Teacher Mortgages: A Guide Made Easy for Educators

Did you know that teachers can afford mortgages just like other professionals?

You might think that low salaries, high cost of living, and temporary contracts make it impossible for you to get on the property ladder, but that’s not always the case.

As a teacher, you play a crucial role in shaping our future. Your service today will always have a lasting impact on the society to come.

In return for this, there are a lot of mortgage deals and schemes available to help you get on the property ladder.

But your profession doesn’t mean you’re automatically entitled to a mortgage. There are still criteria, and factors that could work against you.

That’s why it’s important to understand how teacher mortgages work and how you can ace your mortgage application. In this guide, we’ll explain everything you need to know to have a successful mortgage journey in the UK.

Can Teachers Get Better Mortgage Deals?

Yes, you can. Teachers are essential professionals. So you’re in a good position to secure a mortgage over other borrowers.

There are lenders who are supportive of the teaching profession and are more likely to approve your loan and offer lower interest rates. You can also apply for government schemes, which we’ll talk about later.

While no mortgages are specifically tailored for teachers, you have access to the same standard mortgages as other borrowers. But, as a teacher, you qualify for more flexible terms and favourable rates.

Just like anyone else, it’s important to meet the specific criteria of your lender and be ready before applying for a mortgage.

Eligibility Criteria for Teachers

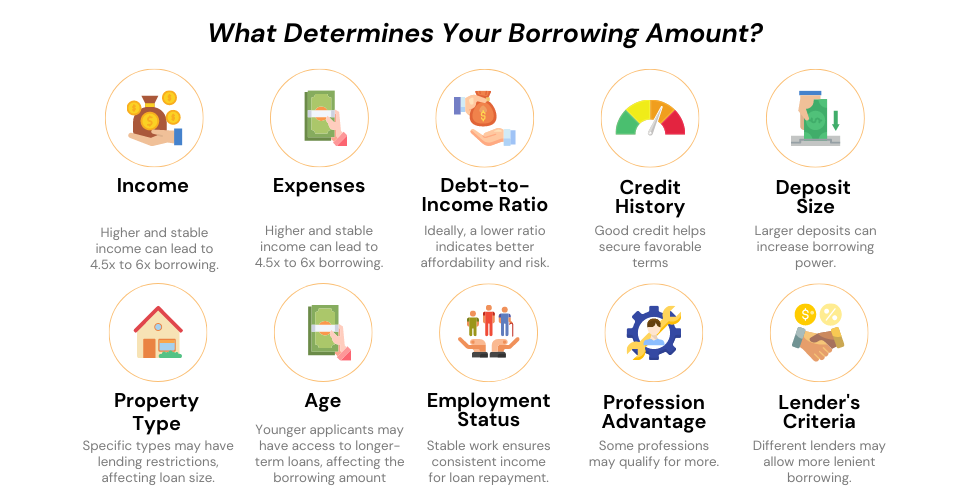

Each lender has a different set of criteria and requirements. But generally, here are the common factors that they will consider:

- Your income and outgoings

- The size of your deposit

- Your credit history

- Your Age

- The type of property you’re interested in

- Your employment type

Income and Outgoings

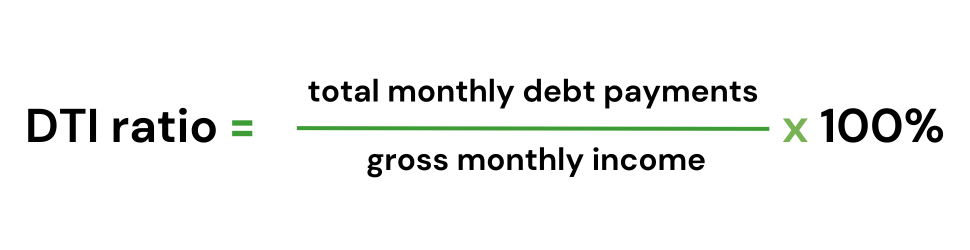

When applying for a mortgage, lenders look at your income and outgoings to know if you can handle monthly payments.

They’ll also calculate your debt-to-income (DTI) ratio. This tells lenders how much of your monthly income goes into your debts. To calculate, use this formula:

For example, you have £1,500 in monthly debt payments from a student loan, car loan, rent, credit card payment, and a gross monthly income of £4,000. Your DTI ratio would be 37.5%. This means you have a good chance of getting a mortgage. The lower the ratio, the better.

It’s advisable to aim for at least a 36% to 43% DTI ratio. If your DTI ratio is too high, you can pay off some debts or find ways to boost your income before getting a mortgage.

Check your debt-to-income-ratio using our calculator.

Deposit Size

The bigger your deposit, the better rates you get. It’s alright if you can manage a 5% deposit, but going higher improves your chances of having better interest rates.

You can save up at least 10% to get access to some fantastic mortgage deals.

Credit History

Lenders want to see how you managed your finances, and if you pay your credit on time. Just remember to check your credit file for any errors before your lender does.

Age

Lenders have age limits for mortgages. Many lenders prefer those who are still working but if you’re nearing retirement or already retired.

There are specialist lenders available who can assist you in such cases.

Type of Property

Lenders may be more cautious about unusual properties with a limited market. This is because once you default on payments, these properties may be harder to sell.

Employment Type

Your job type matters when applying for a mortgage. Lenders want to ensure you can handle the repayments. If you’re newly qualified or a supply teacher, you’ll need to find a lender who understands your income.

How much can Teachers Borrow?

Most lenders in the UK use income multiples to determine how much to lend you. This could be around three or five times your annual salary.

For example, a qualified teacher in England can earn up to £38,810 per year. Your lender will multiply this amount by either 3 or 5. Have a look at the table to see how this works.

| Income Multiple | Potential Mortgage Amount |

|---|---|

| 3x | £116,430 |

| 5x | £194,050 |

Some lenders will include overtime, bonuses, or allowances in your income, while others won’t. So, it’s important to find a lender who will take all your income into account.

In addition, lenders will look at other factors that we’ve discussed above. So you must be able to provide evidence of your income, expenses, credit history, and savings for deposit.

Proving Your Income as a Teacher

Lenders tend to favor borrowers with stable, full-time jobs over those on temporary contracts. If you’re a newly qualified or a supply teacher, you might face some hurdles when getting a mortgage.

Don’t worry though, you can improve your chance by preparing the right documents to prove your income.

Newly Qualified Teachers (NQT) Mortgages

NQTs in the UK start on a 1-year fixed contract. This may be seen as high-risk by some lenders, as there is no guarantee that the contract will be renewed next year.

To get a mortgage, you need to find a specialist lender that understands your situation. They can be more lenient with their criteria and offer you better rates. Just make sure you can afford the repayments and you have the documents to prove your income. This can be:

- 3 or more months of your most recent payslips

- An employment contract or a letter from your employer confirming your status and salary

Supply Teacher Mortgages

Lenders are wary of lending to supply teachers, as you have a temporary or contract-based job. To counter this, you need to have:

- At least 12 months of consistent work to show you have a reliable source of income.

- A proven track record of renewed contracts.

- Any future work contracts.

Teachers with Diverse Income Streams

Teachers who earn income from different sources may need to provide additional documentation to demonstrate income stability.

In general, if you have self-employed income you must have:

- 2-3 years’ worth of accounts verified by a qualified accountant; and

- SA302 tax returns which are official summaries of your annual income reported to the UK’s HM Revenue & Customs (HMRC).

Mortgage Types and Schemes in the UK

While there are no mortgages and government schemes tailored only for teachers, there are few available that can assist you in getting a foot on the property ladder. Here are some popular options to consider:

As a teacher and a key worker, you can get discounts of 30% to 50% on newly constructed homes in England. The discount is permanent and can be passed on to future eligible buyers.

To qualify, you must be a first-time buyer with a household income of less than £80,000 in England (£90,000 in London). You also need to get a mortgage for at least 50% of the property’s price.

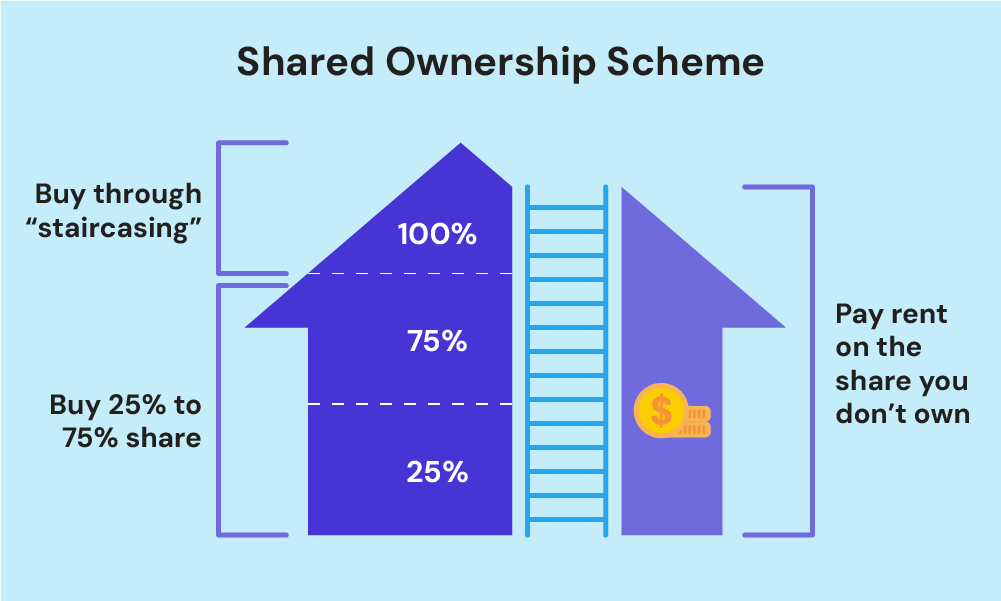

This scheme can be a great option if can’t afford to buy a property outright. Here’s how it works:

- You buy a share of the property between 25% and 75%.

- You pay rent and service charges for the remaining share to your landlord.

- To finance your share, you’ll need to get a mortgage loan and pay a 5% or 10% deposit.

- You can later staircase up to 100% ownership if your landlord agrees.

To be eligible, your household income can’t be more than £80,000 a year (£90,000 in London). You should also not be able to get a full mortgage for a property.

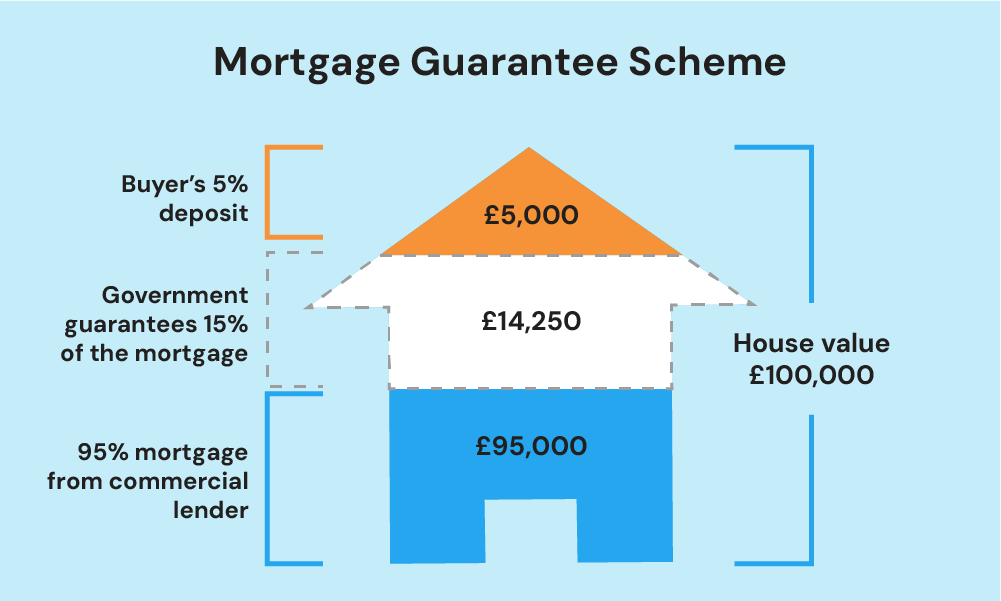

This scheme is similar to a 95% mortgage. The government guarantees 15% of your mortgage, so you can get a mortgage on a property worth up to £600,000 with a deposit of just 5% to 9%.

If you default on your payments, the government will cover your lender for 15% of the mortgage amount. The scheme is open to both first-time buyers and existing homeowners, but it’s only available until the June 30, 2025.

This scheme lets you buy your council home at a discounted price. The largest discount available is £96,000 in England and £127,900 in London.

To qualify, you must be the sole council tenant for at least 3 years, have a plan to use the property as your main home, be a secure tenant, and have no pending evictions, bankruptcies, or significant debts.

Guarantor and Springboard Mortgages

This is a good option for teachers who need a little extra help. Both of these mortgages involve a third party to help you get a mortgage.

The difference? In a guarantor mortgage, a third party agrees to step in and cover the mortgage payments if you default.

In a springboard mortgage, the third party provides a collateral like savings or property equity to add security to the lender.

These options work well for teachers who have low deposits or want a lower interest rate.

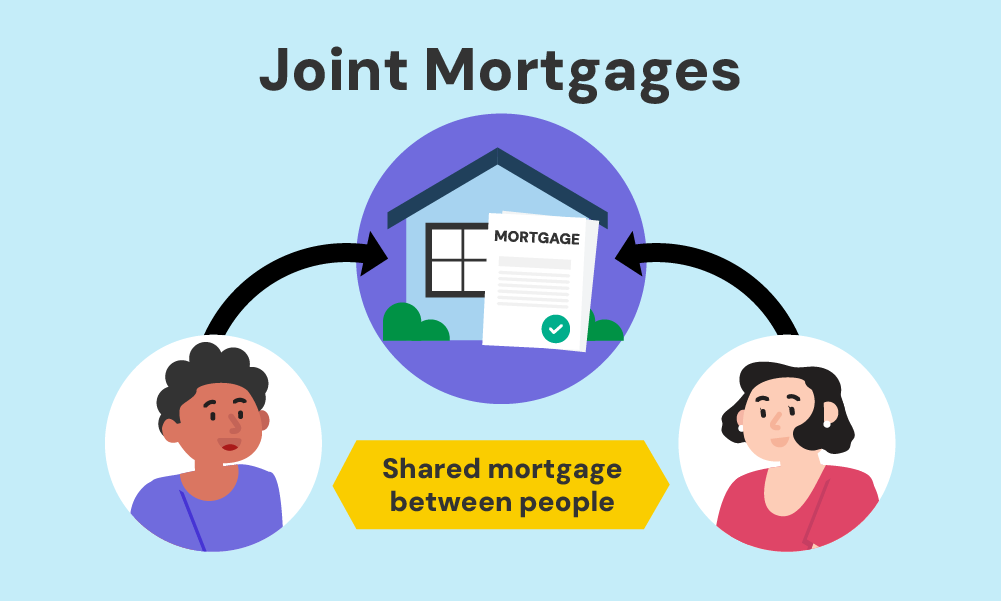

A joint mortgage is when two people, usually a couple, take out a mortgage together. It’s a great option for teachers planning to buy a home as it offers a larger mortgage and lower interest rates.

The Bottom Line

As a teacher, your profession gives you an advantage to get mortgages. You’re in a good position to get better deals. But, your mortgage approval is not guaranteed.

So it’s important to build your financial security. Save up, improve your credit score, and gather proof of all your income. Once you’ve done that, you’ll be in a much better position to apply for a mortgage.

While you’re on the mortgage hunt, get a good mortgage advisor to help you. They can help you get access to specialist lenders and get better deals. Having them on your side will give you peace of mind knowing that everything about the mortgage process will be taken care of.

To take advantage of this, drop us a line today and we’ll hook you up with a good mortgage broker who specialises in teachers’ mortgages.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

Can retired teachers get a mortgage?

Yes, retired teachers can get a mortgage in the UK. Usually, lenders will consider your pension income, other income, and expenses to assess your ability to afford the payments.

You may want to see consider other options for retired teachers such as retirement interest-only mortgages, equity release, downsizing, and remortgaging.

Mainstream banks typically lend up to age 70, so it’s important to speak to a good mortgage advisor to find a specialist lender that meets your needs.

Can trainee teachers get a mortgage?

Yes, you can. Lenders will typically assess you based on the following factors:

-

- Income, including your bursary and any other income they have.

-

- Expenses, such as mortgage payments, bills, and living expenses.

-

- Future employment prospects.

-

- Debts including your student loan debt.

Can I get a teacher mortgage even with bad credit?

Yes, there are specialist lenders who offer bad credit mortgages. How much you can borrow will depend on the nature and time of your bad credit.

Be aware though that these mortgages usually have high-interest rates and large deposit requirements. So it’s best to weigh your options and see if you must wait to improve your credit ratings to get better rates.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Police Mortgages: A Definitive Guide in 2025

Police officers are never off duty. You put your lives on the line every day to keep us safe. But amidst your noble service, you face a unique challenge: securing a mortgage. As a police officer, time can be your enemy. The demands of your profession, the irregular shift patterns, and the sacrifices you make […]

NHS Mortgages: What You Need to Know Before Buying a Home

If you work for the NHS, you’re no stranger to hard work. You put in long hours, manage unpredictable shifts, and care for those who need it most. But when it comes to buying a home, the process can feel unnecessarily complicated. Your irregular hours, varied income, and short-term contracts might make it seem like […]

A Complete Guide: Mortgages for Professionals

If you’ve worked hard, got yourself qualified, and are ready to buy a house, you might be wondering if there are mortgages for professionals like you. The good news is – there are! Mortgage lenders offer professional mortgages with favourable and flexible terms. As a professional, you’ve shown that you’re responsible and have a predictable […]