- What Is Equity Release and Home Equity?

- The Basics of Equity Release Schemes

- Can I Release Equity from My Home for Home Improvements?

- How Much Equity Can You Release for Home Improvements?

- How Do You Release Equity to Renovate Your Home?

- 6 Common Methods of Releasing Equity for Home Improvements

- What Home Improvements Can I Pay for with Equity Release?

- What Are the Benefits of Using Equity for Home Improvements?

- What Are the Potential Risks and Considerations of Equity Release?

- The Bottom Line: Is Equity Release a Smart Choice?

How To Fund Home Improvements With Equity Release?

Transforming your home can be exciting, but it often comes with the big question: how to pay for it all?

If you own your home, there’s good news. You’ve got a handy tool to help with the costs – the equity in your home.

Equity release lets you use the value you’ve already built up in your property to fund your home improvements. It’s a way to unlock this value and turn it into real money you can use.

Whether you’re planning to modernise your kitchen, build a conservatory, or give your house a new look, equity release could be the answer.

In this guide, we’ll walk you through how equity release works for home renovations. You’ll get all the essential info you need, so you can make smart choices about upgrading your home.

Let’s get started!

What Is Equity Release and Home Equity?

Equity release is like unlocking the value of your home while you still live in it. It’s a way for homeowners, usually older ones, to get some cash out of their homes without having to move out.

Think of your home as a piggy bank. Over the years, as you pay your mortgage, you fill this piggy bank. The money you have in this ‘house piggy bank‘ is what we call home equity.

Now, home equity is the part of your house that you truly own. It’s the difference between what your home is worth and how much you owe on your mortgage.

Let’s say your house is worth £200,000, and you owe £50,000 on your mortgage. Your home equity is £150,000.

Equity release is like tapping into this £150,000 without selling your home. It’s a popular choice for folks who might need extra money for things like home improvements or just to make retirement a bit more comfortable.

The Basics of Equity Release Schemes

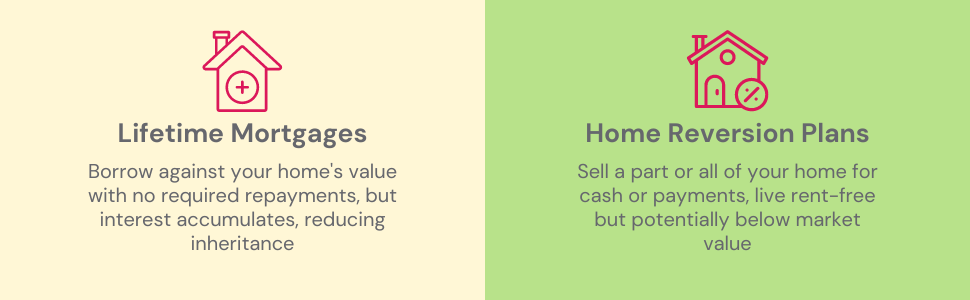

Equity release schemes in the UK come in two main forms: Lifetime Mortgages and Home Reversion Plans.

Lifetime Mortgages are the more common type. This allows homeowners to borrow against their home’s value without the need for monthly repayments.

Instead, the interest accumulates, and the total loan amount, including this interest, is repaid when the home is sold, typically after the owner passes away or enters long-term care.

Home Reversion Plans, less commonly chosen, involve selling a part or all of your home to a reversion company in exchange for a lump sum or regular payments.

You can continue living in your home rent-free, but upon its eventual sale, the company receives their share of the sale price.

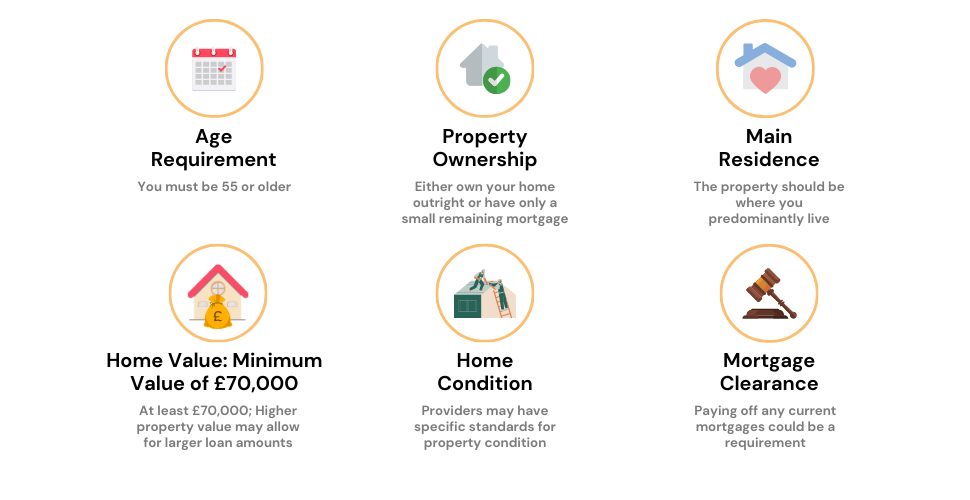

Eligibility for these schemes generally requires the homeowner to be at least 55 years old (or older for home reversion plans), own a property valued at a minimum of £70,000, and have either no or a small outstanding mortgage.

The property must be in the UK and a good state of repair.

Since equity release is a significant financial decision and not suited to everyone, consulting a mortgage advisor is highly recommended to explore the best options for your situation.

Can I Release Equity from My Home for Home Improvements?

Absolutely, you can! If you’re thinking about making some changes to your home, like updating the kitchen or adding a conservatory, releasing equity can be a smart way to get the money for these improvements.

It’s a popular choice for many homeowners.

If you’ve paid off a good chunk of your mortgage and your home’s value has gone up, you’ve likely built up some equity.

This equity is like a pot of money tied up in your house. Releasing some of this equity means you can turn it into cash, which you can then use for your home improvements.

How Much Equity Can You Release for Home Improvements?

The amount of equity you can release for home improvements isn’t a one-size-fits-all answer. It varies depending on several factors:

- Your Age. Generally, the older you are, the more equity you can release. Lenders often feel more comfortable lending larger amounts to older folks.

- Your Home’s Value. The more your home is worth, the more equity you’ll likely be able to release. However, there’s usually a minimum property value requirement, often around £70,000.

- Your Mortgage Balance. If you still owe a lot on your mortgage, it could limit the amount of equity you can release.

As a rough guide, some lenders might let you borrow up to 50% of your home’s value, but this depends on your circumstances. A mortgage advisor can give you a clearer picture based on your specific situation.

To find the right one, simply get in touch. We’ll connect you with a perfect mortgage advisor who can help you decide which options are best suited for you.

How Do You Release Equity to Renovate Your Home?

Here’s how you can go about it:

- Get Your Home Valued. First, you’ll need to find out how much your home is worth. This helps determine how much equity you can release.

- Speak to a Mortgage Advisor. This step is important. A mortgage advisor specialising in equity release can help you understand all your options and the impact on your finances and estate.

- Choose the Right Equity Release Product. There are two main types – Lifetime Mortgages and Home Reversion Plans. Choose the one that suits your needs the best.

- Application Process. Once you’ve chosen a product, you’ll go through an application process. This includes credit checks and assessments of your financial situation.

- Legalities and Paperwork. You’ll need a solicitor to help with the legal side of things. They’ll make sure everything’s above board and in your best interest.

- Receiving the Funds. If your application is successful, you’ll get the money, either as a lump sum or in smaller amounts. Now you can start planning those home improvements!

Pro Tip

It’s vital to pick the right equity release plan and get sound advice. Make sure to choose a plan from a lender who’s a member of the Equity Release Council (ERC) for reliability.

Also, go for an adviser who’s regulated by the Financial Conduct Authority (FCA) to ensure you’re getting trustworthy guidance.

6 Common Methods of Releasing Equity for Home Improvements

Homeowners in the UK looking to fund their home improvements have several options for releasing equity.

Each method suits different needs and financial situations. Here’s a straightforward look at these options:

Remortgaging for Home Renovations

Remortgaging is a strategy where you replace your existing mortgage with a new one, often for a larger amount if your home’s value allows it.

For instance, say your current mortgage balance is £150,000, and you have £50,000 in home equity. You could potentially remortgage for £200,000.

Here’s how it works: The new mortgage of £200,000 is used to pay off your existing £150,000 mortgage.

The remaining £50,000 (which represents the equity you’ve built up in your home) is released to you for your home improvement projects.

However, it’s important to be aware of potential early repayment charges on your existing mortgage. This option hinges on your property’s current value and your ability to meet the lending criteria for the increased amount.

Second Charge Mortgage

This option involves taking out a second loan secured against your property’s equity, alongside your existing mortgage.

It’s an alternative to remortgaging, allowing you to borrow additional funds without disturbing your current mortgage terms. Keep in mind the need for managing two sets of repayments and potential additional fees.

Lifetime Mortgage (Reverse Mortgage)

A lifetime mortgage, suitable for homeowners over 55, lets you borrow a part of your home’s equity, which can be up to 100% in some cases.

This amount is repaid when your home is sold, usually after you pass away or move into care. The interest accumulates over time, increasing the total repayable amount.

Home Equity Loan

A home equity loan allows you to borrow a fixed sum against your home’s equity, typically at a fixed interest rate. This loan requires regular repayments, and failing to meet them could put your property at risk.

Home Equity Line of Credit (HELOC)

HELOC offers a flexible credit line based on your home’s equity. It allows you to draw funds as needed, ideal for ongoing projects.

You pay interest only during the draw period, then start repaying the principal amount.

Secured Personal Loan

These loans use your home equity as collateral and can be more versatile in terms of usage compared to other equity release methods. It’s important to understand their terms to avoid risking your property.

Before proceeding with any of these options, seeking financial and legal advice is crucial.

Equity release solicitors typically charge around £1,000, and their guidance is invaluable in navigating these financial decisions. Consider their fees as part of your budget planning.

What Home Improvements Can I Pay for with Equity Release?

Equity release can be used for a variety of home improvements, but some are more common than others. Here are the top 5:

- Major Renovations. Big projects like kitchen or bathroom remodels, extensions, or loft conversions. These are popular because they can significantly increase the value of your home.

- Energy Efficiency Upgrades. Things like installing solar panels or upgrading to more energy-efficient windows and heating systems. Not only do these improve your home, but they can also reduce your energy bills in the long run.

- Maintenance and Repairs. This could include fixing the roof, updating the plumbing, or sorting out damp issues. Keeping your home in good repair is essential for maintaining its value.

- Garden and Exterior Work. Landscaping, building a patio, or adding a conservatory can enhance your living space and the overall appeal of your property.

- Accessibility Improvements. For older homeowners, installing stairlifts, walk-in showers, or other modifications can make a home more comfortable and accessible.

What Are the Benefits of Using Equity for Home Improvements?

Here are some of the benefits when using home equity to improve your home:

- Boost your home’s value. Sprucing up your place with a new kitchen or extension can be like an investment, adding pounds to its worth.

- Make your life sweeter. Want a sunroom for chilling or a loft for extra space? Equity release helps you create the home you’ve always wanted.

- No repayments right away. Breathe easy! Some plans, like lifetime mortgages, let you enjoy your improvements without monthly bills.

- Tax-free cash. The money you unlock is all yours to spend, with no taxman taking a cut.

- Go green, save money. Swap old fixtures for energy-efficient ones and watch your bills shrink while helping the planet.

What Are the Potential Risks and Considerations of Equity Release?

Like any other loan, equity release comes with its set of drawbacks. Here’s a rundown of the potential risks and considerations before diving in:

- Less to inherit. Using equity release means you’ll have less to leave behind, and the debt can grow, especially without repayments.

- Interest Accumulation. For lifetime mortgages, the interest on the loan accumulates over time, which can quickly increase the amount you owe.

- Limits on Future Borrowing. Once you’ve released equity, it can limit your ability to borrow more money in the future, as you have less equity in your home.

- Impact on Means-Tested Benefits. Releasing equity might affect your eligibility for means-tested benefits. It’s important to check how this could impact your financial situation.

- Upfront Costs. There are costs associated with equity release, like legal and advice fees, and possibly an early repayment charge on your current mortgage if you remortgage.

- Risk of Negative Equity. In a falling property market, there’s a risk your home might end up worth less than the amount you owe, especially if you’ve released a large portion of your equity.

As with any significant financial decision, it’s crucial to get professional advice, which incurs additional costs.

The Bottom Line: Is Equity Release a Smart Choice?

Equity release might be a good option for funding home improvements if you need extra cash and your house is a major asset.

It lets you to tap into your home’s value without selling it, offering a financial boost for renovations that could increase your property’s worth and enhance your living experience.

However, it’s a significant decision with long-term effects. Releasing equity can reduce your future estate value and increase your debt over time due to accumulating interest.

That’s why it’s essential to seek advice from a mortgage advisor. They’ll help you understand how equity release fits into your financial picture, tailoring advice to your specific situation.

Thinking about equity release? Contact us to connect with a skilled mortgage advisor who can guide you through the process, ensuring a choice that’s right for your financial future.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Are there other ways to fund home improvements besides equity release?

Apart from using equity release, there are several other ways you can fund your home improvements:

- Saving Up. It might take longer, but saving up for your home improvements means you won’t have to pay interest. It’s the most cost-effective way if you can wait.

- Credit Cards. For smaller projects, a credit card, especially one with an introductory 0% interest rate, can be a handy option. Just be sure to pay it off before the interest rate kicks in.

- Home Improvement Loans. These are unsecured loans specifically for home improvements. They usually have fixed interest rates and set repayment periods.

- Personal Loans. A personal loan can be another way to finance your home improvements. These loans are often unsecured and can be used for a variety of purposes, including home renovations.

Each of these options has its pros and cons, and the right choice will depend on your financial situation, the cost of the project, and how quickly you need the funds.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Home Improvement Loans Calculator – Get a Personalised Quote

Home improvements can transform your house, but they often come with a big price tag. A home improvement loan can be incredibly useful in this situation. It provides you with the necessary funds to make your dream home a reality. But how do you determine how much you can borrow or what it will cost? […]

Can I Use a Second Mortgage for Home Improvements?

Home improvements are great for making your home more comfortable and valuable. But, they can be expensive. A second mortgage can help you pay for these home upgrades. This means you borrow money based on the value of your house that you own, called equity. It gives you the cash you need for big changes, […]

Revamp Your Space with Home Improvement Loans: A Full Guide

When it comes to giving your home a makeover, one of the biggest hurdles can often be the cost. It’s a common question: what do you do when your savings just don’t stretch far enough? Home improvement loans could be the answer, offering financial support for your renovation journey. This guide will help you understand […]