Decoding Age Caps: What’s the Maximum Age for Mortgages?

Turning 50 (or beyond) can make you wonder, “Am I too old to get a mortgage now?”

It’s a fair question—and the answer might surprise you.

The good news?

There’s no hard-and-fast rule that says you’re too old for a mortgage in the UK. Sure, your age might influence your options, but it doesn’t slam the door shut on your borrowing journey.

In fact, many lenders have products tailored for later stages in life, so your options could be more flexible than you think.

But what’s the deal with age limits? Is there really a maximum age for getting a mortgage?

Not exactly—and that’s what we’ll explore here.

We’ll break down how age plays a role in your mortgage choices, what it means for you, and how to handle this stage of life confidently.

Because while age might matter, it’s not the whole story when it comes to securing a mortgage.

Let’s get started!

How Does Age Affect Mortgage Eligibility?

Age is often viewed as a major barrier when it comes to mortgage eligibility.

It’s an accepted fact that as you age, you may pose a higher risk to lenders, making it more challenging to secure a loan.

Why is that so? Two main reasons: a potential decline in income and the onset of health issues.

After retirement, your steady income from work stops. While you might have a pension, it’s often hard for lenders to pinpoint your exact earnings.

This uncertainty around income can impact the assessment of your mortgage affordability.

Health also becomes a concern as you age. There’s the unfortunate truth that older people are more likely to develop health complications.

This means you’re less likely to live long enough to pay off a 25 to 30-year mortgage. To lessen this risk, most lenders set maximum age limits for mortgages.

Age Milestones and Their Impact on Mortgages

Here’s how crossing certain age milestones can change your mortgage options:

Mortgages for Over 50s

At this stage, you’re in a good place. There’s a wide variety of regular-term options with competitive rates available.

While a stable income and good credit score can open the doors to better deals, still you need to provide evidence of predicted retirement income.

The crucial point to consider is that this could be the last time you’ll have this much mortgage flexibility, so make the most of it.

If you’re thinking about paying off your mortgage early or releasing some equity, now’s the time. But remember, none of these options are risk-free. So it’s important to understand how they work before you make any decisions.

Mortgages for Over 60s

Things start getting a bit tricky. Some benefits from your 50s might still be open. But, you may notice that your options become slightly more restricted.

As retirement approaches, you’ll likely need to provide more proof of retirement income. Regular pension, other investment income, or part-time work income can serve as proof.

Remember, lenders, are looking for assurance that you can repay the loan.

Mortgages for Over 70s

Mortgage term lengths become shorter, usually 10-15 years. You can also consider guarantor mortgages, where a family member agrees to pay your mortgage if you can’t.

But it’s worth noting that some lenders are more flexible than others. You may have more options available depending on your circumstances.

Mortgages for Over 80s

Mortgage options are even more limited and your financial history will be carefully examined. Be ready for extensive financial checks and make sure you have all your documents in order.

| AGE BRACKET | LIKELIHOOD OF APPROVAL | LENDER’S PERSPECTIVE |

|---|---|---|

| Over 50s | High | Many lenders cater to this age group with standard terms and good rates. |

| Over 60s | High to Fair | Affordability is key, even as lenders start to impose age caps. |

| Over 70s | Fair to Moderate | Lenders are fewer. Some accept up to age 75, others up to 80 if criteria are met. Terms may shorten. |

| Over 80s | Moderate to Low | Specialised lenders remain. Shorter terms, higher rates, and strict terms are common in this age. |

What Mortgage Options are Available for Older Borrowers?

Age can undeniably work against you when it comes to securing a mortgage in the UK. As time progresses, your choices become increasingly restricted, regardless of your personal circumstances.

Let’s take a closer look at the possibilities that open up once you reach the significant milestone of turning 50, and subsequent moments along the way.

Retirement Interest-Only Mortgage

With this option, you only pay the interest on the loan. The capital is paid back when the house is sold, which is usually after death or moving into long-term care.

This is a good fit if you have a stable retirement income that can cover the interest payments.

Lifetime Mortgage

This is an equity release option for folks over 80. You borrow a part of your home’s value. The loan plus interest is repaid when the house is sold, often when you move into long-term care or pass away.

This can be a good option for you if you need extra cash to fund your retirement or other expenses.

Home Reversion

This is a form of equity release. You sell part or all of your home to a reversion company in exchange for a lump sum of cash or regular income.

You can continue to live on the property for the rest of your life. You also don’t have to make any repayments on the loan until they die.

It may be a good choice if you’re not concerned about leaving your entire property as an inheritance.

Older People’s Shared Ownership (OPSO)

If you’re 55 or over, you can buy 25% to 75% of your home and pay rent on the rest with this shared ownership scheme.

This can be beneficial if you’re looking to downsize or move to a more suitable property but are finding costs prohibitive.

While these options might not suit everyone, they prove that getting a mortgage in retirement is still possible.

What Other Factors Affect Mortgage Eligibility in Retirement?

When you’re looking to get a mortgage after retirement, there are a few things to consider. This may include factors like affordability, term length, loan-to-value ratio, property type, and more.

Affordability

Can you afford the repayments? That’s the key question here.

Proving that you can meet monthly repayments is paramount to your mortgage approval.

Lenders need solid evidence of your capability, or your mortgage application might not pass the starting gate. For retirees, the income used to show this affordability is often pension-based.

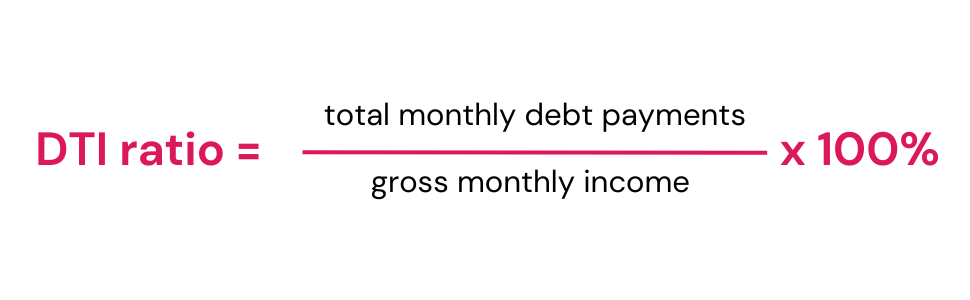

Most lenders use a Debt-to-Income (DTI) ratio to assess your affordability. Simply put, it’s a percentage that shows how much of your monthly income goes towards paying off debts.

Here’s the formula to calculate:

If your monthly income is £2,000 and your debts are £500, your DTI is 25% (500/2000 x 100 = 25). Generally, a lower DTI is preferable. It’s best to aim for at least 36% to 43% DTI.

Moreover, your affordability will also help lenders assess how much to lend you. They’ll usually cap your loan at 3-4.5 times your annual income, but it all depends on your circumstances.

Some lenders may be more lenient and offer flexible borrowing and eligibility criteria.

To check you DTI ratio, use our calculator here.

Mortgage Terms

Many UK lenders have age restrictions.

For example, the maximum age to get a new mortgage is usually between 65 and 70, and the mortgage should be paid off by the time you’re 80-85.

If you’re 65 and looking for a new mortgage. Lenders might be hesitant to offer you a 25- to 30-year term, fearing you might cross their upper age limit halfway through.

But don’t worry, some specialist lenders might be willing to help. They might offer you a shorter borrowing term with higher monthly repayments if you can afford it.

Loan-to-Value (LTV)

The LTV ratio is the proportion of your home’s value that you’re borrowing money for. A higher deposit means a lower LTV, which gives you access to more lenders and better interest rates.

For repayment mortgages, lenders typically approve up to 80% LTV.

Some might even approve 85% LTV, and a few might go as high as 95% LTV, but only if you meet other eligibility criteria.

For interest-only mortgages, the maximum LTV is usually 85%. This drops to around 75% for older borrowers.

In general, a lower LTV means you’re borrowing less money. This means you’ll have lower monthly payments and you’ll build equity in your home more quickly.

You’ll also have more options when it comes to lenders and interest rates.

It’s important to consider your circumstances and budget when deciding how much mortgage you can afford.

To check you LTV ratio, use our loan-to-value ratio calculator.

Other Influential Factors

The type of property can also influence your mortgage eligibility.

Non-standard properties carry certain risks and challenges that might make lenders think twice. For example, unconventional constructions might be seen as riskier.

Moreover, poor credit history or recent adverse financial events could limit your options. Although some specialist lenders may still consider your application.

In sum, there are many factors at play when securing a mortgage in retirement. Being prepared and informed can help navigate this complex landscape.

Key Takeaways

- Age does affect getting a mortgage. When we retire, income drops and health risks rise, but it doesn’t mean you can’t get a mortgage.

- Depending on how old you are, your mortgage options will differ. If you’re over 50, you’ll have lots of choices. As you get older, these choices become less, but options are still available, especially if you have a solid financial history.

- There are special mortgages designed for older people. These include Retirement Interest-Only Mortgages, Lifetime Mortgages, Home Reversion schemes, and Older People’s Shared Ownership schemes.

- Besides your age, other factors like affordability, mortgage term length, loan-to-value ratio, property type, and credit history can impact your ability to get a mortgage.

The Bottom Line

While age can pose a challenge to securing a mortgage, it’s far from an insurmountable hurdle. With the right knowledge, preparation, and specialist broker, you can make your dream of owning a home in your golden years a reality.

If you’re looking for more guidance, team up with a seasoned mortgage broker. They can take the hassle out of your mortgage journey, making it straightforward and worry-free.

The best part? They can unlock doors to favourable terms and opportunities, possibly leading you to a better mortgage deal.

Fill out this quick form today and we’ll match you with a good mortgage broker who can help you find the right mortgage for your retirement.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

At what age can you typically finish paying off your mortgage?

Most people aim to have their mortgage paid off by the time they reach retirement, typically between ages 65-70.

However, this can vary greatly depending on personal circumstances and the type of mortgage.

What is the usual term length for a mortgage?

The standard term length for a mortgage is usually between 25 to 30 years. However, it can be shorter or longer depending on your financial situation, age, and the specific mortgage product you choose.

Are there age limits in place for buy-to-let mortgages?

Age limits for buy-to-let mortgages can vary significantly between lenders. Some may have no upper age limit, while others may require the mortgage to be fully repaid by a certain age, typically between 70-75.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How to Get the Best Mortgages for Older Borrowers in 2025?

Older borrowers in the UK are getting more mortgages than ever. In the third quarter of 2024, 33,840 new loans went to people over 55—a 2% rise from 2023. These loans were worth £5.2 billion, nearly 10% more than the year before. For the first time, over half of new mortgages will go beyond the […]

Is a Reverse Mortgage Right for You? A Guide in 2025

Retirement should be about relaxation, not money worries. But, for many homeowners, the pension pot only goes so far. If you’re feeling the pinch, your property could offer a solution: a reverse mortgage. Sound complex? It doesn’t have to be. In this guide, we’re simplifying reverse mortgages. You’ll discover what they are, how they work, […]

Best Retirement Mortgage Providers in the UK in 2025

When you’re thinking about buying a house, one of the key steps in that journey involves finding a good mortgage lender. Why is this important? Simply put, a mortgage lender provides the financial backing that makes buying a house a feasible option. It’s a lot easier to pay back the cost of a home over […]