- What is a Debt Consolidation Mortgage?

- Can I Consolidate My Debts into a Mortgage?

- What Types of Debts Can I Consolidate to My Mortgage?

- How Does it Work? Debt Consolidation Example

- How to Get a Debt Consolidation Mortgage

- Which Debt Consolidation Method is Right for You?

- Should You Stick with Your Current Lender for Remortgaging?

- How Much Will I Pay After Debt Consolidation?

- Should You Consolidate Your Debt Using Your Mortgage?

- Lenders Providing Debt Consolidation Mortgages in the UK

- What Factors Will Lenders Consider?

- Can I Remortgage Shared Ownership Home for Debt Consolidation?

- Can Bad Credit Affect Debt Consolidation Mortgages?

- The Bottom Line: How Expert Advice Makes Debt Consolidation Easier

How Can Debt Consolidation Mortgages Ease Your Finances

Feeling overwhelmed by multiple debts?

You’re not alone, and there might be a simpler way to get your finances back on track: debt consolidation mortgages.

Imagine lumping all those nagging payments into just one—possibly even with a lower interest rate!

But hold on, it’s not a magic wand that fixes everything for everyone.

That’s why it’s crucial to chat with mortgage experts who get the ins and outs of rolling debts into your mortgage. They can tell you straight if this move makes sense for your unique situation.

In the next few minutes, this article will walk you through how this whole debt consolidation mortgage thing works, what debts you can bundle up, and the steps to get the ball rolling.

Plus, we’ll weigh the good against the bad to help you decide if it’s the financial lifeline you’ve been searching for.

What is a Debt Consolidation Mortgage?

In simple terms, a Debt Consolidation Mortgage lets you combine all your smaller debts into your existing home loan.

Imagine owing money on several credit cards and loans. Instead of juggling multiple payments, you’d make just one payment to cover them all.

Why? Because you roll these smaller debts into your mortgage. This can make life easier and save you money if the mortgage rate is lower than the interest rates on your other debts.

If you’re in the UK, it’s important to know that this isn’t a one-size-fits-all solution. You have to be careful because you’re using your home as collateral.

If you don’t make payments, you could risk losing your home so, it’s smart to talk to mortgage experts who can help you determine if this is right for you.

Can I Consolidate My Debts into a Mortgage?

Yes, you can consolidate debts if you’re already a homeowner.

Being a homeowner gives you the chance to combine various smaller debts—like credit card bills or personal loans—into your existing mortgage.

This could make your life simpler by turning multiple payments into just one and might even lower the interest you have to pay.

But if you’re stepping into the property market for the first time, this choice isn’t available to you.

First-time buyers need to establish their mortgage history before considering such financial moves.

So, if you own your home and are weighed down by multiple debts, using your mortgage for consolidation could be a savvy strategy.

What Types of Debts Can I Consolidate to My Mortgage?

When you’re considering debt consolidation with your mortgage, you have various options. These can range from unsecured to secured debts.

Unsecured Debts

Loans not tied to any assets, like a house or car. This includes:

- Credit Cards

- Personal Loans

- Medical Bills

- Auto Loans (unsecured)

- Hire purchase agreements

- Utility Bills (in arrears)

- Payday Loans

- Overdrafts

Secured Debts

Loans backed by assets, such as property or vehicles, such as:

- Car Loans (secured)

- Home Equity Loans

- Second Mortgages

- Boat Loans

- Recreational Vehicle Loans

- Business Loans (if secured against personal assets)

Note that the option to consolidate secured debts will depend on factors such as your lender’s policies, your credit score, and your home’s current value. Always consult a mortgage advisor to assess the specific risks and benefits of your situation.

How Does it Work? Debt Consolidation Example

To help you get a handle on how debt consolidation might work for you, let’s look at an example that compares repaying multiple debts separately versus consolidating them into a mortgage.

| Debt Type | Initial Amount | Monthly Payment | Interest Rate | Total Interest Paid | Overall Amount Repaid | Repayment Term |

|---|---|---|---|---|---|---|

| Credit Card | £3,000 | £32.11 | 20% | £3,853 | £6,853 | 10 years |

| Personal Loan | £10,000 | £106.07 | 6% | £2,728 | £12,728 | 10 years |

| Car Loan | £5,000 | £53.03 | 10% | £1,364 | £6,364 | 10 years |

| Total without Mortgage | £18,000 | £191.21 | — | £7,945 | £25,945 | — |

| Mortgage Option | £18,000 | £144.32 | 4% | £5,319 | £23,319 | 10 years |

This example illustrates that if you consolidate your £18,000 of debt into a 10-year mortgage at a 4% interest rate, you would make lower monthly payments and also save £2,626 in the overall amount repaid compared to not consolidating.

Note: These figures are illustrative and may not reflect your actual financial situation. For personalized advice, consider speaking to a qualified mortgage broker.

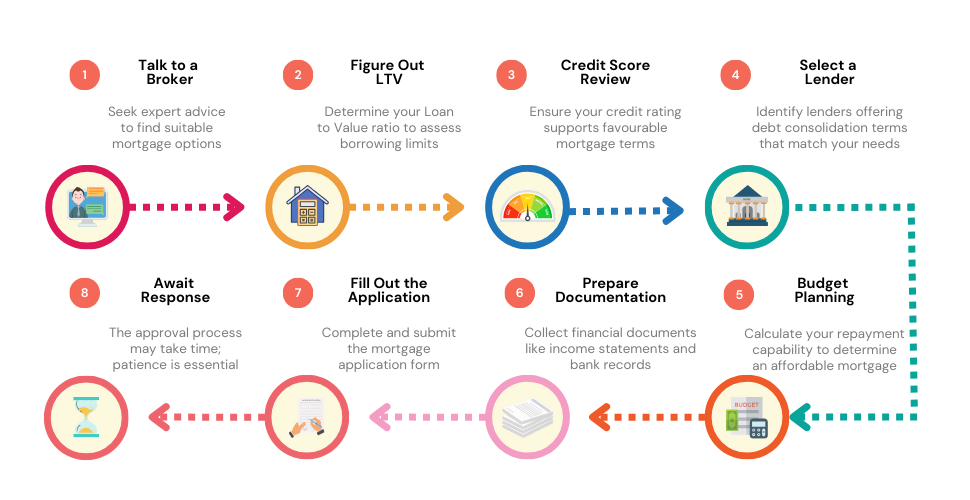

How to Get a Debt Consolidation Mortgage

If you’re thinking about combining your debts into one easy payment, a debt consolidation mortgage could be right for you. Here’s how to get one, step-by-step:

Talk to a Remortgage Broker. The first thing you should do is speak to a mortgage broker. They know all about these types of mortgages and can help find the best one for you.

Figure Out Your LTV. LTV stands for Loan to Value. It’s a number that shows how big your loan is compared to how much your house is worth.

The smaller this number, the better your chances are of getting a good deal.

Check Your Credit Score. You’ll need to know your credit score because it can affect the kind of deal you get. You can download your credit report online from different websites. The higher your score, the better.

Choose the Right Lender. Picking a lender is a big deal. A mortgage broker can help you find the ones that are the best fit for consolidating your debts.

Make a Budget. Before you go any further, sit down and figure out how much money you can afford to pay back each month. This will help you and your broker know what kind of mortgage you can handle.

Get Your Paperwork Together. You’ll need to show things like how much money you make and how much you spend. Gather documents such as:

- Recent payslips or income proof

- The last 3 months’ bank statements

- Existing mortgage statements or loans (if any) showing remaining balances and terms

- Valid IDs for identity verification

- Proof of address, such as a utility bill

- Credit report, as required

Please note, that this list may not cover every requirement; each lender has their unique criteria, especially for properties in probate.

Fill Out the Application. Your mortgage broker will help you fill out the loan application. This is where you officially ask for the money.

Wait for an Answer. Once you send in your application, the lender will decide if they’ll give you the loan. This could take a little time, so be patient.

Follow these steps, and you’ll be well on your way to securing a debt consolidation mortgage that makes managing your debts simpler.

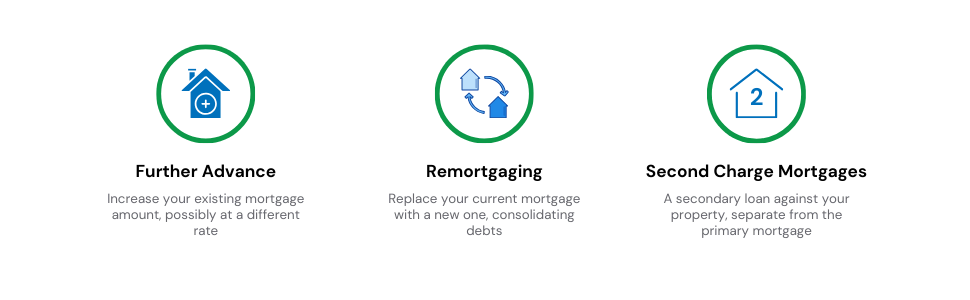

Which Debt Consolidation Method is Right for You?

As a homeowner with an existing mortgage, you’ve got three key choices for consolidating your debt: a Further Advance, Remortgaging, and taking out a Second Charge Mortgage.

Let’s explore what each entails to help you decide what’s right for you.

Further Advance

This is like adding an extra layer to your current mortgage. While the main terms stay the same, the extra cash could come with a higher interest rate.

If your lender provides this option, you’ll need to meet some requirements:

- Your mortgage must be at least 6 months old.

- Prepare for another credit check and financial review.

- The lender may ask for evidence of the debts you aim to pay off.

- You could need a new valuation of your home.

- Usually, you can borrow at least £5,000 more, up to 85% of your home’s value. There might also be some admin fees.

Note though that the requirements may vary between lenders, so it’s best to ask your chosen lender about this

Remortgaging

This isn’t only about snagging a better rate. With remortgaging, you can switch to a new lender to wrap up your current mortgage and debts into one new package.

It’s a good option if you have a significant amount of debt to tackle and offers the possibility to borrow more than a further advance.

Second Charge Mortgages

Also known as a second mortgage, this is a separate loan that also uses your home as security. It’s called a “second charge” because your original mortgage holds the “first charge” on your property.

If you struggle with bad credit, this could be your best bet as approval is more based on how much of your house you own, not just your income or credit history.

In all three scenarios, consulting a mortgage broker can make a huge difference.

They can guide you based on your specific circumstances to ensure you’re taking the most sensible route for debt consolidation.

Should You Stick with Your Current Lender for Remortgaging?

No, you’re not obligated to stick with your current lender when looking to consolidate debts into your mortgage.

Shopping around is often wise. While your existing lender might make an attractive offer, others could provide even better terms.

Another crucial point is the Loan to Value (LTV) cap. Some lenders might have an LTV cap set between 60-85% specifically for debt consolidation, making it essential to compare various offers.

How Much Will I Pay After Debt Consolidation?

To get a sense of your monthly payments and possible savings through debt consolidation, use the calculator below.

[Embedded Debt Consolidation Remortgage Calculator]

However, keep in mind that this calculator serves as a guide, not a guarantee. For a more precise and reliable figure tailored to your needs, it’s advisable to consult a mortgage broker.

Should You Consolidate Your Debt Using Your Mortgage?

Consolidating your debt using your mortgage comes with its own set of pros and cons, and it’s a decision that shouldn’t be taken lightly.

Pros

- Lower Interest Rate. Mortgages usually offer lower interest rates than other types of debt, which can result in savings.

- Simplified Payments. Instead of juggling multiple payments each month, you’ll make one payment toward your mortgage. This makes it easier to manage your finances.

- Improved Cash Flow. With lower interest and a single payment, you could find yourself with extra money at the end of the month.

Cons

- Longer Repayment Period. Although the interest rate is lower, the repayment term is usually longer, which could result in more interest paid over time.

- Risk to Your Home. Since your mortgage is secured by your home, failing to make payments can put your home at risk of repossession.

- Upfront Costs. Depending on your lender, you might have to pay fees to consolidate your debts into your mortgage. Make sure to factor this into your decision.

Using your mortgage for debt consolidation affects your home’s equity and future borrowing options. The stakes are high—you’re using your home as security.

So, make sure you get expert advice from a certified mortgage broker to fully understand the risks and rewards.

Lenders Providing Debt Consolidation Mortgages in the UK

If you’re looking to consolidate your debts through a mortgage, a variety of UK lenders could be viable options for you. This list isn’t exhaustive, but it includes some major players in the mortgage market:

- Barclays

- First Direct

- Halifax

- HSBC

- Kensington

- Lloyds

- Metrobank

- Post Office

- Principality

- Royal Bank of Scotland

- Santander

- TSB

- Virgin Money

- Coventry Building Society

- Atom Bank

- Co-Operative

Given the number of options available, it’s easy to feel overwhelmed. This is where expert mortgage advice can offer invaluable guidance.

What Factors Will Lenders Consider?

When you apply for a debt consolidation mortgage, lenders examine a few critical factors to gauge your eligibility:

- Loan-to-Value (LTV) Ratio. Most lenders focus on your LTV, often capping it between 60% and 85% for debt consolidation.

- Credit Score. A high credit score can open the door to better mortgage rates. However, some lenders do cater to those with less-than-perfect credit histories.

- Age. Some lenders have age limits, often not lending to those above 75, while others might go as high as 85 or more.

- Property Features. If your home has unconventional features like a thatched roof or timber frame, your options may be more limited.

For the most tailored advice, it’s a good idea to consult a qualified mortgage broker. They can help you navigate these factors and find the mortgage that fits your financial needs best.

Can I Remortgage Shared Ownership Home for Debt Consolidation?

Yes, you can remortgage a Shared Ownership property for debt consolidation, but it’s trickier. The pool of lenders willing to offer such remortgages is smaller, making it more challenging to find a suitable offer.

To go ahead, you’ll first need to check the specific terms set by your housing association, as these can vary widely. It’s also good to tell your housing association that you plan to remortgage.

And, of course, working with a mortgage broker can help you locate lenders who are open to offering remortgages on Shared Ownership properties.

Can Bad Credit Affect Debt Consolidation Mortgages?

Having bad credit can complicate your path to securing a mortgage for debt consolidation. Lenders will look at how severe your credit issues are and how long ago they occurred.

While some mortgage providers do cater to individuals with bad credit, these options often come with higher interest rates and stricter terms.

Also, if you’ve missed payments recently or have other issues, many lenders might say no. So, it’s often smart to improve your credit before you apply.

The Bottom Line: How Expert Advice Makes Debt Consolidation Easier

When it comes to debt consolidation through mortgages, expert advice can be a game-changer. An experienced mortgage broker helps you understand the fine print, so there are no unpleasant surprises later.

They can also guide you toward the best deals, saving you money in the long run. These experts can even help you assess if this financial move is the right choice for you, considering factors like your credit history and the terms of any Shared Ownership scheme you might be part of.

Remember, not all lenders are created equal.

Good mortgage brokers have inside knowledge about which lenders are more likely to approve your application.

Having a knowledgeable ally can make the often-confusing process much simpler and stress-free.

So, don’t go it alone. Expert advice is crucial when you’re dealing with something as important as your home and financial future.

Reach out to us now, and we’ll pair you with a mortgage broker who can make the whole process of debt consolidation through mortgages easier and more effective.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Is it a good idea to consolidate debt with a mortgage?

It can be, but it’s not a one-size-fits-all answer. You could end up paying less each month and getting a lower interest rate. However, it also means putting your home at risk if you can’t keep up with the payments.

How can I get rid of debt fast in the UK?

There’s no magic trick, but a solid repayment plan can make a big difference. Cutting expenses, increasing your income, and focusing on high-interest debt first are good strategies. You could also consider debt consolidation to simplify payments.

Will debt consolidation affect my credit score?

In the short term, your credit score may take a small hit when lenders perform necessary checks. However, consolidating your payments into one can improve your long-term credit outlook, provided you keep up with repayments.

Is there a deposit requirement if I get a debt consolidation mortgage?

Yes, most lenders typically require a deposit for a debt consolidation mortgage, often around 15-20% of the property’s value. This could be in the form of equity you’ve built up in your home.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Do I Need To Pay Solicitor Fees When Remortgaging?

Remortgaging your home can be a smart way to reduce your monthly mortgage payments or tap into your property’s equity. But the process isn’t always straightforward. One potential cost that often confuses homeowners is solicitor fees. Do you actually need to pay for a solicitor when remortgaging? Let’s take a closer look. When Do You […]

Unencumbered Mortgage: How To Remortgage a Fully Owned Home?

Owning a property without any debts hanging over it – sounds liberating, doesn’t it? And with that freedom, you might be thinking about the different ways to make the most of your fully paid property. Maybe it’s time to fix up the house or invest in a new opportunity? In this article, we’ll break down […]

How to Remortgage to Buy a Car: A Complete Guide in 2025

Car financing options like auto loans and leasing agreements typically come with scary double-figure interest rates. This coupled with the escalating car costs can discourage you from even dreaming of buying a new vehicle. But whether you’re eyeing a sleek electric sports car or a vintage camper van, getting behind your dream wheels isn’t out […]