How to Afford a Mortgage When It Feels Impossible

Understanding mortgages can be daunting, especially if owning a home feels out of reach. But don’t worry—there are ways to make it possible.

Whether you’re finding it hard to save for a deposit, worried about monthly payments, or unsure about your options, this guide will help you improve your chances of getting a mortgage.

Can’t Afford to Buy a House in the UK?

Buying a house is a huge financial step, and it can feel overwhelming when the numbers don’t add up.

But before you give up, it’s worth looking into all the options that can help you afford a home in the UK.

Mortgage affordability isn’t just about your current bank balance. Lenders look at various factors, including your income, credit score, employment status, and existing debts.

By organising your finances and knowing what to expect, you can improve your chances of getting on the property ladder.

What to Do If You Can’t Afford a Mortgage?

If you’re worried that you can’t afford a mortgage, take a deep breath—there are steps you can take to turn things around.

Start by looking at the key factors lenders consider:

Income Multiples

Most lenders in the UK use an income multiple of 4-4.5 times your salary to determine how much you can borrow.

But did you know some lenders offer higher multiples, up to 5 or 6 times your salary?

This can make a big difference, especially if you’re on a tight budget.

Speak to a mortgage broker to find out which lenders offer higher income multiples that suit your situation.

Save for a Big Deposit

Saving for a big deposit is important.

The larger the deposit, the lower the Loan to Value (LTV) ratio, and the more favourable the mortgage terms.

Try to save at least 10-20% of the house price. This will make your mortgage cheaper and easier to get.

If saving a large deposit seems tough, you can explore government schemes and family help mortgages, which we’ll discuss here.

Government Schemes

The government has schemes to help you buy a home. These schemes make it easier and cheaper to own a home.

Some of these schemes are:

- Help to Buy

- Shared Ownership

- Right to Buy

- Right to Acquire

- Mortgage Guarantee Scheme (ends in June 2025)

- First Homes

- Deposit Unlock Scheme

To qualify, you usually need to be a first-time buyer or someone who doesn’t currently own a home.

The house you buy must be under a certain price, and your income might need to be below a certain amount.

These rules make sure that the schemes help people who need them most.

Family Help

If your family can help, there are ways to make buying a home easier.

- Gifted deposit. Your family can give you money for a deposit.

- Guarantor mortgage. A family member can guarantee your mortgage.

- Offset mortgage. Your family’s savings can help reduce your mortgage interest.

- Joint mortgage. You can buy a house with a family member.

- JBSP mortgage. A family member can help you get a mortgage without owning the house.

- Family Springboard Mortgage. A family member can save money in a linked account to help you get a better deal.

Maximise Your Income

Lenders don’t just consider your basic salary.

If you earn extra income through bonuses, overtime, or a side hustle, you can include this in your mortgage application.

Some lenders also count certain benefits as income. Be sure to gather proof of all your income sources to strengthen your application.

While some lenders limit how much extra income you can declare, a good mortgage broker can often help you declare 100% of it.

Improve Your Credit Score

A good credit score can be your ticket to a better mortgage deal. If your score isn’t great, it’s worth improving it before you apply.

Start by checking your credit score with the three main credit reference agencies in the UK: Experian, Equifax, and TransUnion.

Each one might have slightly different information, so it’s important to check all three.

When reviewing your credit score, look for any errors and correct them if needed.

Simple actions like paying off debts, avoiding missed payments, and keeping your credit use low can boost your score.

Also, avoid applying for new credit close to your mortgage application, as multiple credit checks can reduce your score.

Can’t Afford a Joint Mortgage on Your Own?

If you’re sharing a mortgage with a partner or family member who can no longer contribute, it can quickly become stressful.

Here are some options to consider:

Death of a Joint Owner

If the person you share the mortgage with passes away, you might be left paying the full amount on your own.

Life insurance can help cover the mortgage, giving you some financial relief during a difficult time.

It’s wise to plan ahead by setting up insurance that ensures your mortgage is covered if the worst happens.

A good broker can help you create a plan that suits your needs.

Divorce or Separation

During a divorce or separation, it’s crucial to act quickly to protect your credit score and finances.

You could sell the home, have one partner buy out the other, or keep paying the mortgage together while living separately.

In some cases, both of you may continue paying off the mortgage and retain a stake in the property.

It’s a good idea to discuss your options with a mortgage broker who can guide you on the best steps to take.

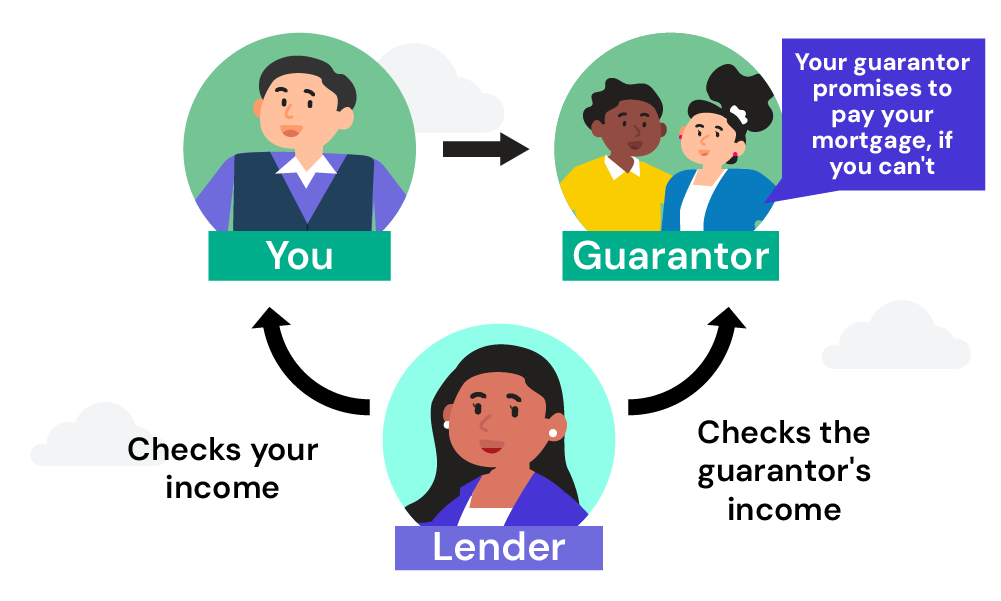

Guarantor Mortgages

If you’re struggling to afford the mortgage on your own, a guarantor mortgage might help.

A family member or friend can act as your guarantor, agreeing to cover any missed payments, which can increase your chances of keeping your home.

Can’t Afford Your Existing Mortgage?

If rising interest rates and living costs are making it tough to keep up with your mortgage payments, you’re not alone. Here’s what you can do:

Talk to Your Lender

They may be able to help. Ask about options like taking a payment holiday or switching to an interest-only mortgage.

But, before you do, it’s wise to understand your finances clearly, so consider getting advice from a mortgage advisor.

This can be a good way to get a better deal on your mortgage. You might be able to get a lower interest rate or a longer mortgage term.

This can help you save money on your monthly payments.

Even if you have a variable mortgage, where the interest rate can change, switching to a mortgage with a fixed interest rate can give you more certainty and save you money.

Switch to Interest-Only

If you have a repayment mortgage, switching to an interest-only mortgage can lower your monthly payments.

This can be arranged with your current lender or a new one and may be a temporary or long-term solution.

Taking in a Lodger

Renting out a room in your home can be a simple way to generate additional income.

Before taking this step, check with your lender to ensure it won’t affect your mortgage agreement.

Request a Payment Holiday

Some lenders may allow you to take a break from mortgage payments for a pre-agreed period, providing some breathing room.

This option became more common during the coronavirus pandemic and may still be available.

If you’re over 55 and struggling with mortgage payments, equity release allows you to access the value tied up in your home.

This can provide a lump sum or regular payments, easing financial pressures, and may even eliminate monthly payments altogether.

A second charge mortgage lets you borrow extra money against the equity in your home without changing your current mortgage.

This can be helpful if you need funds but want to keep your existing mortgage rate.

Government Support Schemes

If you’re struggling to pay your mortgage, government schemes might help.

In England, the Support for Mortgage Interest (SMI) scheme offers assistance, but it’s now a repayable loan.

Scotland and Wales have their own similar support schemes.

Key Takeaways

- If buying a house feels impossible, explore options like saving a larger deposit, using government schemes, and seeking family help.

- If you can’t afford a joint mortgage due to a partner’s death or separation, consider selling the property, buying out the other party, or using a guarantor mortgage.

- If struggling with mortgage payments, talk to your lender about remortgaging, switching to interest-only, or taking a payment holiday.

The Bottom Line

Getting a mortgage today isn’t just about money—you need to understand your options and any challenges that might come up.

Your Loan to Value (LTV) ratio, credit history, and the type of property you want can all affect your mortgage approval and the terms you’re offered.

With recent changes in government schemes and lending policies, staying informed is key.

A good mortgage advisor can offer personalised advice, helping you explore your options and make the best decisions. They can help you with the application, negotiate better deals, and avoid making mistakes.

If you want to save time and stress finding the right broker, get in touch with us. We’ll connect you with a trusted broker who can assist with your specific mortgage needs.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

How can I afford a second mortgage?

If you’re struggling, consider remortgaging onto a buy-to-let (BTL) mortgage and using rental income to cover the payments. Discussing your situation with a broker can help you find the best approach.

What should I do if I can’t afford my mortgage during maternity leave?

You may be able to take a payment holiday or adjust your mortgage term. A mortgage advisor can guide you to the best option.

What can I do if I can’t afford this month’s mortgage payment?

Get professional advice immediately. An expert can help you assess what you can afford and approach your lender with a plan.

How long can I freeze my mortgage for?

The length of a payment holiday varies by lender. It can range from a month to a year, depending on your lender’s policies.

How can I afford a mortgage if I have bad credit?

Improve your credit score before applying, or explore bad credit mortgage options with the help of a broker.

Can I get a mortgage if I’m self-employed?

Yes, but you may need to provide more evidence of your income. Keeping detailed records and staying in the same job can improve your chances.

Is it possible to buy a house without a deposit?

Yes, some government schemes and family assistance options allow you to buy a house with little or no deposit.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Getting a Mortgage with Student Loans: What to Know

As someone looking to get on the property ladder, you already know how important it is to have your finances in order. For many, student loans are a big part of that picture, especially when the average student debt for recent graduates in the UK is £45,600. While it may sound like a lot, student […]

Does Overdrafts Affect Your Mortgage Application?

When you’re on the path to homeownership, every financial detail matters. From saving for a deposit to ensuring your credit score is in top shape, the journey is full of hurdles. But what about that overdraft you’ve been dipping into? Can it really affect your mortgage application? Let’s break it down. Can an Overdraft Impact […]

Does Renting Affect Your Mortgage Application?

In today’s housing market, many people find themselves renting for longer periods before making the leap to homeownership. But what happens when your renting history includes missed payments? Can these rent arrears affect your ability to get a mortgage? This article delves into how rent arrears could influence your mortgage application and what you can […]