- What Are the Requirements for a Mortgage in the UK?

- What Do I Need to Get a Mortgage?

- What’s the Mortgage Application Process in the UK?

- How Long Does It Take to Get a Mortgage Approved?

- How Much Can I Borrow?

- Should You Use a Mortgage Broker?

- Does Having Bad Credit Require a Different Criteria?

- Are There Extra Steps for the Self-Employed?

- How Can I Speed Up My Mortgage Approval?

- What if My Mortgage Application is Rejected?

- The Bottom Line

How To Get A Mortgage Approved In The UK?

Imagine this: you’ve found your dream home – a charming little terrace in Manchester, perhaps, or a spacious semi-detached in Surrey.

Now, all that stands between you and those front door keys is the hurdle of getting a mortgage.

If you’re like most Brits, you’re probably full of questions. How much can I borrow? Will my credit score cut it? What if I’m self-employed? And how long will this all take?

The idea of piles of paperwork and potential rejection can make anyone think twice about buying.

But don’t worry – getting a mortgage approved isn’t as scary as it seems. Whether you’re a first-time buyer or remortgaging, we’ve got you covered.

This guide covers everything about how to get a mortgage approved in the UK.

What Are the Requirements for a Mortgage in the UK?

Before you start house hunting, it’s essential to understand what lenders are looking for.

Here are the key requirements you’ll need to meet:

- Age – Most lenders require you to be at least 18 years old. There’s also usually an upper age limit, typically between 75 and 80 when you take out the mortgage, or 75 to 95 when your mortgage term ends.

- Employment and Income – Lenders want to see a stable income. If you’re employed, you’ll generally need to provide your last three payslips. Self-employed? Be prepared to show 2-3 years of certified accounts.

- Credit Score – Your credit history plays a significant role. Lenders will check your credit report to assess how well you’ve managed past debts. Don’t worry if your credit isn’t perfect – there are still options available, but you might face higher interest rates.

- Deposit – The bigger your deposit, the better your chances of approval. Most lenders require at least a 5% deposit but aim for 10-20% if possible. You’ll need to prove where your deposit came from, so keep clear records.

- Affordability – Lenders will assess your income against your outgoings to ensure you can afford the repayments. They’ll typically offer 4.5 times your income, but some may stretch to 5 or even 6 times.

- Property Type – Standard properties are easier to mortgage. If you’re buying a non-standard property (like a thatched roof house or a flat above a shop), you might have fewer lender options.

What Do I Need to Get a Mortgage?

Gathering the right documents can speed up your application process. Here’s what you’ll typically need:

- Proof of income (payslips, P60s, accounts if self-employed, tax returns, etc.)

- Proof of income/affordability (3+ months of bank statements)

- Workings for any bonuses/commissions

- Proof of deposit source (savings, gift letter if family helped, etc.)

- Proof of identity (passport, driving licence)

- Proof of address (utility bills, bank statements)

- Details of any debts/loans/credit commitments

- College transcripts if you’ve recently graduated

- Cost breakdown for the property

- Hired conveyancer/solicitor details

- Divorce/separation paperwork if applicable

Remember, having these documents ready can significantly reduce the time it takes to get your mortgage approved.

What’s the Mortgage Application Process in the UK?

Understanding the process can help you navigate it more smoothly. Here’s a step-by-step guide:

- Get a Mortgage in Principle – This gives you an idea of how much you can borrow and shows sellers you’re serious.

- Find a Property – Once you’ve got your agreement in principle, start house hunting!

- Make an Offer – When you find your dream home, put in an offer.

- Full Mortgage Application – If your offer is accepted, it’s time to submit your full mortgage application.

- Property Valuation – The lender will arrange a valuation to ensure the property is worth what you’re paying.

- Underwriting – The lender reviews all your information to make a final decision.

- Mortgage Offer – If approved, you’ll receive a formal mortgage offer.

- Exchange and Completion – Your solicitor will handle the legal work, leading to exchanging contracts and completing the purchase.

>> More about How To Get a Mortgage?

How Long Does It Take to Get a Mortgage Approved?

The million-pound question! The time it takes can vary, but here’s a rough timeline:

- Agreement in Principle – This can often be done in a matter of hours or a few days.

- Full Application to Offer – On average, this takes 4-8 weeks. However, it can be quicker if you’re well-prepared, or longer if there are complications.

- Offer to Completion – This typically takes 3-6 weeks but can be longer if you’re in a property chain.

Remember, these are average timelines. Your application could be faster or slower depending on various factors.

How Much Can I Borrow?

“How long is a piece of string?” It’s the mortgage equivalent of asking how much you can borrow.

But let’s cut through the ambiguity.

Most lenders in the UK will offer you 4.5 times your annual income. Some might stretch to 5 times, and a select few could go up to 6 times.

But here’s the rub: it’s not just about your salary.

Lenders are nosy. They want to know about your outgoings, your debts, even your spending habits. That £5 daily coffee habit? It matters.

Here’s a quick way to estimate:

- Take your annual income.

- Multiply it by 4.5.

- Subtract any outstanding debts.

But remember, this is just a starting point. Your actual borrowing power could be higher or lower.

The real question isn’t how much you can borrow. It’s how much you should borrow.

Can you comfortably afford the repayments? Will you still have a life after paying your mortgage each month?

Because a mortgage isn’t just a loan. It’s a lifestyle choice. Choose wisely.

Want a more accurate figure? Talk to a mortgage broker. They’re like GPS for the mortgage maze. They know the shortcuts, the dead ends, and the fastest route to approval.

Remember, the biggest mortgage isn’t always the best mortgage. The best mortgage is the one that lets you sleep at night, knowing you’re not overextended.

So, how much can you borrow? Enough to get you home, without losing your shirt in the process.

Use our mortgage calculator to get a quick estimate.

Should You Use a Mortgage Broker?

Using a mortgage broker can significantly boost your chances of getting approved.

Brokers have access to a wide range of lenders and can find the best deals tailored to your specific needs. They also handle much of the paperwork and communication, saving you time and effort.

A broker can guide you through the entire process, from preparing your application to finding the right lender, making the journey to homeownership smoother and less stressful.

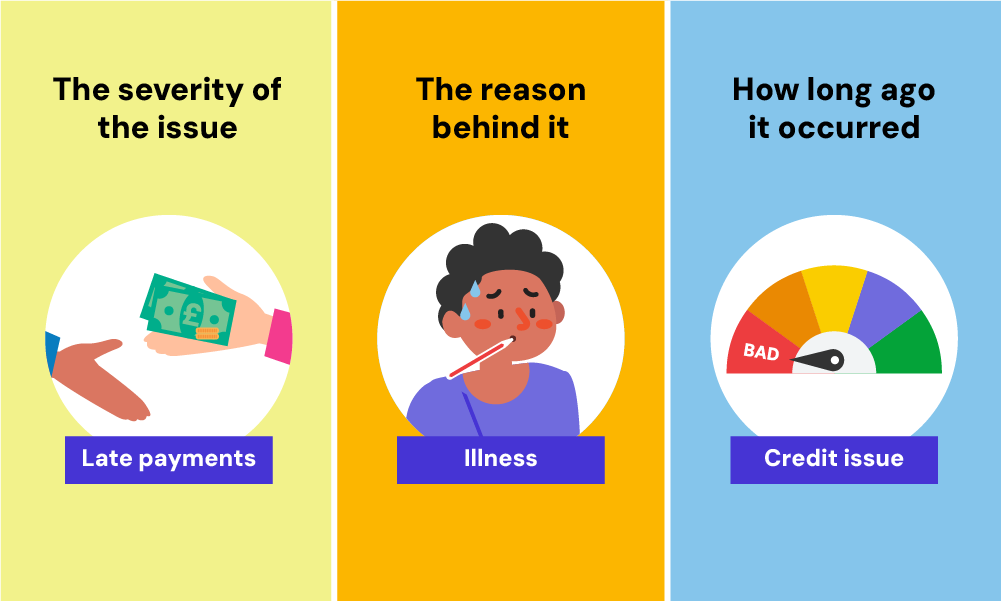

Does Having Bad Credit Require a Different Criteria?

Every lender has its own criteria for assessing applicants with bad credit, but generally, they’ll look at three factors:

- The severity of the issue. Minor issues like a few late payments won’t hurt as much as major problems like bankruptcy.

- The reason behind it. Lenders may consider the reasons behind your bad credit. A one-off issue due to illness, for example, might be viewed more favourably than persistent financial mismanagement.

- How long ago it occurred. The more recent the credit issue, the more impact it’ll have. Most lenders are more lenient about problems from 3+ years ago

Some lenders are more lenient and may still approve your application, though you might face higher interest rates and higher deposit requirements.

Seeking advice from a mortgage broker who specialises in bad credit can be beneficial, as they know which lenders are more likely to approve your application.

Are There Extra Steps for the Self-Employed?

Being self-employed doesn’t bar you from getting a mortgage, but you’ll need to jump through a few extra hoops. You’ll need to have:

- At least two years of business accounts, certified by an accountant. Some may accept one year, while others might ask for three.

- SA302 forms from HMRC showing your tax calculations are often required alongside your accounts.

- Business bank statements, usually for the last 3-6 months.

- Evidence of future work if you’re a contractor.

- Details about your business structure and your share of the company if you’re a company director.

- A projection of future earnings from your accountant, if requested by the lender.

It’s worth noting that lenders will typically use an average of your last 2-3 years’ income to calculate how much you can borrow.

If your income fluctuates, they might use a lower figure or an average.

Consider working with a mortgage broker who specialises in self-employed mortgages. They can guide you to lenders who best understand your financial situation and improve your chances of approval.

How Can I Speed Up My Mortgage Approval?

Want to fast-track your approval? Here are some top tips:

- Get Your Paperwork in Order. Have all your documents ready before you apply. This includes proof of income, bank statements, identification, and details of your current debts. Keeping everything organised and easily accessible can save valuable time.

- Check Your Credit Report. Address any issues before applying. Make sure your credit report is accurate and up-to-date. Dispute any errors you find and consider paying down outstanding debts to improve your credit score.

- Avoid Major Financial Changes. Don’t switch jobs, open new credit accounts, or make large purchases during the application process. Lenders prefer stability, and significant changes can delay approval.

- Be Honest and Accurate. Provide complete and truthful information on your application. Inaccuracies can cause delays or even lead to a rejection if discovered during the underwriting process.

- Consider Using a Mortgage Broker. They can match you with the right lender and help navigate the process. Brokers have access to a wide range of lenders and can often find deals that you might not discover on your own.

- Respond Quickly. If the lender needs additional information, provide it promptly. Delays in your response can slow down the approval process.

- Prepare for the Valuation. Ensure the property is ready for the lender’s valuation. Address any minor repairs or issues that could negatively impact the valuation.

- Maintain a Stable Financial Profile. Keep your financial situation as steady as possible. Avoid changing your spending habits, and ensure your bank account remains healthy.

- Seek Pre-Approval. Get a mortgage pre-approval or agreement in principle. This can speed up the final approval process as much of the groundwork will already be done.

- Improve Your Debt-to-Income Ratio. Pay down existing debts to lower your debt-to-income ratio. Lenders look favourably on applicants with lower ratios, as it indicates a better ability to manage mortgage repayments.

- Have a Larger Deposit. The bigger your deposit, the more favourably lenders will view your application. Aim for a deposit of 10-20% to increase your chances of faster approval.

- Choose the Right Lender. Some lenders are known for their quick turnaround times. Research and select a lender with a reputation for fast processing.

What if My Mortgage Application is Rejected?

Don’t panic! A rejection isn’t the end of the road.

First, find out why your application was rejected. Understanding the reason can help you address the issue.

Next, work on improving your application by focusing on the areas that led to the rejection, whether it’s saving a bigger deposit or improving your credit score.

Consider alternative lenders, as some specialist lenders cater to those who’ve been rejected by mainstream banks.

Seeking professional advice from a mortgage broker can also be beneficial, as they can help you find lenders more likely to accept your application.

The Bottom Line

Getting a mortgage approved in the UK can seem daunting, but with the right preparation and knowledge, you can handle it.

Remember, each application is unique, and what works for one might not work for another. The key is to be well-prepared, patient, and seek help when needed.

Whether you’re a first-time buyer or remortgaging, understanding mortgage approval can make your path to homeownership smoother.

So, gather your documents, improve your credit score, and take that first step towards approval.

To boost your chances of approval, get in touch. We’ll connect you with a qualified mortgage broker who can help with your application and secure the best deal.

Happy mortgage-hunting!

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]