- What Defines a £1 Million Mortgage?

- What Salary Do I Need for a Million-Pound House?

- How Much Deposit Do I Need?

- How Much Interest is on £1 Million?

- Steps to Getting a Million-Pound Mortgage

- What Monthly Repayments to Expect?

- Choosing Your Million-Pound Home: Tips and Considerations

- How to Make a Million Pound Mortgage More Affordable

- Key Takeaways

- The Bottom Line

£1 Million Mortgages: How To Buy A Million-Pound House?

Buying a home worth £1 million used to feel like an impossible dream, but now it’s something more people can consider. These mortgages, once just for the super-rich, are becoming more accessible.

This change means high-value homes aren’t as out of reach as they once were.

If you’re curious about diving into this market, it’s a good idea to understand what’s involved in getting a £1 million mortgage.

This guide will simplify everything for you, with clear advice to help you decide if it’s right for you.

Whether you’re aiming for a luxury upgrade or thinking of investing, a £1 million mortgage might not be as scary as it sounds.

Let’s break it down and look at what these mortgages are all about and the lenders offering them.

What Defines a £1 Million Mortgage?

A £1 million mortgage might sound enormous, and let’s be real — it is. But at its core, it’s simply a loan to help you buy a high-value property.

Taking on this kind of financial commitment means you’ll need to have a solid plan and a clear understanding of what you’re signing up for.

In the UK, you’ve got two main camps when it comes to lenders: high-street banks and private lenders.

Let’s see what each has to offer:

High-Street Banks

- These are your go-to names, like Barclays or NatWest. They’re accessible and have a clear process in place.

- High-street banks are great if your finances are pretty straightforward. You’ve got a stable income, little debt, and no big financial surprises.

Private Lenders

- These folks take a more tailored approach. If you’ve got irregular income, rely on bonuses, or you’re self-employed, private lenders might be more flexible.

- But beware, this flexibility can come at a price. You might face higher interest rates or need to jump through a few more hoops.

Choosing between the two depends on your financial situation and the type of property you’re after.

With more options now available, you’ve got plenty of room to find a lender that suits your needs.

What Salary Do I Need for a Million-Pound House?

So, you’ve got your eyes on a million-pound home. The big question is: can your salary make it happen?

Here’s how it works: lenders typically let you borrow up to 4.5 times your annual income. That means you’ll need to earn a decent whack.

If you’re applying solo, we’re talking upwards of £220,000 a year. Ouch, right?

Let’s break it down with an example.

Say you earn £230,000 a year. Multiply that by 4.5, and you’re looking at a potential loan of around £1,035,000.

Keep in mind, though, this is just a ballpark figure. Lenders will also check your other financial commitments, like debts or outgoings, before giving you the green light.

So, while a big salary helps, it’s not the only thing they’ll consider.

How Much Deposit Do I Need?

Think of your deposit as the first hurdle to getting your dream home.

For a £1 million property, deposits usually range between 10% and 40% of the home’s value. That means you’re looking at saving anywhere from £100,000 to £400,000 upfront.

Here’s the thing: the size of your deposit has a big impact on your mortgage terms. A bigger deposit means:

- Borrowing less money

- Getting better interest rates

On the flip side, a smaller deposit means you’ll need to borrow more, which could mean steeper monthly repayments and higher interest rates.

It’s all about striking a balance between what you can afford to pay now and what you’re comfortable paying later.

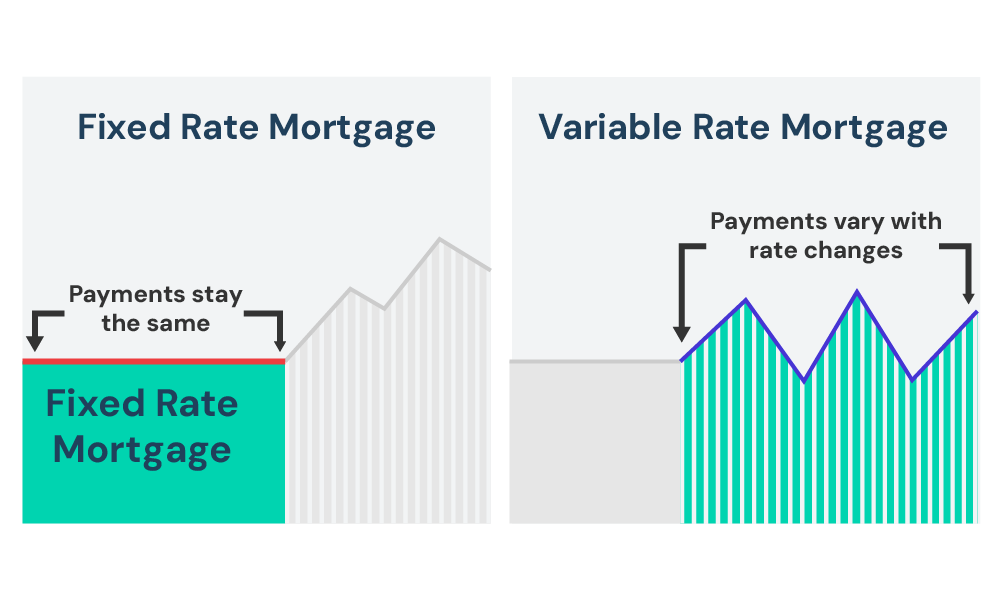

How Much Interest is on £1 Million?

Interest rates depend on a few things: the lender, your credit score, and the type of rate you choose.

There are two main options:

- Fixed-Rate Mortgages. These keep your payments steady for a set period. It’s like putting on a financial seatbelt—no surprises.

- Variable-Rate Mortgages. These go up and down with the market. A bit of a rollercoaster ride, thrilling for some, nerve-wracking for others.

Rates can range from around 1% to 5% or more, depending on your lender and financial situation.

For example, a £1 million mortgage at a 2% fixed rate would cost about £20,000 a year in interest.

Knowing your options and how they fit your budget is key. It might not be the most exciting part of the process, but it’s worth getting right to save money in the long run.

Steps to Getting a Million-Pound Mortgage

Getting a £1 million mortgage isn’t that different from a regular one, but there are a few extra things to think about. Here’s a simple step-by-step:

- Check Your Finances. First, take a good look at how much money you’re making and what you’ve saved up. You also need to know about any debts you have. Make sure you’ve got all your important papers like payslips and bank statements ready.

- Sort Out Your Credit Score. It’s really important to make sure your credit score is as good as it can be. Check your credit report and pay off any debts if you can. A better credit score helps you get a better deal on your mortgage.

- Remember the Extra Costs. Don’t forget that there are extra costs when you get a mortgage. This includes things like stamp duty and legal fees. These can add up, so you need to plan for them.

- Choose the Right Lender. You need to decide if you want to borrow from a regular bank or a private lender. They offer different types of deals, so think about what works best for you.

- Apply for the Mortgage. Once you’ve got everything sorted, you can apply for the mortgage. After that, the lender will check the value of the house and look at your finances to make sure everything’s okay. If it is, they’ll give you an offer.

While this guide can help you understand large mortgages, this stuff can be quite tricky, especially because there’s a lot of money involved.

Talking to a mortgage broker can help. They can give you advice on what mortgage to choose and help you understand all the tricky bits. They’re good at finding the best deal that fits your situation.

To get started, don’t hesitate to reach out. We’ll set up a free, quick, and no-obligation chat with a mortgage broker to help you make a smart financial decision.

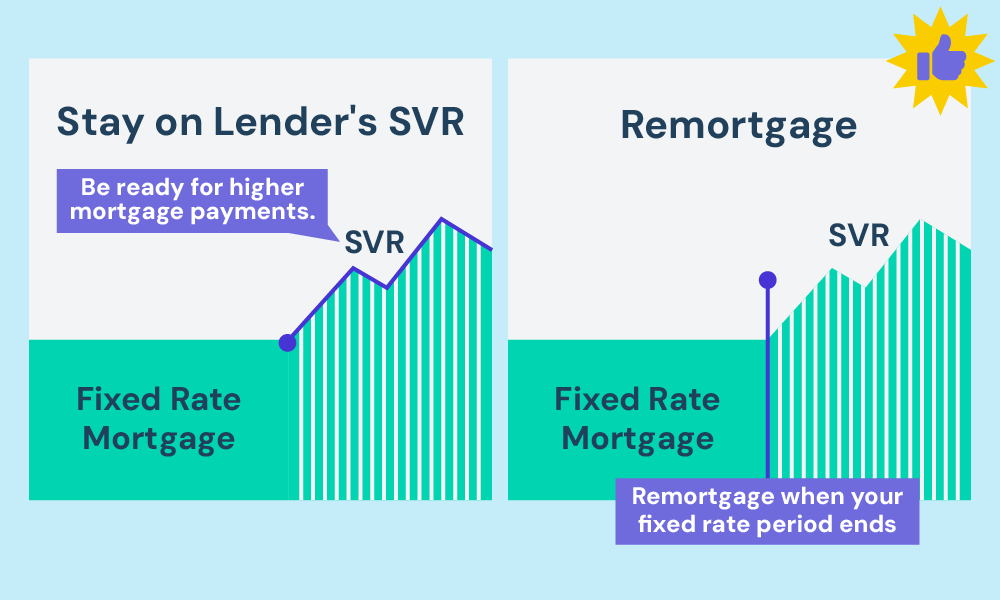

What Monthly Repayments to Expect?

Your monthly repayments for a £1 million mortgage depend on the type of mortgage, the interest rate, and how long the fixed rate lasts.

In the UK, fixed interest rates are common and usually last for 2, 3, or 5 years. During this time, your monthly payments stay the same, which makes budgeting easier.

When the fixed rate ends, most lenders switch you to a standard variable rate (SVR), which is often higher.

At this point, you can choose to remortgage and get a new fixed-rate deal.

Before we go over the numbers, remember, these are just examples to give you an idea. Your actual rates and terms can vary depending on the lender and your financial situation.

There are two main ways to pay back your mortgage.

With a repayment mortgage, you pay off both the loan and the interest every month.

This means your balance gets smaller over time. But your monthly payments are higher compared to an interest-only mortgage.

Here’s an example:

| Interest Rate | Monthly Payment (£) | Total Paid Over 5 Years (£) |

|---|---|---|

| 3.0% | £17,969 | £1,078,121 |

| 4.0% | £18,417 | £1,104,991 |

| 5.0% | £18,871 | £1,132,274 |

If you choose an interest-only mortgage, you’ll only pay the interest each month. This keeps your payments much lower. But the full £1 million loan will still need to be paid off at the end of the term.

Here’s what that might look like:

| Interest Rate | Monthly Payment (£) | Total Paid Over 5 Years (£) |

|---|---|---|

| 3.0% | £2,500 | £150,000 |

| 4.0% | £3,333 | £200,000 |

| 5.0% | £4,167 | £250,000 |

Take your time to explore your options. It’s always wise to speak with a mortgage broker for advice tailored to your circumstances.

And if you want to see an estimate of how much you’ll pay for your mortgage, use our mortgage calculator.

Choosing Your Million-Pound Home: Tips and Considerations

Selecting a million-pound home isn’t just about the price tag; it’s about finding the right fit for your lifestyle and future. Here’s some advice to guide your hunt:

- Choose Your Location Wisely. It’s an old saying but a relevant one. Consider the area’s prospects, amenities, and connectivity.

- Property Features. Make a list of what you want in a home – number of bedrooms, garden space, or maybe a home office. Prioritise your must-haves.

- Think Long-Term. Is the property likely to appreciate? Consider factors like upcoming infrastructure developments or school zones.

- Lifestyle Suitability. Does the property align with your lifestyle? A city-centre apartment offers a different life to a countryside mansion.

- Visit Multiple Times. Revisit the property at different times of the day to get a feel for the area and its dynamics.

- Professional Inspections. Invest in property checks. Surprises are great for birthdays, but not so much for house foundations.

- Negotiation is Key. Be ready to negotiate. The asking price isn’t always the final price, and there’s often room to manoeuvre.

Choosing your million-pound home should be a blend of practicality and aspiration. It’s a significant decision, so take your time, do your research, and make sure it’s a place you’ll be happy calling home.

How to Make a Million Pound Mortgage More Affordable

Thinking about a £1 million mortgage might make your wallet tremble, but there are ways to make it more manageable. Here’s how you can ease the financial load:

- Bigger Deposit. It’s straightforward – the more you put down initially, the less you have to borrow. A larger deposit can also nab you lower interest rates.

- Shop Around for Rates. Don’t just settle for the first offer. Shop around. Different lenders have different rates and terms. It’s like bargain hunting, but for mortgages.

- Consider Different Mortgage Types. Explore options beyond the standard repayment mortgage. An interest-only mortgage, for instance, can reduce your monthly outgoings, though you’ll need a solid plan to pay off the lump sum at the end.

- Remortgaging for Better Rates. If interest rates drop or your financial situation improves, refinancing can be a smart move. It’s like switching tracks for a smoother financial journey.

- Longer Mortgage Term. Stretching the mortgage over a longer period can reduce your monthly payments, but remember, this means you’ll pay more interest in the long run.

By employing these strategies, you can make a million-pound mortgage more affordable and avoid stretching your finances too thin.

Key Takeaways

- Getting a £1 million mortgage means planning carefully and understanding your financial situation and lender options. High-street banks are good for steady incomes, while private lenders can help if your income is less predictable, though their rates might be higher.

- Saving a bigger deposit (10–40% of the property’s price) can help you borrow less and get lower interest rates.

- Your monthly payments depend on the interest rate and how long you take to pay it off – shorter terms mean higher payments but less interest overall.

- You can make a £1 million mortgage easier by shopping around for better rates, refinancing later, or choosing a longer repayment period.

The Bottom Line

Getting a mortgage for a million-pound house is a big deal. It’s not just about your income or how good your credit score is. It’s also about the house you want to buy. This kind of mortgage is a big step, and there’s a lot to think about.

The smartest thing you can do is talk to someone who knows all about this stuff.

A mortgage broker is really helpful because they know all about big mortgages. They can help you find the right mortgage that fits what you need and what you can afford.

If you’re thinking about getting a big mortgage, we can help you find a specialist mortgage advisor. Just get in touch, and we’ll help you get started.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I get a million-pound buy-to-let mortgage?

Yes, it’s possible to get a buy-to-let mortgage for £1 million. These mortgages are based on the property’s potential rental income, which typically needs to cover 125% of your mortgage payments. Generally, you’ll need a deposit of at least 25%

Can I get a million-pound commercial mortgage?

Yes, commercial mortgages are available for amounts like £1 million. These are used for buying commercial properties and are tailored to your business’s specific needs. Working with a specialist broker can help you find the best option for your situation.

Related Articles

Private Mortgage Lenders Explained

You didn’t get where you are by settling for ordinary, so why start now? Regular mortgages might work for most people, but when you’re dealing with serious wealth, they just don’t measure up. Private mortgages, on the other hand, are in a league of their own. Whether it’s a stunning countryside estate, a sleek London […]

Securing High Net Worth Mortgage In The UK

If you’re wealthy, regular mortgages probably don’t work for you. You need something designed to match your lifestyle and financial goals. The good news? With the right mortgage advisor, buying a high-value property or using your assets for smart investments can be simple. This guide breaks down high-net-worth mortgages in 2025, so you can see […]

The Complete Guide To Asset Based Mortgages In the UK

Lenders often seem to miss the bigger picture when it comes to wealth. You could have millions in property, shares, or investments, but if your income doesn’t tick their boxes, they might still turn you down for a mortgage. That’s where asset-based mortgages come in. Instead of focusing on your income, these mortgages consider the […]