- Can I Remortgage to Buy Another Property?

- Who Could Benefit from Remortgaging?

- Property Types You Could Remortgage For

- How Much Equity Can I Remortgage to Buy Another House?

- What Factors Determine Your Eligibility?

- Can I Remortgage to Buy a Second Property in Cash?

- Remortgaging When Relocating

- The Bottom Line

How to Remortgage to Buy Another Property: A 2025 Guide

Using the value of your home can be a smart way to buy another property. If you’ve been paying off your mortgage, you’ve built up equity that’s just waiting to be used.

Through remortgaging, you can unlock this value and put it toward a new investment or even a personal getaway.

In this article, we will walk you through the how-to’s of using a remortgage to easily and efficiently make your next big property move. We also take an in-depth look to help you figure out if this choice fits your financial and personal situation.

Can I Remortgage to Buy Another Property?

Yes, you can.

Remortgaging to buy another property is a viable option, provided you meet the eligibility criteria. This involves refinancing your existing property to raise the funds you need to secure your new home.

However, it’s not just about qualifying for a remortgage.

You must also demonstrate to your mortgage lender that you have the financial capacity to repay the remortgaged mortgage and meet the financial obligations associated with the new property.

If meeting the criteria is not an issue, there are many situations where remortgaging to buy a second home may be appropriate, including:

- Buying a holiday or second home

- Let-to-buy

- Investing in a buy-to-let property

- Remortgaging an existing commercial property

- Using remortgage funds to invest in commercial real estate

- Securing a holiday let

It is always wise to consult with a mortgage advisor to discuss the best options for your circumstances.

Who Could Benefit from Remortgaging?

Remortgaging can be a good option for homeowners with:

- A high income and good credit score.

- A lot of equity in their current home.

- A good understanding of real estate investments.

- A need for more space.

But, it’s important to consider the risks involved before remortgaging, especially if your financial situation is not ideal.

Remortgaging means borrowing more against your property, which you will ultimately have to pay back. It’s important to make sure you can afford your new mortgage payments, even if something goes wrong.

Also, keep in mind that property values can change. If the market slumps, you could be left with negative equity, where your mortgage debt is greater than the value of your property.

If you’re unsure about whether remortgaging is right for you, it’s best to wait until you’re in a more financially stable position.

Here are some additional tips for remortgaging to buy another property:

- Thoroughly assess your financial health and review mortgage terms.

- Take a bird’s-eye view of market conditions.

- Consider working with a dedicated broker to increase your chances of success.

Remortgaging can be a complex process, but it can be a great way to finance the purchase of another property and achieve your financial goals.

For an easy start, enquire with us. We’ll connect you with a remortgage broker to help you with the process and get you the best deal.

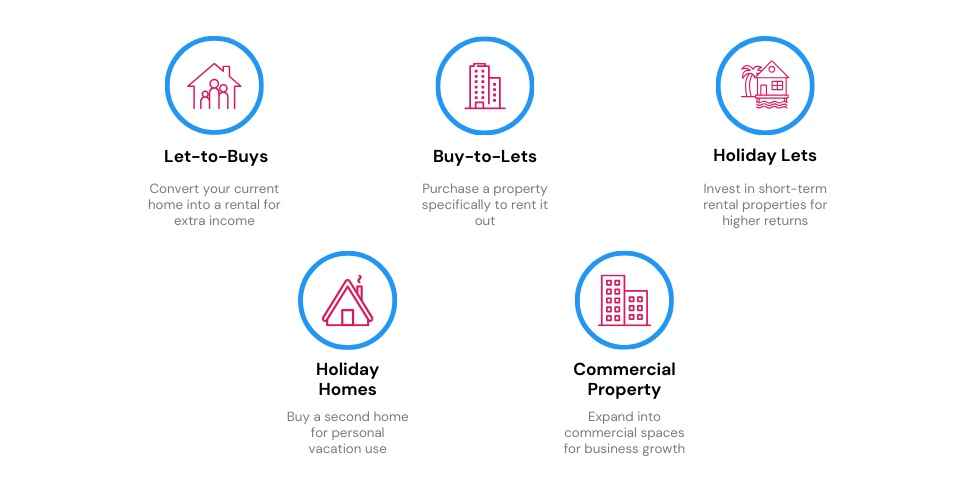

Property Types You Could Remortgage For

People in the UK remortgage for many reasons. It may be to take a leap into the landlord realm and earn passive income, or to buy a blissful retreat where you can leave the worries of the world behind.

The possibilities are endless, so let’s explore the most popular options for remortgaging a property to buy another:

- Let-to-buys – This plan allows you to generate additional income by renting out your current home. Opting for let-to-buys could be extremely cost-effective if you think you need help to handle your new remortgaging costs.

- Buy-to-lets – Alternatively, you could use the funds raised from remortgaging to buy a new property and rent it out.

- Holiday lets – You might want to acquire a property specifically intended for short-term rentals, capitalising on the lucrative market to earn some extra dough.

- Holiday homes and second homes – If you’re looking to create more cherished memories with friends and family, you could use the funds raised through a remortgage to purchase a holiday home.

- Commercial property – You could also use freed-up funds to invest in a shop, an office space, or any other commercial property to create or grow your business.

The type of property you intend to buy and what you’re planning to use it for is an important factor for the success of your remortgage application.

Details are also vital. Lenders might even be interested in the type of construction used in your preferred house. Most lenders prefer brick-and-mortar since anything else is typically considered non-standard.

Also, keep in mind that lenders may have more rigorous selection criteria for certain property types like vacation rentals or commercial properties.

How Much Equity Can I Remortgage to Buy Another House?

How much equity you need depends on your mortgage lender’s remortgage criteria and the amount you want to borrow for your second property (assuming you’re not buying it outright).

To calculate your available equity, subtract the outstanding balance on your current mortgage from your property’s valuation. Remortgaging allows you to tap into this equity.

Use our remortgage calculator below to estimate how much equity you could release to buy another property and see what your new mortgage repayments could be.

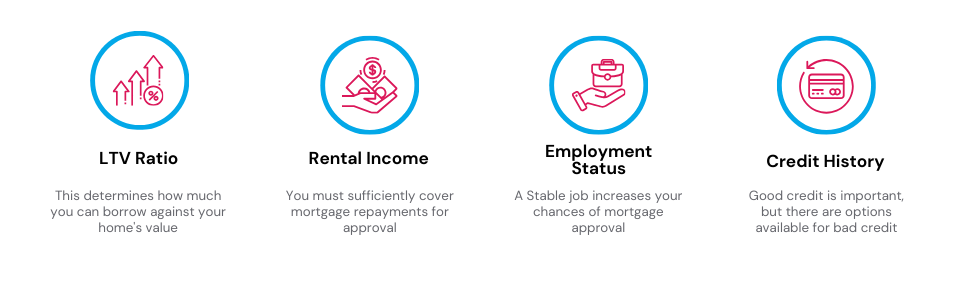

What Factors Determine Your Eligibility?

The Loan-To-Value (LTV) Ratio You Want to Achieve

In remortgaging, your Loan-to-Value (LTV) ratio is an important metric that determines your borrowing power.

The ratio represents the amount of your mortgage secured against your house, stated as a proportion of its worth.

You can calculate your LTV by subtracting the balance of your existing mortgage from the current market value of your house.

The higher your equity, the greater the opportunity to access funds for your new property venture.

The maximum Loan-to-Value (LTV) you can borrow depends on various factors, including your age, credit history, and the purpose of the loan. Let’s break it down:

- For standard residential mortgages, the maximum LTV normally hits 90%. This implies you can borrow up to 90% of the property’s value, with the remaining 10% required as a deposit.

- When it comes to let-to-buy or buy-to-let mortgages, the maximum LTV is often slightly lower at around 85%. This plan can require a higher deposit compared to a standard residential mortgage.

- Holiday let mortgages have a relatively lower maximum LTV, typically ranging from 75% to 80%. You would most probably need to provide a larger deposit compared to both standard residential and let-to-buy mortgages.

These LTV limits are not set in stone and can vary depending on lenders and circumstances.

Remortgage lenders will consider factors such as your financial stability, property type, and rental income potential when determining the maximum LTV they are willing to offer.

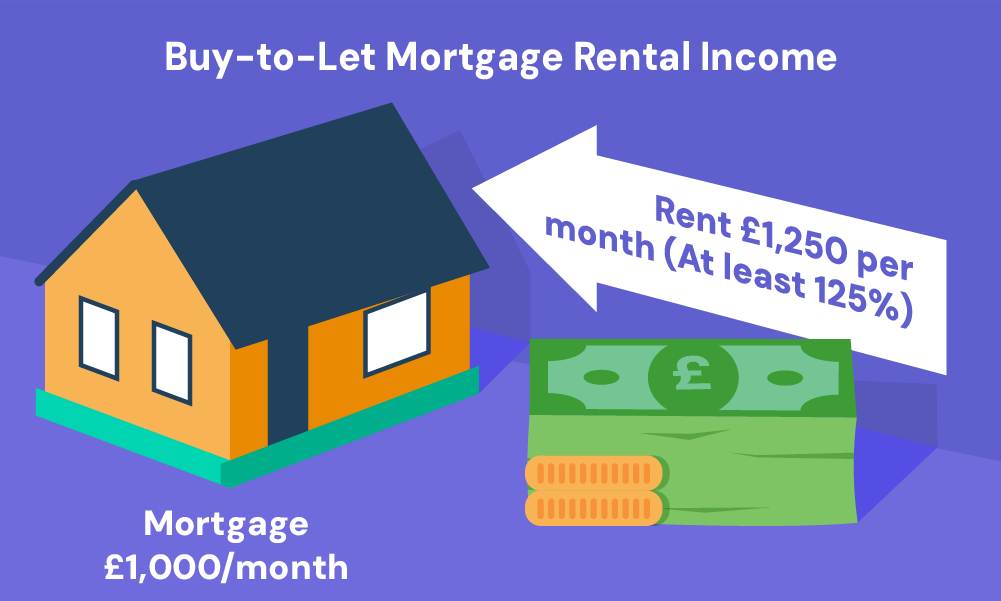

Affordability of Buy-to-Let and Let-to-Buy

When considering a remortgage to buy a second home to rent out, or planning to rent out your existing home through a let-to-buy mortgage, the affordability of the mortgage predominantly depends on the expected rental income of the property, among other criteria.

In the case of a buy-to-let mortgage, it is generally expected that the rental income will cover a substantial portion of the mortgage repayments.

The exact percentage varies between mortgage lenders, but typically, you would be looking at a range of about 125-145%.

Whether You Have Stable Employment

When it comes to remortgaging a property to buy another, your employment status plays a key role.

While many lenders prefer full-time workers, some focus exclusively on serving the needs of independent contractors.

Your salary is a major factor in figuring out the size of your mortgage. Lenders normally follow a set rule that permits mortgages up to 4 times your salary.

But others are ready to contemplate greater ratios, with some willing to go as high as five or six times (5x – 6x) your income.

It’s important to understand that income consists of more than just your wage. Lenders take a thorough view of your annual earnings, taking into account all sources.

This can include consistent bonuses, dividends, tax credits, and even child benefit payments.

No matter where your income comes from, it’s vital to demonstrate your ability to meet your financial obligations.

Whether You Have Bad Credit and Outstanding Debts

Applying for a mortgage with a history of bad credit can be challenging, but there are specialist mortgage lenders who can help people in this situation.

These lenders consider various factors, such as the age, severity, and reasons behind your bad credit history, to create deals that are tailored to your specific circumstances.

A knowledgeable mortgage broker can help you find these lenders.

It is worth noting that existing loans and credit card debts are only considered to be bad credit if they include missed payments.

However, having a big amount of debt in either category could potentially affect your borrowing capacity, especially if lenders doubt your ability to manage debt repayments alongside your mortgage commitments.

>> More about Remortgaging with Bad Credit

Can I Remortgage to Buy a Second Property in Cash?

Yes, it is possible to buy another property in cash with a remortgage if you can raise enough money by remortgaging your current home.

You may even find that maximising the borrowing on your existing mortgage could be cheaper than taking out a buy-to-let or second-home mortgage.

However, if you cannot raise enough money to buy the next property outright, you may need to get another mortgage.

The type of mortgage you choose will depend on your plans for the property. For example, if you plan to rent out the property, you should look into buy-to-let mortgages.

There are also specialist mortgages available if you plan to use the property as a holiday home or second residence.

Remortgaging When Relocating

It is possible to move to a new home without selling your current property. Many lenders offer let-to-buy mortgages.

This allows borrowers to rent out their current property to tenants while raising the money they need for a new home purchase or deposit.

Additionally, if your existing mortgage has good rates, you may be able to transfer your mortgage to the new property, which is known as mortgage porting.

The Bottom Line

Remortgaging can offer an extremely practical approach to buying different types of properties. Whether it’s providing more space to your growing family or investing in lucrative holiday lets, the strategy can help you bring your real estate aspirations to life.

But with so many lenders out there, you’ll need to gather your wits to find the best available deal. It’s essential to compare the terms, fees, and interest rates on offer. Don’t settle for the first deal that comes your way—shop around like a seasoned bargain hunter!

To help you on the way, it’s generally wise to consult professional remortgage brokers who scrutinise the best deals on the market. These guys boast exceptional expertise and exclusive connections with lenders to help you find a perfect match. Research is your secret power for cutting straight through the fluff and partnering with real pros.

Still puzzled about remortgaging property to buy another? Drop us a line and we’ll match you with a remortgage broker to get you in the groove.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What is the difference between remortgaging and a second-charge mortgage?

Remortgaging means replacing your existing mortgage with a new one. This can be a good option if you want to switch to a better deal, but it usually involves additional costs such as legal, valuation, and arrangement fees.

A second-charge mortgage is a separate loan that is secured against your home. This means that you can borrow more money without having to remortgage your entire home. This can be a good option if you don’t have enough equity in your home to cover the down payment on a second property, but the interest rates are usually higher than those for remortgaging.

What are the benefits and risks of remortgaging to buy another property?

Benefits:

- Access a large sum of money without selling your current home.

- Potentially get a lower interest rate than on a new mortgage.

- Consolidate your debts into one monthly repayment.

- Potentially increase your borrowing capacity.

- Release equity to use for other purposes related to the purchase of the second property, such as a down payment, closing costs, or renovations.

Risks:

- Pay additional costs, such as legal, valuation, and arrangement fees.

- Be more exposed to the housing market, as you will have two properties instead of one.

- Be left with negative equity if the value of your properties falls.

- Have difficulty repaying your mortgage if your financial circumstances change.

- Be liable for stamp duty on your second property.

Are there any penalties for remortgaging?

There might be early repayment charges or exit fees associated with your current mortgage. These charges vary depending on your mortgage agreement, so it’s essential to check with your lender to see if there are any penalties.

Can I remortgage multiple properties?

Yes, you can remortgage multiple properties. However, it is important to note that each lender will have its own criteria for remortgaging multiple properties. Some lenders may be more willing to lend to borrowers with multiple properties, while others may be more cautious.

Here are some factors that lenders will consider when deciding whether to approve a remortgage for multiple properties:

- Your credit score

- Your income and debt-to-income ratio

- The amount of equity you have in your properties

- The loan-to-value (LTV) ratio of your proposed remortgage(s)

- The type of properties you are remortgaging

If you are considering remortgaging multiple properties, it is important to compare offers from multiple lenders to find the best deal. You should also seek professional mortgage advice to ensure that remortgaging is the right option for you.

Can I remortgage if I work part-time?

As long as you prove you can comfortably afford the mortgage payments, working part-time should not be a hindrance. It’s crucial to list any additional sources of income to strengthen your case, such as returns on investments, regular overtime, and bonuses.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Do I Need To Pay Solicitor Fees When Remortgaging?

Remortgaging your home can be a smart way to reduce your monthly mortgage payments or tap into your property’s equity. But the process isn’t always straightforward. One potential cost that often confuses homeowners is solicitor fees. Do you actually need to pay for a solicitor when remortgaging? Let’s take a closer look. When Do You […]

Unencumbered Mortgage: How To Remortgage a Fully Owned Home?

Owning a property without any debts hanging over it – sounds liberating, doesn’t it? And with that freedom, you might be thinking about the different ways to make the most of your fully paid property. Maybe it’s time to fix up the house or invest in a new opportunity? In this article, we’ll break down […]

How to Remortgage to Buy a Car: A Complete Guide in 2025

Car financing options like auto loans and leasing agreements typically come with scary double-figure interest rates. This coupled with the escalating car costs can discourage you from even dreaming of buying a new vehicle. But whether you’re eyeing a sleek electric sports car or a vintage camper van, getting behind your dream wheels isn’t out […]