- What is Residential Development Finance?

- How Does Residential Development Finance Work?

- Is This Similar to a Residential Land Development Loan?

- Securing the Best Rates in Residential Development Finance

- How Much Money Can I Borrow?

- Interest Rates and Additional Fees

- Why Work With a Residential Development Finance Broker?

- Is Residential Development Finance Available Across the UK?

- How to Prepare Yourself for Residential Development Finance?

- What Are My Other Options Besides Residential Development Finance?

- The Bottom Line

Residential Development Finance: A Complete Guide

If you’re eyeing a property development opportunity, chances are you’re also wondering how to finance it.

It’s rare for anyone to have enough upfront cash to cover all the costs, and that’s precisely why residential development finance is invaluable.

This specialised loan could be the linchpin that holds your project together, setting the scope and making it feasible.

Whether you’re a seasoned developer or new to property investment, knowing how to prepare before applying for finance is crucial.

In this article, we’ll guide you through each step to secure your funds, from improving your credit standing to having a financial cushion for any unplanned expenses.

What is Residential Development Finance?

Residential development finance is a specialised loan designed to help you fund your residential property project. Unlike standard mortgages, these loans are short-term and operate on an interest-only basis.

These loans are structured to disburse funds in multiple phases, each one corresponding to a significant milestone in your construction plan.

To qualify for this kind of loan, you’ll need to present a well-defined exit strategy. Commonly, borrowers repay the loan either by selling the completed residential development or by refinancing with a more traditional mortgage.

How Does Residential Development Finance Work?

Most lenders in the UK are willing to cover between 70-75% of your initial land acquisition costs, with the remaining development expenses funded 100% through staged disbursements.

Before each drawdown, a site visit usually takes place to evaluate the project’s progress. After these inspections, providers may charge a fee.

When the loan period ends, full repayment is expected. Usually, borrowers fulfil this through their pre-arranged exit strategy, either by selling the completed property or by refinancing it into a longer-term mortgage.

Is This Similar to a Residential Land Development Loan?

Some lenders might refer to ‘residential development finance‘ as a ‘residential land development loan‘. Essentially, they’re the same thing. These loans are primarily for buying land you plan to develop.

However, if you’re looking to purchase an existing property only to tear it down and rebuild, lenders will typically assess the land’s value without the existing structure. Generally, your loan terms would be based on the gross development value of the site you’re working on.

Securing the Best Rates in Residential Development Finance

The interest rates for residential development finance are typically higher than those for regular mortgages. But the interest only applies to the funds you’ve drawn down.

To secure the most advantageous rates, lenders typically look for the following:

- A Solid Exit Strategy – Lenders need assurance that their loan will be repaid. A well-laid-out exit strategy can make your application more attractive.

- A Substantial Deposit – Lenders usually provide 70-75% of the initial purchase funds and 100% of the development costs. A larger upfront deposit could lead to better rates as it minimises the lender’s risk.

- Experience in the Industry – Lenders generally favour borrowers with a track record in property development, although there are specialists who work with first-timers who have strong exit strategies.

- Good Credit Score – While options exist for those with poor credit, a clean credit history can greatly enhance your chances of securing favourable loan terms.

To unlock the best deals, consider using a broker who has access to the entire market. They can help tailor the loan to your specific circumstances, ensuring you get the best rates possible.

How Much Money Can I Borrow?

When it comes to residential development finance, you can potentially borrow anywhere from £200,000 to £50 million, although the exact amount will vary depending on your chosen lender.

Whether you’re a small-scale developer looking to renovate a single property or a larger operation aiming for a more ambitious project, there’s likely a loan tailored to your financial requirements.

To get an idea of what your repayments could be, you can use the calculator provided below. This tool allows you to tweak variables like the Loan-to-Value (LTV) ratio and loan term to estimate your monthly repayments.

[Embedded Residential Development Finance Calculator]

While the calculator offers a useful initial estimate, it’s advisable to consult a specialist broker for a more accurate and personalised assessment of your loan options.

Interest Rates and Additional Fees

Interest rates for residential development finance can vary, usually falling between 7% and 15% APR. Although these rates may seem high, remember that these are typically short-term loans.

Thus, the overall loan cost, including various lender-specific fees and terms, can be just as important as the interest rate itself. The lowest rate doesn’t necessarily translate to the best deal for your project.

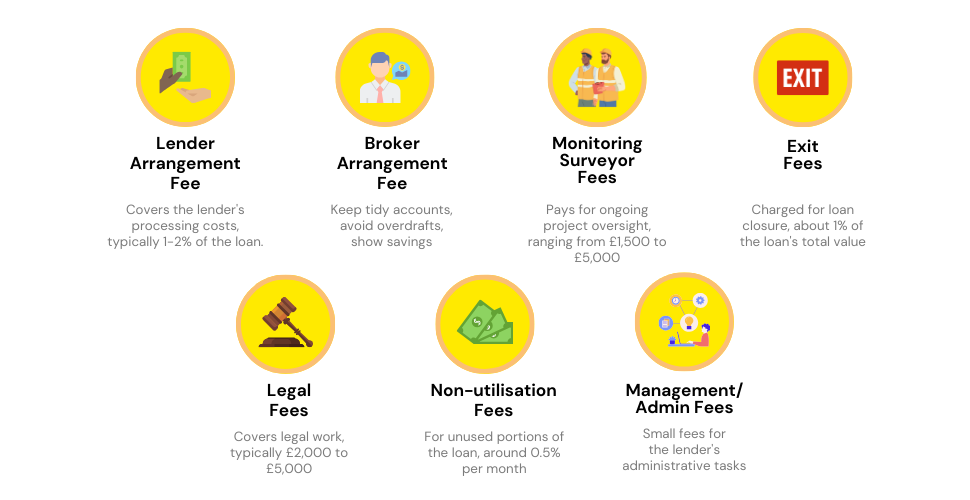

In addition to the loan’s principal and interest, you should be aware of several other fees:

- Lender Arrangement Fee – Usually 1-2% of the total loan amount. For example, a £1 million loan could incur a fee of £10,000 to £20,000.

- Broker Fee – If you work with a broker, expect to pay around 1% of the loan amount as their arrangement fee.

- Monitoring Surveyor Fees – Also known as Quantity Surveyor Fees, these can range from £1,500 to £5,000, depending on your project’s complexity.

- Exit Fees – These can vary, but are often around 1% of either the loan’s total value or the project’s Gross Development Value.

- Legal Fees – Typically between £2,000 and £5,000, covering costs like solicitor fees.

- Non-utilisation Fees – Though less common, these are typically about 0.5% of the undrawn loan amount per month.

- Management/Admin Fees – Generally nominal, maybe a few hundred pounds, to cover administrative costs from the lender.

For a comprehensive understanding of your loan options, including both interest rates and additional fees, it’s advisable to consult a broker specialised in residential development finance.

Why Work With a Residential Development Finance Broker?

Choosing the right residential development finance option can be complex and challenging.

With very few lenders authorised by the Financial Conduct Authority (FCA) to offer this kind of loan, the search for reasonable rates can be daunting.

That’s where a dedicated development finance broker can be a game-changer. These experts not only help you sift through your options but also give tailored advice specific to your project.

They can introduce you to lenders who are likely to offer you a deal that aligns with your needs. So, if you’re seeking personalised advice, consider reaching out to a broker who has a wide market reach.

Is Residential Development Finance Available Across the UK?

Well, it’s a mixed bag. It’s generally easier to secure a loan in England and Wales due to a larger number of operating lenders.

Scotland and Northern Ireland pose a bit more of a challenge. Regional restrictions may apply, particularly in remote areas like the Scottish Highlands.

Lenders willing to offer loans in these regions may impose additional conditions such as elevated interest rates or a capped loan-to-value ratio (LTV).

Given these complexities, consulting a specialised broker becomes doubly crucial if your project is situated in these areas.

How to Prepare Yourself for Residential Development Finance?

Before you apply for residential development finance, it’s important to take some steps to prepare. Here are some tips:

Know Your Borrowing Limit

Firstly, get clear on the amount you’re eligible to borrow. The amount hinges on your financial stability and the thoroughness of your project plan.

Lenders look for signs that you’re already financially stable. If you lack experience in property development, pairing up with an experienced partner is wise.

Along with payslips and bank statements, you might be asked for evidence of stable employment.

Tidy Up Your Credit History

Before approaching a lender, your credit history should be in tip-top shape. A sketchy credit file could mean a loan rejection or higher interest rates.

Apart from defaults, having numerous credit enquiries could also affect your application.

If your credit history isn’t sparkling, it might be prudent to wait a bit longer before diving into property development finance.

Keep a Cash Buffer

Unexpected costs are part of the game in property development. Delays can occur due to disagreements between the builder and subcontractors or even union involvement.

Lenders appreciate it when you’ve set aside some funds for unforeseen expenses.

Be Prepared with Asset Security

You’ll need to secure the loan with an asset, often real estate. It could be your home or the property you’re developing.

These assets act as a safety net for the lender if you default on the loan. Know what you’re willing to put up as security to gauge your readiness for this financial venture.

Conduct a Comprehensive Feasibility Study

Create an exhaustive feasibility study to convince lenders of your project’s profitability.

This should outline not just the expected profits but also details like the builder’s certifications, the site’s location, and zoning restrictions.

You should also account for various costs such as development permits, building expenses, and even a construction timeline. Aiming for a profit margin between 20-35% is a good benchmark.

What Are My Other Options Besides Residential Development Finance?

While residential development finance is a popular route, it’s not the only game in town. Here are some alternatives:

- Using Equity – If you already own a portfolio of properties, refinancing them could free up equity to fund your new project.

- Bridging Loans – These are another short-term borrowing option. If you’ve already set aside some capital for your project but it’s not enough, a bridging loan can fill the gap. These loans differ from development finance options in that they’re not released in stages.

- Self-Build Mortgage – These are pretty similar to residential development loans but tailored specifically for residential projects. You might find more favourable interest rates with this option.

The Bottom Line

Getting the right loan is just as important as choosing the best team for your home-building project. You’ve got lots of options—from banks to niche property lenders. Each one wants different things from you.

Some may ask for lots of plans and forms, while others just look at how much your property is worth and what your credit score is.

Working with a broker who knows about residential development finance can make things easier. They can find lenders that are a good fit for your project, help you get better loan terms, and save you time by handling all the paperwork.

If you’re thinking of taking the plunge, get in touch. We can match you with a top development finance broker who knows how to get you the best deal.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What's the timeline for a typical residential development loan?

The timeline varies depending on the complexity of the project and the lender’s requirements. However, loan periods are generally short-term, ranging from 6 to 24 months. Make sure to consult your lender for specifics.

Can I get a loan for smaller projects?

Yes, some lenders specialise in providing loans for smaller-scale developments. Loan amounts and terms might differ, so it’s crucial to shop around.

Are there restrictions on the type of residential property I can develop?

Lenders usually have specific criteria for the types of projects they will finance. For instance, some may prefer traditional residential properties over mixed-use developments. It’s advisable to consult your broker or lender for more information.

What happens if I fail to repay the loan?

Failing to repay a residential development finance loan can lead to severe consequences, including the loss of the asset you’ve used as security for the loan. It can also significantly impact your credit score and future borrowing ability.

Can I extend the loan period?

Some lenders offer extension options, often at a higher interest rate. However, it’s essential to discuss this possibility upfront to avoid any surprises later.

What documents do I need?

Preparing for development finance isn’t as simple as getting a regular home loan. You’ll need to offer:

- An application form

- CV outlining your development experience

- Financial statements, including asset and liability, as well as income and expenditure reports

- Annual accounts or tax returns, if applicable

- Valuation and quantity surveyor (QS) reports

- Project details, including location and cost estimates

- A comprehensive development appraisal, including proposed specification and finish

- Timeline and cash-flow forecast that considers preliminary costs, construction, and a realistic sales window

- Planning permissions and plans, including accommodation schedule

- Comparables for sale and rent in your area

- List of your project team, including their CVs and financial accounts, to demonstrate their ability to deliver the project

What's the difference between Gross Development Value (GDV) and Loan-to-Value (LTV) Ratio?

Gross Development Value (GDV) and Loan-to-Value (LTV) ratio are two crucial metrics in residential development finance.

- Gross Development Value (GDV) – This is the estimated market value of your completed project. It’s what you expect the development to be worth once all work is finished. Lenders use this to gauge the potential profitability of your project.

- Loan-to-Value (LTV) Ratio – This represents the loan amount as a percentage of the property’s value used as security. Lenders use this to assess their risk.

Formulas:

- GDV – (Estimated Selling Price of Property × Number of Units) + Any Additional Income (like rent)

- LTV Ratio – (Loan Amount ÷ Property Value) × 100

Understanding these metrics can help you better plan your project and loan application.

Related Articles

How To Get Better Development Finance Rates In The UK?

Did you know that even a small change in interest rates can cost you a lot of money? For example, if you borrow £1 million for a property project and the interest rate goes up by just 1%, you’ll pay an extra £10,000 each year. Over a three-year project, that adds up to £30,000 more! […]

Development Finance Calculator: Get A Quick Quote

In development finance, the borrowing range is expansive, stretching from £200,000 to as much as £50 million, depending on your chosen lender. However, unlike more straightforward loan types, what you can borrow is influenced by unique factors such as the projected profitability of your development, the loan-to-cost (LTC) ratio, and even planning permissions. That’s where […]

Why You Need a Development Finance Broker on Your Side

In property development, sorting your finances can often be the deciding factor in your project’s success. Whether you’re eyeing a line of townhouses or a towering apartment block, you need money solutions that fit your plans like a glove. To make this happen, you will need a development finance broker. These experts not only connect […]