- Can You Secure a £30,000 Loan?

- What Will Your Monthly Repayments Be on a £30,000 Loan?

- How Much Will a £30,000 Loan Cost You in the End?

- Should You Choose a Secured or Unsecured £30,000 Loan?

- What Are the Best Uses for a £30,000 Loan?

- What Should You Know About Interest Rates?

- What Do You Need for Your Loan Application?

- What Credit Score Do You Need to Secure a £30,000 Loan?

- Can I Get a £30,000 Loan with Bad Credit?

- How To Get Approved For a £30,000 Loan?

- How to Choose the Best £30,000 Loan?

- The Bottom Line

How To Get A £30,000 Loan Successfully?

Taking out a £30,000 secured loan is a major decision. But, it could be a game-change for someone like you, looking to reach your personal and professional goals.

You might be considering upgrading your home or starting your own business. Regardless, you’ll need some CLEAR information on this topic

This guide will walk you through everything you need to know about securing a £30,000 loan and how to successfully navigate the process in the UK.

Can You Secure a £30,000 Loan?

Yes you can.

Securing a £30,000 loan is a possibility, provided you successfully meet the criteria outlined by the lenders.

Keep in mind, since £30,000 is a large amount to borrow, you might be required to present a guarantor or some form of security during your application process.

Having a strong credit history can also be a beneficial factor.

Whether you intend to consolidate debts or undertake home renovations, a £30,000 financial boost can significantly change your circumstances.

Nevertheless, it’s vital to be cautious, as even a slight variance in the interest rate can influence the total amount you’ll repay, particularly if you opt for a prolonged repayment term.

Therefore, securing a loan that aligns with your specific requirements is essential.

What Will Your Monthly Repayments Be on a £30,000 Loan?

Determining your monthly repayments for a £30,000 loan involves several factors. Lenders generally consider your credit score, the loan term, and the interest rate when calculating your monthly dues.

A higher rate escalates the interest you’ll need to cover. Meanwhile, extending your loan term reduces your monthly payments but increases the total interest you’ll incur.

To get an initial grasp, you can try using the secured loan calculator. It provides an estimate of what your monthly repayments might be.

While these figures provide an estimate, it’s wise to consult with a financial advisor who can help you grasp the full picture, inclusive of all potential fees and costs.

This way, you can make an informed decision that aligns well with your financial goals and circumstances.

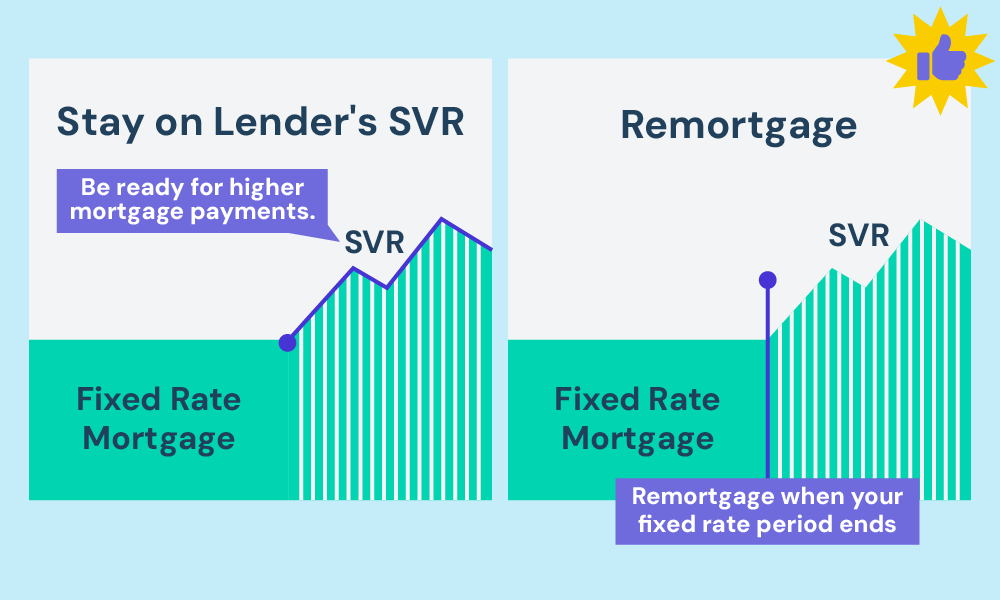

How Much Will a £30,000 Loan Cost You in the End?

Borrowing £30,000 is a big decision, so it’s helpful to know what your payments might look like during the first few years.

Most loans in the UK start with a fixed interest rate for a set period—usually around 2 to 5 years.

During this time, your monthly payments stay the same, making it easier to plan your budget.

Here’s an example of what your monthly repayments and total costs could look like during a 5-year fixed-rate period at different interest rates:

| Fixed Interest Rate (%) | Monthly Repayment | Total Repayment |

|---|---|---|

| 5% | £556 | £33,960 |

| 7% | £594 | £35,640 |

| 10% | £637 | £38,220 |

After the fixed-rate period ends, your payments might go up or down if you move to your lender’s standard variable rate (SVR) or remortgage to a new deal.

Keep in mind, these numbers are only examples to help you understand how costs can vary depending on the interest rate.

Your actual payments and total costs will depend on your financial situation and the lender’s requirements.

Always check with your lender or a financial advisor to get personalised advice and accurate estimates.

Should You Choose a Secured or Unsecured £30,000 Loan?

Deciding between a secured or an unsecured loan is vital, especially when you’re eyeing a substantial amount like £30,000. It’s relatively common to find unsecured loans offering up to a £25,000 limit.

But, if you have a goodcredit score, you might spot lenders willing to provide up to £30,000 or even £35,000 as an unsecured loan.

In case your credit score isn’t in the excellent range, considering a secured loan would be wise. This kind of loan demands you to use a valuable asset, typically your home, as a guarantee that you will repay the loan.

If you already have a mortgage, this secured loan would be a secondary charge, meaning the lender could claim the value from your property if, unfortunately, you cannot repay the loan.

What Are the Best Uses for a £30,000 Loan?

The beauty of a £30,000 loan is its versatility; it can cater to a plethora of needs and desires, including:

For Personal and Business Goals

Whether you’re nurturing a personal dream or aiming to kickstart a business venture, a £30,000 loan can be your ally. Imagine not having to postpone your plans because of a financial constraint. You can:

- Boost Your Education. Enhance your knowledge or learn a new skill set to climb up the career ladder.

- Home or Vehicle Purchase. Acquire a comfortable home or a car without depleting your savings.

- Venture into Business. Have a business idea simmering in your mind? This loan can serve as the initial capital to set the wheels in motion.

And guess what? You can even splurge on that luxurious vacation or dream wedding you’ve always envisioned!

Ever wished to revamp your living space? A £30,000 loan can make this possible.

From adding a sparkling new bathroom to extending your living space, this loan can be a conduit to enhance the aesthetic and monetary value of your home.

Moreover, you can promptly address urgent repairs without denting your wallet significantly.

Juggling multiple debts can be a nerve-wracking experience. Fortunately, a £30,000 loan can be a solution.

It allows you to consolidate different high-interest debts into one, offering you the convenience of a single monthly payment and potentially lowering your overall interest expenditure.

In essence, it offers a simplified and more manageable approach to debt repayment, easing your financial strain.

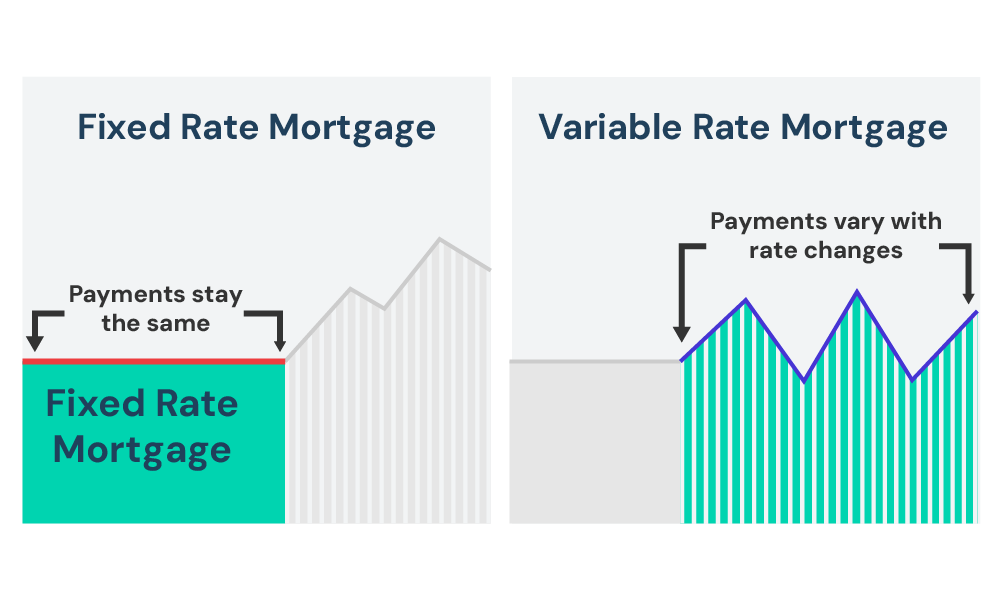

What Should You Know About Interest Rates?

Interest rates are essentially the cost of borrowing money, and it’s crucial to understand how it works before you settle on a £30,000 loan. There are mainly two types you’ll come across:

Fixed Interest Rates – This type of interest rate remains unchanged throughout the loan term. It means your monthly payments will be predictable, allowing you to budget more effectively without worrying about fluctuations.

Variable Interest Rates – Unlike fixed rates, variable rates can change over time, usually based on an underlying benchmark interest rate or index that fluctuates. While this might potentially offer you lower initial payments, remember that your monthly payment can increase, sometimes significantly, if the interest rates rise.

What Do You Need for Your Loan Application?

If you’re applying for a £30,000 loan, here’s a checklist of essential documents you may need, but remember, the requirements might vary depending on the lender:

- Proof of Income – Usually your recent payslips or income statements to confirm your earnings.

- Credit Reports – These show your financial history and will help the lender assess your creditworthiness.

- Personal Identification – You’d need documents like your ID or utility bills to confirm your identity and residence.

Having these documents on hand can help speed up the loan application process and bring you one step closer to obtaining your loan.

What Credit Score Do You Need to Secure a £30,000 Loan?

Getting your hands on a £30,000 loan is a big step, and to do that, you’ll usually need to have a sparkling credit score.

This kind of loan is quite a hefty amount when we talk about personal unsecured loans. If you have a good credit score, lenders will be more likely to trust you with this large amount.

But don’t worry too much if your credit score isn’t top-notch. You can still have a shot at getting that loan if you’re willing to use your home as a security net.

This way, even if your credit score isn’t the best, you can still get approved for a £30,000 loan. But remember, if things don’t go as planned and you miss your repayments, you might lose your home.

So, tread carefully.

Can I Get a £30,000 Loan with Bad Credit?

Getting approved for a £30,000 loan might seem a bit of a stretch if your credit score is less than stellar.

But, not all hope is lost.

Several UK lenders are more understanding and willing to consider your application, even if your financial past includes late payments, defaults, or County Court judgments (CCJs).

Lenders specialising in bad credit loans focus more on your current financial status rather than your past.

They are keen on understanding your existing income and expenditure pattern to gauge your repayment capacity.

It’s vital to prepare yourself to discuss your current financial standing candidly when applying with bad credit.

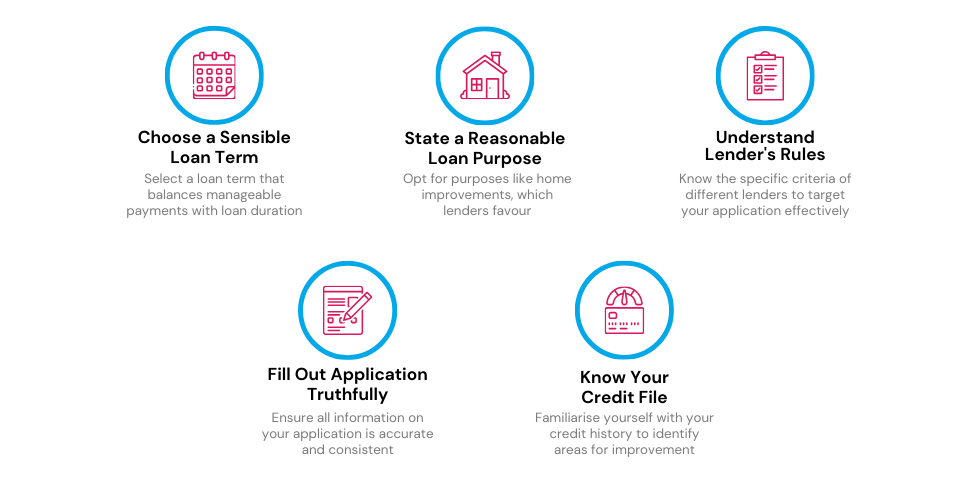

How To Get Approved For a £30,000 Loan?

Securing a £30,000 loan is a significant financial move.

If you’re aiming to see that hefty amount in your bank account soon, here are some insider tips and strategies to enhance your chances of approval:

- Choose a Sensible Loan Term. It’s all about finding the perfect balance – a term that allows you to manage your monthly payments comfortably without prolonging the loan period unnecessarily.

- State a Reasonable Purpose for Your Loan. When discussing your loan purpose with potential lenders, be sure to keep it sensible. Opt for reasons like home improvements or debt consolidation that are typically viewed more favourably by lenders.

- Understand the Lender’s Rules. Save yourself time and frustration by understanding the unique rules of different lenders. It will help you steer clear of lenders who might not entertain your application due to their specific criteria.

- Fill Out Your Application Truthfully. Maintain consistency and truthfulness when filling out your application to avoid any red flags that might arise due to discrepancies between your application and your credit file.

- Know Your Credit File Inside and Out. Get ahead by familiarising yourself with your credit file. Understanding it can be your first step towards making improvements that could enhance your loan approval chances.

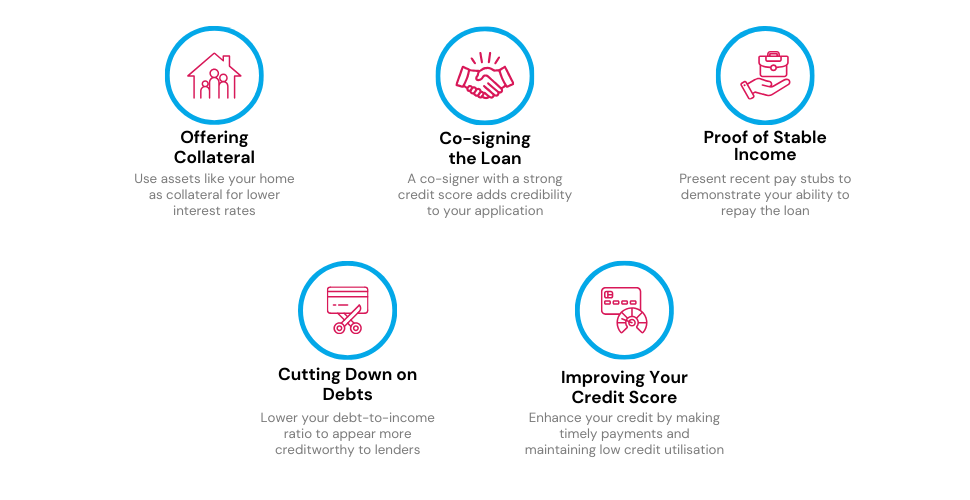

In addition to these, consider adopting the following strategic moves to bolster your loan application and possibly secure a loan with more favourable terms:

- Offering Collateral. Boost your chances by offering a valuable asset, like your home, as collateral. It not only reassures lenders of your commitment to repaying the loan but also might fetch you a loan with a lower interest rate.

- Co-signing the Loan. Having a co-signer with an excellent credit score can considerably uplift your application. A co-signer provides an extra layer of assurance to the lender, promising to cover the loan if you default.

- Providing Proof of Stable Income. Demonstrate your financial stability by presenting recent pay stubs or income statements. It helps in showcasing your capability to manage loan repayments efficiently.

- Cutting Down on Other Debts. Enhance your debt-to-income ratio by reducing existing debts before applying for a new loan. A favourable ratio is a significant green signal to lenders.

- Improving Your Credit Score. Every point counts when it comes to credit scores. Work towards enhancing your score by adopting responsible financial habits such as timely bill payments and not exhausting your credit card limits.

By following these comprehensive steps and strategies, you’re positioning yourself as a strong candidate for securing the £30,000 loan you desire, without straining your finances. Good luck!

How to Choose the Best £30,000 Loan?

While on the hunt for that perfect £30,000 loan, keep these factors in mind to make an informed choice:

- Interest Rate – Remember, the advertised APR might not be what you get. Lenders only need to offer this to 51% of applicants. Your actual rate could be higher, depending on your creditworthiness.

- Total Amount Payable – This is the sum of the loan amount and all the interest you’ll pay over the loan term.

- Term Length – Look for a lender offering a variety of term lengths. Keep in mind, that a longer term means higher interest charges.

- Fees – While setup fees aren’t common for unsecured personal loans, homeowner loans usually come with them. Make sure to factor this into your total cost.

- Eligibility – Understand the lender’s criteria before you apply to avoid disappointment.

The Bottom Line

Securing a £30,000 loan is a notable financial milestone.

While the journey might seem daunting, adopting the right strategies and being prepared can greatly smooth the path ahead.

Remember, the key is to present yourself as a responsible and capable borrower. Furthermore, don’t hesitate to lean on the expertise of a reliable broker.

So, as you step into this significant phase, arm yourself with knowledge and choose the right aid to navigate through the process with ease.

Ready to take the leap? Fill out this quick form, and we’ll connect you with a broker to help you get the best deal for a £30,000 loan in the UK.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Is it hard to get a £30,000 loan?

Getting a £30,000 loan can be difficult or easy, depending on your credit score, income stability, and the lender’s criteria. A high credit score and stable income will make it easier to get a loan. However, it is advisable to research and prepare to meet the specific requirements of potential lenders.

Is it possible to consolidate £30,000 of debt?

Yes, many lenders approve loans for debt consolidation. Ensure you can manage the new repayments, and be aware that you might pay more in total interest over time.

Can I secure an unsecured personal loan of £30,000?

Yes, more lenders, including some mainstream ones, now offer such loans. Your approval odds depend on your credit score and financial stability.

How long would it take to pay back a 30,000 loan?

The time it takes to pay back a £30,000 loan depends on the terms agreed with the lender. Loan terms typically range from short-term (1-3 years) to medium-term (3-7 years) to long-term (7 years and above).

It is important to choose a term that you can afford to repay regularly without straining your budget. Some loans offer repayment flexibility, allowing you to pay it off early and potentially save money on interest.

Is it possible to secure a £30k loan for business purposes?

Yes, obtaining a £30k business loan is certainly possible, though it often requires approaching specialist lenders focused on business loans. Many personal loans have stipulations that prevent the funds from being used for business ventures. It’s important to communicate the purpose of the loan clearly to find the right type of loan and lender for your business needs.

Related Articles

Secured Loan Calculator – No Personal Details Required

If you’re sitting on a valuable asset like a home, why not put it to work for you? Secured loans can open doors to more funds, better repayment terms, and even loan approval when all other avenues fail. But remember, there’s a flip side: you could lose your prized asset if you don’t keep up […]

Loans for Pensioners: How to Get the Cash You Need?

Suppose you’ve reached retirement and find that, despite having assets in property or a robust pension plan, your daily cash flow isn’t quite as fluid. In that case, you may contemplate taking out a loan for things like home renovations, a new car, or even a well-deserved holiday. And why not? If you have a […]

How To Get a Secured Loan If You’re Self Employed

Starting a business takes courage, hard work, and, let’s be honest, money. Whether you want to launch a new product, buy better tools, or make your workspace bigger, a secured loan could help you make it happen. Finding a loan when you don’t have a regular job can feel tricky. But here’s the good news: […]