calculator

- Why Do Development Finance Calculator Estimates Vary?

- Do Commercial Property Calculators Differ?

- What is Development Finance?

- Development Finance Interest and Fees Explained

- Different Types of Development Finance

- Eligibility Criteria for Development Finance

- Documents You’ll Need for a Smooth Application

- Is Full Financing an Option in Development Finance?

- Can I Get Loans for Rental Developments?

- The Bottom Line

Development Finance Calculator: Get A Quick Quote

In development finance, the borrowing range is expansive, stretching from £200,000 to as much as £50 million, depending on your chosen lender.

However, unlike more straightforward loan types, what you can borrow is influenced by unique factors such as the projected profitability of your development, the loan-to-cost (LTC) ratio, and even planning permissions.

That’s where our development finance calculator becomes invaluable, offering you a tailored estimate in an instant.

Keep reading to learn more.

How Much Can You Borrow?

Curious about your project’s potential costs?

A handy calculator can give you a quick, personalised financial snapshot in less than half a minute.

All you need to do is punch in some basic numbers like projected costs and expected returns. It’s a breeze.

[Embedded Calculator for Development Finance Calculator]

But let’s be clear, while a calculator provides a quick estimate, it’s not the be-all and end-all.

In development finance, key details like the project’s expected profitability and loan-to-cost ratios often weigh heavier in the lender’s decision.

These crucial factors can greatly influence the terms of your loan.

Consulting a finance expert is the way to go for a more tailored overview. They’ll look at your project’s specifics and give you a clearer idea of your loan options.

Want to take these next steps? Just send in an inquiry and we’ll arrange you for a free, no-strings-attached discussion with a qualified advisor specialising in development finance.

How to Get the Most Out of Our Development Finance Calculator

The calculator is more than just user-friendly—it’s a simplified guide to the complexities of development finance. Best of all, there’s no need to give away sensitive personal information to get going.

Here’s a quick guide:

- Enter Key Financial Metrics – Fill in essential data like land cost, build cost, and Gross Development Value (GDV). Lenders use these numbers—alongside key ratios like Loan to Gross Development Value (LTGDV) and Loan to Cost (LTC)—to gauge how much they’re willing to lend you.

- Adjust Loan Details – Provide the loan term in months, and account for any additional costs like stamp duty or land tax.

- Run and Rerun – Once you’ve got all the data in, hit ‘calculate’. Feel free to adjust the numbers as you see fit. If the calculator flags an issue, it’s a prompt for you to fine-tune your inputs.

Things to Keep in Mind:

- Be Accurate. The more closely your inputs mirror your real-life situation, the better your results will be.

- It’s Not One-Size-Fits-All. Individual lenders can have different criteria. For detailed advice, speak with a development finance advisor.

- Use it as a Guide. The numbers you get are just an estimate. For a full financial picture, always consult a development finance specialist.

The calculator doesn’t merely churn out numbers; it provides a clear picture of your loan’s overall cost by factoring in fees and interest rates. This allows you to make informed decisions on your development project.

Why Do Development Finance Calculator Estimates Vary?

You might notice that the quotes from different development finance calculators can vary quite a bit. This isn’t a glitch—it’s because each lender uses their own calculator, and they range from basic to highly sophisticated.

Simpler calculators churn out an estimate based on essential details like Loan to Cost (LTC) and Loan to Gross Development Value (LTGDV), your deposit, and how long you’ll need the loan for.

More advanced calculators go a step further. They assess:

- Your credit score

- Your experience in the industry

- The viability of your project

- The credentials of your contractors or tradesmen

These variables directly influence the lender’s perceived risk, which in turn affects the interest rates you might get and how much you can borrow.

Do Commercial Property Calculators Differ?

Yes, they do. Some lenders offer calculators fine-tuned for commercial projects. While the basic metrics like LTGDV and LTC remain, commercial calculators might assess additional variables, such as your exit strategy and your borrowing profile, more closely.

Bear in mind, calculators serve as excellent starting points but differ in complexity. They may yield different results, making a chat with a development finance expert highly advisable.

What is Development Finance?

Development finance is a short-term loan tailored specifically for property development projects.

Unlike traditional mortgages for buying existing properties, these loans usually last between 6 to 24 months and can finance everything from new builds to extensive renovations.

A Practical Example of Development Finance

Imagine you find a piece of land for £550,000. You want to construct eight four-bedroom houses, with the total building cost estimated at £1,800,000.

To calculate the estimated Gross Development Value (GDV):

- GDV = Price per house × Number of houses = £400,000 per house × 8 = £3,200,000

Key Figures

- Land cost: £550,000

- Build cost: £1,800,000

- Total deal cost: £2,350,000

- GDV: £3,200,000

| Description | Percentage | Calculation | Loan Amount |

|---|---|---|---|

| Land Cost Loan | 65% | 65% of £550,000 | £357,500 |

| Build Cost Loan | 85% | 85% of £1,800,000 | £1,530,000 |

| Total Loan Facility (The Pool) | – | £357,500 + £1,530,000 | £1,887,500 |

How the Loan Works

- Initial Land Purchase. The lender will provide £357,500 (65% of land cost), and you’ll need to contribute £192,500 from your own funds to complete the land purchase.

- Construction Phase. The remaining £1,530,000 (85% of build cost) will be released in phases as construction moves forward. You’ll use your own funds first, then the lender follows with further drawdowns as needed.

- Loan Repayment. Upon selling the houses, you’ll repay the borrowed amount of £1,887,500 plus any accrued interest. Since this isn’t a joint venture, you’ll retain all the profits.

- Interest. Interest is typically only charged on the funds that have been drawn from the loan pool. This way, you’re not paying interest on the full £1,887,500 from the get-go, but only on the funds you’ve actually used.

Clearing the Jargon

LTC (Loan To Cost). Measures the loan amount as a percentage of the total cost of a development project. Unlike LTV (Loan To Value), which is based on the appraised value of an existing property, LTC focuses specifically on covering the immediate expenses of a new project.

LTGDV (Loan To Gross Development Value). Represents the loan amount as a percentage of the projected market value of the completed project. While LTC assesses the loan against the initial costs, LTGDV looks at the loan in relation to the expected future value of the development.

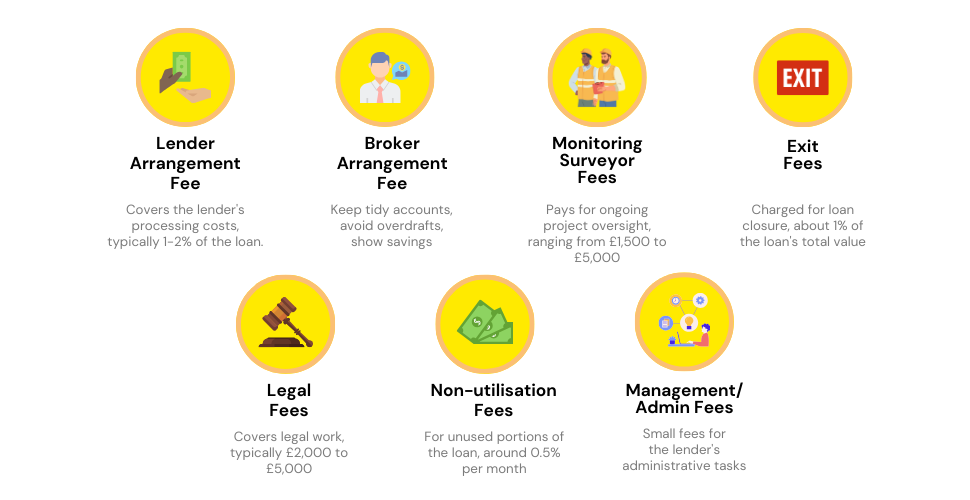

Development Finance Interest and Fees Explained

Interest rates for development finance loans usually vary between 7% and 16% APR.

These loans are short-term, often lasting from 6 to 24 months. As such, the interest rate might not be as impactful as the total cost of the loan, which also includes various fees and terms. Therefore, the lowest interest rate might not necessarily be the best option for you.

Beyond the principal and interest, there are additional costs you should be aware of, and these can vary depending on your project and loan details.

Here’s what to expect:

- Lender Arrangement Fee – This fee is commonly 1-2% of the loan amount. For instance, if you’re borrowing £1 million, the fee could be anywhere between £10,000 to £20,000.

- Broker Arrangement Fee – Using a broker will also likely incur a fee, generally around 1% of the loan amount.

- Monitoring Surveyor Fees – Depending on your project’s complexity, these could range from £1,500 to £5,000.

- Exit Fees – These are generally around 1% of either the total loan amount or the gross development value of the project.

- Legal Fees – Legal costs, including solicitor fees, typically fall between £2,000 to £5,000.

- Non-utilisation Fees – These are less common but can be around 0.5% of the undrawn loan amount per month.

- Management/Admin Fees – These cover the lender’s administrative costs and are usually nominal.

It’s important to check on the rates and fees when evaluating your loan options. And to get advice of what’s best for you, consider speaking with a development finance broker who can offer further insights catered to your situation.

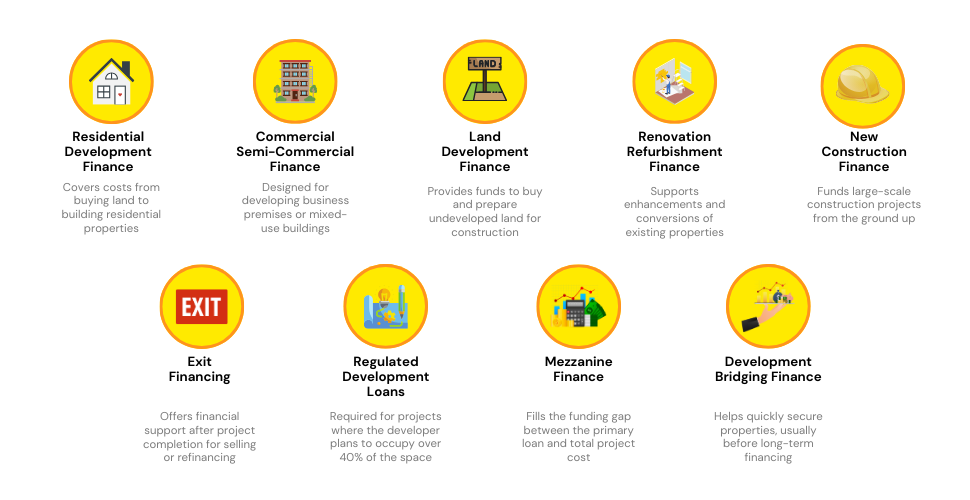

Different Types of Development Finance

There’s no universal financial solution for every development project, as each has its unique requirements. Various types of development finance are available to cater to these different needs. Here’s a guide to help you understand your choices:

- Residential Development Finance – Ideal for projects ranging from a single home to larger residential schemes. This type of finance generally covers everything from land acquisition to construction costs.

- Commercial and Semi-Commercial Development Finance – Suited for projects that involve business premises or mixed-use buildings. This option usually accommodates more complex valuation criteria.

- Land Development Finance – Used for purchasing undeveloped land and preparing it for construction, including obtaining the necessary permits and conducting site improvements.

- Renovation and Refurbishment Finance – Geared toward the enhancement of existing properties, whether it’s a straightforward refurbishment or a more complex conversion.

- New Construction Finance – Ideal for large-scale, ground-up construction projects, covering both material and labour costs.

- Exit Financing – Provides a short-term financial cushion after the completion of your project, giving you time to sell the property or secure refinancing.

- Regulated Development Loans – Required when more than 40% of the development will be a residential space occupied by the borrower. These loans are regulated by the Financial Conduct Authority (FCA).

- Mezzanine Finance – Bridges the gap between the primary loan and the total project cost, offering additional funds to ensure the project’s completion.

- Development Bridging Finance – Useful for quick property acquisitions or auction purchases, acting as a temporary measure before more long-term financing is secured.

Some projects may demand a mix of these finance types. If you’re still uncertain about which financing route to go down, consult a professional. They can guide you through the process, ensuring you choose the best option for your project.

Eligibility Criteria for Development Finance

To qualify for development finance, you’ll need to meet certain criteria. While this might differ from each lender, here are some of the usual criteria to qualify:

- Proven Track Record – Lenders usually seek applicants with a history of successful property development. If you’re new, having a strong team or expert partners can enhance your application.

- Clean Credit History – A solid credit history with no bankruptcies or defaults is a strong point in your favour for getting lender approval.

- Detailed Project Plans – Be prepared to present comprehensive plans outlining the project’s costs, estimated profits, and timelines. A professional valuation of the development property is often mandatory.

- Security – Lenders generally require collateral, which could be the property being developed or another significant asset.

- Deposit Requirement – You’ll need to make an upfront deposit, typically ranging between 20% and 40% of the project’s total cost.

- Experience and Expertise – Beyond having a proven track record, the level of expertise in your team can also influence a lender’s decision. The presence of certified professionals in relevant fields may be a requirement.

- Location – The location of the property could also be a factor. Some lenders specialise in specific geographic areas or types of developments.

Documents You’ll Need for a Smooth Application

Beyond the criteria for qualification, the application process itself involves several steps, all requiring their own set of documents.

Here’s what you should have at hand:

- Planning permission and architectural drawings.

- Any planning restrictions that could affect profitability.

- A complete cost breakdown of the project.

- Examples of your past developments, if any.

- A detailed operational calendar.

- Contacts for your architects and contractors.

- A list of your current assets and liabilities.

- Your exit strategy.

- The project’s projected final value.

Note: Individual lenders may require additional documentation, such as property valuations or anticipated post-development values.

Remember, the more robust your application, the better the terms you may receive. It’s always advisable to consult directly with potential lenders and ideally, a mortgage broker who specialises in development finance, to get a complete understanding of the qualification criteria.

Is Full Financing an Option in Development Finance?

Yes, 100% development finance is a viable option, also known as joint venture development finance. This funding model allows the lender to cover all aspects of your project, from land acquisition to construction costs, without requiring you to contribute financially.

Once the project is complete, you can either sell the property or refinance it. The profits are typically shared between you and the lender, often on a 50/50 basis, although terms can vary.

Some lenders may offer to accumulate interest on the loan in exchange for a smaller share of the profits.

It’s worth noting that in 100% development finance, traditional collateral is not always necessary. Instead, the property under development often serves as the de facto collateral, and lenders usually secure their investment by taking a charge over it.

Given the risk involved, lenders might require a strong business plan, a viable exit strategy, and possibly personal guarantees.

The lender is more than just a financial contributor; they often play an active role in project management, usually through a Special Purpose Vehicle (SPV).

The lender frequently takes an active role in the project, often managing finances through a Special Purpose Vehicle (SPV).

This finance model is particularly advantageous for large-scale projects with a Gross Development Value (GDV) over £1 million and expected profit margins of at least 25%.

Eligibility criteria can be strict, focusing on your experience in property development and the project’s GDV. While you might not have to put up additional assets as collateral, these other factors are crucial for approval.

Can I Get Loans for Rental Developments?

Yes, a Build to Let mortgage caters specifically to property developers looking to venture into the rental market. This specialised loan provides financial support for both the acquisition of land and the subsequent construction phases of your development.

The distinct feature of this loan type is that it’s tailored for projects where the end goal isn’t a sale but rather retaining the property to generate consistent rental revenue.

This form of financing is especially valuable for large residential schemes, commonly referred to as build-to-rent projects.

The Bottom Line

Development finance calculators can give you quick estimates, but they’re just a starting point for securing a loan for your project.

To understand the real costs and criteria, you need to do more than crunch numbers.

The development finance industry is complex, with different lenders having their own specific requirements, such as detailed business plans, extensive documentation, and assessments of your creditworthiness and the property’s value.

That’s where a specialist development finance broker can be invaluable. They can help you identify the right lender for your needs, negotiate favourable terms, and manage the paperwork, making the entire process more efficient.

If you want a hassle-free loan application that aligns perfectly with your project’s needs, consulting with the right development finance advisor is your next logical step.

If that’s what you look for, reach out to us. We’ll match you with a development finance advisor to help you make the smartest financial decisions for your project.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I approach lenders directly when applying for development loans?

Certainly. While you can approach lenders directly for your development finance, it’s often riskier and less advantageous than going through a broker.

Brokers not only connect you to suitable lenders but also help prepare a robust application and can negotiate better terms on your behalf. Their expertise and industry leverage make it more likely you’ll secure favourable financing for your project.

What is a Special Purpose Vehicle?

A Special Purpose Vehicle (SPV) is a separate legal entity created for a specific business purpose, usually to isolate financial risk.

In property development, an SPV is commonly used to hold the property and associated loans, protecting the main business from the risks related to the development.

It’s a structure favoured by many lenders, as it limits their exposure to the project’s risks and makes the lending more secure.

Do I need planning permission for a loan?

Yes, you usually must secure full planning permission before a lender will green-light your loan. Some might still entertain your application if you have outline planning permission, but don’t expect the funds to be released until you get the full go-ahead.

What are the alternatives to development finance in the UK to fund my project?

In the UK, besides development finance, there are various other ways to fund your property development project. You could consider:

- Joint Ventures – Partnering with another developer or an investor can spread the financial burden and risk.

- Bridging Loans – These are short-term financing options designed to bridge a gap in your financing, usually for quick projects or buying at auctions.

- Private Investors or Angel Investors – Some individuals are willing to invest in property projects in exchange for equity or a share of the profits.

- Mezzanine Financing – This is a hybrid of debt and equity financing that gives the lender the right to convert to an equity interest in case of default, generally, after venture capital companies and other senior lenders are paid.

- Crowdfunding – Online platforms allow you to raise small amounts from a large number of people, although this might come with its own set of challenges, such as management complexity.

Each of these options comes with its own benefits and drawbacks, so it’s essential to consult with financial advisors or mortgage brokers specialising in development finance to find the best solution for your project.

Related Articles

Residential Development Finance: A Complete Guide

If you’re eyeing a property development opportunity, chances are you’re also wondering how to finance it. It’s rare for anyone to have enough upfront cash to cover all the costs, and that’s precisely why residential development finance is invaluable. This specialised loan could be the linchpin that holds your project together, setting the scope and […]

How To Get Better Development Finance Rates In The UK?

Did you know that even a small change in interest rates can cost you a lot of money? For example, if you borrow £1 million for a property project and the interest rate goes up by just 1%, you’ll pay an extra £10,000 each year. Over a three-year project, that adds up to £30,000 more! […]

Why You Need a Development Finance Broker on Your Side

In property development, sorting your finances can often be the deciding factor in your project’s success. Whether you’re eyeing a line of townhouses or a towering apartment block, you need money solutions that fit your plans like a glove. To make this happen, you will need a development finance broker. These experts not only connect […]