- Can I Change or Switch a Fixed Rate Mortgage?

- When Can I Switch A Fixed-Rate Mortgage?

- Acceptable Reasons to Consider Switching a Fixed Rate Mortgage

- The Risks of Switching a Fixed Rate Mortgage Early

- Which Mortgage Type Should I Switch?

- How To Switch a Fixed Rate Mortgage the Right Way

- The Bottom Line: Should You Switch Your Fixed Rate Mortgage?

What You Should Know About Changing A Fixed Rate Mortgage

When you have a fixed rate mortgage, you’re locked into that interest rate for a set period, typically between 2 to 5 years. However, things can change during this time.

Perhaps your financial situation has improved and you want to reduce your monthly payments, or you’re expecting interest rates to rise based on economic forecasts.

Any of these reasons might make you consider switching mortgage products.

But the real question is, can you actually change or switch from a fixed rate mortgage before it ends?

Can I Change or Switch a Fixed Rate Mortgage?

Yes, you can switch a fixed rate mortgage before it ends. If you find a better deal with lower rates, you might save money by switching.

But, watch out for extra costs. Some banks charge you a fee for leaving your deal early. This is called an early repayment charge (ERCs). If you decide to switch, compare the savings with the fees to see if it’s worth it.

If you’re unsure, you might want to talk to a qualified mortgage advisor to get advice about what’s best for you. Remember, you have the power to change your mortgage if you need to.

When Can I Switch A Fixed-Rate Mortgage?

Anytime!

Even if you’re tied into your fixed rate mortgage for the length of the term, you can switch your deal ANYTIME.

However, the best time to make a move is often just before your fixed term ends to dodge extra charges.

Here’s a rundown of situations where you can change or switch products:

At the End of the Fixed Rate Period

The easiest and best time to change or switch a fixed rate mortgage is when you reach the end of the fixed rate period.

At this point, you’re no longer tied into the fixed rate and are free to remortgage to a new deal with NO early repayment charges (ERCs).

Your mortgage will revert to your lender’s standard variable rate (SVR) when the fixed period ends if you don’t remortgage.

SVRs tend to be higher than fixed rate deals, so it’s advisable to shop around and switch to a new fixed or tracker mortgage at this point.

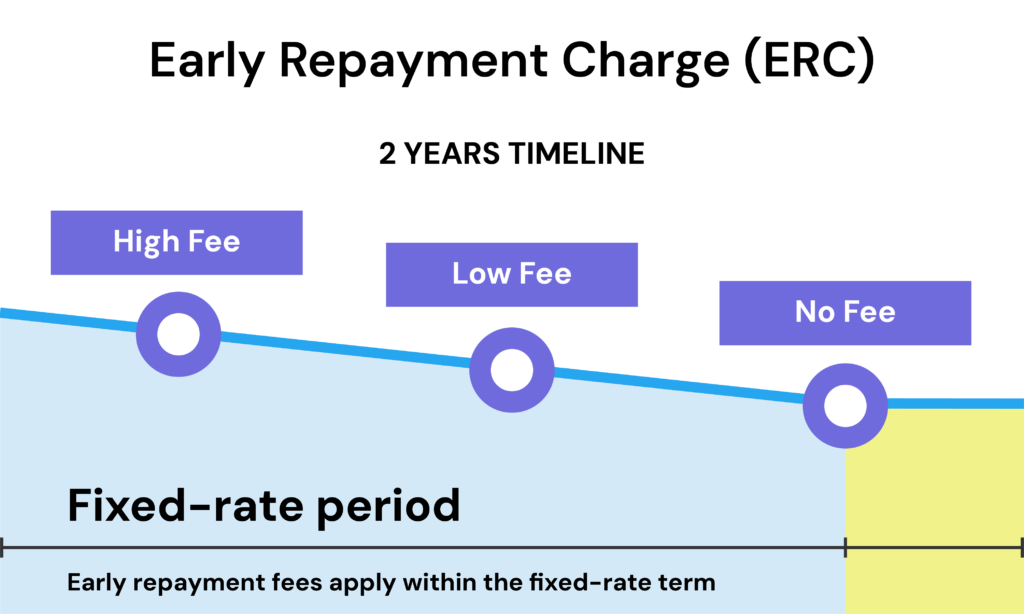

During the Fixed Rate Period – Paying Early Repayment Charges

It is possible to switch a fixed rate mortgage before the end of the fixed term, but your lender will charge you early repayment charges (ERCs) which can be quite costly– typically 1-5% of the outstanding mortgage balance.

The amount of ERC reduces the closer you get to the end of the fixed rate period. Some lenders may waive the ERC if you are within the last 6 months or so of the fixed period when you switch.

You’ll need to weigh up the costs of paying the ERC against any potential savings you might make by switching to a new, lower mortgage deal.

It only makes financial sense to switch mid-fixed term and pay ERCs if the savings you’d make on the new mortgage outweigh the ERC costs over the remaining fixed term.

Acceptable Reasons to Consider Switching a Fixed Rate Mortgage

There are a few common situations where it may be worth considering switching your fixed rate mortgage despite the ERC:

Interest Rates Have Dropped Significantly

If interest rates have fallen dramatically since you took out your fixed rate mortgage, it could make financial sense to switch and pay the ERC. This lets you make substantial savings on a new, lower rate over the remaining term.

For example, if you fixed at 5% for 5 years but rates have since fallen to 2.5% – you may be able to recoup the costs of the ERC and save money long-term with the much lower monthly payments on the new mortgage.

Your Circumstances Have Changed

Changes in your personal circumstances like divorce, losing a job, having children etc. can mean your current mortgage no longer suits your needs.

Switching to a more affordable mortgage deal may be better than struggling with unaffordable payments and risking arrears or repossession.

You Want to Borrow More

If you need to borrow more capital–e.g. for home improvements–you can choose to remortgage to release equity and increase your mortgage borrowing amount.

You’ll pay ERCs with your current lender but may be able to offset this with a better rate on your new, larger mortgage.

You Want to Overpay or Underpay

Some fixed rate mortgages restrict you from making overpayments above a certain amount each year.

If you want the flexibility to overpay and clear the mortgage faster, you may decide it’s worth switching products and paying the ERC despite still being in a fixed rate period.

Likewise, if you want to reduce your monthly payments by switching to an interest-only mortgage, you’d need to remortgage and pay ERCs if you’re currently on a repayment fixed rate.

The Risks of Switching a Fixed Rate Mortgage Early

While there are some scenarios where switching a fixed rate mortgage can make sense, it’s important to carefully consider the risks:

You May End Up Paying More

Even if interest rates have dropped, you may not actually save enough on the new mortgage to fully recover the early repayment charge costs, leaving you out of pocket overall.

Rates would need to have dropped significantly for switching mid-term to be worthwhile.

Interest Rates Could Rise Again

If you switch from a fixed rate to a variable-rate mortgage because of currently low rates, there’s a risk these rates could increase later.

If they do, your new mortgage payments might rise, potentially costing you more than if you had stayed with your original fixed rate.

You May Get Rejected for Remortgaging

When you remortgage, the lender will need to evaluate your income, credit record and affordability as if you were a new borrower.

If your financial situation has deteriorated, you may struggle getting approved for a new mortgage.

You’ll Pay Exit Fees and Setup Costs

In addition to early repayment charges, there are usually exit fees to pay your current lender plus setup costs like valuation fees, legal fees etc. for your new mortgage that can run into hundreds or thousands of pounds.

Which Mortgage Type Should I Switch?

Deciding to switch your mortgage can save you money, but which type should you choose?

Here are a few options:

- Switch to a Tracker Mortgage. This type changes with the Bank of England’s base rate. If the base rate goes down, you might pay less each month. But, if it goes up, so do your payments. This is good if you think rates will drop and stay low. Tracker mortgages often let you pay more when you can, reducing what you owe faster.

- Change to a Variable Rate Mortgage. Here, your lender decides the rate, which can change anytime. This means your monthly payments can go up or down. People with this mortgage aren’t tied to fixed payments, which gives some flexibility. But, it can be risky if rates go up because your payments will increase too.

- Go for Another Fixed Rate. When your fixed term ends, you could lock in a new fixed rate. This is great if you like knowing exactly what you’ll pay each month. Remember, there might be a fee to set this up, but it can protect you from rate rises.

When choosing a mortgage type, think about what you need from your mortgage. Talking to a broker can help you find the best option for you.

How To Switch a Fixed Rate Mortgage the Right Way

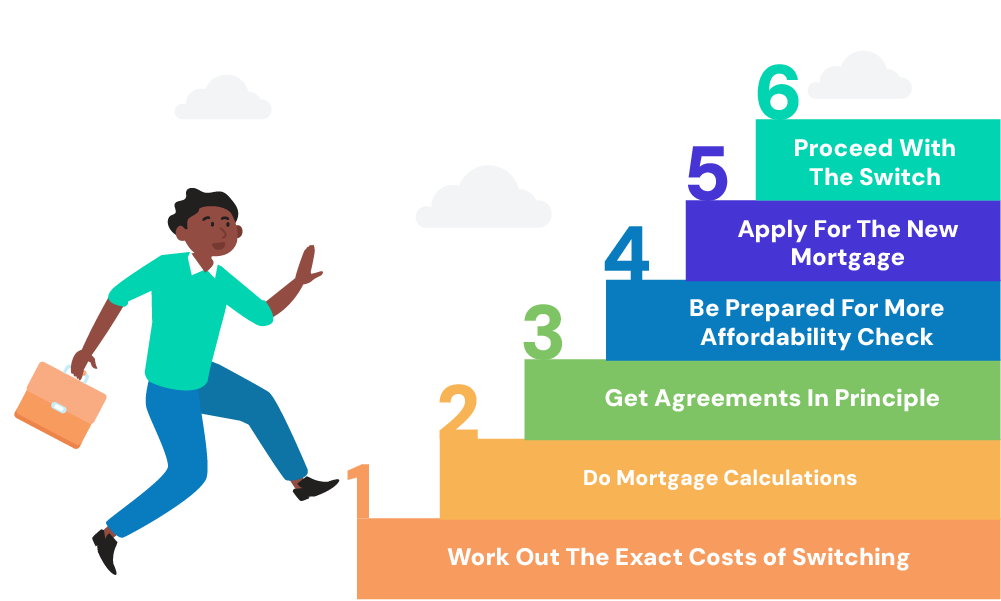

If, having understood the risks and costs, you still think switching your fixed rate mortgage is the best financial decision, here are the steps to take:

- Work Out The Exact Costs of Switching. Ask your current lender for a redemption statement showing exactly how much the ERC would be to exit your fixed rate mortgage early. Also get fee quotes from solicitors and removal firms if you plan to switch lenders.

- Do Mortgage Calculations. Crunch the numbers to calculate whether you’ll actually SAVE enough on a new mortgage. Factor in the costs of switching like the ERC, fees and a potentially higher interest rate if rates rise again.

- Get Agreements In Principle. Before fully committing, get a mortgage agreement in principle from the new lender. This confirms how much they’re willing to lend you and at what rate, based on a preliminary assessment of your financial situation.

- Be Prepared For More Affordability Check. Lenders have tightened affordability checks in recent years. This means MORE documentation is required from borrowers proving their income, expenditure and ability to afford the repayments.

- Apply For The New Mortgage. Once you’re ready, apply for the NEW mortgage. Ensure all your financial documents are in order, such as proof of income and recent bank statements, to smooth the application process.

- Proceed With The Switch. After receiving formal mortgage approval and considering all financial implications, you can proceed with switching your mortgage. Ensure you understand ALL the terms and conditions of the new agreement before finalising.

The Bottom Line: Should You Switch Your Fixed Rate Mortgage?

For most borrowers, the costs and risks of switching a fixed rate mortgage early outweigh any potential benefits.

It’s usually BEST to simply wait until the end of the fixed rate period when you can remortgage for free with no early repayment charges.

However, in certain situations—like if rates have significantly dropped or you urgently need lower payments due to financial changes—it may be worth paying the charge to switch before the term ends.

But you should always calculate the long-term savings you’d make to justify the upfront costs of an early switch from your fixed rate deal.

If you’re unsure about any steps or how the switch might affect your finances, consult a good mortgage broker. They can provide you tailored financial advice and peace of mind.

A broker can scan the entire market for the most suitable remortgage deal for your needs.

Looking for a broker? Reach out to us. We’ll connect you with a qualified mortgage broker who can handle the entire remortgaging process and find you the best deal.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What are the disadvantages of a fixed rate mortgage?

Firstly, they often have higher interest rates than variable rates at the start. If interest rates fall, you won’t benefit as you’re locked into a set rate.

Additionally, there are usually significant charges if you want to switch or repay early during the fixed term.

Is it good to have a fixed-rate mortgage?

Yes, having a fixed-rate mortgage can be beneficial. It provides stability because your monthly payments stay the same throughout the term, making budgeting easier.

This is especially helpful in periods of rising interest rates. However, the suitability depends on your financial situation and future plans.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How Long Should I Fix My Mortgage For? 2,3, or 5 Years?

For homebuyers and owners in the UK, deciding whether to fix your mortgage interest rate can be a tough decision. With rates RISING rapidly over the past year, securing a fixed rate deal protects you from further hikes – but it also locks YOU into a deal if rates start to fall again. This guide […]

What Happens When Your Fixed-Rate Mortgage Ends?

As your fixed rate mortgage draws to a close, it’s natural to ponder what lies ahead. 🤔 Whether your deal was locked in for 2 years or stretched out over 5, the end of this period marks a significant turning point in your mortgage journey. Let’s explore what’s in store when your fixed term is […]

What is a Long-Term Fixed Rate Mortgage?

A long-term fixed rate mortgage allows you to lock in an interest rate for an extended period, often 5 years or longer. With a traditional fixed rate deal, your interest rate is only set for 2-5 years before you need to remortgage. But with a long-term fixed, you can secure your rate for 10, 15, […]