Graduate Mortgages: A Comprehensive Guide in 2025

Imagine this: You’ve tossed your graduation cap in the air, bidding farewell to university life.

Armed with a degree and boundless dreams, you set your sights on the next big milestone—buying your first home in the UK.

Excitement builds as you picture a place to call your own, complete with stylish furnishings and Instagram-worthy décor. But, reality hits hard.

As a fresh graduate, you realise that buying a home is not as easy as it looks. The hurdles are huge.

Your student loan debt is a looming threat. Your credit history is weak, and the uncertainty of entry-level employment casts a shadow over your financial future.

Trying to figure out mortgages is like trying to solve a complex puzzle without instructions. That’s where we step in.

In this comprehensive guide, we’ll shed light on the challenges faced by UK graduates when it comes to mortgages. We’ll also provide important insights and mortgage options that are available to you.

By the end of this guide, you’ll be well on your way to making an informed decision about mortgages as a graduate.

What are Mortgages for Graduates?

There are no specific mortgage products aimed at graduates in the UK. You’re likely to get what’s available in the market.

But, there are some mortgage products that may be more accessible to graduates than others.

Some lenders specialise in graduate mortgages. They may come with more flexible underwriting and lower interest rates.

Still, you’ll have to meet the lender’s criteria which depends on factors such as your income, deposit size, and credit history.

As a graduate, this can be a challenge. You might be facing some of these situations:

- A low-paying entry-level job.

- A small or no deposit.

- High student loan debt.

- No credit history or it’s not looking good.

These things may worry lenders and lead to application rejections. But, don’t worry. The key to getting a mortgage is to meet the right lender who understands your situation.

It’s also important not to rush into homeownership, as this can be your biggest investment. Take your time to wait until you’re ready.

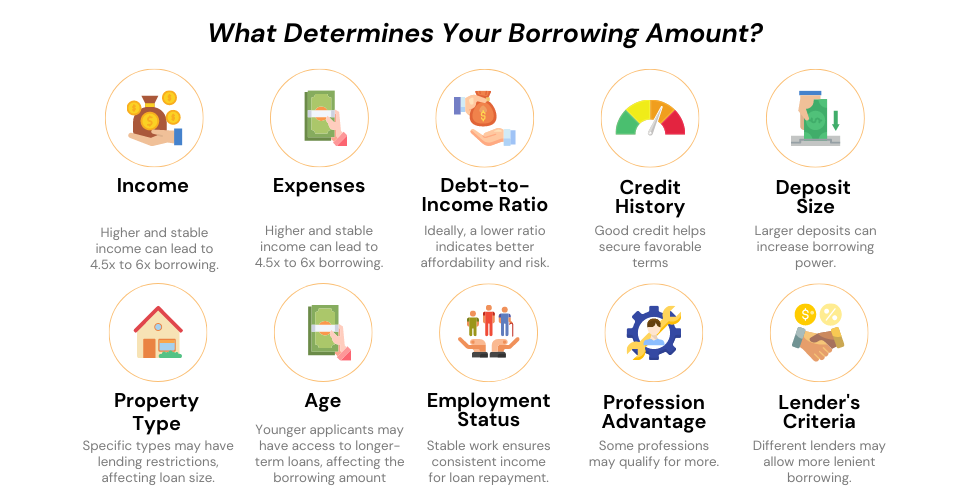

How Much Can Graduates Borrow?

Lenders will conduct an affordability assessment to determine how much you can afford to borrow. This assessment will take into account these factors:

- Income – Lenders seek stable and reliable income to repay your mortgage. This should be enough to cover your monthly payments and expenses.

- Expenses – These are monthly costs like rent, utilities, and transportation. Lenders want manageable expenses with enough disposable income for mortgage payments.

- Debt-to-income ratio – This measures the part of your monthly income allocated to debt repayments. Lenders usually prefer a ratio below 43%.

- Deposit size – This is the money you put for the down payment. It’s usually good to save at least 10% deposit to get better rates and deals.

- Credit score – This reflects your creditworthiness. Lenders look for a good credit score and check to see if you’ve paid your debts on time.

- Type of job and qualifications – If you have a job lined up after graduation or a professional degree that is in high demand, lenders will be more likely to lend you more money, as they will see your potential to earn a higher income in the future.

In addition to this, lenders usually use income multiples, ranging from 3.5x to 4.5x your annual salary, to determine your borrowing capacity.

For example, if you earn £27,000 per year, your potential mortgage amount would be:

- Minimum: £27,000 x 3.5 = £94,500

- Maximum: £27,000 x 4.5 = £121,500

If you meet the lender’s affordability criteria, you’re likely to receive a mortgage offer.

Deposit Requirements for Graduates

Some lenders will lend you money with a 5% deposit, but here’s a pro-tip: aim higher.

A bigger deposit will get you better rates, access to more lenders, and lower mortgage repayments. Ultimately, this can save you money in the long run.

If you get financial help from a family member, certain lenders can help you. Alternatively, it’s advisable to wait until you’ve saved up a large enough deposit.

You can use tax-free savings accounts like Lifetime ISAs to help you save for a deposit.

If you’re a high-risk borrower, the lender might ask for a bigger deposit to cover any repayment issues. Such as when you default on your mortgage repayments.

Credit History of Graduates

A good credit history demonstrates responsible borrowing habits. This boosts your chances of mortgage approval.

As a graduate, student loans may be your only form of credit. This doesn’t directly affect your credit score. They only affect your borrowing amounts and affordability assessment.

Lenders may find it hard to assess your creditworthiness if you don’t have or you lack credit history. This could lead to your application being rejected.

So, it’s a wise move to build your credit score before applying for a mortgage. To do this, make sure to pay your debts on time, and stay within your credit limit to show responsible credit usage.

If you were also denied for credit before, avoid making too many applications all at once. This could indicate to lenders that you’re struggling for money.

Can I Get a Mortgage if I’m on a Graduate Scheme?

Yes, you can get a mortgage if you’re on a permanent and paid graduate scheme. Lenders will treat you the same as other borrowers. They’ll ask for your contract and some proof of income to see if you can handle the monthly repayments.

Mortgages can be harder to get if you’re on a fixed-term contract or probationary period. Many lenders like stability and consistent income. So permanent employment is usually seen as more favourable.

If you’re not in a permanent role yet, it might be best to wait before applying for a mortgage. This will give you a higher chance of getting a mortgage deal.

Mortgages Available to Graduates

Professional Mortgages

If you’re a graduate in a skilled profession, like medicine, law, or accounting, you’ll find it easier to get a mortgage.

As a sought-after professional, you’re likely to earn a higher income and less likely to default on mortgage payments. In return, many lenders see you as a low-risk borrowers.

Because of that, they will offer you more flexible criteria and terms on your mortgage. This could mean lower fees, more favourable interest rates, or higher income multiples.

>> More about Professional Mortgages

Government Schemes

These schemes are not specifically tailored for graduates. They are for anyone who may struggle to get on the property ladder without additional help.

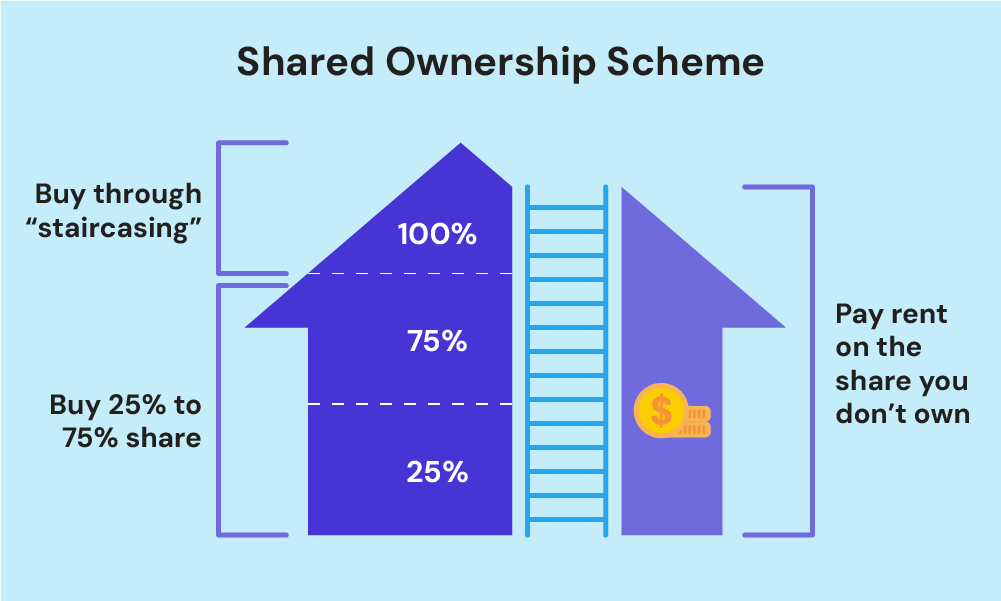

This scheme lets first-time buyers in England buy a new-build home at a 30-50% discount. The discount is permanent, so it will apply to future buyers too.

To qualify, you need to be 18 or older, a first-time buyer with a household income of less than £80,000 (£90,000 in London), and be able to secure a mortgage for at least half of the property’s value.

You can buy a share, anywhere from 10% to 75%, and pay rent on the rest. You’ll also need to pay a deposit, usually 5% to 10% of the share you’re buying.

Every month you’ll make payments for a mortgage on the portion of the property you bought, rent for the portion you don’t own, and a service charge.

You can then gradually increase your ownership by buying additional shares. This is called “staircasing”. Lenders’ assessments are easier and more lenient as you only buy a share of the property. This is a good option if you have limited savings.

>> More about government schemes in our First-Time Buyers Guide

Family Mortgage Options

As a graduate, you might find it challenging to save up for a deposit or you have limited credit history.

The good news: there are mortgage options available that lets you get financial help from your family. This can be a great way to get on the property ladder early.

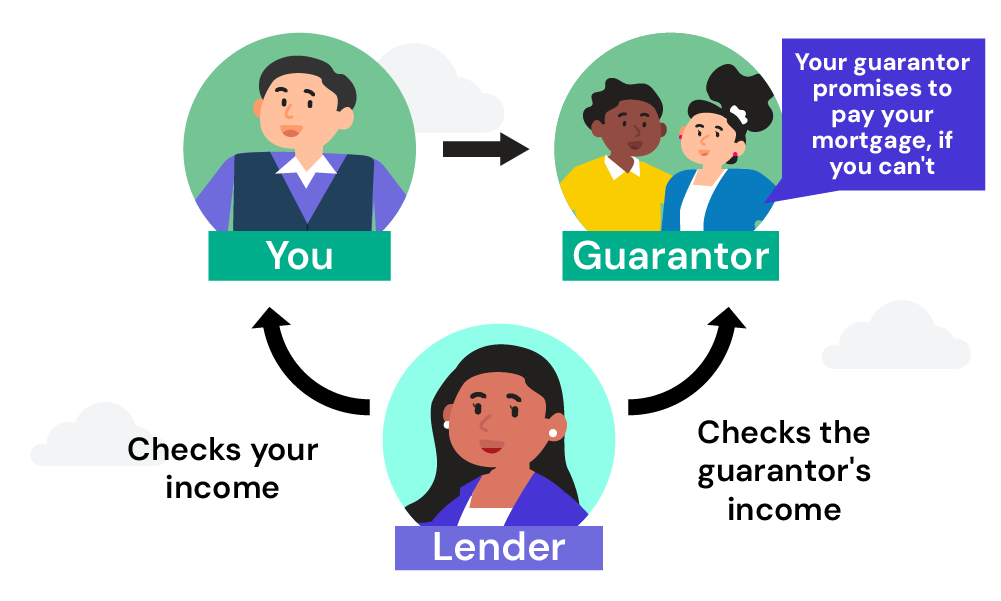

- With this type, your parent or grandparent agrees to pay the mortgage if you can’t. While they don’t have any legal claim to the property, they are still legally responsible for the payment.

- It’s a helpful option if you lack a sufficient deposit or income to qualify for a mortgage on your own.

Joint Mortgages with family members

- This mortgage allows two or more people to share responsibility for the mortgage payments. Both of you must meet the lender’s criteria and be financially stable to afford payments.

- This is a good choice if you’re aiming to buy a home with a family member, like a parent or sibling.

- A gifted deposit is a sum of money from a family member or friend to put as downpayment for your mortgage. It should not be a loan, and the giver doesn’t expect to be paid back. You may need to sign a declaration stating you won’t repay it.

- This can be a real helping hand if you’re struggling to save up for a deposit. It also reduces your borrowing need and increases your chance of mortgage approval. But, you still need to afford monthly repayments.

Family Offset Mortgages

- This mortgage type lets you link or offset your family members’ savings accounts to your mortgage.

- Your family member’s savings account will be inaccessible until you’ve met the lender’s criteria, such as paying 25-30% of the loan.

- The savings account offset to your mortgage can help reduce monthly mortgage payments and save money in interest.

The Bottom Line

As a fresh graduate in the UK, owning a home may seem like a distant dream. Although there’s no such thing as a graduate mortgage, there are lenders who’ll understand your situation. They offer more flexible underwriting and products designed to meet your needs.

To qualify for these deals, you’ve got to meet your lender’s criteria. Your income, expenses, deposit size, and credit score will all play a part in your application. So, focus on saving up for a bigger deposit and work on building a solid credit rating. That way, you’ll present yourself in the best light to mortgage lenders.

While many mortgage options are available for you, finding them can be tricky. To increase your chances of landing the perfect deal, team up with a good mortgage broker. Their expertise can take the stress off your shoulders and get you the best deal for your needs and budget.

To take advantage of this, inquire with us today and we’ll connect you with a good broker that specialises in mortgages for graduates.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

Can graduates with no credit history qualify for a mortgage?

It’s possible to get a mortgage with no credit history, but it’ll be more challenging. Lenders will need to do more checking, so the application process will be longer. Mortgage rates might be higher to compensate for the risk. Some lenders may also ask for proof of bill payments to assess your reliability. They’ll also consider your income and deposit size.

Can self-employed graduates get a mortgage?

Yes, you can if you can prove your income. Most lenders need 2 or more years of accounts and SA302 tax returns, which are official summaries of your annual income reported to the UK’s HM Revenue & Customs (HMRC). But, specialist lenders may consider applicants with only 1 year of accounts verified by a qualified accountant.

>> More about Self-Employed Mortgages

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Police Mortgages: A Definitive Guide in 2025

Police officers are never off duty. You put your lives on the line every day to keep us safe. But amidst your noble service, you face a unique challenge: securing a mortgage. As a police officer, time can be your enemy. The demands of your profession, the irregular shift patterns, and the sacrifices you make […]

NHS Mortgages: What You Need to Know Before Buying a Home

If you work for the NHS, you’re no stranger to hard work. You put in long hours, manage unpredictable shifts, and care for those who need it most. But when it comes to buying a home, the process can feel unnecessarily complicated. Your irregular hours, varied income, and short-term contracts might make it seem like […]

A Complete Guide: Mortgages for Professionals

If you’ve worked hard, got yourself qualified, and are ready to buy a house, you might be wondering if there are mortgages for professionals like you. The good news is – there are! Mortgage lenders offer professional mortgages with favourable and flexible terms. As a professional, you’ve shown that you’re responsible and have a predictable […]