- What is a Retirement Mortgage Calculator?

- How to Use Retirement Mortgage Calculators?

- How Lenders Calculate Your Retirement Mortgage Amount

- Impact of Age on Retirement Mortgage Calculations

- Equity Release: Exploring Beyond Standard Retirement Mortgages

- Can Pensioners Get Mortgages Even with Bad Credit?

- Key Takeaways

- The Bottom Line

How are Retirement Mortgages Calculated?

From the calculator apps that guide our finances to the digital tools that aid our retirement planning, the digital era has become an invaluable partner in our financial journey.

Whether you’re a retiree, soon-to-be pensioner, or just someone planning for their golden years, you’re likely to have some interaction with a Retirement Mortgage Calculator.

But what else can you use to get the most out of your retirement planning?

And how do these tools fit into your larger financial landscape?

This guide aims to help you understand how these tools work, what factors they take into account, and how they can help you plan better for your mortgage in your later years.

Plus, we’ll explore the different mortgage products available for retirees and how these calculators can help you assess the best options for your circumstances.

The goal here is not just to understand these tools, but to make them a natural extension of your financial management strategy.

What is a Retirement Mortgage Calculator?

A retirement mortgage calculator is a tool designed to estimate the mortgage amount that you could potentially borrow for in retirement. But why is this tool important?

Mortgages can be tricky, especially when you’re planning for or are already in your retirement years. Factors like your age, income, equity in your home, health, and the type of mortgage product you choose, all play a role in determining your borrowing power.

A retirement mortgage calculator simplifies this process. It gives you an idea of what’s financially feasible before you even approach a lender.

Now, let’s dig a bit deeper and understand the types of retirement mortgage products that could be on your radar. These options usually include:

- Retirement Interest Only Mortgages (RIOs)

- Equity Release Mortgages such as Lifetime Mortgages and Home Reversion

- Government Schemes such as Older People Shared Ownership

- Remortgages

Each has its unique features, benefits, and potential drawbacks. A retirement mortgage calculator can be a handy tool to see how each product might affect your financial situation.

This will enable you to make an informed choice that best aligns with your mortgage plans and lifestyle expectations during your senior years.

How to Use Retirement Mortgage Calculators?

After knowing what is a retirement mortgage calculator and why it’s important, let’s talk about how lenders use it.

Lenders use retirement mortgage calculators to get a rough idea of how much money they can lend to you. They take into account your age, income, and the value of your home.

The calculator can also help you understand how different mortgage products might work for you. But remember, it’s just a tool to guide your understanding.

The actual amount you can borrow will depend on the lender’s criteria and other factors.

Here’s a simplified table to illustrate this:

| PENSIONER MORTGAGE PRODUCT | DEFINITION | HOW A CALCULATOR CAN HELP |

|---|---|---|

| Retirement Repayment Mortgage | A mortgage where the borrower is required to pay both the loan and interest in fixed instalments over a set period. | A calculator can help estimate your potential monthly repayments and the overall cost of the mortgage, aiding in budget planning. |

| Retirement Interest-Only Mortgage (RIO) | Similar to a standard interest-only mortgage, the loan is typically repaid when you die, move into long-term care, or sell the house. | A calculator can assist in estimating your potential monthly interest payments, helping you decide if a RIO could be a sustainable option for your retirement years. |

| Hybrid Equity Release | This scheme requires you to pay the loan’s interest monthly, but you can opt to cease payments at any time, accruing the interest to your loan which is paid off when you pass away or move into residential care. | Demonstrates the overall cost of the loan if you choose to make regular interest payments versus deferring all payments. |

| Equity Release | A way for older homeowners to release the wealth tied up in their property without having to move. Includes Lifetime Mortgages and Home Reversion Plans. | A calculator can help you see how much you could potentially release and the impact it might have on the inheritance you can leave behind. |

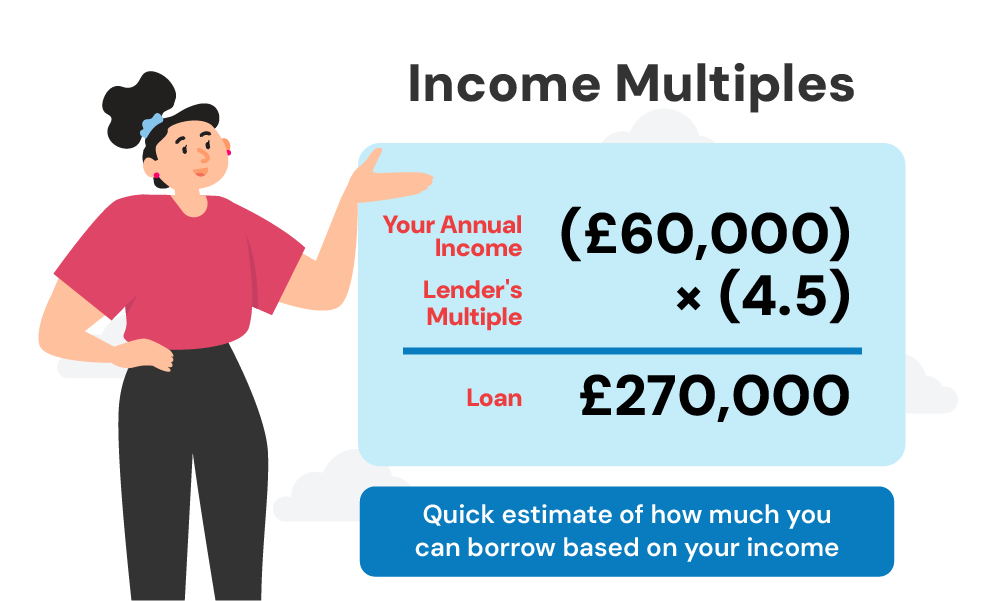

How Lenders Calculate Your Retirement Mortgage Amount

How much you can borrow in retirement depends on your income and circumstances. Normally, for repayment mortgages, lenders in the UK will use income multiples.

This is usually capped at 4-4.5 times your annual income, but some may make exceptions in certain cases.

To visualize this, let’s assume a retiree’s annual income stands at £35,000:

| INCOME MULTIPLIER | POTENTIAL LOAN AMOUNT |

|---|---|

| 4x | £140,000 |

| 5x | £175,000 |

| 6x | £210,000 |

But, it’s important to bear in mind that post-retirement, some lenders might limit the Loan-to-Value (LTV) ratio to 50%, attributing to the increased risk linked with your non-working status.

But fear not – this is not a universal rule. Many specialist lenders can offer appropriate mortgage solutions tailored to your circumstances.

Impact of Age on Retirement Mortgage Calculations

Your age plays a crucial role when working out mortgage terms.

While most online calculators default to a standard repayment term of 25 years, lenders tend to shorten this term when dealing with pensioners. But why does this happen?

Consider a simple example. Let’s imagine Barbara, a spirited lady of 70, who wishes to borrow £100,000.

Now, if we spread her repayments over a traditional term of 25 years, Barbara would be 95 before her mortgage is fully paid off.

Given the average life expectancy in the UK, this poses a higher risk for lenders, as it increases the possibility of Barbara passing away before settling her mortgage.

That’s why your age directly influences how easily you’ll secure a lender. Here’s a brief snapshot of how lenders usually respond to different age brackets:

| AGE BRACKET | LIKELIHOOD OF ACCEPTANCE | LENDER’S STANCE |

|---|---|---|

| Over 55-65 | High Acceptance | Majority of lenders consider, presenting the widest range of mortgage options. |

| Over 65-75 | Fair to Moderate Acceptance | Fewer lenders may be willing to consider, resulting in a somewhat restricted pool of mortgage options. |

| Over 76+ | Low Acceptance | Very few lenders are likely to consider this due to higher perceived risks, leading to significantly limited mortgage options. |

It’s worth noting, though, that some lenders cater specifically to older applicants, even those aged 85 and above.

A handful of lenders don’t set upper age limits, focusing instead on your ability to repay the mortgage. The key here is to research thoroughly and explore all options available to you.

Equity Release: Exploring Beyond Standard Retirement Mortgages

If you’re over 55, you might qualify for an equity release loan. But if you’re older, you could potentially unlock even more value from your home.

Why is this so?

Lenders often perceive a shorter life expectancy as a decrease in risk, as it usually means a quicker repayment of the loan.

For example, let’s say a homeowner aged 80 wants to take out an equity release loan.

Due to their age, the lender may increase the Loan-to-Value (LTV) ratio, allowing the homeowner to borrow a larger proportion of their home’s value.

This higher LTV can provide them with more funds for retirement needs or other expenses.

But, the story is different for younger borrowers, usually around the age of 55. Lenders tend to be more cautious. As they may need to top into their equity for future retirement costs, such as care home fees.

Interestingly, your health can also influence your LTV. If you have health issues that could lead to a shorter life expectancy, lenders could allow you to borrow more against your home’s value. A medical report can confirm this to the lender.

Can Pensioners Get Mortgages Even with Bad Credit?

Mortgages can feel like a puzzle when you’re retired, especially if you’ve had credit problems. Many mortgage calculators for retirees don’t look at the full picture.

They often miss out on important affordability factors like bad credit. This can lead to confusion as some lenders are pretty strict with borrowers who’ve had money troubles.

Picture your credit score as a map. It helps lenders see how good you are with money.

If your score is low, it might feel like getting a mortgage is a big hill to climb. But don’t worry, it’s not a dead end.

Even if you’re retired and have bad credit, there are options. Start by knowing your credit score and how to make it better.

Simple things like paying your bills on time, clearing debts, and keeping your credit report clean can help improve your score.

And if your score isn’t quite up to scratch, don’t lose hope. Some lenders help people with not-so-great credit.

Yes, it might be a bit harder, but getting a mortgage in retirement with bad credit is not impossible. Certain lenders might be okay with a bit of bad credit. They’ll look at when the problem happened and how bad it was.

They’ll also look at your income, any debts you have, and the value of the house you’re buying. Once you understand these, you’re in a better position to sort out your mortgage.

Key Takeaways

- Retirement mortgage calculators are handy tools to help you understand potential mortgage products and terms that could work for you.

- Your income, age, health, type of mortgage product, and credit score are all pivotal in determining your borrowing capacity.

- There are various types of mortgages available to retirees, each with its unique benefits and considerations.

- Specialised lenders exist for pensioners with unique circumstances, including those with bad credit or advanced age.

The Bottom Line

Remember, each journey is unique, and what worked for others might not work for you. That’s why professional guidance is invaluable.

To get started, fill out this quick form, and we’ll pair you with a knowledgeable mortgage broker. They can shed light on the process, helping you find your way through this complex terrain with no fuss.

We’re here for you, offering support without any pressure or stress.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

How are mortgages calculated now?

Mortgage calculations consider several key factors including the principal amount you borrow, the interest rate on your mortgage, and the term over which you repay the loan. Using these parameters, a mortgage calculator computes the amount of your monthly payments.

Retirement mortgage calculators add an extra dimension, considering factors unique to retirees such as age, health, and post-retirement income.

What is the difference between RIO and equity release?

Retirement Interest Only (RIO) mortgages and equity releases are two different ways retirees can tap into their home’s value.

RIO is a mortgage where you only pay the interest on the loan during the term, with the principal amount repaid when the home is sold, typically when you move into care or pass away.

On the other hand, equity release allows you to unlock the wealth tied up in your home, either as a lump sum or a regular income, without having to make regular payments. The loan, plus accrued interest, is repaid when your house is sold, often after your death or when you move into long-term care.

How is interest calculated on lifetime mortgages?

In a lifetime mortgage, a form of equity release, interest is calculated on the amount you choose to release, plus any interest already added. This interest can be fixed or variable, depending on the product chosen.

It’s compounded, meaning you’re charged interest on the original loan plus any interest already added. As a result, the amount you owe can grow quickly, reducing the equity left in your home and the inheritance you might leave.

Related Articles

How to Get the Best Mortgages for Older Borrowers in 2025?

Older borrowers in the UK are getting more mortgages than ever. In the third quarter of 2024, 33,840 new loans went to people over 55—a 2% rise from 2023. These loans were worth £5.2 billion, nearly 10% more than the year before. For the first time, over half of new mortgages will go beyond the […]

Is a Reverse Mortgage Right for You? A Guide in 2025

Retirement should be about relaxation, not money worries. But, for many homeowners, the pension pot only goes so far. If you’re feeling the pinch, your property could offer a solution: a reverse mortgage. Sound complex? It doesn’t have to be. In this guide, we’re simplifying reverse mortgages. You’ll discover what they are, how they work, […]

Best Retirement Mortgage Providers in the UK in 2025

When you’re thinking about buying a house, one of the key steps in that journey involves finding a good mortgage lender. Why is this important? Simply put, a mortgage lender provides the financial backing that makes buying a house a feasible option. It’s a lot easier to pay back the cost of a home over […]